|

시장보고서

상품코드

2062003

메탄 설폰산 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Methane Sulfonic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

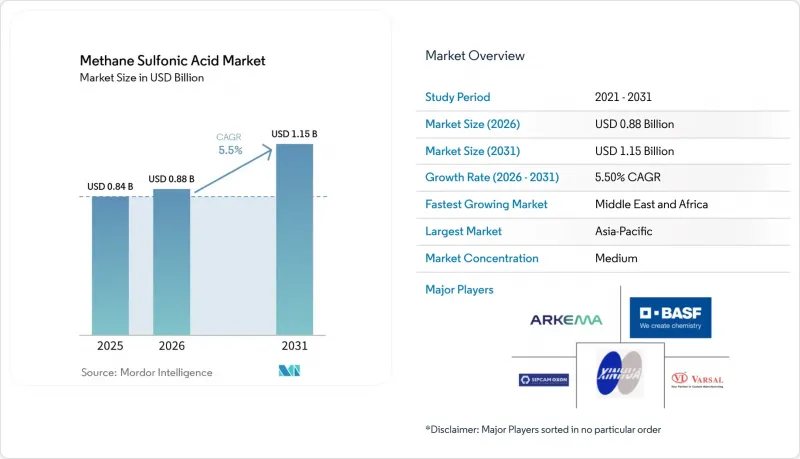

Mordor Intelligence에 의하면, 메탄 설폰산 시장 규모는 2025년 8억 4,000만 달러에서 2026년에는 8억 8,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.5%로 성장을 지속하여, 2031년까지 11억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 등급/순도(기술 등급, 전자용 등급 등), 형태(액체, 고체/플레이크), 최종 이용 산업(금속 마감 및 전기도금, 의약품 및 생화학 처리 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 메탄 설폰산 시장 동향 및 분석

전기도금 및 금속 표면 처리 분야 수요 증가

자동차의 경량화와 전자기기의 소형화로 인해 주석 및 귀금속 도금 수요가 증가하고 있으며, 메탄 설폰산 도금욕은 황산계 시스템에 비해 수소 발생이 적어 더 뛰어난 피복력을 발휘합니다. 광둥성과 대만의 인쇄회로기판 제조업체들은 메탄 설폰산이 고농도 주석 환경에서도 용해성을 유지하여 도금욕의 수명을 연장함으로써, 미세 피치 도금을 유지하고 있습니다. 자동차 업계의 1차 공급업체들은 크로메이트 코팅층을 사용하지 않고도 ISO 9227 염수 분무 시험의 내구성 기준을 충족하기 위해 알루미늄 배터리 케이스에 메탄설포네이트계 코팅을 적용하고 있습니다. 또한, 메탄 설폰산(MSA)의 비산화성 덕분에 기판에 대한 부식이 최소화됩니다. 이러한 성능 향상으로 인해 양산 시 불량률이 감소했으며, 장식용 및 기능성 코팅 분야 모두에서 메탄 설폰산 시장이 확대되고 있습니다.

제약 및 특수 합성 분야에서의 용도 확대

펩타이드 API 제조업체는 포름산에 2%의 메탄 설폰산을 함유한 PFAS 무첨가 전 세계적 탈보호 칵테일을 검증했습니다. 이를 통해 트리플루오로아세트산에 비해 강산 사용량을 98% 줄였으며, 모델 서열에서 99%의 절단율을 달성했습니다. 전체 길이의 틸제파티드는 TFA 워크플로우와 동등한 순도를 달성하고 있으며, 전 세계 생산량 증가에 따라 톤 단위의 GLP-1 작용제 제조에서 MSA가 중요한 위치를 차지하게 되었습니다. 가역적인 포르밀화 부반응은 온화한 수산화암모늄 세척을 통해 제거되며, 진공 증류를 통해 MSA의 88%를 회수하여 재순환할 수 있으므로 환경적 및 경제적 이점이 강화되었습니다.

부식성 및 취급 시 위험

MSA는 H314 위험성 분류를 받았으며, 내산성 장갑, 고글 및 밀폐형 이송 시스템의 사용이 요구됩니다. 일반적인 스테인리스 스틸은 80°C 이상에서 부식되기 때문에 사용자는 듀얼 페이즈 강이나 특수 합금으로 전환할 수밖에 없어 설비 투자 부담이 커집니다. 물질별로 정해진 OSHA 기준치가 없기 때문에 규정 준수 관련 문서 작성이 복잡해지고 있으며, 특히 전담 산업위생 담당자가 없는 소규모 도금 업체나 위탁 가공 업체에게는 큰 과제가 되고 있습니다.

부문별 분석

2025년에는 기존의 전기도금 및 세정 용도가 여전히 생산량의 대부분을 차지하는 가운데, 테크니컬 등급이 매출의 45.55%를 차지했습니다. 전자 및 의약품 등급은 합쳐서 약 35%의 시장 점유율을 차지하며, 낮은 염화물 및 전이금속 함량이 요구되는 PCB 도금 및 펩타이드 API에 공급되고 있습니다. 차세대 반도체 노드에서는 철 및 구리의 오염 물질 기준이 1ppm 미만으로 강화됨에 따라, 초고순도 등급이 연평균 성장률(CAGR) 6.56%로 가장 빠른 성장세를 보일 것으로 전망됩니다. 증류 및 이온 교환 정제 공정에 대한 공급업체들의 투자로 공급량이 증가함에 따라, 팹 사업자들 간의 메탄 설폰산 시장이 확대되고 있습니다.

인공지능 가속기 및 자동차용 파워 모듈용 칩 수요가 증가함에 따라 주석 및 주석-은 합금의 침전량이 늘어나면서, 전자 등급 MSA에 대한 수요가 확대되고 있습니다. 의약품 등급의 경우, 규제 당국의 PFAS(퍼플루오로알킬 물질)에 대한 규제가 강화됨에 따라 제조업체들이 트리플루오로아세트산 대체를 추진하게 되어 수요가 더욱 증가할 것으로 예측됩니다. 기술 등급의 경우, 황산으로 충분한 용도가 있는 분야에서는 이익률 압박에 직면하고 있지만, 습식 야금이나 희토류 재활용 분야에서는 여전히 금속 메탄 설폰산의 높은 용해성이 중요하게 여겨지고 있습니다.

지역별 분석

2025년 매출의 54.25%를 아시아태평양이 차지했으며, 광둥성과 장쑤성의 중국 전기도금 거점, 하이데라바드와 아메다바드 주변의 인도 펩타이드 산업 회랑, 그리고 한국의 반도체 투자가 이를 견인했습니다. 중국의 ‘이산화탄소 배출 정점 달성 및 탄소 중립’ 로드맵은 생분해성 특수 산 및 폐쇄형 배터리 전해액을 장려함으로써 구조적인 수요를 강화하고 있습니다.

북미는 2025년에 상당한 시장 점유율을 차지했으며, 보스턴 지역의 펩타이드 CDMO, 중서부 지역의 자동차 도금 업체, 그리고 캘리포니아주와 텍사스주에서의 흐름전지 초기 도입이 이를 뒷받침했습니다. 2026년에 발표된 하이드라이트 케미컬사의 사우스캐롤라이나주 내 6,300만 달러 규모의 공장은 남동부 지역의 자동차 및 전자 산업 클러스터에 현지 공급을 보장하는 것입니다. 유럽은 약 18%를 차지하며, 독일 루트비히스하펜의 화학 단지 및 스칸디나비아의 청정 수소 프로젝트가 그 핵심을 이루고 있습니다. 한편, 프랑스와 벨기에의 제약 거점들은 PFAS에서 벗어나기 위해 MSA를 도입하고 있습니다.

중동 및 아프리카는 사우디아라비아와 아랍에미리트(UAE)의 하류 부문 확장에 따라 특수산이 다각화된 석유화학 산업 체인에 통합됨에 따라, 지역별로는 가장 높은 연평균 성장률(CAGR) 6.66%를 나타낼 것으로 전망됩니다. 알주베일과 아부다비에 대한 투자는 원료의 안정적인 공급을 확보하고, 도금 및 배터리 제조업체를 걸프 지역으로 유치하고 있습니다. 남미는 8%의 점유율로 안정적인 모습을 보이고 있으며, 브라질의 사탕수수 정제소에서는 리그노셀룰로오스 전처리에 MSA가 사용되고 있고, 아르헨티나에서는 메탄 설폰산을 이용한 리튬 추출 시범 사업이 진행되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the methane sulfonic acid market size is expected to grow from USD 0.84 billion in 2025 to USD 0.88 billion in 2026 and is forecast to reach USD 1.15 billion by 2031 at 5.5% CAGR over 2026-2031.

This report is Segmented by Grade/Purity (Technical Grade, Electronic Grade, and More), Form (Liquid, and Solid/Flakes), End-Use Industry (Metal Finishing and Electro-Plating, Pharmaceuticals and Biochemical Processing, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Methane Sulfonic Acid Market Trends and Insights

Growing Demand in Electroplating and Metal Finishing

Automotive lightweighting and electronics miniaturization lift tin and precious-metal plating volumes, and methanesulfonic acid baths deliver higher throwing power alongside lower hydrogen evolution than sulfuric systems. Printed-circuit board fabricators in Guangdong and Taiwan maintain fine-pitch deposits because methanesulfonate salts stay soluble at elevated tin concentrations, extending bath life. Tier-1 automotive suppliers coat aluminum battery enclosures to reach ISO 9227 salt-spray durability without chromate layers, and MSA's non-oxidizing nature minimizes substrate attack. These performance gains reduce reject rates in volume production, broadening the methane sulfonic acid market across both decorative and functional coatings.

Expanding Use in Pharmaceutical and Specialty Synthesis

Peptide API producers have validated a PFAS-free global deprotection cocktail containing 2% methanesulfonic acid in formic acid, cutting strong-acid use 98% versus trifluoroacetic acid and yielding 99% cleavage for model sequences. Full-length tirzepatide achieved comparable purity to TFA workflows, positioning MSA for ton-scale GLP-1 agonist manufacture as global output climbs. Reversible formylation side reactions are cleared by mild ammonium hydroxide washes, and vacuum distillation recovers 88% of MSA for circular reuse, strengthening environmental and economic cases.

Corrosiveness and Occupational Handling Risks

MSA carries H314 hazard classification and requires acid-resistant gloves, goggles, and enclosed transfer systems. Standard stainless grades corrode above 80 °C, pushing users toward duplex steels or exotic alloys that raise capital outlays. Absence of substance-specific OSHA limits complicates compliance documentation, particularly for small platers and job shops that lack dedicated industrial hygiene staff.

Other drivers and restraints analyzed in the detailed report include:

- Adoption in Flow-Battery and Hydrogen Fuel-Cell Electrolytes

- Catalyst Role in Biomass-Derived Fuel Refining

- Price Competition from Sulfuric and P-Toluenesulfonic Acids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Technical grade commanded 45.55% revenue in 2025 as legacy electroplating and cleaning continued to dominate volumes. Electronic and pharma grades together held around 35% share, serving PCB plating and peptide APIs that demand low chloride and transition-metal levels. Ultra-high-purity is projected to record the fastest advance at 6.56% CAGR because next-generation semiconductor nodes tighten contaminant limits to below 1 ppm for iron and copper. Supplier investments in distillation and ion-exchange polishing raise availability, enlarging the methane sulfonic acid market among fab operators.

Rising chip demand for artificial intelligence accelerators and automotive power modules boosts tin and tin-silver deposition, reinforcing pull for electronic-grade MSA. Pharma Grade receives additional lift as regulators tighten PFAS limits, encouraging manufacturers to switch from trifluoroacetic acid. Technical Grade faces margin pressure where sulfuric acid remains adequate, but hydrometallurgy and rare-earth recycling still value high metal-methanesulfonate solubility.

Geography Analysis

Asia-Pacific controlled 54.25% of 2025 revenue, led by Chinese electroplating hubs in Guangdong and Jiangsu, India's peptide corridors around Hyderabad and Ahmedabad, and Korean semiconductor investments. China's dual-carbon roadmap favors biodegradable specialty acids and closed-loop battery electrolytes, reinforcing structural demand.

North America accounted for significant market share in 2025, underpinned by Boston-area peptide CDMOs, Midwestern automotive platers and early flow-battery deployments in California and Texas. Hydrite Chemical's USD 63 million plant in South Carolina, announced in 2026, promises local supply for Southeast vehicle and electronics clusters. Europe held roughly 18%, anchored by Germany's chemical complex at Ludwigshafen and Scandinavia's green hydrogen projects, while pharmaceutical hubs in France and Belgium adopt MSA to exit PFAS.

The Middle East and Africa is projected to clock the fastest regional CAGR at 6.66% as Saudi and Emirati downstream expansions integrate specialty acids into diversified petrochemical chains. Al-Jubail and Abu Dhabi investments improve feedstock security and draw plating and battery makers to the Gulf. South America's 8% slice is stable, with Brazil's sugarcane refineries using MSA in lignocellulosic pretreatment and Argentina piloting methanesulfonate-based lithium extraction.

- Arkema

- BASF

- Central Drug House

- Chemos

- Haihang Industry

- Helsa-Chemie

- Hydrite Chemical

- Kanto Chemical

- Kao Corporation

- Nanjing Chemical Material Corp.

- Shandong Xinhua Pharma

- SHINYA CHEM

- Sipcam Oxon Spa

- Solvay Fluor & Derivatives

- Varsal

- Tokyo Chemical Industry

- Xingrui Industry

- Yingrui Industry Development

- Zibo DeHong Chemical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand in electroplating and metal finishing

- 4.2.2 Expanding use in pharmaceutical and specialty synthesis

- 4.2.3 Adoption in flow-battery and hydrogen fuel-cell electrolytes

- 4.2.4 Catalyst role in biomass-derived fuel refining

- 4.2.5 Circular economy push for electrolyte recycling

- 4.3 Market Restraints

- 4.3.1 Corrosiveness and occupational handling risks

- 4.3.2 Price competition from sulfuric and p-toluenesulfonic acids

- 4.3.3 Regulatory classification gaps for battery-grade MSA

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade/Purity

- 5.1.1 Technical Grade (70-99%)

- 5.1.2 Electronic Grade (>= 99.9%)

- 5.1.3 Pharma Grade (>= 99.5%)

- 5.1.4 Ultra-High-Purity (>= 99.99%)

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid/Flakes

- 5.3 By End-use Industry

- 5.3.1 Metal Finishing and Electro-plating

- 5.3.1.1 Precious-metal plating

- 5.3.1.2 Printed-circuit-board plating

- 5.3.1.3 Automotive components

- 5.3.2 Pharmaceuticals and Biochemical Processing

- 5.3.3 Energy Storage and Hydrogen Production

- 5.3.3.1 Vanadium-redox flow batteries

- 5.3.3.2 PEM fuel cells

- 5.3.4 Industrial and Fine-Chemical Catalysis

- 5.3.5 Electronics Cleaning and Etching

- 5.3.6 Other Specialty Applications

- 5.3.1 Metal Finishing and Electro-plating

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle-East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 BASF

- 6.4.3 Central Drug House

- 6.4.4 Chemos

- 6.4.5 Haihang Industry

- 6.4.6 Helsa-Chemie

- 6.4.7 Hydrite Chemical

- 6.4.8 Kanto Chemical

- 6.4.9 Kao Corporation

- 6.4.10 Nanjing Chemical Material Corp.

- 6.4.11 Shandong Xinhua Pharma

- 6.4.12 SHINYA CHEM

- 6.4.13 Sipcam Oxon Spa

- 6.4.14 Solvay Fluor & Derivatives

- 6.4.15 Varsal

- 6.4.16 Tokyo Chemical Industry

- 6.4.17 Xingrui Industry

- 6.4.18 Yingrui Industry Development

- 6.4.19 Zibo DeHong Chemical

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment