|

시장보고서

상품코드

2062007

사료용 지방 및 단백질 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Feed Fats And Proteins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

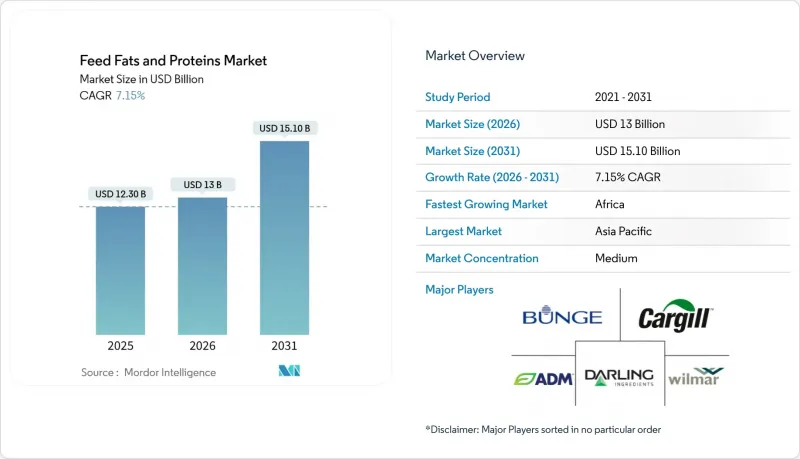

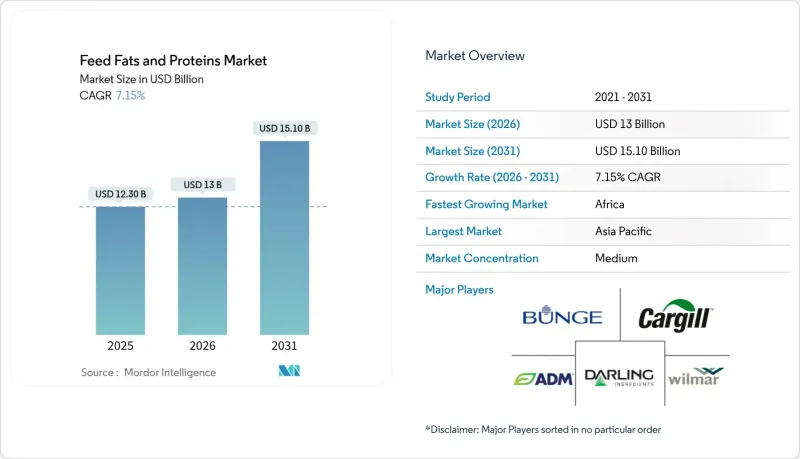

Mordor Intelligence에 의하면, 사료용 지방 및 단백질 시장 규모는 2025년 123억 달러로 평가되었습니다. 2026년 130억 달러로 확대되어 2031년까지 151억 달러에 이를 것으로 예측됩니다. 2026-2031년 CAGR은 7.15%를 나타낼 전망입니다.

본 보고서는 제품 유형(동물성 지방, 식물성 기름, 혼합 특수 지질), 형태(건조 분말·가루, 액상 유지), 가축(가금류, 돼지, 반추동물, 수산 양식, 반려동물사료), 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 사료용 지방 및 단백질 시장 동향과 인사이트

재생 가능 디젤 플랜트에서 발생하는 잉여 동물성 지방 부산물

재생 가능 디젤 플랜트에서 발생하는 잉여 동물성 지방 부산물은 사료용 지방 및 단백질 시장의 중요한 촉진요인으로 부상하고 있습니다. 재생 가능 디젤 생산이 증가함에 따라 동물성 부산물공급량도 늘어나고 있으며, 이러한 부산물들은 현재 사료 배합에서 비용 효율이 높고 영양가가 높은 성분으로 효과적으로 활용되고 있습니다. 이러한 접근 방식은 폐기물을 최소화함으로써 지속가능성을 증진할 뿐만 아니라, 사료 원료공급 안정화에도 기여하고 있습니다. 미국 환경보호청(EPA)의 2026-2027년도 재생 가능 연료 기준에 따르면, 바이오매스 유래 디젤의 생산량이 36억 갤런으로 설정되어 원료에 대한 수요가 확보되는 동시에 부산물의 안정적인 공급이 보장됩니다.

항생제 의존도를 낮추는 특수 지질 혼합물

세계의 가금류 및 돼지 사육 농가들은 항생제를 이용한 성장 촉진제 사용을 단계적으로 중단하고 있으며, 기능성 지질이 효과적인 대체재로 부상하고 있습니다. ADM와 Berg+Schmidt GmbH &Co.KG(Stern-Wywiol Gruppe)는 라우린산과 캡슐화된 오메가-3를 결합한 정밀한 배합을 개발하여, 소매업체의 ‘항생제 무사용’ 약속에 부합하는 프리미엄 솔루션을 통합 업체에 제공합니다. 이러한 특수 지질 혼합물은 동물의 건강을 지원할 뿐만 아니라, 항생제 의존도를 낮춤으로써 지속 가능한 농업 관행에 기여하고 있으며, 이는 전 세계 소비자와 규제 당국이 점점 더 요구하는 요건입니다.

동물성 사료 원료에 대한 소비자의 반발

유럽의 반려동물사료 구매자들 사이에서 동물성 원료의 지속가능성에 의문을 제기하는 목소리가 높아지고 있으며, 규모와 비용이 여전히 과제로 남아 있음에도 불구하고, 브랜드 측에 조류나 곤충 유래 오일의 시범 도입을 요구하는 압력이 강해지고 있습니다. 이러한 추세는 ‘식물성’ 고기에 대한 마케팅 주장이 더욱 힘을 얻게 되면, 일반 축산 분야로도 파급될 가능성이 있습니다. 이러한 소비자 의식의 변화는 반려동물사료 분야에 그치지 않고, 보다 광범위한 가축 사료 시장에도 영향을 미칠 가능성이 있습니다. 인간용 식품 업계에서 지속가능성을 중시하는 마케팅이 계속해서 확대된다면, 동물 영양 분야에서도 비슷한 기대가 생길지도 모릅니다. 사료 제조업체들은 규제 당국의 감시 강화나 배합 변경 요구에 직면할 가능성이 있으며, 그 결과 업계는 기존의 동물성 원료를 대체할 혁신적이고 비용 효율적인 대체재로 눈을 돌리게 될 것입니다.

부문별 분석

2025년에는 렌더링 업체들이 통합형 기업에 비용 효율이 높은 동물성 지방과 가금류 지방을 공급함에 따라, 동물성 지방이 최대 부문으로 부상하여 사료용 지방 및 단백질 시장 점유율의 44.5%를 차지했습니다. 이러한 장점은 주로 육류 가공 및 렌더링 산업의 부산물로 널리 구할 수 있다는 점에 기인하며, 사료 배합에 있어 비용 효율이 높고 지속 가능한 선택지가 되고 있습니다. 또한, 동물성 지방은 발열량이 높아 사료의 에너지 밀도를 높여주며, 가축의 체중 증가와 사료 전환율 향상에 기여합니다. 확립된 공급망과 기존 사료 가공 시스템 간의 호환성은 특히 가격에 민감한 시장에서 그 입지를 공고히 하고 있습니다.

혼합 특수 지질은 가장 빠르게 성장하는 부문으로, 2026년부터 2031년까지 9.8%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이 제품들은 식물성 오일이나 해양 오일 등 다양한 지방 원료를 기능성 첨가제와 결합하여 맞춤형 영양 성분을 구현하도록 배합되었습니다. 이러한 채용 확대는 특정 종, 성장 단계, 건강 상태에 맞추어 사료를 최적화하는 ‘정밀 영양’에 대한 중시에서 비롯되고 있습니다. 수산물 양식에서 블렌드 지질은 오메가-3 함량을 높여 어류의 건강을 증진시킵니다. 한편, 가금류 및 돼지 분야에서는 면역력 향상, 장내 환경 개선, 그리고 전반적인 생산성 향상에 기여합니다.

지역별 분석

아시아태평양은 최대 시장이며, 2025년에는 사료용 지방 및 단백질 시장의 34.2%를 차지했습니다. 이러한 우위는 해당 지역, 특히 중국, 인도, 베트남, 인도네시아 등의 국가에서 대규모로 급속히 성장하고 있는 축산 및 양식 산업에 의해 주도되고 있습니다. 2025년, 중국이 2030년까지 대두박의 배합 비율을 10%로 줄이겠다는 목표를 제시함에 따라, 제분업체들은 대체 단백질원을 확보하고 에너지 밀도를 유지하기 위해 지방 함량을 높여야 할 필요에 직면해 있으며, 이로 인해 가금류용 지방 및 카놀라유 수입이 증가하고 있습니다. 인구 증가, 가처분 소득의 향상, 그리고 동물성 단백질에 대한 수요 증가가 해당 지역의 사료 생산을 뒷받침하는 주요 요인이 되고 있습니다. 또한, 사료 제조업체들의 강력한 입지, 원료의 확보 가능성, 그리고 상업 농업 및 수산 사료 인프라에 대한 지속적인 투자가 아시아태평양 시장에서 이 회사의 선도적 지위를 더욱 공고히 하고 있습니다.

아프리카는 가장 빠르게 성장하고 있는 지역으로, 2026년부터 2031년까지 7.2%라는 지역별 최고 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이러한 성장은 주로 도시화의 진전, 단백질 소비량 증가, 그리고 축산 및 양계 농법의 점진적인 현대화에 의해 주도되고 있습니다. 정부와 민간 기업 모두 농업 생산성을 높이기 위해 사료 품질 향상과 공급망 개선에 투자하고 있습니다. 이 시장의 발전 수준은 다른 지역보다 여전히 뒤처져 있지만, 균형 잡힌 동물 영양에 대한 인식이 높아지고 상업적 농업이 확대됨에 따라 아프리카의 사료용 지방 및 단백질 수요는 지속될 것으로 전망됩니다.

남미에서는 식용유 종자 가공의 동향과 바이오연료 정책의 변화를 배경으로, 향후 몇 년간 꾸준한 성장이 예상됩니다. 브라질에서는 활발한 대두 압착 활동으로 인해 대두박 및 관련 부산물공급이 확대되면서 사료 생산이 촉진되고 있습니다. 북미에서는 재생 가능 디젤 연료의 생산 확대가 시장 성장을 뒷받침하고 있으며, 이로 인해 대량의 동물성 지방 및 기타 지질 부산물이 생산되고 있습니다. 이러한 부산물은 비용 효율성과 입수 용이성 덕분에 사료 용도로의 활용이 점점 더 늘어나고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the feed fats and proteins market size is projected to increase from USD 12.30 billion in 2025 to USD 13.00 billion in 2026 and reach USD 15.10 billion by 2031, growing at a CAGR of 7.15% over 2026-2031.

This report is Segmented by Product Type (Animal Fats, Vegetable Oils, and Blended Specialty Lipids), by Form (Dry Meals and Powders, and Liquid Fats and Oils), by Livestock (Poultry, Swine, Ruminants, Aquaculture, and Pet Food), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Feed Fats And Proteins Market Trends and Insights

Surplus Animal-Fat By-Products from Renewable-Diesel Plants

Surplus animal-fat by-products from renewable diesel plants are becoming a significant driver of the feed fats and proteins market. The rise in renewable diesel production has increased the availability of animal by-products, which are now being effectively used as cost-efficient, nutrient-dense components in animal feed formulations. This approach not only promotes sustainability by minimizing waste but also helps stabilize the supply of feed ingredients. The Environmental Protection Agency's 2026-2027 Renewable Fuel Standard fixed biomass-based diesel at 3.6 billion gal, locking in demand for feedstocks while guaranteeing steady coproduct availability.

Specialty Lipid Blends That Reduce Antibiotic Reliance

Global poultry and swine producers are eliminating antibiotic growth promoters, while functional lipids have emerged as viable substitutes. ADM and Berg+Schmidt GmbH & Co.KG (Stern-Wywiol Gruppe) precision blends that combine lauric acid with encapsulated omega-3s, offering integrators a premium solution that aligns with retailer antibiotic-free pledges. These specialty lipid blends not only support animal health but also contribute to sustainable farming practices by reducing reliance on antibiotics, a demand increasingly sought by consumers and regulatory bodies worldwide.

Consumer Backlash Against Animal-Based Feed Ingredients

A rising cohort of European pet-food buyers questions the sustainability of rendered animal inputs, pressuring brands to trial algal and insect oils even though scale and cost remain constraints. This sentiment could spill into mainstream livestock channels if marketing claims around "plant-based" meat continue to gain traction. This changing consumer sentiment extends beyond the pet-food segment and could influence the broader livestock feed market. If sustainability-focused marketing in the human food industry continues to grow, similar expectations may emerge in animal nutrition. Feed producers may face increased regulatory scrutiny and demands for reformulation, driving the industry toward innovative yet cost-effective alternatives to traditional animal-derived inputs.

Other drivers and restraints analyzed in the detailed report include:

- Aquafeed Milling Expansion in Southeast Asia

- Mandatory Deforestation-Free Soy Sourcing Spurring Alternative Fats

- Photo-Oxidation Losses in High-Polyunsaturated Fatty Acids (PUFA) Liquid Fats During Bulk Storage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Animal fats led the largest segment, with 44.5% of the feed fats and proteins market share in 2025, as renderers supplied cost-effective tallow and poultry fat to integrators. This dominance is largely due to their widespread availability as by-products of the meat processing and rendering industries, making them a cost-effective and sustainable option for feed formulations. Animal fats also provide a high calorific value, enhancing the energy density of feed and contributing to improved weight gain and feed conversion ratios in livestock. Their established supply chains and compatibility with existing feed processing systems strengthen their position, particularly in price-sensitive markets.

Blended specialty lipids are the fastest-growing segment and will post the highest CAGR of 9.8% through 2026-2031. These products are formulated by combining various fat sources, such as vegetable oils and marine oils, with functional additives to achieve customized nutritional profiles. Their increasing adoption is driven by the emphasis on precision nutrition, which optimizes feed for specific species, growth stages, and health outcomes. In aquaculture, blended lipids enhance omega-3 content and promote fish health, while in poultry and swine, they improve immunity, gut health, and overall productivity.

Geography Analysis

Asia-Pacific is the largest region, with 34.2% of the feed fats and proteins market share in 2025. This dominance is driven by the region's large and rapidly expanding livestock and aquaculture industries, particularly in countries such as China, India, Vietnam, and Indonesia. In 2025, China's aim to cut soybean-meal inclusion to 10% by 2030 forces mills to secure alternative proteins and raise fat levels to maintain energy density, stimulating imports of poultry fat and canola oil. Rising population, increasing disposable incomes, and growing demand for animal protein are key factors supporting feed production in the region. Additionally, the strong presence of feed manufacturers, availability of raw materials, and continued investments in commercial farming and aquafeed infrastructure further reinforce Asia-Pacific's leading position in the market.

Africa is the fastest-growing region, projected to log the highest regional CAGR of 7.2% through 2026-2031. This growth is mainly driven by rising urbanization, increasing protein consumption, and the gradual modernization of livestock and poultry farming practices. Both governments and private entities are investing in improving feed quality and supply chains to boost agricultural productivity. While the market remains less developed than in more established regions, growing awareness of balanced animal nutrition and the expansion of commercial farming are projected to sustain demand for feed fats and proteins in Africa.

South America is projected to experience steady growth in the coming years, driven by evolving oilseed processing dynamics and biofuel policies. In Brazil, robust soybean crushing activity has enhanced the availability of soybean meal and related by-products, bolstering feed production. In North America, market growth is supported by the expansion of renewable diesel production, which produces substantial volumes of animal fat and other lipid coproducts. These by-products are increasingly used in feed applications due to their cost-effectiveness and availability.

- Cargill, Incorporated.

- Archer-Daniels-Midland Company

- Darling Ingredients Inc.

- Bunge Global SA

- Wilmar International Limited

- AAK AB

- BASF SE

- Alltech, Inc.

- The Scoular Company

- GrainCorp Limited

- DSM-Firmenich AG

- Evonik Industries AG

- Berg + Schmidt GmbH & Co. KG

- Adisseo SAS

- SARIA SE & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surplus animal-fat by-products from renewable-diesel plants

- 4.2.2 Specialty lipid blends that reduce antibiotic reliance

- 4.2.3 Aquafeed milling expansion in Southeast Asia

- 4.2.4 Mandatory deforestation-free soy sourcing spurring alternative fats

- 4.2.5 Rising demand for energy-dense poultry and swine rations

- 4.2.6 Blockchain-enabled rendering traceability, unlocking new premiums

- 4.3 Market Restraints

- 4.3.1 Price volatility of tallow and poultry fat

- 4.3.2 Trade barriers on rendered products after disease outbreaks

- 4.3.3 Consumer backlash against animal-based feed ingredients

- 4.3.4 Photo-oxidation losses in high-Polyunsaturated Fatty Acids (PUFA) liquid fats during storage

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Animal Fats

- 5.1.2 Vegetable Oils

- 5.1.3 Blended Specialty Lipids

- 5.2 By Form

- 5.2.1 Dry Meals and Powders

- 5.2.2 Liquid Fats and Oils

- 5.3 By Livestock

- 5.3.1 Poultry

- 5.3.2 Swine

- 5.3.3 Ruminants

- 5.3.4 Aquaculture

- 5.3.5 Pet Food

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 New Zealand

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Nigeria

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products And Services, And Recent Developments)

- 6.4.1 Cargill, Incorporated.

- 6.4.2 Archer-Daniels-Midland Company

- 6.4.3 Darling Ingredients Inc.

- 6.4.4 Bunge Global SA

- 6.4.5 Wilmar International Limited

- 6.4.6 AAK AB

- 6.4.7 BASF SE

- 6.4.8 Alltech, Inc.

- 6.4.9 The Scoular Company

- 6.4.10 GrainCorp Limited

- 6.4.11 DSM-Firmenich AG

- 6.4.12 Evonik Industries AG

- 6.4.13 Berg + Schmidt GmbH & Co. KG

- 6.4.14 Adisseo SAS

- 6.4.15 SARIA SE & Co. KG