|

시장보고서

상품코드

2062015

신축성 전도성 재료 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Stretchable Conductive Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

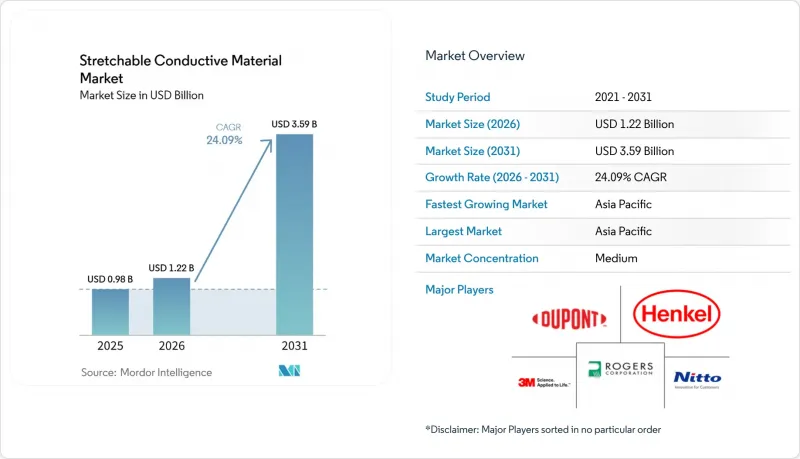

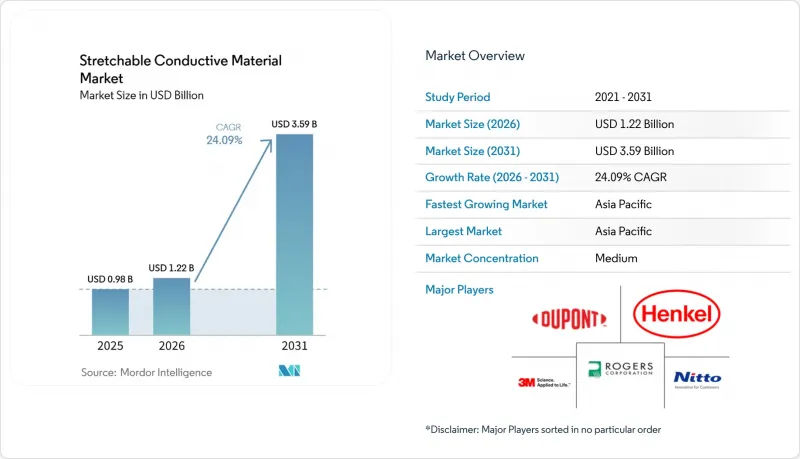

Mordor Intelligence에 의하면, 신축성 전도성 재료 시장 규모는 2025년에 9억 8,000만 달러로 평가되었습니다. 2026년 12억 2,000만 달러에서 2031년까지 35억 9,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 24.09%를 나타낼 전망입니다.

본 보고서는 재료의 유형(그래핀 계열, 은 계열 등), 형태(잉크, 필름·포일 등), 용도(웨어러블 일렉트로닉스, 의료용·생체전위 디바이스 등), 최종 사용자(소비자용 전자기기, 의료 등), 지역(아시아태평양, 북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 신축성 전도성 재료 시장 동향 및 인사이트

웨어러블 일렉트로닉스 및 스마트 텍스타일에 대한 수요 증가

지속적인 건강 모니터링이 일반 시장에 보급됨에 따라, 신축성 전도체는 특수한 조사 용도에서 소비재로 그 위상이 높아지고 있으며, 2025년 FDA 승인을 통해 임상용 패치용 은 나노와이어 전극이 상용화되었습니다. 열가소성 폴리우레탄에 인쇄된 은 나노와이어 잉크는 10만 회의 굴곡 사이클을 견디며, 산업용 세탁에도 견딜 수 있는 의류 일체형 센서를 구현합니다. 산업 안전 규제로 인해 스마트 텍스타일에 대한 수요가 증가하고 있으며, 그 예로 2025년 후반에 파나소닉이 6G 안테나용 의류를 위해 출시한 ‘Copper Clad Stretch’ 소재를 들 수 있습니다. 5G 엣지 컴퓨팅의 부상에 따라 기가헤르츠 대역의 신호 품질을 유지할 수 있는 신축성 있는 상호 연결이 요구되고 있지만, 이는 10% 이상의 성장률에서는 경질 구리박으로 대응할 수 없는 과제입니다. ISO 13485 준수에 따라, 소재 선정은 입증된 생체적합성과 세탁 내구성을 중시하는 방향으로 이루어지고 있으며, 설계 워크플로우에 품질 기준이 반영되어 있습니다.

유연·신축성 전자 기술의 발전

재료 과학 분야의 획기적인 발전으로 인해, 경질 실리콘과 신축성 유기 소재 간의 격차가 점차 좁혀지고 있습니다. EPFL은 300%의 변형률 하에서도 95%의 전도성을 유지하는 액체 금속 섬유를 입증함으로써, 촉각의 충실도를 갖춘 인공 피부의 길을 열었습니다. MXene 기반 변형 불변 소자는 0-50%의 변형 범위에서 안정적인 저항을 유지하며, 전기-기계적 히스테리시스를 2%로 저감합니다. 한국의 KAIST-POSTECH 컨소시엄은 30%의 변형률 하에서 신축성 OLED에서 25%의 외부 양자 효율을 달성함으로써, 플렉서블 디스플레이의 적용 분야를 자동차 대시보드와 AR 바이저로 확대했습니다. 상업적 실현 가능성은 1제곱미터당 5달러 미만의 비용으로 10마이크로미터 미만의 미세 구조를 구현하는 롤-투-롤 인쇄 기술에 달려 있으며, 헨켈과 듀폰은 AI 최적화 잉크를 활용해 이 목표를 추구하고 있습니다. 이러한 발전은 종합적으로 볼 때, 신축성 전도성 재료 시장을 저전류 센서 분야에서 고출력 밀도 액추에이터 및 에너지 수확 모듈 분야로 확대시키고 있습니다.

첨단 나노 소재 및 제조 기술의 높은 비용

단층 탄소나노튜브는 1kg당 500달러, 그래핀은 1kg당 200달러를 초과하기 때문에 그 용도는 고급 분야로 한정되어 있습니다. 자동차 1차 공급업체들은 센서 모듈 가격을 2달러 미만으로 낮추는 것을 목표로 하고 있지만, 현재 나노 소재의 가격 책정 수준으로는 이 장벽을 넘을 수 없습니다. 5µm 미만의 정렬 정밀도를 갖춘 롤 투 롤(R2R) 프린터는 1,000만 달러가 넘는 설비 투자(CAPEX)가 필요하기 때문에 신규 진입을 가로막고 있습니다. DexMat사의 연속 CNT 합성 기술 덕분에 2024년에는 비용이 1kg당 150달러까지 절감되었으나, 변환업체들이 잉크의 유변학에 대한 전문 지식이 부족하여 도입이 지연되고 있습니다. 2028년 이후, 중국과 한국의 대규모 제조 시설이 수 톤 규모의 생산 능력에 도달하면 가격 압박은 완화될 것입니다.

부문별 분석

액체 금속 및 하이브리드 시스템은 2026년부터 2031년까지 연평균 성장률(CAGR) 25.67%를 나타낼 것으로 예측되며, 갈륨-인듐 합금이 나노와이어 필름에서 습기로 인한 산화 열화 문제를 극복함에 따라 신축성 전도성 재료 시장 점유율을 확대해 나갈 것으로 보입니다. 은계 소재는 닛토덴코가 C3Nano에 1,500만 달러를 투자해 생산 능력을 확충한 데 힘입어, 2025년에는 42.44%의 시장 점유율을 유지하며 우위를 지키고 있습니다. 그래핀·금속 나노멤브레인은 100% 변형 하에서도 기가헤르츠 수준의 안정성을 보여, 6G 웨어러블 안테나 개발을 주도하고 있습니다. CNT는 OCSiAl이 생산하는 150톤 규모의 TUBALL을 공급받는 혜택을 누리고 있으며, 이를 통해 15년간의 신뢰성이 요구되는 배터리 팽창 센서의 구현을 가능하게 하고 있습니다.

현재 재료 선택은 용도별로 구분되어 있습니다. 의료기기 분야에서는 생체 적합성이 뛰어난 은이 선호되고, 방위 분야에서는 자가 복원성 때문에 액체 금속이 선택되며, 소비자용 전자 기기에서는 비용 면에서 구리가 표준적으로 채택되고, 소프트 로보틱스 분야에서는 유연성을 높이기 위해 CNT-폴리머 복합재료가 채택되고 있습니다. 2027년 이후, 파나소닉의 ‘Copper Clad Stretch’가 제조 설계 규격을 확립함에 따라, 강성 아일랜드 칩과 신축성 배선을 결합한 하이브리드 구조의 신축성 전도성 재료 시장 점유율은 확대될 전망입니다.

잉크는 0.10 미화 달러 미만의 의료용 패치를 가능하게 하는 저비용 스크린 인쇄를 통해 2025년 매출의 51.50%를 차지했습니다. 그러나 OEM 업체들이 프린터에 대한 투자를 피할 수 있는 라미네이션 지원 모듈을 요구함에 따라, 엘라스토머 복합재료는 2031년까지 25.74%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 파나소닉의 ‘FineX’ 등 필름 및 포일은 50%의 성장률에서 10Ω/sq 미만의 저항값을 실현하여, 폴더블 디스플레이의 경첩에 활용되고 있습니다. 테이프와 코팅은 연구 개발 용도로 사용되고 있으며, 3M이 2025년에 출시한 전도성 테이프의 성능 개선 덕분에 20%의 전단 하에서도 1Ω 미만의 접촉 저항을 유지하고 있습니다. 롤 투 롤(roll-to-roll) 생산 능력이 확대됨에 따라, 소프트 로봇 액추에이터 및 자동차용 센서용 엘라스토머 복합재에 사용되는 신축성 전도성 재료 시장 규모는 잉크 시장을 점점 더 앞지를 것으로 전망됩니다.

지역별 분석

아시아태평양은 2025년 매출의 41.6%를 차지했으며, 중국의 플렉서블 디스플레이에 대한 보조금, 한국의 효율 25%를 자랑하는 신축성 OLED, 그리고 일본의 파나소닉이 출시한 CCS에 힘입어 2031년까지 연평균 성장률(CAGR) 25.45%를 달성할 것으로 전망됩니다. 장쑤 Cnano사의 500톤 규모 그래핀 생산 능력과 20억 달러를 넘는 대만의 PCB 투자 등, 수직 통합형 공급망이 이 지역의 주도적 지위를 확고히 하고 있습니다. 소재 분야의 혁신은 여전히 동북아시아를 중심으로 이루어지고 있지만, 인도와 아세안(ASEAN) 국가들이 저비용 조립 거점으로 부상하고 있습니다.

북미에서는 DARPA와 미 육군의 전자 피부 프로토타입에 대한 자금 지원이 호재로 작용하여, 2028년까지 이러한 기술들이 의료 및 자동차 분야의 상용화로 이어질 것입니다. FDA 승인 절차와 ISO 13485 인증 공장은 3M이나 듀폰과 같은 일류 공급업체들을 유치하고 있으며, 두 기업 모두 시장 점유율을 지키기 위해 수십억 달러 규모의 연구개발 투자를 진행하고 있습니다. 캐나다와 멕시코는 미국 자동차 업계의 채용 동향을 따라, 전기차 배터리 모니터링용 신축성 센서의 평가를 진행하고 있습니다.

유럽의 성장은 재활용 의무화와 밀접한 관련이 있습니다. IEC TC-111의 2025년 개정안에 따라 조달 프로세스에 자재 회수 지표가 반영됨에 따라, 헨켈의 박리용 접착제와 헤라에우스의 재활용 가능한 페이스트가 경쟁 우위를 점하게 될 것입니다. 독일과 프랑스가 학술적인 돌파구를 주도하는 한편, 북유럽 국가들에서는 산업용 세탁을 견딜 수 있는 센서에 대한 조기 도입 수요가 발생하고 있습니다. 제재 조치로 인해 러시아 시장 진입이 제한되고 있습니다. 남미 및 중동 및 아프리카(MEA) 지역은 여전히 발전 단계에 있지만, 브라질의 공중보건 시스템과 사우디아라비아의 스마트시티 프로젝트에서는 2028년 이후의 보급을 위한 비용 절감 로드맵이 검토되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the stretchable conductive material market size was valued at USD 0.98 billion in 2025 and is estimated to grow from USD 1.22 billion in 2026 to reach USD 3.59 billion by 2031, at a CAGR of 24.09% during the forecast period (2026-2031).

This report is Segmented by Type of Material (Graphene-Based, Silver-Based, and More), Form (Inks, Films and Foils, and More), Application (Wearable Electronics, Medical and Biopotential Devices, and More), End-User (Consumer Electronics, Healthcare, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Stretchable Conductive Material Market Trends and Insights

Growing Demand for Wearable Electronics and Smart Textiles

Mass-market acceptance of continuous health tracking is elevating stretchable conductors from specialty research to consumer staples, with FDA clearances in 2025 validating silver-nanowire electrodes for clinical-grade patches. Silver-nanowire inks printed on thermoplastic polyurethane survive 100,000 flex cycles, enabling garment-integrated sensors that withstand industrial laundry. Industrial safety mandates are adding smart-textile demand, illustrated by Panasonic's Copper Clad Stretch material launched in late 2025 for 6G antenna garments. The rise of 5G edge computing requires stretchable interconnects that maintain gigahertz integrity, a task rigid copper foils cannot meet beyond 10% elongation. ISO 13485 compliance is guiding material selection toward proven biocompatibility and wash durability, embedding quality benchmarks into design workflows.

Advancements in Flexible and Stretchable Electronics

Material-science milestones are closing the gap between rigid silicon and stretchable organics. EPFL demonstrated liquid-metal fibers retaining 95% conductivity at 300% strain, opening a path to prosthetic skin with tactile fidelity. MXene-based strain-invariant devices sustain stable resistance across 0-50% strain, reducing electromechanical hysteresis to 2%. South Korea's KAIST-POSTECH consortium achieved 25% external quantum efficiency in stretchable OLEDs at 30% strain, pivoting flexible displays toward automotive dashboards and AR visors. Commercial viability hinges on roll-to-roll printing at sub-10 µm features under USD 5 per m2, targets Henkel and DuPont pursue via AI-optimized inks. These developments collectively expand the stretchable conductive material market beyond low-current sensors to power-dense actuators and energy-harvesting modules.

High Cost of Advanced Nanomaterials and Production Technology

Single-walled carbon nanotubes at USD 500 per kg and graphene above USD 200 per kg confine usage to premium sectors. Automotive Tier 1 suppliers target sub-USD 2 sensor modules, a hurdle current nanomaterial pricing cannot meet. Roll-to-roll printers with sub-5 µm registration exceed USD 10 million CAPEX, deterring entrants. DexMat's continuous CNT synthesis cut costs to USD 150 per kg in 2024, yet adoption lags as converters lack ink-rheology expertise. Price pressure will relax post-2028 when large-scale Chinese and Korean fabs reach multi-ton capacities.

Other drivers and restraints analyzed in the detailed report include:

- Healthcare Monitoring Devices Proliferation

- Defense-Funded Electronic Skin Research and Development Programs

- Performance Fatigue Under Cyclic Strain

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid metals and hybrid systems are projected to grow at 25.67% CAGR during 2026-2031 and will capture an incremental stretchable conductive material market size as gallium-indium alloys overcome humidity-induced oxidation failures in nanowire films. Silver-based materials maintain dominance with a 42.44% 2025 share, supported by Nitto Denko's USD 15 million capacity investment in C3Nano. Graphene-metal nanomembranes demonstrated gigahertz-level stability under 100% strain, advancing 6G wearable antennas. CNTs benefit from OCSiAl's 150-ton TUBALL output, enabling battery-swelling sensors that demand 15-year reliability.

Material choice now segments by end-use: medical devices prefer biocompatible silver; defense favors liquid metals for self-healing; consumer electronics default to copper for cost; soft robotics adopts CNT-polymer composites for compliance. The stretchable conductive material market share of hybrid architectures combining rigid-island chips with stretchable interconnects will widen post-2027 as Panasonic's Copper Clad Stretch formalizes manufacturing design-rules.

Inks retained 51.50% of 2025 revenue owing to low-cost screen printing that delivers sub-USD 0.10 medical patches. Yet elastomeric composites will log the highest 25.74% CAGR through 2031 as OEMs seek laminate-ready modules that bypass printer investment. Films and foils such as Panasonic's FineX provide foldable-display hinges with less than 10 Ω/sq resistance at 50% elongation. Tapes and coatings serve research and development, with 3M's 2025 conductive-tape expansion keeping less than 1Ω contact resistance under 20% shear. As roll-to-roll capacity scales, the stretchable conductive material market size for elastomeric composites in soft-robotic actuators and automotive sensors will increasingly outpace inks.

Geography Analysis

Asia-Pacific generated 41.6% of 2025 revenue and is projected to achieve a 25.45% CAGR through 2031, driven by China's flexible-display subsidies, South Korea's 25%-efficient stretchable OLEDs, and Panasonic's CCS launch in Japan. Vertically integrated supply chains, such as Jiangsu Cnano's 500-ton graphene output and Taiwan PCB investments topping USD 2 billion, anchor regional leadership. India and ASEAN nations emerge as low-cost assembly hubs, although material innovation remains Northeast-Asian-centric.

North America benefits from DARPA and U.S. Army funding of electronic-skin prototypes, pulling technologies into commercial healthcare and automotive by 2028. FDA pathways and ISO 13485 plants attract premium suppliers like 3M and DuPont, both channeling multibillion-dollar research and development to defend shares. Canada and Mexico follow U.S. automotive adoption curves, evaluating stretchable sensors for EV battery monitoring.

Europe's growth aligns with recyclability mandates; IEC TC-111's 2025 update embeds material-recovery metrics in procurement, advantaging Henkel's debonding adhesives and Heraeus's recyclable pastes. Germany and France drive academic breakthroughs, while Nordic pilots in occupational safety offer early-adopter demand for industrial-laundry-proof sensors. Sanctions limit Russia's participation; South America and MEA remain nascent, with Brazil's public health system and Saudi smart-city projects monitoring cost-down roadmaps for post-2028 uptake.

- 3M

- ACS Material

- ANP CORPORATION

- Dow

- DuPont

- Henkel AG & Co. KGaA

- Heraeus Holding GmbH

- Indium Corporation

- ITOCHU Corporation

- Liquid Wire Inc.

- NextFlex

- Nissha Co., Ltd.

- Nitto Denko Corporation

- Panasonic Corporation

- Priways Co., Ltd.

- Rogers Corporation

- Shanghai Huzheng Industrial Co., Ltd.

- Sun Chemical Corporation

- TOYOBO CO., LTD.

- Vorbeck Materials Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for wearable electronics and smart textiles

- 4.2.2 Advancements in flexible and stretchable electronics

- 4.2.3 Healthcare monitoring devices proliferation

- 4.2.4 Defense-funded "electronic skin" research and development programs

- 4.2.5 Sustainability push toward recyclable printed electronics

- 4.3 Market Restraints

- 4.3.1 High cost of advanced nanomaterials and production tech

- 4.3.2 Performance fatigue under cyclic strain

- 4.3.3 Electromechanical hysteresis limiting sensor precision

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type of Material

- 5.1.1 Graphene-based Materials

- 5.1.2 Silver-based Materials

- 5.1.3 Carbon Nanotubes (CNTs)

- 5.1.4 Copper-based Materials

- 5.1.5 Conductive Polymers

- 5.1.6 Liquid Metals and Hybrid Systems

- 5.2 By Form

- 5.2.1 Inks

- 5.2.2 Films and Foils

- 5.2.3 Elastomeric Composites

- 5.2.4 Tapes and Coatings

- 5.3 By Application

- 5.3.1 Wearable Electronics

- 5.3.2 Medical and Biopotential Devices

- 5.3.3 Soft Robotics and Actuators

- 5.3.4 Stretchable Displays and Sensors

- 5.3.5 Energy Storage and Harvesting

- 5.3.6 Electronic Skin and Smart Textiles

- 5.4 By End-user Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Healthcare

- 5.4.3 Aerospace and Defense

- 5.4.4 Automotive and e-Mobility

- 5.4.5 Energy and Utilities

- 5.4.6 Industrial Automation and Sports/Fitness

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 ACS Material

- 6.4.3 ANP CORPORATION

- 6.4.4 Dow

- 6.4.5 DuPont

- 6.4.6 Henkel AG & Co. KGaA

- 6.4.7 Heraeus Holding GmbH

- 6.4.8 Indium Corporation

- 6.4.9 ITOCHU Corporation

- 6.4.10 Liquid Wire Inc.

- 6.4.11 NextFlex

- 6.4.12 Nissha Co., Ltd.

- 6.4.13 Nitto Denko Corporation

- 6.4.14 Panasonic Corporation

- 6.4.15 Priways Co., Ltd.

- 6.4.16 Rogers Corporation

- 6.4.17 Shanghai Huzheng Industrial Co., Ltd.

- 6.4.18 Sun Chemical Corporation

- 6.4.19 TOYOBO CO., LTD.

- 6.4.20 Vorbeck Materials Corp.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Growth in e-Healthcare, Smart Clothing and Personalized Wearables