|

시장보고서

상품코드

2062019

3가 크롬 표면처리 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Trivalent Chromium Finishing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

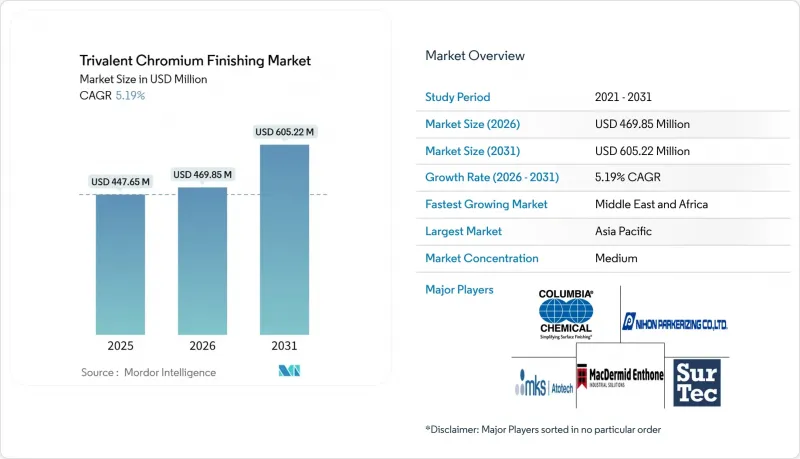

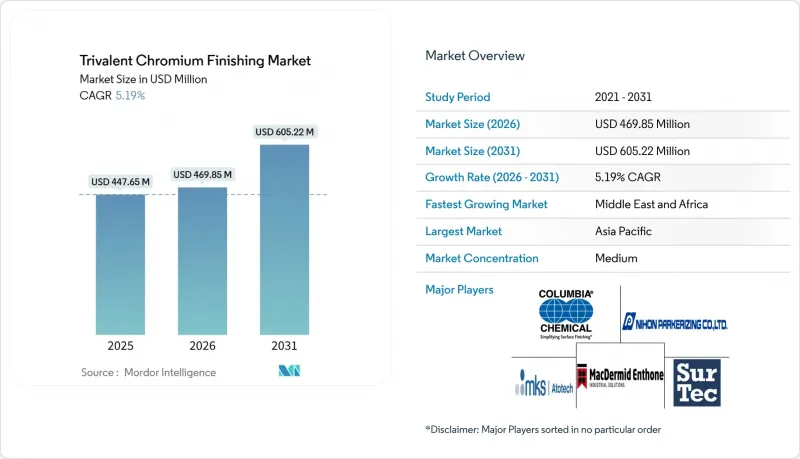

Mordor Intelligence에 의하면, 3가 크롬 표면처리 시장 규모는 2025년에 4억 4,765만 달러로 평가되었고 2026년 4억 6,985만 달러에서 2031년까지 6억 522만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.19%를 나타낼 전망입니다.

본 보고서는 유형별(도금, 컨버전 코팅 등), 기판별(강철 및 스테인리스 스틸, 알루미늄 및 합금 등), 최종 사용자 산업별(자동차, 항공우주 및 항공, 가전·전자기기 등), 그리고 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 3가 크롬 표면처리 시장 동향 및 분석

6가 크롬(Cr(VI))의 사용을 제한하는 엄격한 환경 규제

각 관할 구역에서는 6가 크롬의 이행 기간이 단축됨에 따라, 3가 크롬 표면처리 시장은 급속한 대체 국면으로 접어들고 있습니다. 유럽화학물질청(ECHA)은 2025년 4월에 18개월의 이행 기간을 제안했으며, 2027년부터 2028년까지 발효되는 것을 목표로 하고 있습니다. 한편, 캘리포니아주 대기자원국은 2027년까지 장식용 크롬 표면처리을 단계적으로 폐지하고, 2039년까지 경질 크롬 표면처리를 전면 금지하도록 의무화하고 있습니다. 두 지역에 제품을 공급하는 OEM 업체들은 현재 듀얼 케미스트리 방식의 생산 라인을 설계하고 있어 설비 투자 부담은 커지고 있지만, 3가 크롬계 처리에 대한 노력을 강화하고 있습니다. 일본 경제산업성은 수출 관련 일정을 REACH(화학물질의 등록, 평가, 허가 및 제한)에 맞추어, 사실상 이 기준을 세계 표준으로 정립했습니다. 사우스코스트 대기질 관리 구역의 규정 제1469호는 배출량을 1암페어시당 0.01mg으로 엄격히 제한하고 있으며, 남부 캘리포니아에서는 전해 정련을 수반하는 폐쇄형 3가 크롬 시스템이 표준으로 자리 잡고 있습니다. 이러한 법규들은 전반적으로 삼가 크롬 표면처리 시장을 국제 공급업체들에게 있어 규제상의 안전한 피난처로 확고히 자리매김하게 하고 있습니다.

EV 배터리 팩용 커넥터에는 Cr(III) 패시베이션이 필수입니다.

중국에서는 2025년에 1,200만 대 이상의 신에너지차가 출고되어, 커넥터의 염수 분무 시험 요건이 18개월 동안 48시간에서 96시간으로 두 배로 늘어남에 따라 구리 버스바의 3가 패시베이션에 대한 수요가 급증했습니다. 각 차량에는 20-30개의 커넥터가 장착되어 있으며, 이는 연간 1억 2,000만 개 이상의 부품에 RoHS 준수 코팅이 필요함을 의미합니다. 쑤저우의 도금 공장에서는 2025년 하반기 동제 커넥터 마감 작업 수주가 50% 급증했으며, 급속 충전의 보급에 따라 열 안정성 기준치가 150-200°C까지 상승했습니다. SurTec 등의 코팅제 제조업체들은 졸-겔계 탑코트와 결합하여 임피던스를 10배로 높이는 하이브리드 지르코늄-크롬 층을 도입하고 있으며, 향후에는 완전히 크롬이 포함되지 않은 대체재로 전환될 것으로 전망됩니다. 그러나 중기적으로는 3가 크롬 표면처리 시장이 기존의 구리 세정 및 활성화 공정과의 드롭인 호환성이라는 장점을 유지하고 있습니다.

기존 6가 크롬 표면처리 라인의 전환에 필요한 설비 투자

일반적인 전환 예산은 정류기, 여과 장치, 폐수 처리 설비의 업그레이드를 포함해 라인당 15만-50만 달러 수준이며, 연간 1,000개 미만의 부품을 도금하는 공장의 경우 투자 회수 기간은 5년을 초과합니다. ADCR 컨소시엄은 REACH 규정의 시행 기한에 대응하기 위해 유럽의 항공우주 관련 기업들이 12억 유로를 투자할 것으로 추산하고 있지만, 많은 중소기업들은 저비용 자금 조달 수단이 부족한 실정입니다. 그 결과, 3가 크롬 표면처리 시장은 양극화되고 있습니다. Tier 1 공급업체들은 자체 생산 라인을 구축하는 한편, 소규모 위탁 가공 업체들은 폐업하거나 통합을 추진하고 있습니다.

부문별 분석

도금 시장은 장식용 트림 및 기능성 내마모 코팅의 성장에 힘입어 2025년 매출의 42.45%를 차지했으나, OEM 업체들이 6가 및 3가 보고 기준치를 모두 회피할 수 있는 공정을 모색하고 있기 때문에 예측 기간(2026-2031년) 동안 패시베이션이 연평균 성장률(CAGR) 6.12%로 가장 빠르게 성장하고 있습니다. 컨버전 코팅은 분체 도장 전 알루미늄 케이스에 사용되기 때문에 안정적인 중간 위치를 차지하고 있지만, 최근 SurTec사의 하이브리드 지르코늄·크롬 패시베이션이 임피던스를 10배 향상시킨 것이 입증됨에 따라, 향후 지르코늄이 주류가 될 것이라는 추세가 시사되고 있습니다. 도금 분야의 3가 크롬 표면처리 시장 규모는 여전히 크지만, 나노 세라믹 및 졸-겔계 탑코트가 90초 사이클로 처리 가능한 저온 3가 크롬 코팅과 결합됨에 따라, 대량 생산되는 자동차용 프레스 부품의 타크트 타임이 개선되어 해당 시장 점유율은 축소될 전망입니다.

이에 반해 도금 지지파는 보잉사의 Cr(III)-Fe 합금 특허가 전류 밀도 100-500 mA cm?²를 규정하고 있으며, 거시 균열의 형성을 최소화하면서 1,250 비커스 경도를 목표로 하고 있다는 점을 지적하며, 기능성 크롬 표면처리이 계속 유지될 것이라고 반박하고 있습니다. 한편, 컨버전 코팅의 30-90초라는 짧은 침지 시간과 낮은 설비 투자 비용은 매주 알루미늄, 아연, 마그네슘 재질의 케이스를 교체해야 하는 가전 제조업체의 요구 사항에 부합합니다. 이러한 경제성 덕분에 3가 크롬 표면처리 시장은 단일 공정에 의해 지배되지 않고, 다양한 도금 기술로 분산된 상태를 유지하게 될 것입니다.

지역별 분석

2025년 3가 크롬 표면처리 시장의 매출에서 아시아태평양은 41.22%를 차지했습니다. 중국에서는 1,200만 대의 전기차(EV)가 커넥터 패시베이션 수요를 뒷받침하고 있으며, 일본에서는 정밀 기계 분야에서 EU 고객의 요구 사항을 충족하기 위해 3가 크롬 표면처리이 표준화되어 있습니다. 한국은 CHIPS법이 도금 인프라에 대한 자금 지원을 제외하고 있음에도 불구하고, 3가 크롬 코팅을 사용하여 반도체 리드 프레임을 보호하고 있습니다. 아세안 국가들은 ‘차이나 플러스 원’ 정책에 따른 생산 거점 이전의 혜택을 누리고 있으며, 베트남과 태국에 삼가 크롬 표면처리 신규 생산 라인이 추가되고 있습니다.

북미 시장에서는 미국의 항공우주 산업과 멕시코의 니어쇼어 자동차 부품이 시장 점유율을 주도하고 있습니다. 캘리포니아주의 ATCM(알루미늄 열교환기 규정)에 따라, 서부 해안 지역의 공장들은 2027년까지 장식용 크롬 표면처리, 2039년까지 경질 크롬 표면처리으로 전환해야 하는 압박을 받고 있으며, 이는 해당 지역 내 폐쇄형 3가 크롬 표면처리 설비에 대한 투자를 촉진하고 있습니다. 캐나다에서는 OEM 업체들이 경량화를 추진함에 따라 알루미늄 열교환기의 도금 수요가 확대되고 있습니다.

유럽은 가장 힘든 과도기를 겪고 있습니다. 2027년부터 시작되는 ECHA(유럽화학물질청)의 18개월 기한이, 폐자동차 규정(ELV)의 0.1% Cr(VI) 기준치와 겹치면서 추적성 비용을 상승시키고 있습니다. 기가캐스팅을 시범 도입하고 있는 독일의 각 OEM 기업들은 사내 3가 크롬 표면처리 라인을 필요로 하는 반면, ADCR 그룹의 12억 유로 규모 설비 투자 전망은 중소 항공우주 도금 업체들이 감당해야 할 재정적 부담을 여실히 드러내고 있습니다.

남미와 중동 및 아프리카는 합쳐서 시장 점유율이 가장 낮은 지역이지만, 후자는 2031년까지 연평균 성장률(CAGR) 6.31%라는 가장 높은 성장률을 기록하며 확대될 것으로 예측됩니다. 사우디아라비아의 ‘비전 2030’은 방위 및 건설 분야를 위한 자체 도금 사업에 자금을 지원하고 있는 반면, 남아프리카공화국의 크롬철광 매장량은 전 세계 3가 크롬 표면처리 시장에 영향을 미치는 인력 부족 상황에도 불구하고, 세계 3가 크롬염 공급의 기반을 이루고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the trivalent chromium finishing market size was valued at USD 447.65 million in 2025 and is estimated to grow from USD 469.85 million in 2026 to reach USD 605.22 million by 2031, at a CAGR of 5.19% during the forecast period (2026-2031).

This report is Segmented by Type (Plating, Conversion Coatings, and More), Base Material (Steel and Stainless Steel, Aluminum and Alloys, and More), End-User Industry (Automotive, Aerospace and Aviation, Appliances and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Trivalent Chromium Finishing Market Trends and Insights

Strict Environmental Regulations Limiting Cr(VI) Use

Jurisdictions are compressing the compliance window for hexavalent chrome and propelling the trivalent chromium finishing market toward rapid substitution. The European Chemicals Agency proposed an 18-month transition in April 2025, intending entry into force during 2027-2028, while California's Air Resources Board mandates decorative phase-outs by 2027 and hard-chrome elimination by 2039. OEMs serving both regions now engineer dual-chemistry lines, elevating capital intensity but deepening their commitment to trivalent chemistries. Japan's Ministry of Economy, Trade, and Industry aligned export timelines with REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), effectively globalizing the standard. South Coast Air Quality Management District Rule 1469 tightens emissions to 0.01 mg per amp-hour, making closed-loop trivalent systems with electrowinning the default in Southern California. Collectively, these statutes cement the trivalent chromium finishing market as the regulatory safe harbor for international suppliers.

EV Battery-Pack Connectors Require Cr(III) Passivation

China delivered more than 12 million new-energy vehicles in 2025, and connector salt-spray requirements doubled from 48 hours to 96 hours within 18 months, creating a surge in demand for trivalent passivation of copper busbars. Each vehicle houses 20-30 connectors, translating into over 120 million components annually needing RoHS-compliant coatings. Plating parks in Suzhou experienced a 50% order spike for copper connector finishing in H2-2025, and thermal stability thresholds rose to 150-200°C as fast-charging proliferated. Formulators such as SurTec have introduced hybrid zirconium-chromium layers that extend impedance tenfold when paired with sol-gel topcoats, hinting at future migration toward entirely chromium-free alternatives. For the medium term, however, the trivalent chromium finishing market retains the advantage of drop-in compatibility with existing copper cleaning and activation sequences.

Capex for Converting Legacy Cr(VI) Plating Lines

Typical conversion budgets range from USD 150,000 to USD 500,000 per line, including rectifiers, filtration, and wastewater upgrades, and payback exceeds five years for shops plating fewer than 1,000 parts yearly. The ADCR consortium estimates EUR 1.2 billion in capital across European aerospace players to meet REACH deadlines, and many SMEs lack access to low-cost financing. Consequently, the trivalent chromium finishing market is bifurcating: Tier-1 suppliers embed captive lines while small job shops shutter or consolidate.

Other drivers and restraints analyzed in the detailed report include:

- Automotive Lightweighting Demands Corrosion-Proof Finishes

- Aerospace Shift Toward High-Efficiency Trivalent Hard-Chrome

- Limited High-Temperature Wear Resistance vs. Hard-Chrome

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plating delivered 42.45% of 2025 revenue, driven by decorative trim and functional wear coatings, but passivation is expanding fastest at 6.12% CAGR for the forecast period (2026-2031) as OEMs chase processes that skirt both hexavalent and trivalent reporting thresholds. Conversion coatings occupy a stable middle ground because they serve aluminum housings before powder paint, yet SurTec's hybrid zirconium-chromium passivation recently demonstrated tenfold impedance gains, foreshadowing a future tilt toward zirconium dominance. The trivalent chromium finishing market size for plating remains large, yet its share is set to erode as nano-ceramic and sol-gel topcoats converge with low-temperature trivalent seals that run in 90-second cycles, improving takt time on high-volume automotive stampings.

Plating advocates counter that Boeing's Cr(III)-Fe alloy patent specifies current densities of 100-500 mA cm-2 and aims for 1,250 Vickers with minimal macro-crack formation, suggesting functional chrome will endure. Meanwhile, conversion coatings' 30-90 second immersion windows and low capital needs resonate with consumer-electronics plants that must pivot between aluminum, zinc, and magnesium chassis weekly. These economics ensure the trivalent chromium finishing market remains diversified across finishing techniques rather than dominated by a single process.

Geography Analysis

Asia-Pacific held 41.22% of 2025 revenue for the trivalent chromium finishing market, with China's 12 million EVs anchoring connector passivation demand and Japan's precision engineering segments standardizing on trivalent to appease EU customers. South Korea protects its semiconductor lead frames with trivalent coatings despite the CHIPS Act omitting plating infrastructure funding. ASEAN economies gain from "China-plus-one" relocation, adding greenfield trivalent lines in Vietnam and Thailand.

North America's market share is dominated by the U.S. aerospace and Mexican near-shored automotive parts. California's ATCM forces West Coast shops to shift decorative chrome by 2027 and hard chrome by 2039, propelling regional investment in closed-loop trivalent cells. Canada's aluminum heat-exchanger plating grows as OEMs push lightweighting.

Europe faces the tightest transition window: ECHA's 18-month deadline starting in 2027 converges with the End-of-Life Vehicle Regulation's 0.1 % Cr(VI) threshold, raising traceability costs. German OEMs piloting gigacasting need in-house trivalent lines, while the ADCR group's EUR 1.2 billion capex estimate underlines the financial strain on smaller aerospace platers.

South America and the Middle East & Africa together command the least market share, but the latter is expected to grow at the fastest 6.31% CAGR to 2031. Saudi Arabia's Vision 2030 funds captive plating for defense and construction, while South Africa's chromite reserves anchor global Cr(III) salt supply despite labor disruptions that reverberate through the trivalent chromium finishing market worldwide.

- Asterion, LLC

- Atotech

- Chem Processing, Inc.

- Columbia Chemical

- DIPSOL Chemicals Co., Ltd.

- ECS Environmental Solutions

- Freudenberg SE

- Hohman Plating & Mfg.

- Integer Holdings

- JCU International, Inc.

- Kakihara Industries Co., Ltd.

- MacDermid Enthone

- Master Finish Co.

- Nihon Parkerizing Co., Ltd.

- Quaker Houghton

- Ronatec C2C, Inc.

- SurTec Group

- TIB Chemicals AG

- Uyemura

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strict environmental regulations limiting Cr (VI) use

- 4.2.2 EV battery-pack connectors require Cr (III) passivation

- 4.2.3 Automotive lightweighting demands corrosion-proof finishes

- 4.2.4 Aerospace shift toward high-efficiency trivalent hard-chrome

- 4.2.5 Micro-throwing-power edge for complex 3-D printed metal parts

- 4.3 Market Restraints

- 4.3.1 Capex for converting legacy Cr (VI) plating lines

- 4.3.2 Limited high-temperature wear resistance vs. hard-chrome

- 4.3.3 Volatile supply and price of high-purity Cr (III) salts

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Plating

- 5.1.2 Conversion Coatings

- 5.1.3 Passivation

- 5.1.4 Other Finishing Types (Anodizing, Electro-coloring, etc.)

- 5.2 By Base Material

- 5.2.1 Steel and Stainless Steel

- 5.2.2 Aluminum and Alloys

- 5.2.3 Zinc and Alloys

- 5.2.4 Magnesium

- 5.2.5 Other Metals (Copper, Nickel, etc.)

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace and Aviation

- 5.3.3 Appliances and Electronics

- 5.3.4 Construction

- 5.3.5 Machinery and Heavy Equipment

- 5.3.6 Consumer Goods

- 5.3.7 Other End-user Industries (Medical, Defense, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Asterion, LLC

- 6.4.2 Atotech

- 6.4.3 Chem Processing, Inc.

- 6.4.4 Columbia Chemical

- 6.4.5 DIPSOL Chemicals Co., Ltd.

- 6.4.6 ECS Environmental Solutions

- 6.4.7 Freudenberg SE

- 6.4.8 Hohman Plating & Mfg.

- 6.4.9 Integer Holdings

- 6.4.10 JCU International, Inc.

- 6.4.11 Kakihara Industries Co., Ltd.

- 6.4.12 MacDermid Enthone

- 6.4.13 Master Finish Co.

- 6.4.14 Nihon Parkerizing Co., Ltd.

- 6.4.15 Quaker Houghton

- 6.4.16 Ronatec C2C, Inc.

- 6.4.17 SurTec Group

- 6.4.18 TIB Chemicals AG

- 6.4.19 Uyemura

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Replacement opportunity for hexavalent chromium finishing

- 7.3 Decorative-functional hybrid coatings

- 7.4 In-line recycling and zero-liquid-discharge plating systems