|

시장보고서

상품코드

2062028

스테인리스강 400 시리즈 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Stainless Steel 400 Series - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

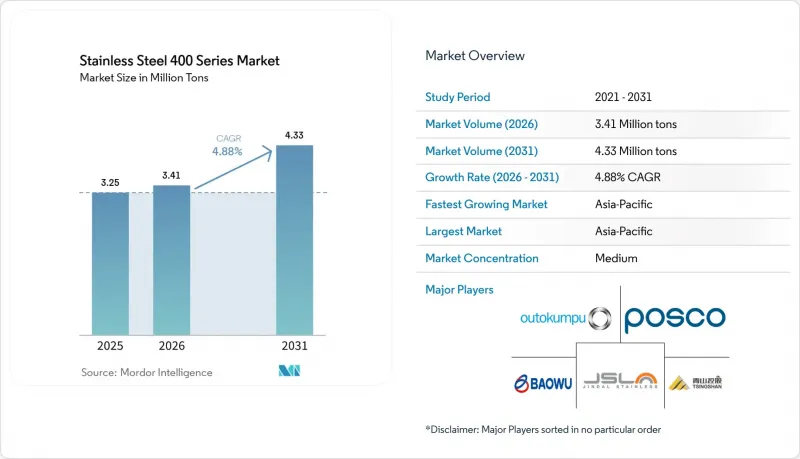

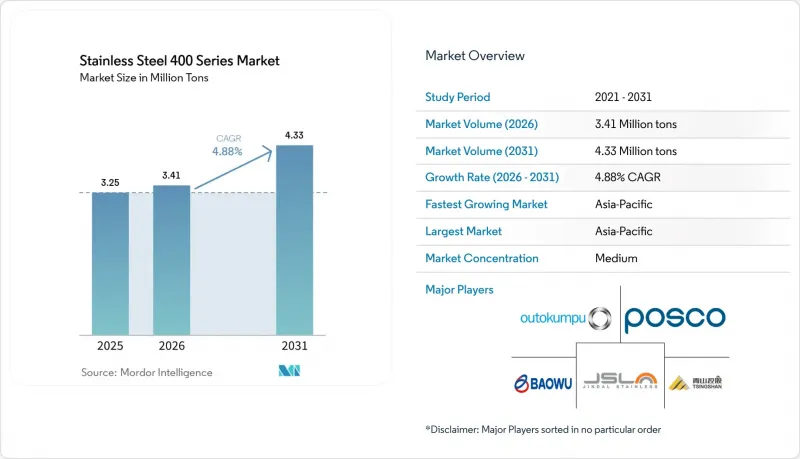

Mordor Intelligence에 의하면, 스테인리스강 400 시리즈 시장 규모는 2025년 325만 톤으로 평가되었고, 2026년에는 341만 톤으로 추정되겸, 2031년까지 433만 톤에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR)은 4.88%가 될 것으로 전망됩니다.

본 보고서는 등급별(409, 410, 기타), 제품 유형별(시트 플레이트, 코일, 기타), 용도별(자동차 배기 시스템, 기타), 최종 이용 산업별(자동차 및 운송, 건축 및 건설, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

세계의 스테인리스강 400 시리즈 시장 동향 및 분석

건설 및 인프라 지출 증가

중국의 2026년도 중앙 예산에서는 도시 건설 사업에 7,550억 위안(1,092억 2,000만 달러), 스테인리스 구조 제품을 우대하는 초장기 국채에 8,000억 위안(1,157억 3,000만 달러)이 계상되어 있어, 교량, 수도관, 대중교통 시설 개보수 분야의 페라이트계 강종 수요를 뒷받침하고 있습니다. 크롬 함량 16-18%인 430 등급은 내식성과 성형성의 균형이 뛰어나기 때문에 교량의 데크판이나 농업 기계 분야에서 아연 도금 강재를 대체하고 있습니다. 인도의 생산 연계형 인센티브 제도에서는 스테인리스 장형 제품의 증분 판매에 대해 4-15%의 보조금이 지급되어, 새로운 페라이트계 용강 공장의 설립이 촉진되고 있습니다. 중국 농촌 지역의 상수도 안전화 사업이 전개됨에 따라, 그동안 상수도 시설이 갖춰지지 않았던 현에도 스테인리스 배관이 보급되면서 잠재적 시장 규모가 확대되고 있습니다. 만안 지역이나 동남아시아의 메가 프로젝트는 지리적 범위를 확대하지만, 그 실행은 여전히 공공재정의 사이클과 투입 가격의 안정성에 좌우됩니다.

니켈 가격 변동 하에서 오스테나이트계 등급의 비용 경쟁력

409 등급의 거래 가격은 톤당 1,800-2,200달러인 반면, 304 등급은 3,000-3,500달러이며, 니켈 가격이 톤당 1만 8,000달러를 넘으면 이 가격 차이는 더욱 벌어집니다. 인도네시아는 전 세계 니켈 광석의 약 70%를 공급하고 있지만, 2026년 할당량이 축소됨에 따라 2021년 정점 대비 40% 하락했던 가격이 회복되었습니다. 니켈을 거의 또는 전혀 포함하지 않는 페라이트계 등급은 OEM의 예산을 압박하지 않으면서, 배기 시스템, 가전제품 패널, 재압연 업체의 원료 분야에서 대체 수요를 창출하고 있습니다. 니켈 가격이 하락하면, 내식성 향상이 필수적인 부문에서 오스테나이트계 강재가 시장 점유율을 회복하게 되며, 최종 시장 전체에서 가격 탄력성에 따른 가격 변동이 두드러지게 나타납니다.

크롬과 페로크롬의 가격 변동

2026년 초, 인도의 페로크롬 가격은 톤당 74,000-75,000 루피(784.17-794.77 달러)에 달했습니다. 한편, 중국의 수입 제안 가격은 파운드당 약 0.84달러로, 남아프리카공화국의 생산 감축으로 인한 공급 제약을 반영한 것이었습니다. 탄소국경조정메커니즘(CBAM)은 검증되지 않은 수입품에 대해 3.5-4톤의 기본 이산화탄소(CO2) 계수를 적용하고 있으며, 그 결과 고로제 스테인리스 스틸에 대한 과세 및 전기 아크로(EAF)의 프리미엄 상승으로 이어지고 있습니다. 가격 변동 가능성에 대비하기 위해 중국의 국영 광산 기업들은 해외에서 5억 톤 이상의 크롬철광을 확보했습니다. 자체 광석 자원을 보유하지 않은 제철소는 페로크롬 가격 상승 시 이익률 압박에 직면하고 있으며, 이는 수직 통합형 생산자 간의 통합을 촉진하고 있습니다.

부문별 분석

2025년 기준으로, 409 등급은 스테인리스강 400 시리즈 시장 점유율의 41.11%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 5.45%로 확대될 것으로 전망됩니다. 자동차 배기관용 스테인리스강 400 시리즈 시장 규모는 409 등급의 10.5-11.75% 크롬 함유량으로 인한 내열성(600℃의 가스를 견딤)과 304 등급의 절반 수준인 비용이라는 장점에 힘입어 성장하고 있습니다. 430 등급은 중국의 가전제품 교체 장려 정책에 힘입어 가전제품 및 건축용 패널 시장에서 수요가 확대되고 있습니다. 마르텐사이트계 410, 420, 440 등급은 55 HRC 이상의 경도를 구현하여, 외과용 기구 및 산업용 나이프 시장 수요를 주도하고 있습니다. 니치 시장용 446 등급은 23-27%의 크롬 함유량으로 인해 용광로 내벽재나 열교환기에 사용되지만, 합금 할증료가 높게 책정되어 있습니다.

T4003이나 SOLEIL 4003과 같은 신흥 페라이트계 강종은 13% 이하의 크롬 함량과 티타늄 안정제를 조합함으로써, 열차 차체나 교량 상판용의 용접성과 연성을 향상시키고 있습니다. 신일본제철이 특허를 취득한 표면 활성화 처리는 산화 피막의 안정성을 높여, 600°C에서 산화에 의한 중량 증가를 0.3 mg/cm²로 억제하며, 습한 환경의 열교환기에서 수명을 연장합니다. 각 제조업체들은 단순한 금속 조직뿐만 아니라 코팅 및 산세척 기술력을 통해 차별화를 꾀하는 경우가 늘고 있습니다.

2025년에는 시트와 플레이트가 전체의 42.32%를 차지한 것으로 평가되었으며, 이는 매끄러운 표면과 정확한 두께가 요구되는 가전제품 외장, 클래딩, 차체 패널로의 용도를 반영한 것입니다. 봉강과 봉재 시장은 정밀 기계 가공된 밸브 및 기어, 그리고 0.15-0.30%의 황을 함유한 가공성 416강종에 대한 수요에 힘입어 5.67%라는 가장 높은 연평균 성장률(CAGR)을 달성할 것으로 전망됩니다. 코일은 수 톤 단위의 전체 로트에 걸쳐 일관된 화학 성분을 중시하며, 서비스 센터 및 재압연 업체의 요구에 부응하고 있습니다. 파이프와 튜브는 건설 및 에너지 부문에 공급되는 반면, 두께 0.1mm 이하의 박막은 고체산화물 연료전지(SOFC) 및 전해조 스택을 뒷받침하며, 스테인리스강 400 시리즈 시장에서 높은 수익률을 기록하는 부문을 형성하고 있습니다.

중국의 제철소들은 산업 기준을 높여가고 있습니다. 푸순 제철의 빅데이터 제어를 통해 강판 정밀도가 65% 향상되었으며,? 양더롱은 세계 최대 폭인 2,680mm의 열간 압연기를 가동하고 있으며, 산시푸젠은 1,550mm 20롤 냉간 압연기를 도입하여 마이크론 수준의 공차를 실현하고 있습니다. 2B에서 8K에 이르는 표면 마감에는 10-30%의 프리미엄이 붙으며, 이것이 연마 공정에 대한 투자를 촉진하고 있습니다. 와이어 아크 직접 에너지 적층(DED) 기술은 대규모 보수 시 원자재 사용량을 78% 절감하지만, 여전히 기존 압연 방식에 비해 시트 처리 능력 면에서 효율이 낮아 기존 압연 방식이 여전히 주류를 이루고 있습니다.

지역별 분석

아시아태평양은 2025년 생산량의 52.34%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 5.72%로 성장할 전망입니다. 이는 중국의 7,550억 위안(1,092억 2,000만 달러) 규모의 인프라 예산과 2,500억 위안(361억 6,000만 달러) 규모의 가전제품 교체 지원 계획에 의해 뒷받침되고 있습니다. 중국 상위 3대 제철소는 2024년 스테인리스 스틸 생산량의 67.30%를 차지하며, 공급을 통합해 협상력을 높였습니다. 인도의 가동률은 750만 톤의 생산 능력 대비 60% 전후로 유지되고 있어, 페라이트계 강철의 증산 여지가 있습니다. 또한, 진달(Jindal)의 인도네시아 내 120만 톤 용해 공장은 지역의 자급자족 체제를 강화하고 있습니다. 인도네시아의 포스코-칭산 합작 사업은 자사 광석을 원료로 하는 200만 톤의 생산 능력을 추가하여, 해당 국가를 저비용 허브로 자리매김하고 있습니다.

미국 자동차 산업에서는 여전히 409 등급이 주류를 이루고 있지만, 전기차의 보급으로 인해 차량당 스테인리스 사용량은 감소하고 있습니다. 미국, 캐나다, 멕시코에 걸쳐 있는 다층적인 관세 체계가 무역을 복잡하게 만들면서, 구매자들이 지역 제철소로 눈을 돌리고 있습니다.

유럽은 CBAM(탄소국경조정메커니즘)에 직면하여, 기본 CO2 계수를 적용함으로써 배출량이 많은 수입품의 입고 비용을 인상하고 있습니다. 아웃쿰프(Outcomp)사가 2억 유로(2억 2,965만 달러)를 투자한 토르니오 공장 개보수 사업은 이상강 및 석출경화형 강종으로의 전환을 핵심으로 하고 있으며, 한편, 아셀리녹스사와 아펠람사는 수요 부진 속에서 에너지 사용량을 억제하기 위해 1억 6,000만 유로(1억 8,372만 달러)를 투자하고 있습니다. 독일과 북유럽 국가들은 전해조 도입을 주도하고 있으며, 금속 양극판을 선호하여 채택하고 있습니다. 남미와 중동 및 아프리카는 여전히 시장 점유율이 낮고 환율 리스크도 존재하지만, 현지 가전제품 및 건설 수요의 혜택을 누리고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the stainless steel 400 series market size is projected to grow from 3.25 million tons in 2025 to 3.41 million tons in 2026 to reach 4.33 million tons by 2031, growing at a CAGR of 4.88% from 2026 to 2031.

This report is Segmented by Grade (409, 410, and More), Product Type (Sheets and Plates, Coils, and More), Application (Automotive Exhaust Systems, and More), End-Use Industry (Automotive and Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Stainless Steel 400 Series Market Trends and Insights

Growth in Construction and Infrastructure Spending

China's 2026 central budget sets aside CNY 755 billion (USD 109.22 billion) for municipal works and CNY 800 billion (USD 115.73 billion) in ultra-long treasury bonds that favor stainless structural products, propelling demand for ferritic grades in bridges, water pipelines, and public-transit upgrade. Grade 430, with 16-18% chromium, replaces galvanized steels in bridge decks and agricultural equipment because it balances corrosion resistance and formability. India's production-linked incentive scheme grants 4-15% on incremental stainless long-product sales, encouraging new ferritic melt shops. Rural water-safety rollouts in China extend stainless piping into previously untreated counties, enlarging the addressable base. Mega-projects in the Gulf and Southeast Asia broaden geographic exposure, though execution still hinges on public-finance cycles and input-price stability.

Cost Advantage Over Austenitic Grades Amid Nickel Volatility

Grade 409 trades at USD 1,800-2,200 per ton versus USD 3,000-3,500 for 304, a gap that widens when nickel surpasses USD 18,000 per ton. Indonesia supplies roughly 70% of global nickel ore, yet stricter 2026 quotas revived pricing after a 40% slide from 2021 peaks. Ferritic grades, containing little to no nickel, insulate OEM budgets and trigger substitution in exhausts, appliance panels, and re-rollers' feedstock. When nickel retreats, austenitic grades claw back share where higher corrosion thresholds are essential, underscoring a price-elastic see-saw across end markets.

Chromium and Ferrochrome Price Volatility

In early 2026, India's ferrochrome prices reached INR 74,000-75,000 (USD 784.17-794.77) per ton. Meanwhile, Chinese import offers were around USD 0.84 per pound, reflecting supply constraints due to production curtailments in South Africa. The Carbon Border Adjustment Mechanism (CBAM) applies default carbon dioxide (CO2) factors of 3.5-4.0 tons to unverified imports, resulting in taxes on blast-furnace stainless steel and higher Electric Arc Furnace (EAF) premiums. To address potential price fluctuations, China's state-owned mining companies secured over 500 million tons of chromite from international sources. Mills without captive ore resources face margin pressures during ferrochrome price increases, driving consolidation among vertically integrated producers.

Other drivers and restraints analyzed in the detailed report include:

- Rising Usage in Kitchenware and Home Appliances

- Adoption in Bipolar Plates for Green-Hydrogen Electrolyzers

- Additive-Manufacturing Cracking and Printability Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Grade 409 accounted for 41.11% of the stainless steel 400 series market share in 2025 and is projected to expand at 5.45% CAGR to 2031. The stainless steel 400 series market size for automotive exhaust lines benefits from grade 409's 10.5-11.75% chromium chemistry that withstands 600°C gases at half the cost of 304. Grade 430 capitalizes on appliance and architectural panels, buoyed by China's appliance-trade-in bounty. Martensitic 410, 420, and 440 grades deliver greater than or equal to 55 HRC hardness, fueling surgical-instrument and industrial-knife demand. Niche grade 446 services furnace linings and heat exchangers thanks to 23-27% chromium, but trades at a higher alloy surcharge.

Emerging ferritic variants such as T4003 and SOLEIL 4003 marry smaller than or equal to 13% chromium with titanium stabilizers, improving weldability and ductility for train shells and bridge decks. Patented surface activation by Nippon Steel enhances oxide-film stability, shrinking oxidation weight gain to 0.3 mg/cm2 at 600°C and extending service life in humid heat exchangers. Producers increasingly differentiate through coating and pickling know-how rather than raw metallurgy alone.

In 2025, sheets and plates accounted for 42.32% of the volume, reflecting their application in appliance skins, cladding, and body panels that require smooth surfaces and precise gauges. Bars and rods are projected to achieve the highest compound annual growth rate (CAGR) of 5.67%, driven by demand for precision-machined valves, gears, and the free-cutting 416 variant containing 0.15-0.30% sulfur. Coils address the needs of service centers and re-rollers, focusing on consistent chemistry across multi-ton lots. Pipes and tubes cater to the construction and energy sectors, while foils thinner than 0.1 mm support solid oxide fuel cell (SOFC) and electrolyzer stacks, creating a high-margin segment within the stainless steel 400 series market.

China's mills are advancing industry benchmarks: Fushun's big-data controls have improved plate precision by 65%, Liyang Delong operates the world's widest 2,680 mm hot mill, and Shanxi Fujian has implemented a 1,550 mm 20-roll cold mill, achieving micron-level tolerances. Surface finishes ranging from 2B to 8K command premiums of 10-30%, driving investments in polishing processes. While wire-arc directed energy deposition (DED) technology reduces raw material usage by 78% during large repairs, it remains less efficient in sheet throughput compared to conventional rolling, which continues to dominate.

Geography Analysis

Asia-Pacific commanded 52.34% of 2025 volume and is advancing at a 5.72% CAGR to 2031, underscored by China's CNY 755 billion (USD 109.22 billion) infrastructure budget and CNY 250 billion (USD 36.16 billion) appliance-trade-in plan. China's top three mills captured 67.30% of 2024 stainless output, consolidating supply and raising bargaining power. India's utilization hovers near 60% against 7.5 million t capacity, giving headroom for ferritic ramp-ups; Jindal's 1.2 million ton Indonesian melt shop reinforces regional self-sufficiency. Indonesia's POSCO-Tsingshan venture adds 2 million t of captive-ore-fed capacity, positioning the archipelago as a low-cost hub.

U.S. automotive still pulls grade 409, but EV diffusion trims per-vehicle stainless loadings. Tariff layers across the U.S., Canada, and Mexico entangle trade, steering buyers toward regional mills.

Europe confronts CBAM, allocating default CO2 factors that inflate landed costs for high-emission imports. Outokumpu's EUR 200 million (USD 229.65 million) Tornio upgrade pivots to duplex and precipitation-hardened grades, while Acerinox and Aperam sink EUR 160 million (USD 183.72 million) to curb energy use amid soft demand. Germany and the Nordics spearhead electrolyzer rollouts, favoring metallic bipolar plates. South America and MEA remain smaller slices but gain from localized appliance and construction needs despite currency risk.

- Acerinox

- Aperam

- Baosteel Desheng Stainless Steel Co., Ltd.

- Eternal Tsingshan Group Co., Ltd.

- Fushun Special Steel Co., Ltd.

- Jindal Steel

- NIPPON STEEL CORPORATION

- Outokumpu

- POSCO

- Shanxi Taigang Stainless

- Shyam Metalics

- Viraj Profiles Pvt. Ltd.

- Yieh Corp.

- China Baowu Steel Group

- TSINGSHAN HOLDING GROUP

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in construction and infrastructure spending

- 4.2.2 Cost advantage over austenitic grades amid nickel volatility

- 4.2.3 Rising usage in kitchenware and home appliances

- 4.2.4 Adoption in bipolar plates for green-hydrogen electrolyzers

- 4.2.5 Demand for ultra-thin ferritic foils in solid-oxide fuel cells and metal-supported batteries

- 4.3 Market Restraints

- 4.3.1 Chromium and ferro-chrome price volatility

- 4.3.2 Additive-manufacturing cracking and printability issues

- 4.3.3 Carbon-border-adjustment and lifecycle-CO2 rules raising compliance costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 409

- 5.1.2 410

- 5.1.3 420

- 5.1.4 430

- 5.1.5 440

- 5.1.6 Other Grades (446, etc.)

- 5.2 By Product Type

- 5.2.1 Sheets and Plates

- 5.2.2 Coils

- 5.2.3 Bars and Rods

- 5.2.4 Pipes and Tubes

- 5.2.5 Other Product Types (Ultra-thin foil, etc.)

- 5.3 By Application

- 5.3.1 Automotive Exhaust Systems

- 5.3.2 Kitchenware and Cookware

- 5.3.3 Industrial Equipment

- 5.3.4 Construction and Architecture

- 5.3.5 Electrical Appliances

- 5.3.6 Energy Generation

- 5.3.7 Other Applications (Hydrogen Electrolyzer Plates, etc.)

- 5.4 By End-User Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Building and Construction

- 5.4.3 Consumer Goods

- 5.4.4 Industrial Machinery

- 5.4.5 Energy and Power

- 5.4.6 Aerospace and Defense

- 5.4.7 Other End-user Industries (Healthcare, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Initiatives

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Acerinox

- 6.4.2 Aperam

- 6.4.3 Baosteel Desheng Stainless Steel Co., Ltd.

- 6.4.4 Eternal Tsingshan Group Co., Ltd.

- 6.4.5 Fushun Special Steel Co., Ltd.

- 6.4.6 Jindal Steel

- 6.4.7 NIPPON STEEL CORPORATION

- 6.4.8 Outokumpu

- 6.4.9 POSCO

- 6.4.10 Shanxi Taigang Stainless

- 6.4.11 Shyam Metalics

- 6.4.12 Viraj Profiles Pvt. Ltd.

- 6.4.13 Yieh Corp.

- 6.4.14 China Baowu Steel Group

- 6.4.15 TSINGSHAN HOLDING GROUP

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment