|

시장보고서

상품코드

2062030

마이크로 사출성형 플라스틱 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Micro Injection Molded Plastic - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

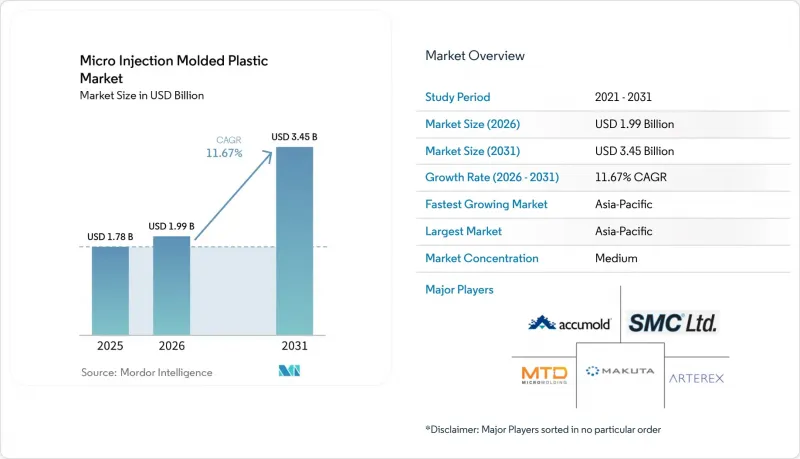

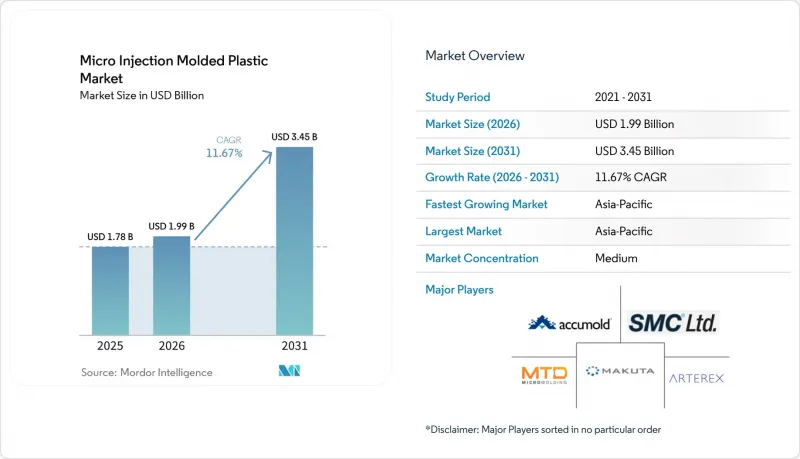

Mordor Intelligence에 의하면, 마이크로 사출성형 플라스틱 시장 규모는 2025년 17억 8,000만 달러로 평가되었고, 2026년에는 19억 9,000만 달러로 추정되고, 2031년까지 34억 5,000만 달러에 이를 것으로 예상되고 있으며, 2026-2031년 CAGR 11.67%로 성장할 전망입니다.

본 보고서는 소재별(폴리에테르에테르케톤, 액정 폴리머, 폴리카보네이트, 폴리에틸렌, 기타), 최종 이용 산업별(의료 진단, 자동차 및 운송, 전기 및 전자, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 마이크로 사출 성형 플라스틱 시장 동향 및 분석

자동차용 센서 분야의 정밀 플라스틱 수요

첨단 운전자 보조 시스템(ADAS)이 탑재된 차량에는 최대 30개의 개별 센서가 장착되어 있으며, 각 센서는 -40°C에서 150°C의 온도 변화 주기를 견디고, 0.05mm를 초과하는 치수 변형을 일으키지 않는 폴리머 재질의 케이스에 담겨 있습니다. 이로 인해 77GHz 레이더 신호를 감쇠시키는 알루미늄 다이캐스팅 부품의 사용이 불필요해집니다. PEEK 및 LCP 소재의 레이돔은 기계 가공된 금속에 비해 부품 단가를 60% 절감했으며, 2024년에 출시된 폴리카보네이트 소재의 루프 센서 모듈은 씰과 보스를 18초간의 단일 사출 성형 공정을 통해 일체화함으로써, 물 유입으로 인한 보증 청구 건수를 40% 줄였습니다. 자동차 제조업체들은 집중형 존 컨트롤러로의 재설계를 추진 중이며, 2028년까지 센서의 설치 면적을 30% 축소할 계획입니다. 이를 위해서는 0.5mm 이하의 두께가 필요하지만, 이를 반복 성형할 수 있는 것은 50톤 이하의 프레스기뿐입니다.

MEMS 실리콘에서 내열성 폴리머로의 전환

실리콘 소재의 마이크로 전자 기계식 다이(MEMS 다이)는 개당 2-4달러이며, 1,500G를 초과하면 파손되지만, 성형 폴리머는 개당 0.80-1.20달러로 동등한 성능을 발휘하며, 125 °C에서 2,000시간의 에이징 테스트에서도 2% 이하의 드리프트로 견딜 수 있습니다. 2025년에 TSMC와 Samsung Electronics로부터 인증받은 LCP 기판은 AIP(안테나 인 패키지) 모듈을 지원하여, 이로 인해 별도의 RF 커넥터가 필요 없어지고 28GHz에서 삽입 손실을 0.8 dB 저감합니다. 2028년까지 폴리머는 첨단 노드의 칩렛의 20%를 차지할 것으로 예상되지만, 항공우주 분야에서는 여전히 100kRad를 초과하는 방사선 내성을 지닌 실리콘이 선호되고 있습니다.

초정밀 금형 제조업체의 부족

128 캐비티 금형에서 ±1 마이크로미터의 정밀도를 구현할 수 있는 공구 제조업체는 전 세계적으로 50개사 미만이며, 2025년의 리드타임은 22주까지 늘어났습니다. 유와 코퍼레이션의 생산망은 아시아태평양의 0.1g 이하 사출 성형 수요의 불과 12%만을 충당하고 있는 반면, 8억 달러 규모의 북미 생산 복귀 계획은 숙련된 기계 기술자의 15%가 매년 은퇴하고 있어 지연될 위험에 직면해 있습니다. LCP 금형은 등방성 소재에 비해 가공 시간이 40% 더 소요되기 때문에 생산 능력 부족 문제를 더욱 악화시키고 있습니다.

부문별 분석

폴리에테르에테르케톤(PEEK)은 2025년 매출의 35.11%를 차지했으며, 이는 척추 임플란트 및 150℃ 환경에서 사용되는 자동차용 센서 분야에서의 확고한 입지를 반영한 것입니다. 2026-2031년 액정 폴리머가 연평균 성장률(CAGR) 12.10%를 기록할 것으로 예측되며, 고주파 포장용 마이크로 사출 성형 플라스틱 시장 규모가 재편될 전망입니다. 이는 액정 폴리머의 접선 손실이 0.002이므로, 폴리이미드에 비해 mm파(mmWave)의 삽입 손실이 절반으로 줄어들기 때문입니다. 폴리카보네이트는 89%의 투명도를 자랑하며 안과용 기기 시장에서 우위를 점하고 있지만, 유리전이온도(Tg)가 147℃에 달하기 때문에 엔진룸 내 적용에는 한계가 있습니다. 사이클로올레핀 공중합체는 100°C의 온도 변화를 견뎌도 뒤틀림이 발생하지 않는 현장 진단용 PCR 플레이트의 기판으로 사용됩니다. 반면, 폴리에틸렌과 폴리프로필렌은 개당 0.10달러 이하의 실험용 기구 분야에서 여전히 비용 효율성을 중시하는 선택지로 자리 잡고 있습니다.

현재 설비 투자의 초점은 PEEK 및 LCP 성형품에서 CpK 값 1.67 이상을 확보하기 위한 폐쇄 루프 방식의 금형 온도 제어기 및 인라인 CT 스캐너로 옮겨가고 있습니다. 이러한 설비 투자 증가는 중견 수탁 성형 업체들 시장 진입 장벽을 높여, 소재 집약적인 틈새 시장에서 마이크로 사출 성형 플라스틱 산업의 집중화를 더욱 가속화할 것으로 보입니다. 용융 온도를 ±5°C 이내로 제어할 수 있음을 보장할 수 있는 공급업체는 범용 성형 업체로부터 마이크로 사출 성형 플라스틱 시장 점유율을 더욱 확대할 수 있는 입장에 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 41.12%를 차지했으며, 중국의 정밀 금형 산업이 2030년까지 1조 위안 규모의 생산액을 목표로 하는 가운데, 2026-2031년 연평균 성장률(CAGR) 12.51%로 성장할 것으로 전망됩니다. 일본 금형 제조업체가 자랑하는 ±0.01mm의 정밀도에는 15-20%의 프리미엄이 붙지만, 임플란트 부문에서는 여전히 필수적이며, 한편 한국의 반도체 패키징이 현지 LCP 소비를 주도하고 있습니다. 아세안은 2024년에 310억 달러 규모의 전자 부문 외국인 직접투자(FDI)를 유치했으며, 베트남과 말레이시아는 '중국 플러스 원' 전략의 생산 거점으로서의 입지를 확고히 하고 있습니다.

북미와 유럽의 성장률은 아시아태평양보다 3-4% 뒤처져 있습니다. 미국에는 2025년 매출이 4억 6,000만 달러에 달한 것으로 평가되는, 테시 플라스틱(Tessy Plastics)을 포함해 세계 최대 15개 마이크로 성형 제조업체 중 8곳이 거점을 두고 있으나, 초정밀 금형 제조업체의 부족으로 인해 신규 금형의 리드타임은 22주를 초과하고 있습니다. 독일 바덴뷔르템베르크주와 바이에른주의 클러스터는 프라운호퍼 IPT의 계측 기술을 활용하여 불량률을 0.15%로 억제하고, 5,000개 단위의 경제적인 생산을 실현하고 있습니다. 2024년에 전면 시행된 EU 의료기기 규정의 추적성 요건으로 인해, 최초 의료기기 신청에 8-12주의 추가 기간이 필요하게 되어, ISO 13485 인증을 취득한 기존 기업들이 유리한 입장에 있습니다.

남미와 중동 및 아프리카에서는 시장이 눈에 띄게 성장하고 있습니다. 브라질에서는 2027년에 시행될 센서 국내 조달률 60% 규정에 따라, 1차 공급업체는 3개의 현지 성형 업체를 사전 인증해야 합니다. 사우디아라비아의 킹 살만 메디컬 시티 입찰에서는 국내 ISO 13485 인증을 취득한 공급업체가 지정되어 있어, 이를 통해 연간 1억 2,000만 달러 규모 수요가 창출되고 있으나, 현재는 그 중 90%가 수입품으로 충당되고 있습니다. 아르헨티나에서는 통화 변동에 따라 계약이 유로화로 전환되는 반면, 이집트와 모로코에서는 2028년까지 사전 충전 주사기의 현지 조달률 40%를 목표로 하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the micro injection molded plastic market size is expected to increase from USD 1.78 billion in 2025 to USD 1.99 billion in 2026 and reach USD 3.45 billion by 2031, growing at a CAGR of 11.67% over 2026-2031.

This report is Segmented by Material (Polyether Ether Ketone, Liquid Crystal Polymers, Polycarbonate, Polyethylene, and More), End-Use Industry (Healthcare and Diagnostics, Automotive and Transportation, Electrical and Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Micro Injection Molded Plastic Market Trends and Insights

Precision-Plastic Needs in Automotive Sensors

Advanced driver-assistance vehicles contain up to 30 discrete sensors, each housed in polymer enclosures that tolerate -40°C to 150°C cycles without dimensional creep beyond 0.05 mm, eliminating aluminum die-castings that attenuate 77 GHz radar signals. PEEK and LCP radomes cut per-part costs 60% versus machined metal, and a 2024 polycarbonate roof-sensor module integrated seals and bosses in one 18-second shot, reducing warranty water-ingress claims by 40%. Automakers are redesigning toward centralized zone controllers, shrinking sensor footprints 30% by 2028, which requires wall thicknesses below 0.5 mm that only presses under 50 tons can repeatably mold.

Migration from MEMS Silicon to High-Temperature Polymers

Silicon micro-electromechanical dies cost USD 2-4 each and fracture above 1,500G, whereas molded polymers deliver similar performance for USD 0.80-1.20 per part and survive 2,000-hour 125 °C aging with less than 2% drift. LCP substrates, qualified by TSMC and Samsung in 2025, support antenna-in-package modules that remove discrete RF connectors and cut 28 GHz insertion loss by 0.8 dB. By 2028, polymers are expected to carry 20% of advanced-node chiplets, though aerospace still favors radiation-hard silicon above 100 kilorads.

Scarcity of Ultra-Precision Toolmakers

Fewer than 50 tool shops worldwide hold +-1 µm capability across 128-cavity molds, and 2025 lead times stretched to 22 weeks. Yuwa Corporation's network covers only 12% of Asia-Pacific sub-0.1 g shot demand, while North American reshoring plans worth USD 800 million risk delays because 15% of senior machinists retire annually. LCP molds exacerbate capacity strain by needing 40% more machining hours than isotropic materials.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Minimally-Invasive Drug-Delivery Systems

- AI-Enabled In-Line Metrology Cutting Scrap Below 0.2%

- Limited Global Supply of Implant-Grade Bio-Absorbable Polymers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyether ether ketone (PEEK) accounted for 35.11% of 2025 revenue, reflecting entrenched use in spinal implants and 150°C automotive sensors. Liquid crystal polymers' 12.10% CAGR during 2026-2031 will reshape the micro injection molded plastic market size for high-frequency packages because their 0.002 loss tangent halves mmWave insertion loss versus polyimide. Polycarbonate holds ophthalmic devices owing to 89% transparency, although its 147°C Tg limits under-hood deployment. Cyclic olefin copolymer underpins point-of-care PCR plates that endure 100°C cycling without warpage, whereas polyethylene and polypropylene remain cost-driven choices for labware priced under USD 0.10 per part.

Equipment investments now pivot around closed-loop mold-temperature controllers and inline CT scanners that secure CpK greater than or equal to1.67 for PEEK and LCP geometries. That uptick in capital elevates barriers for mid-tier contract molders and will keep the micro injection molded plastic industry concentrated in fewer hands within material-intensive niches. Suppliers able to guarantee melt-temperature control within +-5°C are positioned to capture additional micro injection molded plastic market share from commodity molders.

Geography Analysis

Asia-Pacific owned 41.12% of 2025 revenue and is forecast to expand at 12.51% CAGR during 2026-2031 as China's precision-mold industry heads toward CNY 1 trillion output by 2030. Japanese toolmakers' +-0.01 mm capability commands 15-20% premiums but remains essential for implants, while South Korea's semiconductor packaging drives local LCP consumption. ASEAN nations attracted USD 31 billion in 2024 electronics FDI, positioning Vietnam and Malaysia as overflow hubs within China-plus-one strategies.

North America and Europe trail Asia-Pacific growth by 3-4 points. The United States hosts eight of the fifteen largest micro-molders, including Tessy Plastics with USD 460 million in 2025 sales, but a shortage of ultra-precision toolmakers has pushed new-mold lead times past 22 weeks. Germany's Baden-Wurttemberg and Bavaria clusters leverage Fraunhofer IPT metrology to sustain scrap at 0.15% and enable economical 5,000-part runs. EU Medical Device Regulation traceability rules, fully enforced in 2024, tack on 8-12 weeks to first-time device filings, favoring incumbents with ISO 13485 pedigrees.

South America and Middle East-Africa are witnessing considerable market growth. Brazil's 60% domestic-content rule for sensors, effective 2027, is forcing Tier-1s to pre-qualify three local molders. Saudi Arabia's King Salman Medical City tenders specify domestic ISO 13485 suppliers, creating USD 120 million annual demand currently met 90% by imports. Currency volatility in Argentina pushes contracts toward euro denomination, while Egypt and Morocco pursue 40% local content in pre-filled syringes by 2028.

- Accu-Mold

- ARTEREX

- Ingersoll Rand

- Makuta, Inc.

- Medbio Inc.

- Microdyne Plastics

- Microsystems UK

- MTD Micro Molding

- Nissha Medical Technologies

- PreciKam

- Rapidwerks, Inc.

- SMC Ltd.

- Tessy Plastics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Precision-plastic needs in automotive sensors

- 4.2.2 Migration from MEMS silicon to high-temperature polymers

- 4.2.3 Rising adoption of minimally-invasive drug-delivery systems

- 4.2.4 AI-enabled in-line metrology cutting scrap below 0.2%

- 4.2.5 mmWave LCP connectors for 5G/6G antenna arrays

- 4.3 Market Restraints

- 4.3.1 Scarcity of ultra-precision toolmakers

- 4.3.2 Limited global supply of implant-grade bio-absorbable polymers

- 4.3.3 Resin lot-to-lot variability triggering device re-validation

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Polyether Ether Ketone (PEEK)

- 5.1.2 Liquid Crystal Polymers (LCP)

- 5.1.3 Polycarbonate (PC)

- 5.1.4 Polyethylene (PE)

- 5.1.5 Polyvinyl Chloride (PVC)

- 5.1.6 Polypropylene (PP)

- 5.1.7 Cyclic Olefin Copolymer (COC)

- 5.1.8 Other Materials

- 5.2 By End-user Industry

- 5.2.1 Healthcare and Diagnostics

- 5.2.2 Automotive and Transportation

- 5.2.3 Electrical and Electronics

- 5.2.4 Aerospace and Defence

- 5.2.5 Industrial and Energy

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Accu-Mold

- 6.4.2 ARTEREX

- 6.4.3 Ingersoll Rand

- 6.4.4 Makuta, Inc.

- 6.4.5 Medbio Inc.

- 6.4.6 Microdyne Plastics

- 6.4.7 Microsystems UK

- 6.4.8 MTD Micro Molding

- 6.4.9 Nissha Medical Technologies

- 6.4.10 PreciKam

- 6.4.11 Rapidwerks, Inc.

- 6.4.12 SMC Ltd.

- 6.4.13 Tessy Plastics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment