|

시장보고서

상품코드

2062036

침전 탄산칼슘 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Precipitated Calcium Carbonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

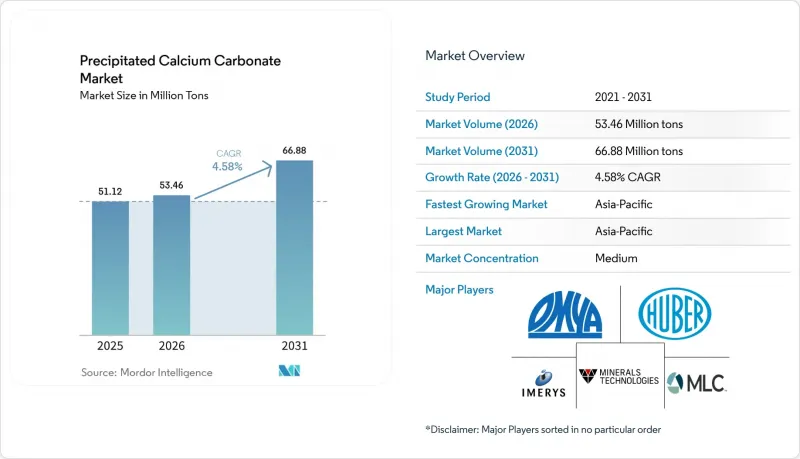

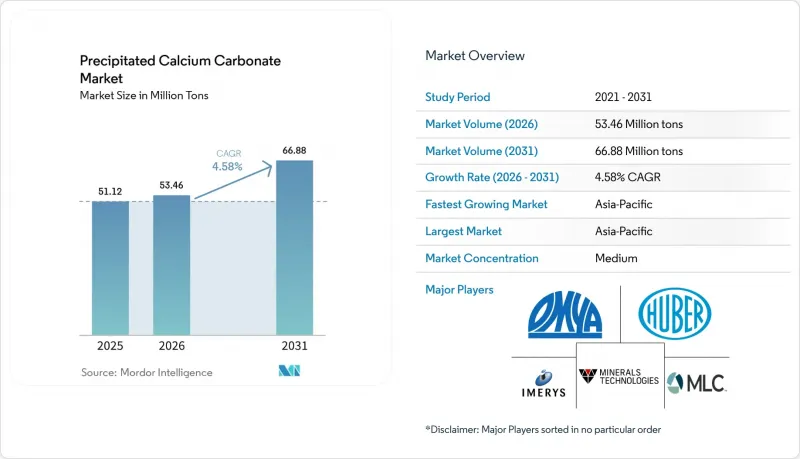

Mordor Intelligence에 의하면, 침전 탄산칼슘 시장 규모는 2025년에 5,112만 톤, 2026년에 5,346만 톤이 되어, 2031년까지 6,688만 톤에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 4.58%로 성장할 것으로 전망됩니다.

본 보고서에서는 용도별(종이 및 판지, 페인트 및 코팅, 접착제 및 실란트 등), 최종 사용자 산업별(포장, 건설 및 인프라, 자동차 및 운송 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 시장을 분류하고 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

세계 침전 탄산칼슘 시장 동향 및 분석

고급 용지 등급에 대한 수요 급증

브랜드 소유주들은 광산란을 극대화하기 위해 사방정계 PCC에 의존하는 고불투명도 포장용지나 코팅지로 전환하고 있으며, 이를 통해 강도를 저하시키지 않으면서 25% 이상의 충전제 함유율을 실현하고 있습니다. 크실란 개질 PCC를 함유한 실험용 핸드 시트는 밝기와 불투명도가 향상되었을 뿐만 아니라 파열 강도와 인열 강도도 개선되어, 제지 업체는 인쇄 품질을 유지하면서 섬유 등급을 낮출 수 있게 되었습니다. 재활용 섬유의 순환이 주류를 이루는 아시아에서는 나노 PCC가 자외선(UV)에 의해 퇴색하는 형광 증백제를 대체하여 비용 효율적인 백색도 조절을 실현하고 있습니다. 대리석 폐기물을 원료로 한 PCC를 사용한 파일럿 시험에서 103.3°의 접촉각을 달성하여 식품 포장재의 발수성을 향상시켰습니다. 이러한 결과는 차세대 PCC가 순수 섬유로는 실현할 수 없는 미적 및 지속가능성상의 이점을 제공한다는 사실을 입증하고 있습니다.

경량화를 위한 고충진 플라스틱

자동차 및 포장용 컨버터 업체들은 수지 비용 절감과 부품 중량 감소를 위해 최대 40%의 PCC 마스터배치를 배합하고 있으며, 이를 통해 연비가 직접적으로 향상됩니다. 40%의 분쇄 PCC를 배합한 폴리프로필렌 복합재에서는 영률이 69% 상승했으나, 설계자는 입자 크기를 조절하여 강성과 연성을 균형 있게 조정하고 있습니다. 오미야사의 Smartfill 개질 PCC는 PET의 고유 점도를 0.74 dL/g로 유지했습니다(일반 PCC는 0.61 dL/g). 이를 통해 충전율 5%에서 병의 내하중이 40% 향상되었으며, 이산화티타늄 사용량을 줄일 수 있게 되었습니다. PCC를 6중량% 함유한 유리섬유 에폭시 부품은 인장 강도가 130.58 MPa에 달하여, 전기차의 경량 차체 패널 개발의 길을 열었습니다. 2024년에 1,550만 대에 달할 것으로 예상되는 북미 자동차 생산 대수(대당 429파운드의 플라스틱 사용량)는 플라스틱 충전재에 대한 잠재적 수요 증가를 뒷받침하고 있습니다.

석회석의 가격 변동과 공급 현황

미국 지질조사국(USGS)은 2024년 석회 생산량을 4억 2,000만 톤으로 추산하고 있으며, 이 중 72%가 중국산인 만큼 수입업체들의 집중 위험이 높아지고 있습니다. 채석장 허가 기준이 강화되고 유류할증료가 인상됨에 따라, 2024년에는 생석회 가격이 톤당 190달러까지 상승했습니다. 의약품 등급 PCC에 적합한 고순도 광상은 지리적으로 희귀하여, 전문 제조업체들은 투자 회수 기간이 길어지는 선광 설비에 투자할 수밖에 없습니다.

부문별 분석

PCC 충전제가 백도를 향상시키고 제지 공장에 있어 중요한 비용 절감 요인인 섬유 사용량을 줄였기 때문에 2025년 세계 제지 및 판지 시장에서 PCCC는 총 생산량의 35.12%를 계속 차지했습니다. 그럼에도 불구하고, 의약품 및 식품 분야는 USP 등급의 순도를 활용해 더 높은 수익률을 달성함으로써 연평균 성장률(CAGR) 6.77%로 성장할 것으로 전망됩니다. 경질 포장재, 플렉서블 필름, 엔지니어링 수지 등 플라스틱 용도는 경량화 요구와 수지 원가 상승으로 인해 충전제 배합량이 증가함에 따라 확대되고 있으며, 표면 개질 등급을 활용하면 기계적 강도의 저하 없이 20-40%의 폴리머 대체가 가능해졌습니다.

특수 부형제 수요는 미국 FDA의 21 CFR 184.1191에 근거한 명확한 GRAS(일반적으로 안전하다고 인정되는) 지위와 전 세계 신청 절차를 간소화하는 착색 첨가물 면제 규정에 힘입어 유지되고 있으며, 이러한 요인들이 시장 진입 장벽으로 작용하고 있습니다. 서방형 마이크로스피어, 조영제, 그리고 알긴산염-PCC 하이브리드 캐리어는 입자 공학을 통해 PCC가 기존의 제산제로서의 역할을 넘어 응용되고 있음을 보여줍니다. 종이용 용도가 여전히 총 취급량의 대부분을 차지하고 있지만, 가격 결정력은 범용 충전재로는 구현할 수 없는 성능을 제공하는 미량 원소가 정밀하게 조절된 서브마이크론 등급으로 이동하고 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 생산량의 40.25%를 차지해, 2031년까지 연평균 성장률(CAGR) 5.05%로 성장할 것으로 전망됩니다. 미네랄스 테크놀로지스는 2026년, 중국과 인도의 제지 공장을 위해 3개의 새로운 현장형 PCC 위성 공장을 설립하여 운송에 따른 배출량을 줄이는 동시에 적기 공급의 이점을 확보했습니다. 일본과 한국은 정밀한 공정 제어를 활용하여 전자 및 제약 산업용 나노 스케일 PCC를 목표로 하고 있습니다. 한편, 베트남과 인도네시아에서는 플라스틱 컴파운딩 분야에 대한 외국인 직접 투자가 환영받고 있으며, 이는 지역 내 소비를 견인하고 있습니다. 인도의 포장 산업은 전자상거래와 식품 안전 규제의 영향으로 인도 표준국(BIS)의 순도 기준을 충족하는 코팅 처리된 PCC에 대한 수요가 증가하고 있습니다.

북미에서는 2024년에 가동을 시작한 돔타(Domtar)와 오미야(Omya)의 위스콘신주 현장 공장이 제지 공장의 석회 가마에서 배출되는 CO2를 재활용하여, 연간 27,500 드라이톤의 PCC를 생산함으로써, 연간 운송 배출량을 15,000 쇼트톤(CO2 환산) 감축합니다. 미국과 멕시코에서 자동차 경량화가 진행됨에 따라, 폴리프로필렌, 폴리에틸렌, 폴리아미드 부품용 개질 PCC에 대한 수요가 유지되고 있습니다. 카본프리(CarbonFree)의 스카이사이클 프로젝트(유나이티드 스틸 게리 공장)는 북미 최초로 대규모 탄소 포집 및 활용(CCU) 기반의 PCC 공급을 실현함으로써, 기업의 기후 목표를 달성하는 동시에 지속가능성을 중시하는 구매자로부터 프리미엄 가격을 받을 가능성을 내포하고 있습니다.

유럽에서는 엄격한 환경 정책과 도료, 코팅, 의약품 분야의 성숙한 수요가 맞물려 있으며, 유럽연합(EU)의 VOC(휘발성 유기 화합물) 상한선, REACH(화학물질의 등록, 평가, 허가, 제한) 규정, 그리고 다가오는 PFAS(퍼플루오로알킬 물질 및 폴리플루오로알킬 물질)의 단계적 폐지 등으로 인해 배합 재검토가 가속화되고 있으며, 배합 제조업체들은 저흡유성 비불소계 PCC 등급으로 전환하고 있습니다. 독일은 자동차용 복합재료의 도입을 주도하고 있으며, 영국은 영양보충제 분야에서 진전을 보이고 있고, 프랑스와 이탈리아는 건축용 도료 수요를 뒷받침하고 있습니다. 주요 3개 지역 이외에는 브라질, 사우디아라비아, 남아프리카공화국이 소규모 기반에서 두 자릿수 성장을 기록하고 있지만, 원자재 및 물류 제약으로 인해 단기적인 규모 확대는 완만하게 진행되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the precipitated calcium carbonate market size is projected to be 51.12 million tons in 2025, 53.46 Million tons in 2026, and reach 66.88 million tons by 2031, growing at a CAGR of 4.58% from 2026 to 2031.

This report Segments the Industry by Application (Paper and Paperboard, Paints and Coatings, Adhesives and Sealants, and More), End-User Industry (Packaging, Construction and Infrastructure, Automotive and Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Precipitated Calcium Carbonate Market Trends and Insights

Surging Demand From Premium Paper Grades

Brand owners are shifting toward high-opacity packaging and coated paper that rely on scalenohedral PCC to maximize light scattering, enabling filler loadings above 25% without sacrificing strength. Laboratory handsheets containing xylan-modified PCC showed brightness and opacity gains alongside improved burst and tear strength, letting mills downgrade fiber while protecting print quality. In Asia, where recycled-fiber loops dominate, nano-PCC replaces optical brightening agents that fade under UV, supporting cost-effective brightness control. Pilot trials using marble-waste-derived PCC achieved water contact angles of 103.3°, enhancing hydrophobicity for food wrappers. These results confirm that next-generation PCC provides aesthetic and sustainability benefits that pure fiber cannot match.

High-Fill Plastics for Lightweighting

Automotive and packaging converters incorporate up to 40% PCC masterbatch to curb resin costs and lower part weight, directly improving fuel economy. Polypropylene composites with 40% ground PCC posted a 69% rise in Young's modulus, though designers balance stiffness with ductility through particle-size control. Omya's Smartfill modified PCC sustained intrinsic viscosity in PET at 0.74 dL/g versus 0.61 dL/g for commodity PCC, boosting bottle top-load 40% at 5% filler, and enabling titanium dioxide cuts. Glass-fiber-epoxy parts filled with 6 wt% PCC reached 130.58 MPa tensile strength, opening pathways for lighter body panels in electric vehicles. Rising North American vehicle output of 15.5 million units in 2024, with 429 lb of plastics per car, underlines the latent plastics filler pull.

Limestone Price Volatility and Availability

The United States Geological Survey pegged lime output at 420 million tons in 2024, 72% of it from China, heightening concentration risk for importers. Quicklime prices rose to USD 190 per ton in 2024 as quarry permits tightened and fuel surcharges widened. High-purity deposits suitable for pharma-grade PCC are geographically scarce, forcing specialty producers to invest in beneficiation that stretches payback periods.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for VOC-Free Paints and Coatings

- Carbon-Negative PCC via CCU Routes

- Energy-Intensive Calcination and CO2 Footprint

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Global paper and paperboard retained 35.12% of 2025 volume as PCC fillers improved brightness and reduced fiber, a critical cost lever for mills. Nonetheless, pharmaceuticals and food applications are projected to grow at 6.77% CAGR, leveraging USP-grade purity to tap higher margins. Plastics applications, spanning Rigid Packaging, Flexible Films, and engineering resins, are expanding as lightweighting mandates and resin-cost inflation drive higher filler loadings, with surface-modified grades enabling 20-40% polymer substitution without sacrificing mechanical integrity.

Specialty excipient demand rests on clear United States FDA GRAS status under 21 CFR 184.1191 and color-additive exemptions that simplify global filings, creating barriers to entry. Controlled-release microspheres, imaging agents, and alginate, PCC hybrid carriers illustrate how particle engineering extends PCC beyond traditional antacid roles. Paper applications still anchor bulk tonnage, yet pricing power tilts toward trace-element-controlled, sub-micron grades that offer performance impossible for commodity fillers.

Geography Analysis

Asia-Pacific held 40.25% of global volume in 2025 and is forecast to expand at 5.05% CAGR through 2031. Minerals Technologies Inc. opened three new on-site PCC satellites in 2026 to serve Chinese and Indian paper mills, shrinking freight emissions and capturing just-in-time supply advantages. Japan and South Korea target nano-scale PCC for electronics and pharma, leveraging precise process control, while Vietnam and Indonesia welcome foreign direct investment in plastics compounding that lifts regional consumption. India's packaging sector, propelled by e-commerce and food safety mandates, escalates demand for coated PCC that meets Bureau of Indian Standards purity benchmarks.

In North America, Domtar and Omya's Wisconsin on-site plant, commissioned in 2024, recycles CO2 from the mill's lime kiln to make 27,500 dry tons per year of PCC, lowering annual transport emissions by 15,000 short tons CO2-equivalent. Automotive lightweighting in the United States and Mexico maintains demand for modified PCC in polypropylene, polyethylene, and polyamide parts. CarbonFree's SkyCycle project at United States Steel Gary brings the first large-scale Carbon Capture and Utilisation (CCU)-based PCC supply to North America, aligning with corporate climate targets and potentially capturing premium pricing from sustainability-focused buyers.

Europe, mixes strict environmental policy with mature demand in paints, coatings, and pharmaceuticals. European Union (EU) VOC (Volatile Organic Compound) ceilings, REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulations, and the looming PFAS (per- and polyfluoroalkyl substances) phase-out accelerate reformulation, steering formulators toward low-oil-absorption, non-fluorinated PCC grades. Germany leads automotive composites uptake, the United Kingdom advances in dietary supplements, and France and Italy anchor architectural-coating volumes. Outside the Big-Three regions, Brazil, Saudi Arabia, and South Africa post double-digit growth off small bases, though feedstock and logistics constraints moderate near-term scale-up.

- Cales de Llierca

- Carmeuse

- Changzhou Calcium Carbonate Co.

- Fimatec Ltd

- Gulshan Polyols Ltd

- HiTech Minerals and Chemicals Group

- Imerys

- J.M. Huber Corporation

- Lhoist

- Maruo Calcium Co. Ltd

- Minerals Technologies Inc.

- Mississippi Lime Company d/b/a MLC

- Nordkalk Corporation

- Omya

- SHIRAISHI CHEMICAL KAISHA, LTD

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand from premium paper and packaging grades

- 4.2.2 High-fill plastics for lightweighting

- 4.2.3 Regulatory push for VOC-free paints and coatings

- 4.2.4 Carbon-negative PCC via CCU routes

- 4.2.5 Nano-PCC improving opacity in recycled paper loops

- 4.3 Market Restraints

- 4.3.1 Limestone price volatility and availability

- 4.3.2 Energy-intensive calcination and CO2 footprint

- 4.3.3 PFAS scrutiny on fluorinated surface modifiers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 Paper and Paperboard

- 5.1.2 Plastics

- 5.1.2.1 Rigid Packaging

- 5.1.2.2 Flexible Films

- 5.1.3 Paints and Coatings

- 5.1.4 Adhesives and Sealants

- 5.1.5 Rubber

- 5.1.6 Pharmaceuticals and Food

- 5.1.7 Personal Care and Cosmetics

- 5.1.8 Other Applications

- 5.2 By End-user Industry

- 5.2.1 Packaging

- 5.2.2 Construction and Infrastructure

- 5.2.3 Automotive and Transportation

- 5.2.4 Healthcare and Life Sciences

- 5.2.5 Consumer Goods and Electronics

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Turkey

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Cales de Llierca

- 6.4.2 Carmeuse

- 6.4.3 Changzhou Calcium Carbonate Co.

- 6.4.4 Fimatec Ltd

- 6.4.5 Gulshan Polyols Ltd

- 6.4.6 HiTech Minerals and Chemicals Group

- 6.4.7 Imerys

- 6.4.8 J.M. Huber Corporation

- 6.4.9 Lhoist

- 6.4.10 Maruo Calcium Co. Ltd

- 6.4.11 Minerals Technologies Inc.

- 6.4.12 Mississippi Lime Company d/b/a MLC

- 6.4.13 Nordkalk Corporation

- 6.4.14 Omya

- 6.4.15 SHIRAISHI CHEMICAL KAISHA, LTD

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment