|

시장보고서

상품코드

2062039

IoT 인프라 보안 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)IoT Infrastructure Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

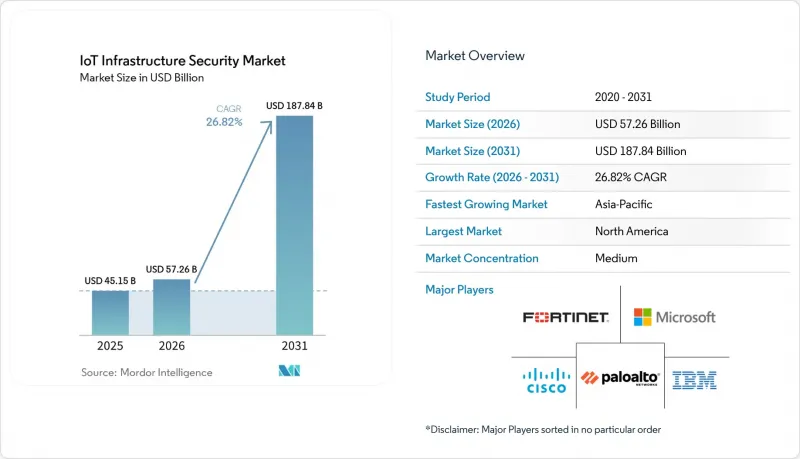

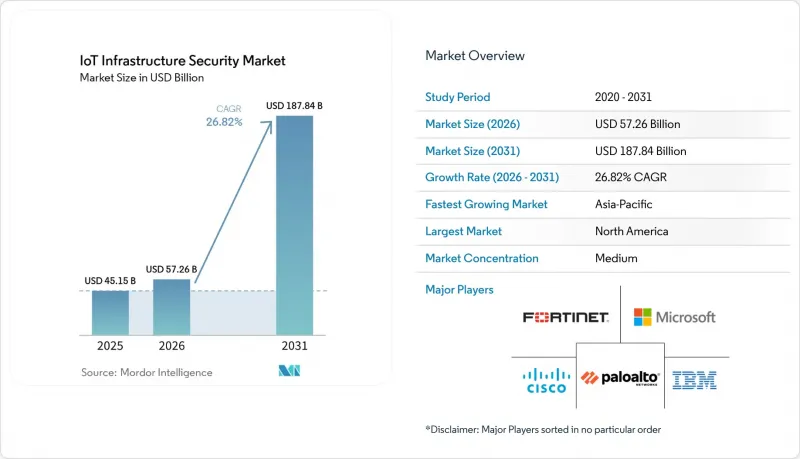

Mordor Intelligence에 의하면, IoT 인프라 보안 시장 규모는 2025년 451억 5,000만 달러로 평가되었고, 2026년에는 572억 6,000만 달러로 추정되고, 2031년까지 1,878억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 26.82%로 성장할 전망입니다.

본 보고서는 보안 유형별(네트워크 보안, 엔드포인트 보안 등), 배포 방식별(온프레미스, 클라우드 기반 등), 인프라 계층별(디바이스 및 엔드포인트 계층 등), 조직 규모별(대기업, 중소기업), 업종별(제조업, 의료 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 IoT 인프라 보안 시장 동향 및 인사이트

IoT의 대규모 도입에 따른 공격 표면의 확대

연결 기기 증가 규모는 IoT 인프라 보안 시장 전체의 사이버 방어 비용 효율성을 변화시키고 있습니다. Vectra AI는 2025년 1월부터 10월 사이에 136억 건의 IoT 공격이 발생했다고 보고했으며, 또한 연결된 기기의 50% 이상이 심각한 펌웨어 취약점을 안고 출하되고 있다고 지적했습니다. 장치 수 증가와 취약한 기본 보안 설정이 맞물리면서, 기업 환경에서 수동 패치 적용 및 수동 자산 관리 프로세스는 점점 더 실행 불가능해지고 있습니다. 그 결과, 특히 관리가 전혀 이루어지지 않거나 관리가 미흡한 기기가 다수 존재하는 환경에서 자동화된 자산 감지, 기기 ID 관리, 네트워크 세분화 및 제로 트러스트의 철저한 적용에 대한 수요가 높아지고 있습니다. Palo Alto Networks 역시 지난 1년간 노출된 기기가 332% 증가했다는 점을 강조하며, 사이버 사고의 70%가 보호되지 않은 IoT 진입점을 통해 IT 환경에서 발생하고 있다고 밝혔습니다. 이는 IoT 인프라 보안 시장에서 이것이 여전히 가장 강력한 성장 동력으로 남아 있는 이유를 설명하는 한 가지 요인입니다.

OT 네트워크와 IT 네트워크의 융합이 보안 수요를 높이고 있습니다.

OT 네트워크와 IT 네트워크의 융합으로 인해 IoT 인프라 보안 시장의 위험성이 높아지고 있습니다. 기업 내에서 발생한 사건이 현재 공장, 유틸리티, 인프라 운영에 직접적인 영향을 미칠 가능성이 있기 때문입니다. SANS의 조사에 따르면, 초기 ICS 및 OT 공격의 58%는 IT 시스템 침해에서 시작되었으며, 이는 기업 환경과 운영 환경이 얼마나 밀접하게 연결되어 있는지를 여실히 보여주고 있습니다. 인증 정보 공유, 연결된 통신 경로, 통합 관리 도구는 효율성을 높여주지만, 동시에 피싱이나 취약한 원격 접속과 같은 일반적인 침입 경로를 만들어내어 중요한 생산 시스템을 위험에 빠뜨릴 수 있습니다. 이로 인해 OT 팀과 IT 팀은 결과에 대한 책임을 공유할 수밖에 없게 되었으며, 이러한 변화는 고립된 도구에서 벗어나 보다 광범위한 가시성과 정책 제어 기능을 갖춘 통합 플랫폼으로의 전환을 촉진하고 있습니다. 점점 더 많은 기업이 통합 환경을 구축함에 따라, IoT 인프라 보안 시장에서는 감지, 모니터링, 세분화, 규정 준수 보고 및 관리형 대응을 단일 구매 결정으로 통합한 대규모 기업용 계약이 증가하고 있습니다.

레거시 산업 자산에 대한 제한된 보안 예산

레거시 산업 자산은 많은 사업자에게 여전히 교체 비용이 너무 높기 때문에 IoT 인프라 보안 시장의 발전을 저해하고 있습니다. TXOne Networks에 따르면, 단일 레거시 산업 제어 시스템을 교체할 경우 하드웨어 비용만 240만 달러가 소요되며, 6개월의 재검증 기간이 필요하고, 2주간의 생산 중단을 초래할 수 있습니다. SANS의 조사에서도 응답자의 34%가 전체 보안 예산 배분에 대해 불분명하다고 답했으며, 41%는 총 예산의 불과 0-25%만을 ICS 및 OT 보안에 할당하고 있는 것으로 나타났습니다. 이러한 상황에서는 경영진이 구식 제어 시스템이나 긴 자산 수명에 따른 위험을 인식하고 있더라도, 완전한 현대화는 어렵습니다. 가상 패치 적용, 패시브 모니터링, 네트워크 마이크로 세분화과 같은 대체적인 제어 수단은 안전한 가동 기간을 연장할 수 있지만, 이러한 수단의 도입은 여전히 운영상의 성과를 입증할 수 있는지 여부에 달려 있으며, 이것이 IoT 인프라 보안 시장의 성장을 저해하는 요인이 되고 있습니다.

부문별 분석

2025년, 네트워크 보안은 IoT 인프라 보안 시장의 35.4%를 차지한 것으로 평가되었으며, 이는 연결 계층에서 시작되는 지속적인 위험 노출을 반영한 것입니다. 기업이 관리 대상 외의 기기를 식별하고, 위험한 동작을 격리하며, 횡방향 이동을 차단하려 할 때, 라우터, 게이트웨이 및 기타 네트워크에 노출된 구성 요소는 여전히 첫 번째 통제 지점 역할을 합니다. 많은 구매자에게 있어 초기 투자는 여전히 시각화, 세분화 및 프로토콜 지원 모니터링에 집중되고 있습니다. 이러한 기능들은 다양한 기기가 혼재된 환경 전반에서 즉각적인 가치를 창출하기 위한 것입니다. 네트워크 보안 현황을 보면, 구매자들이 여전히 네트워크 계층을 대규모 IoT 방어의 주요 실행 기반으로 삼고 있음을 알 수 있습니다. IoT 인프라 보안 시장의 전반적인 동향을 살펴보더라도, 조직들이 기존의 경계 방어 도구에서 산업용 트래픽을 와이어 스피드로 분석할 수 있는 네트워크 감지 및 대응 플랫폼으로 전환하고 있음을 알 수 있습니다.

클라우드 보안은 가장 빠르게 성장하고 있는 보안 분야로, 2031년까지 연평균 성장률(CAGR)이 31.2%를 나타낼 것으로 전망됩니다. 이는 기업들이 집중 관리, 지속적인 업데이트, 그리고 관리형 지원을 점점 더 많이 요구하고 있기 때문입니다. 이러한 성장은 클라우드 네이티브 제로 트러스트 모델과 밀접한 관련이 있으며, 이 모델을 통해 정책 관리, 디바이스 컨텍스트 및 자동 대응을 분산된 거점 간에 보다 효율적으로 조정할 수 있습니다. 파로알토 네트웍스는 기존의 IoT 보안 포털을 Strata Cloud Manager 내의 'Device Security'로 이전하고, 2026년 8월을 포털 종료일로 정했습니다. 이는 주요 벤더들이 감지, 분류, 가상 패치 적용, 규정 준수 보고서를 공유 워크플로에 통합하고 있음을 보여줍니다. 엔드포인트 보안, 용도 보안 및 기타 분야는 특히 AI 지원 용도, 관리 대상 외 기기, 규제 대상 워크로드가 확대됨에 따라 계속해서 큰 수요를 창출하고 있습니다. 이러한 상황 속에서 IoT 인프라 보안 시장은 네트워크, 엔드포인트, 애플리케이션, 클라우드의 각 제어 기능 간에 자산 정보를 공유하는 통합 플랫폼으로 분명히 전환되고 있습니다.

2025년에는 클라우드 기반 솔루션 도입이 매출의 57.2%를 차지할 것으로 예상되며, 이는 IoT 인프라 보안 시장에서 통합된 가시성과 구독형 비즈니스 모델의 경제성이 여전히 매우 매력적임을 입증하고 있습니다. 클라우드 기반의 주도적인 도입은 구매자들이 유연한 분석 능력, 통합된 위협 인텔리전스, 그리고 신속한 기능 제공을 중시하고 있음을 반영합니다. 이 모델은 모든 거점, 공장 또는 지점마다 대규모 사내 보안 팀을 구성하기를 원하지 않는 기업에게 특히 매력적입니다. 클라우드 기반 제공은 AI 기반 보안 도구의 역할 확대와도 부합합니다. 이러한 도구들은 벤더 관리 환경 내에서 이루어지는 지속적인 모델 업데이트와 광범위한 텔레메트리 데이터의 집계라는 이점을 누리고 있습니다. 2026년 2월에 출시된 'AWS Security Hub Extended' AWS 보안 서비스와 엄선된 파트너 솔루션의 전문 지식을 표준화된 출력 형식과 통합된 과금 체계를 갖춘 단일 인터페이스로 통합함으로써 이러한 방향성을 뒷받침하고 있습니다.

하이브리드 모델은 가장 빠르게 성장하고 있는 모델로, 2031년까지 연평균 성장률(CAGR)이 32.2%를 나타낼 것으로 전망됩니다. 이는 많은 운영 사업자가 여전히 에어갭 환경이나 엄격하게 관리되는 OT 환경을 필요로 하기 때문입니다. 이러한 구매자들은 클라우드의 경제성을 부정하는 것이 아니라, 온프레미스 환경에서의 제어 기능과 통합된 위협 인텔리전스 및 정책 관리를 결합하고 있는 것입니다. 실제로 하이브리드 아키텍처를 통해 기업은 보안이 극히 중요한 프로세스나 기밀성이 높은 워크로드를 온프레미스에 유지하면서, 분석, 오케스트레이션, 보고서 작성에는 오프사이트 도구를 활용할 수 있습니다. 주권, 회복탄력성 또는 내부 정책으로 인해 클라우드의 광범위한 활용이 여전히 제한되고 있는 국방, 공공 서비스 및 일부 의료 환경에서는 온프레미스 구축이 여전히 중요하게 여겨지고 있습니다. 따라서 IoT 인프라 보안 시장은 단순히 온프레미스에서 클라우드로의 전환이라기보다는 두 가지를 융합한 전환 과정에 있다고 할 수 있습니다.

지역별 분석

북미는 2025년에 38.6%의 점유율을 차지했으며, 지역 내 최대 시장 지위를 유지했습니다. 이는 해당 지역의 성숙한 기업들의 보안 예산, 규제 강도, 그리고 IoT 인프라 보안 시장에서 광범위한 중요 인프라에 대한 노출을 반영한 것입니다. 또한, 이 지역은 보다 광범위한 생태계 수요를 뒷받침하는 막대한 공공 사이버 보안 지출의 혜택을 누리고 있습니다. 미국 국방부는 2026 회계연도에 사이버 보안 프로그램에 83억 1,000만 달러를 배정하는 한편, CISA(미국 사이버보안 및 인프라보안국)는 지속적 진단 및 완화(CDM) 프로그램 내 IoT 및 OT 자산 관리와 관련된 2026 회계연도 마일스톤을 수립했습니다. 북미의 기업용 5G IoT 연결 건수는 2025년 500만 건에서 2030년까지 3,900만 건으로 증가할 것으로 예상되며, 이에 따라 안전한 엣지 연결에 대한 수요가 확대되는 한편, 벤더와 통신 사업자를 겨냥한 공격 표면도 넓어지게 될 것입니다. 캐나다에서는 OT 및 ICS에 대한 예산 배분이 보다 신중하게 이루어지고 있어, 매니지드 서비스 제공업체나 도입 장벽이 낮은 플랫폼 서비스에 기회가 생기고 있습니다.

유럽은 IoT 인프라 보안 시장에서 가장 엄격한 규정 준수 환경을 보이고 있습니다. 이는 몇 가지 주요 디지털 및 운영 보안 프레임워크가 동시에 발전하고 있기 때문입니다. NIS2, 사이버 복원력법, DORA 및 무선 장비 지침은 해당 지역에 연결 제품을 판매하는 통신 사업자, 제조업체 및 공급업체에 영향을 미치는 다층적인 요구 사항들을 구성하고 있습니다. 독일에서는 KRITIS 관련 의무를 통해 추가적인 요건이 더해졌으며, 이로 인해 설명 책임의 범위가 확대되고, 보안이 중요 인프라의 계획 단계에서 더욱 심도 있게 반영되고 있습니다. 이러한 구조로 인해 규정 준수 기한이 직접적인 구매 동인이 되고 있습니다. 특히, 기한 내에 취약점 보고, 제품 강화 및 공식 거버넌스 프로세스 구축이 필요한 기기 제조업체나 사업자의 경우 더욱 그렇습니다.

아시아태평양에서는 2031년까지 IoT(사물인터넷) 인프라 보안 시장이 연평균 성장률(CAGR) 32.2%로 확대될 것으로 예상되며, 이는 제조업 및 스마트 인프라 분야의 도입 규모와 신규 프로젝트의 형성 속도를 모두 반영한 것입니다. 일본이 여전히 중요한 시장인 이유는 통신 사업자들이 보안을 연결성 그 자체의 일부로 간주하고 있기 때문입니다. 그 예로, NTT 도코모 비즈니스는 2025년 12월에 IoT 서비스용 보안 기능을 탑재한 'docomo business SIGN'을 출시할 예정입니다. 남미, 중동 및 아프리카는 시장 규모는 작지만, 산업의 디지털화와 스마트 시티 계획에 힘입어 이전보다 훨씬 더 초기 단계부터 보안이 신규 프로젝트에 반영되고 있어, 그 전망은 밝습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the ioT infrastructure security market size is expected to increase from USD 45.15 billion in 2025 to USD 57.26 billion in 2026 and reach USD 187.84 billion by 2031, growing at a CAGR of 26.82% over 2026-2031.

This report is Segmented by Security Type (Network Security, Endpoint Security, and More), Deployment (On-Premises, Cloud-Based, and More), Infrastructure Layer (Device/Endpoint Layer, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, Healthcare, and More), and Geography. The Market Forecasts Provided in Terms of Value (USD).

Global IoT Infrastructure Security Market Trends and Insights

Increasing Attack Surface Due to Massive IoT Adoption

The scale of connected device growth is changing the economics of cyber defense across the IoT infrastructure security market. Vectra AI reported 13.6 billion IoT attacks between January and October 2025, and it also noted that more than 50% of connected devices ship with critical firmware vulnerabilities.That mix of rising device counts and weak default security makes manual patching and manual inventory processes increasingly unworkable in enterprise environments. The result is a stronger demand for automated asset discovery, device identity controls, network segmentation, and zero-trust enforcement, especially in environments with large fleets of unmanaged or lightly managed devices. Palo Alto Networks also highlighted a 332% rise in exposed devices over the past year and stated that 70% of cyber incidents originated in IT environments through unprotected IoT entry points, which helps explain why this remains the strongest growth engine in the IoT infrastructure security market.

Convergence of OT and IT Networks Elevating Security Needs

The convergence of OT and IT networks is increasing risk in the IoT infrastructure security market, as events that begin on the corporate side can now spread directly into plant, utility, and infrastructure operations. SANS research found that 58% of initial ICS and OT attacks began as IT compromises, underscoring how deeply enterprise and operational environments are now linked.Shared credentials, connected communication paths, and centralized management tools improve efficiency, but they also create common entry points, such as phishing or weak remote access, that can compromise critical production systems. This forces OT and IT teams to share accountability for outcomes, and that change is supporting a move away from isolated tools toward unified platforms with broader visibility and policy control. As more operators build converged environments, the IoT infrastructure security market is seeing larger enterprise deals that bundle discovery, monitoring, segmentation, compliance reporting, and managed response into a single buying decision.

Limited Security Budgets for Legacy Industrial Assets

Legacy industrial assets slow the IoT infrastructure security market because the cost of replacement is still too high for many operators. TXOne Networks stated that replacing a single legacy industrial control system can cost USD 2.4 million in hardware alone, require 6 months of revalidation, and create 2 weeks of production downtime. SANS research also showed that 34% of respondents were unsure about their overall security budget allocations, while 41% allocated only 0-25% of their total budgets to ICS and OT security. Those conditions make full modernization difficult, even when leadership understands the risk exposure tied to older control systems and long asset life cycles. Compensating controls such as virtual patching, passive monitoring, and network microsegmentation can extend the secure operating life, but adoption still depends on proving operational returns, which tempers growth in the IoT infrastructure security market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates such as US IoT Cybersecurity Improvement Act

- Integration of AI-Powered Anomaly Detection in IoT Endpoints

- Fragmented Standards Across IoT Ecosystem

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Network security retained 35.4% of the IoT infrastructure security market in 2025, a position that reflects the continued exposure that begins at the connectivity layer. Routers, gateways, and other network-facing components remain the first point of control when enterprises try to identify unmanaged devices, isolate risky behavior, and contain lateral movement. For many buyers, the first wave of spending still goes to visibility, segmentation, and protocol-aware monitoring because those functions create immediate value across mixed device estates. Network security indicates that buyers still treat the network layer as the primary enforcement plane for large-scale IoT defense. The broader direction of the IoT Infrastructure Security Market also shows that organizations are shifting away from traditional perimeter tools toward network detection and response platforms that can analyze industrial traffic at wire speed.

Cloud security is the fastest-growing security type, with a projected CAGR of 31.2% through 2031, because enterprises increasingly want centralized operations, continuous updates, and managed support. This growth is closely tied to cloud-native zero-trust models, where policy management, device context, and automated response can be coordinated more efficiently across distributed sites. Palo Alto Networks moved its legacy IoT Security portal into Device Security within Strata Cloud Manager, setting August 2026 as the portal's shutdown date, demonstrating how leading vendors are consolidating discovery, classification, virtual patching, and compliance reporting into shared workflows. Endpoint security, application security, and other categories continue to drive meaningful demand, especially as AI-enabled applications, unmanaged devices, and regulated workloads expand. Across this mix, the IoT infrastructure security market is clearly moving toward unified platforms that share asset intelligence across network, endpoint, application, and cloud controls.

Cloud-based deployments accounted for 57.2% of revenue in 2025, confirming that centralized visibility and subscription economics remain highly attractive in the IoT infrastructure security market. Cloud-based deployment that leads reflects the value buyers place on elastic analytics capacity, integrated threat intelligence, and faster feature delivery. This model is especially appealing to enterprises that do not want to build large in-house security teams for every site, plant, or branch. Cloud delivery also aligns with the growing role of AI-driven security tools, which benefit from continuous model updates and broad telemetry pooling within vendor-managed environments. AWS Security Hub Extended, launched in February 2026, supports that direction by combining findings from AWS security services and curated partner solutions into a single interface with standardized outputs and unified billing.

Hybrid deployment is the fastest-growing model, with a projected CAGR of 32.2% through 2031, because many operators still need air-gapped or tightly controlled OT environments. These buyers are not rejecting cloud economics; they are blending local control with centralized threat intelligence and policy management. In practice, a hybrid architecture helps enterprises keep safety-critical processes and sensitive workloads on-site while using off-site tools for analysis, orchestration, and reporting. On-premises deployment remains relevant in defense, utilities, and some healthcare environments where sovereignty, resilience, or internal policy still limit wider cloud use. The IoT infrastructure security market is therefore undergoing a blended transition rather than a simple shift from on-premises to the cloud.

Geography Analysis

North America retained the largest regional position, with a 38.6% share in 2025, reflecting the region's mature enterprise security budgets, regulatory density, and broad critical infrastructure exposure in the IoT Infrastructure Security Market. The region also benefits from substantial public cybersecurity spending that supports broader ecosystem demand. The US Department of Defense allocated USD 8.31 billion to cybersecurity programs in fiscal year 2026, while CISA set out fiscal year 2026 milestones for IoT and OT asset management within the Continuous Diagnostics and Mitigation program. Business 5G IoT connections in North America are expected to rise from 5 million in 2025 to 39 million by 2030, expanding both demand for secure edge connectivity and the attack surface for vendors and operators. Canada offers an opportunity of a different kind because more cautious OT and ICS budget allocation leaves room for managed service providers and lower-friction platform offerings.

Europe presents the most demanding compliance environment in the IoT Infrastructure Security Market, as several major digital and operational security frameworks are advancing simultaneously. NIS2, the Cyber Resilience Act, DORA, and the Radio Equipment Directive create a layered set of requirements that affect operators, manufacturers, and vendors selling connected products into the region. Germany adds another layer through KRITIS-related obligations that broaden accountability and push security deeper into essential infrastructure planning. This structure is making compliance timelines a direct buying trigger, especially for device manufacturers and operators that need vulnerability reporting, product hardening, and formal governance processes in place before deadlines arrive.

Asia-Pacific is projected to expand at a 32.2% CAGR in the Internet of Things (IoT) infrastructure security market through 2031, reflecting both the scale of deployment and the speed of new project formation in manufacturing and smart infrastructure. Japan remains important because telecom operators are positioning security as part of connectivity itself, as shown by NTT Docomo Business launching docomo business SIGN in December 2025, with built-in security features for IoT services. South America, the Middle East, and Africa represent a smaller base, but the direction is strong because industrial digitization and smart city programs are bringing security into new projects much earlier than before.

- Cisco Systems Inc.

- IBM Corporation

- Microsoft Corporation

- Palo Alto Networks Inc.

- Fortinet Inc.

- Check Point Software Technologies Ltd.

- Trend Micro Incorporated

- McAfee LLC

- Amazon Web Services Inc.

- Huawei Technologies Co. Ltd.

- Armis Inc.

- Broadcom Inc. (Symantec Enterprise Division)

- Thales Group

- Kaspersky Lab

- Forescout Technologies Inc.

- Rapid7 Inc.

- Zscaler Inc.

- Akamai Technologies Inc.

- Darktrace plc

- Claroty Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Attack Surface Due to Massive IoT Adoption

- 4.2.2 Convergence of OT and IT Networks Elevating Security Needs

- 4.2.3 Emergence of 5G-Enabled IoT Driving Edge-Focus Security

- 4.2.4 Regulatory Mandates Such as US IoT Cybersecurity Improvement Act

- 4.2.5 Integration of AI-Powered Anomaly Detection in IoT Endpoints

- 4.2.6 Rapid Growth of IIoT Platforms in Developing Economies

- 4.3 Market Restraints

- 4.3.1 Limited Security Budgets for Legacy Industrial Assets

- 4.3.2 Fragmented Standards Across IoT Ecosystem

- 4.3.3 Skill Shortage in IoT-Specific Cybersecurity Expertise

- 4.3.4 High Implementation Complexity for Multi-Layer Security

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Security Type

- 5.1.1 Network Security

- 5.1.2 Endpoint Security

- 5.1.3 Application Security

- 5.1.4 Cloud Security

- 5.1.5 Other Security Types

- 5.2 By Deployment Model

- 5.2.1 On-Premises

- 5.2.2 Cloud-based

- 5.2.3 Hybrid

- 5.3 By Infrastructure Layer

- 5.3.1 Device / Endpoint Layer

- 5.3.2 Connectivity / Network Layer

- 5.3.3 Edge / Fog Layer

- 5.3.4 Cloud and Data Center Layer

- 5.3.5 Application / Platform Layer

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Healthcare

- 5.5.3 Energy and Utilities

- 5.5.4 Transportation and Logistics

- 5.5.5 Smart Cities and Infrastructure

- 5.5.6 Retail and Consumer IoT

- 5.5.7 BFSI

- 5.5.8 Government and Defense

- 5.5.9 Others Industry Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems Inc.

- 6.4.2 IBM Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 Palo Alto Networks Inc.

- 6.4.5 Fortinet Inc.

- 6.4.6 Check Point Software Technologies Ltd.

- 6.4.7 Trend Micro Incorporated

- 6.4.8 McAfee LLC

- 6.4.9 Amazon Web Services Inc.

- 6.4.10 Huawei Technologies Co. Ltd.

- 6.4.11 Armis Inc.

- 6.4.12 Broadcom Inc. (Symantec Enterprise Division)

- 6.4.13 Thales Group

- 6.4.14 Kaspersky Lab

- 6.4.15 Forescout Technologies Inc.

- 6.4.16 Rapid7 Inc.

- 6.4.17 Zscaler Inc.

- 6.4.18 Akamai Technologies Inc.

- 6.4.19 Darktrace plc

- 6.4.20 Claroty Ltd.

7 MARKET OPPORTUNITIES and FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment