|

시장보고서

상품코드

2062040

항응고제계 살서제 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Anticoagulant Rodenticides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

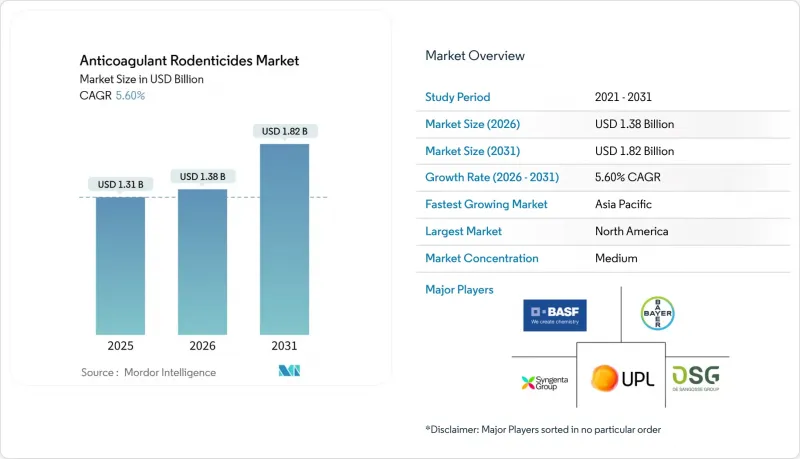

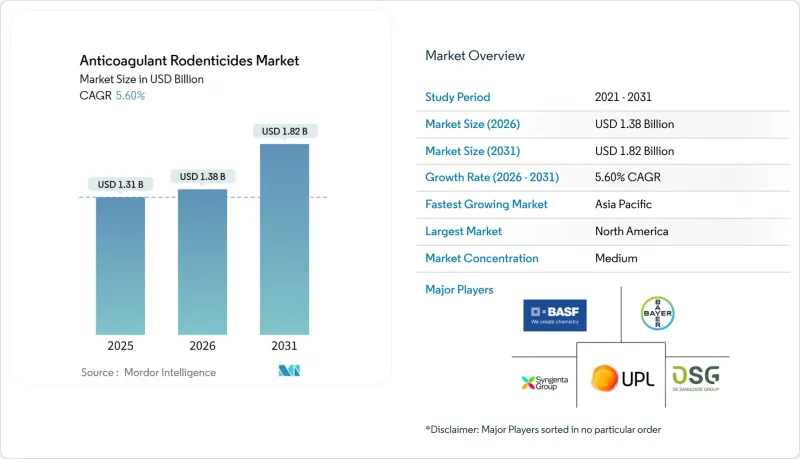

Mordor Intelligence에 의하면, 항응고제계 살서제 시장 규모는 2025년 13억 1,000만 달러로 평가되었고, 2026년에는 13억 8,000만 달러로 추정되고, 2026-2031년 CAGR 5.60%로 성장을 지속할 전망이며, 2031년까지 18억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 유형별(1세대 항응고제 및 2세대 항응고제), 제형별(펠릿, 블록 등), 용도별(곡물, 유지종자 및 콩류 등), 유통 채널별(직접 판매 등), 지역별(북미, 유럽, 남미, 아시아태평양 등)으로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항응고성 살서제 시장 동향 및 분석

농업 저장 분야에서 수확 후 손실 방지에 대한 관심 증가

농업 분야에서 수확 후 손실 최소화에 대한 관심이 높아짐에 따라, 항응고성 살서제 시장이 크게 성장하고 있습니다. 곡물 저장 시설, 사일로, 농장 창고로의 쥐 침입은 곡물, 콩류, 지방종자에 양적 및 질적 측면에서 막대한 손실을 초래하며, 농가의 수익성과 국가의 식량 안보에 악영향을 미치고 있습니다. 농업 생산이 확대됨에 따라, 저장 중인 수확물을 보호하는 것은 매우 중요한 운영상의 우선순위가 되고 있습니다. 대규모 곡물 취급 시스템에서는 부패, 오염 및 인프라 손상을 줄이기 위해 체계적인 쥐 방제 프로그램 도입이 확대되고 있습니다. 항응고성 살서제은 밀폐된 환경에서 뿌리 깊은 쥐 개체군을 효과적으로 통제하는 것으로 입증되었기 때문에 주변부 미끼 설치나 내부 저장 보호 전략에 일반적으로 사용되고 있습니다. 개체 수를 지속적으로 감소시키는 이러한 능력은 반복되는 침입의 악순환을 끊어, 그로 인해 장기적인 저장 손실을 줄이는 데 도움이 됩니다.

온대 곡물 지대에서 기후 변화에 따른 쥐 개체수의 급증

겨울철 기온 상승으로 인해 번식기가 길어지면서, 농업력상 쥐 무리가 가장 많아지는 시기가 앞당겨지고 있습니다. 수년에 걸친 연구를 통해, 공통된 사회경제적 경로를 기반으로 한 기후 시나리오 하에서 Mus속 및 Rattus속이 더 높은 위도 지역으로 분포 범위를 확대하고 있음이 확인되었습니다. 저장 시설 내에서 쥐 피해가 심각해지면, 사업자는 피해를 신속하게 억제하기 위해 1세대 약제에서 1회 투여형 2세대 유효 성분으로 전환합니다. 따라서 기후 변화의 영향으로 사용되는 사료의 총량이 증가하고 보충 주기가 단축됨에 따라, 곡물 생산국에서의 항응고성 살서제 시장 수요가 직접적으로 확대되고 있습니다.

생물학적 안전성을 갖춘 식품 공급망 구축을 위한 규제 추진

생물학적 안전성을 갖춘 식품 공급망 확보에 대한 규제 당국의 관심이 높아지고 있는 것은 항응고성 살서제 시장의 주요 성장 동력이 되고 있습니다. 주요 농업 경제국의 규제 당국이 시행하는 엄격한 식품 안전 기준은 수확 전, 저장, 유통 단계를 포함한 밸류체인 전반에 걸친 효과적인 쥐 방제 대책을 요구하고 있습니다. 미국 환경보호청(EPA)은 멸종 위기종 서식지 내 먹이 설치 기록 및 사체 조사를 의무화하고 있으며, 이에 따라 사업자들은 센서 데이터를 자동으로 기록하는 변조 방지형 스테이션을 도입할 수밖에 없게 되었습니다. 호주에서는 일반 소비자의 2세대 제품 접근이 제한되어 있으며, 착색제나 쓴맛 첨가제의 사용이 의무화되어 있어, 판매 채널은 사실상 전문 업체로 한정되어 있습니다.

부문별 분석

2세대 항응고제는 가장 큰 시장 점유율을 차지하고 있으며, 2025년에는 항응고성 살서제 시장 점유율의 63%를 차지한 것으로 평가되었는데, 가장 빠르게 성장하는 부문은 2026-2031년 연평균 성장률(CAGR) 8.8%를 나타낼 것으로 전망됩니다. 이러한 우위는 주로 높은 효능과 단회 투여 시의 치사율에 기인하며, 이를 통해 농지, 저장 시설, 도시 환경에서 내성 쥐 개체군을 박멸할 수 있습니다. 이러한 광범위한 도입은 특히 곡물 저장 및 식품 가공과 같은 대규모이며 위험이 높은 분야에서 신속하고 신뢰할 수 있는 해충 방제 솔루션에 대한 수요에 힘입어 이루어지고 있습니다.

1세대 항응고제 시장의 경우, 환경적 위험 및 2차 중독에 대한 우려로 인해 2세대 화합물에 대한 규제가 강화되고 있는 것이 주된 요인입니다. 그 결과, 특히 규제가 엄격한 지역에서 더 안전하고 독성이 낮은 대체품으로의 전환이 진행되고 있습니다. 1세대 항응고제는 생태계에 미치는 영향을 줄이기 위해 반복적이고 통제된 투여가 권장되는 통합 해충 관리(IPM) 프로그램에서 인기를 얻고 있습니다. 이러한 추세는 유효성이 여전히 필수적인 요소인 동시에, 지속가능성과 규제 준수가 제품 수요를 형성하는 데 있어 동등하게 중요해지고 있는 보다 광범위한 시장의 변화를 여실히 보여주고 있습니다.

펠릿은 가장 큰 비중을 차지하고 있으며, 2025년에는 항응고성 살서제 시장 점유율의 41%를 차지한 것으로 평가되었습니다. 이러한 광범위한 활용은 사용이 간편하고 비용 대비 효과가 높으며, 대규모 농업 작업, 특히 신속한 작업이 필수적인 노지나 살포 용도에 적합하기 때문입니다. 농가와 해충 방제 업체들은 넓은 범위를 커버할 수 있는 유연성과 다양한 설치류 종에 대한 효과 덕분에 펠릿을 선호하여 사용하고 있습니다.

블록체인은 가장 빠르게 성장하는 분야로, 2026-2031년 연평균 성장률(CAGR) 9.4%를 나타낼 것으로 전망됩니다. 이러한 성장은 내구성, 기상 조건에 대한 내성, 그리고 특히 창고, 식품 가공 시설, 저장 시설과 같은 통제된 환경에서 미끼 스테이션과의 호환성에 힘입어 이루어지고 있습니다. 이 분산제는 습기나 가혹한 환경에서도 쉽게 분해되지 않고 효과가 장기간 지속되므로, 엄격한 식품 안전 규정을 준수하는 데 가장 적합합니다. IoT 지원 유인 트랩 등 체계화되고 모니터링이 가능한 해충 방제 솔루션이 시장에서 점점 더 널리 채택됨에 따라, 방충제에 대한 수요가 크게 증가할 것으로 예측됩니다.

지역별 분석

북미는 가장 큰 비중을 차지하며, 2025년 항응고성 살서제 시장 규모의 38%를 차지했습니다. 이러한 우위는 해당 지역의 확고한 농업 및 식품 저장 산업, 식품 안전 규제, 그리고 현대적인 해충 관리 기법의 광범위한 도입에 기인합니다. 또한, 수확 후 손실에 대한 높은 인식과 주요 살서제 제조업체의 존재가 북미를 주요 시장으로 하는 입지를 더욱 공고히 하고 있습니다. 예를 들어, 미국 중서부에서는 아이오와주와 일리노이주의 곡물 저장 시설에서 증가하는 쥐의 침입을 억제하고 곡물 손실을 방지하기 위해 저장 기간 동안 2세대 항응고성 살서제의 사용을 늘리고 있으며, 이것이 안정적인 시장 수요를 뒷받침하고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2026-2031년 연평균 성장률(CAGR) 8.5%를 나타낼 것으로 전망됩니다. 이러한 성장은 대규모 농업의 확대, 곡물 저장 및 가공 인프라에 대한 투자 증가, 그리고 작물 보호 및 식량 안보에 대한 인식 제고에 힘입어 이루어지고 있습니다. 또한, 인구 증가와 주곡 및 고부가가치 작물에 대한 수요 증가가 아시아태평양 신흥 경제국에서의 항응고성 살서제 채택을 촉진하고 있으며, 이 지역은 시장에 있어 매우 중요한 성장 거점으로서의 입지를 확고히 하고 있습니다. 호주에서 시행된 1년간의 소비자 대상 판매 중단 조치는 수요를 없애기 위한 것이 아니라 인가 기업으로 유도하기 위한 것으로, 판매량을 유지하면서 데이터 수집 체계를 강화하고 있습니다.

유럽은 광범위한 곡물 저장 인프라와 확립된 전문 해충 관리 네트워크의 혜택을 누리고 있습니다. 보다 엄격한 관리 체제와 역량 증명 요건의 도입, 그리고 지속적인 하드웨어 업그레이드를 통해 공급업체들은 수익성을 유지하고 있습니다. 내성 확산으로 인해 플로쿠마펜이나 비항응고제 계열 제품으로의 전환이 진행되고 있어, 제제 개선의 기회가 생기고 있습니다. 아프리카와 중동에서는 수확 후 손실을 줄이고 식량 안보를 강화하기 위해 정부가 현대식 사일로를 도입함에 따라 시장이 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the anticoagulant rodenticides market size is projected to grow from USD 1.31 billion in 2025 to USD 1.38 billion in 2026 and is forecast to reach USD 1.82 billion by 2031 at 5.60% CAGR over 2026-2031.

This report is Segmented by Type (First-Generation Anticoagulants and Second-Generation Anticoagulants), by Formulation (Pellets, Blocks, and More), by Application (Cereals and Grains, Oilseeds and Pulses, and More), by Distribution Channel (Direct and More), by Geography (North America, Europe, South America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Anticoagulant Rodenticides Market Trends and Insights

Increasing Focus on Post-Harvest Loss Prevention in Agricultural Storage

The growing emphasis on minimizing post-harvest losses in agriculture is a significant driver for the anticoagulant rodenticides market. Rodent infestations in grain storage facilities, silos, and farm warehouses result in substantial quantitative and qualitative losses of cereals, pulses, and oilseeds, adversely affecting farmer profitability and national food security. As agricultural production scales up, safeguarding harvested crops during storage has become a critical operational priority. Large-scale grain handling systems are increasingly adopting structured rodent management programs to reduce spoilage, contamination, and infrastructure damage. Anticoagulant rodenticides are commonly employed in perimeter baiting and internal storage protection strategies due to their proven effectiveness in controlling persistent rodent populations in enclosed environments. Their ability to achieve sustained population reduction helps break recurring infestation cycles, thereby mitigating long-term storage losses.

Climate-Linked Rodent Population Surges in Temperate Grain Belts

Warmer winters are extending breeding windows, so rat colonies reach peak numbers earlier in the agricultural calendar. Multiyear studies confirm that Mus and Rattus genera are expanding their geographic ranges toward higher latitudes under shared socioeconomic pathway climate scenarios. When rodent pressure escalates inside storage facilities, operators shift from first-generation to single-feed second-generation actives to curb damage rapidly. Climate amplification, therefore, enlarges the total quantity of bait deployed and reduces waiting time between replenishment cycles, directly expanding the Anticoagulant Rodenticides Market demand in cereal-growing nations.

Regulatory Push for Bio-Secure Food Supply Chains

The increasing regulatory focus on ensuring bio-secure food supply chains is a key driver for the anticoagulant rodenticides market. Strict food safety standards enforced by regulatory authorities in major agricultural economies require effective rodent control measures across the value chain, including pre-harvest, storage, and distribution stages. The United States Environmental Protection Agency requires baiting records and carcass searches in endangered-species zones, forcing operators to adopt tamper-resistant stations that automatically log sensor data. Australia has restricted consumer access to second-generation products and insists on the use of dyes and bittering agents, effectively professionalizing sales channels.

Other drivers and restraints analyzed in the detailed report include:

- Internet of Things (IoT)-Enabled Bait-Station Telemetry Adoption

- Environmental, Social, and Governance (ESG) Guidelines Set by Asset Owners for Managing Vertebrate Pest Welfare

- Volatile Vitamin K Antidote Precursor Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Second-generation anticoagulants hold the largest segment, capturing 63% of the anticoagulant rodenticides market share in 2025, while the fastest-growing segment is with an 8.8% CAGR through 2026-2031. This dominance is primarily due to their high efficacy and single-feed lethality, which enable them to control resistant rodent populations across agricultural fields, storage facilities, and urban environments. Their widespread adoption is driven by demand for rapid, reliable pest control solutions, particularly in large-scale, high-risk applications such as grain storage and food processing.

The first-generation anticoagulants market is largely driven by increasing regulatory restrictions on second-generation compounds due to concerns about environmental and secondary poisoning risks. Consequently, there is a shift toward safer, lower-toxicity alternatives, particularly in regions with stringent regulatory frameworks. First-generation anticoagulants are gaining popularity within integrated pest management (IPM) programs, where repeated, controlled dosing is preferred to reduce ecological impact. This trend highlights a broader market transition in which efficacy remains essential, but sustainability and regulatory compliance are becoming equally significant in shaping product demand.

Pellets hold the largest segment, accounting for 41% of the anticoagulant rodenticides market share in 2025. Their widespread use is attributed to their ease of application, cost-effectiveness, and suitability for large-scale agricultural operations, particularly in open fields and broadcast applications where rapid deployment is critical. Farmers and pest control operators prefer pellets for their flexibility in covering extensive areas and their effectiveness in targeting a wide range of rodent species.

The blocks segment is the fastest-growing segment, projected to grow at a 9.4% CAGR between 2026 and 2031. This growth is driven by their durability, resistance to weather conditions, and compatibility with bait stations, particularly in controlled environments such as warehouses, food processing units, and storage facilities. Blocks are less susceptible to disintegration in moist or harsh conditions and provide longer-lasting efficacy, making them well-suited for compliance with stringent food safety regulations. As the market increasingly adopts structured, monitored pest control solutions, including IoT-enabled bait stations, demand for block formulations is projected to grow significantly.

Geography Analysis

North America held the largest region, accounting for 38% of the anticoagulant rodenticides market size in 2025. This dominance is attributed to the region's well-established agricultural and food storage industries, food safety regulations, and widespread adoption of modern pest management practices. Additionally, high awareness of post-harvest losses and the presence of major rodenticide manufacturers further strengthen North America's position as the leading market. For instance, in the United States Midwest, grain elevators in Iowa and Illinois have increased the use of second-generation anticoagulant rodenticides during the storage season to control rising rodent infestations and prevent grain losses, supporting consistent market demand.

Asia-Pacific is the fastest-growing region, projected to grow at a 8.5% CAGR between 2026 and 2031. This growth is driven by the expansion of large-scale farming, increased investments in grain storage and processing infrastructure, and rising awareness of crop protection and food security. Furthermore, the growing population and increasing demand for staple and high-value crops are driving the adoption of anticoagulant rodenticides across emerging economies in the Asia-Pacific region, positioning the region as a critical growth area for the market. Australia's one-year consumer suspension channels demand into licensed firms rather than eliminating it, sustaining volumes while improving data capture.

Europe benefits from an extensive grain storage infrastructure and well-established professional pest management networks. The implementation of stricter stewardship schemes and proof-of-competence requirements, along with ongoing hardware upgrades, helps vendors maintain profit margins. The prevalence of resistance has led to a shift toward flocoumafen and non-anticoagulant products, creating opportunities for reformulation. In Africa and the Middle East, the market is expanding as governments implement modern silos to reduce post-harvest losses and enhance food security.

- BASF SE

- Bayer AG

- Syngenta Group

- UPL Limited

- Reckitt Benckiser Group plc

- Rentokil Initial plc

- Anticimex AB

- Neogen Corporation

- Kemin Industries, Inc.

- Fumakilla Limited

- Bell Laboratories, Inc.

- PelGar International Limited

- De Sangosse SAS

- Vetoquinol SA

- JT Eaton & Co., Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing focus on post-harvest loss prevention in agricultural storage

- 4.2.2 Climate-linked rodent population surges in temperate grain belts

- 4.2.3 Consolidation of farm-management service providers

- 4.2.4 Internet of Things (IoT)-enabled bait-station telemetry adoption

- 4.2.5 Gene-edited cereal cultivars increasing rodent palatability

- 4.2.6 Environmental, Social, and Governance (ESG) Guidelines set by asset owners for managing vertebrate pest welfare

- 4.3 Market Restraints

- 4.3.1 Regulatory push for bio-secure food supply chains

- 4.3.2 Escalating multi-species resistance to first-generation actives

- 4.3.3 Community-led bans after raptor secondary-poisoning events

- 4.3.4 Volatile vitamin K antidote precursor pricing

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 First-generation anticoagulants

- 5.1.2 Second-generation anticoagulants

- 5.2 By Formulation

- 5.2.1 Pellets

- 5.2.2 Blocks

- 5.2.3 Powders

- 5.2.4 Liquids

- 5.3 By Application

- 5.3.1 Cereals and Grains

- 5.3.2 Oilseeds and Pulses

- 5.3.3 Fruits and Vegetables

- 5.3.4 Other Applications

- 5.4 By Distribution Channel

- 5.4.1 Direct (Manufacturers to Co-operatives)

- 5.4.2 Agro-chemical Retailers

- 5.4.3 Online Platforms

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Australia

- 5.5.4.4 Japan

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Bayer AG

- 6.4.3 Syngenta Group

- 6.4.4 UPL Limited

- 6.4.5 Reckitt Benckiser Group plc

- 6.4.6 Rentokil Initial plc

- 6.4.7 Anticimex AB

- 6.4.8 Neogen Corporation

- 6.4.9 Kemin Industries, Inc.

- 6.4.10 Fumakilla Limited

- 6.4.11 Bell Laboratories, Inc.

- 6.4.12 PelGar International Limited

- 6.4.13 De Sangosse SAS

- 6.4.14 Vetoquinol SA

- 6.4.15 JT Eaton & Co., Inc.