|

시장보고서

상품코드

2062050

건설용 드론 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Construction Drones - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

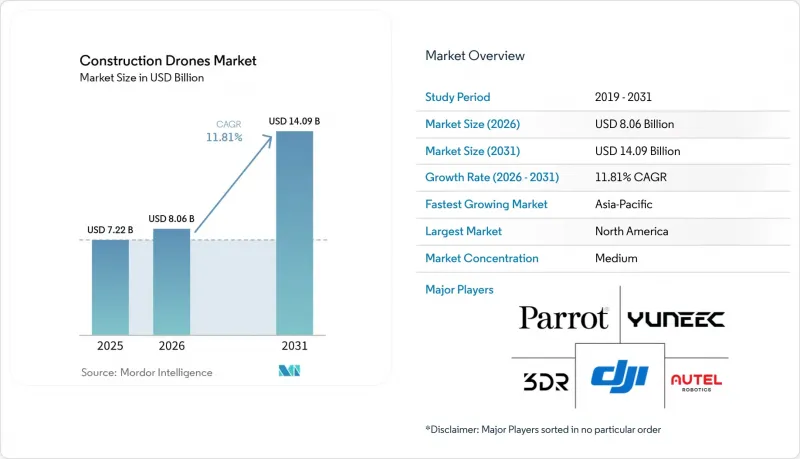

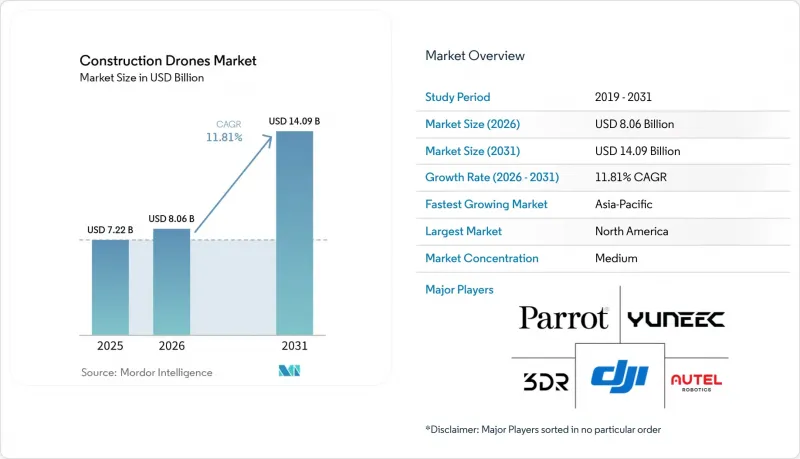

Mordor Intelligence에 의하면, 건설용 드론 시장 규모는 2025년에 72억 2,000만 달러로 평가되었고 2026년 80억 6,000만 달러에서 2031년까지 140억 9,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 11.81%를 나타낼 것으로 예측됩니다.

본 보고서는 유형(회전익, 고정익, 하이브리드), 구성 요소(하드웨어, 소프트웨어, 서비스), 용도(토지 측량 및 지형도 작성 등), 최종 사용자(주택 건설 회사, 상업용 건설 도급업체, 산업용), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 건설용 드론 시장 동향과 인사이트

현장 측량 및 매핑 분야로의 급속한 확산

건설용 드론 시장에서 드론을 활용한 측량 업무는 전문적인 작업에서 다양한 프로젝트 유형의 일반적인 업무 워크플로로 전환되고 있습니다. 프로젝트 팀은 기존의 인력 중심 방식에 비해 현장에서의 업무 부담을 줄이면서, 항공 촬영 데이터를 활용해 포인트 클라우드 데이터와 3D 측량 결과물을 생성하고 있습니다. BIM과 드론의 통합에 관한 조사에 따르면, 드론을 통한 현장 데이터 수집은 현장에서 생성된 3D 측량 이미지와 설계 모델을 직접 비교할 수 있게 함으로써 모니터링 및 진행 상황 관리를 개선합니다. 이로 인해 더 빈번한 측량 주기가 현실화되면서, 건설용 드론 시장 전반에서 정기적인 소프트웨어 구독 및 관리형 데이터 서비스에 대한 수요가 증가하고 있습니다. 또한, 주간 또는 일일 단위의 캡처 작업이 비용과 시간 측면에서 타당성이 인정되기 쉬워, 준공 도면에 대한 발주자의 기대도 높아지고 있습니다. 이러한 기대가 계약 조건에 반영됨에 따라, 건설용 드론 시장에서는 일회성 기체 구매가 아닌 지속적인 이용을 통한 안정적인 수익원이 확대되고 있습니다.

BIM과 디지털 트윈의 통합을 통한 주도

건설용 드론 시장에서는 단순한 드론 도입 캠페인뿐만 아니라, BIM 및 디지털 트윈 워크플로우에서도 구조적인 수요가 발생하고 있습니다. 드론으로 생성된 포인트 클라우드 데이터가 디지털 프로젝트 환경에 통합됨에 따라, 팀은 수작업 확인을 최소화하면서 계획된 작업과 실제 현장 상황을 보다 신속하게 비교할 수 있게 됩니다. 동료 심사를 거친 연구에 따르면, 드론으로 수집한 실측 데이터를 기반으로 하는 디지털 트윈 시스템이 가상 계획과 실제 건설 진행 상황을 실시간으로 더 효과적으로 연동시키는 것으로 확인되었습니다. 즉, 공공 기관의 발주처, 금융 기관, 또는 표준 규격에 기반한 공급망에서 새로운 BIM 요구 사항이 하나씩 추가될 때마다, 건설용 드론의 목표 시장도 확대된다는 의미입니다. 소프트웨어 공급업체들은 이러한 추세로 인해 큰 혜택을 보고 있습니다. 왜냐하면 가치가 단순히 기체의 성능뿐만 아니라 분석, 모델 비교, 워크플로 통합으로 옮겨가고 있기 때문입니다. 따라서 건설용 드론 시장에서는 소프트웨어의 성장세가 하드웨어의 성장세를 앞지르고 있습니다.

엄격한 공역 규제 및 개인정보 보호 규정

규제의 파편화는 건설용 드론 시장 확대에 있어 여전히 가장 뚜렷한 제약 요인 중 하나입니다. 밀집된 도시 지역의 프로젝트 구역은 대개 관제 공역 내에 위치해 있어, 승인, 면제 및 운영 조건이 기술 자체보다 더 복잡합니다. 미국에서는 FAA가 2025년 8월 BVLOS(시야 밖 비행)에 관한 규정 제정안을 공표하고, 여러 인구 위험 범주에 걸친 성능 기반 프레임워크를 제시했으나, 의견 수렴 절차는 2026년까지 이어졌습니다. 유럽에서는 규정(EU) 2019/947에 대한 EASA 개정안 제5호가 2025년 5월에 발효됨에 따라, 프랑스는 2026년 1월부터 기존의 국내 기준에 따른 운영 시나리오를 종료하고, DGAC의 감독 하에 EU 고유의 범주에 따른 인가로 전환할 것을 의무화했습니다. 이러한 차이점은 국경을 넘어 사업을 전개하는 기업이나 민감한 시설 인근에서 사업을 영위하는 기업에게 규정 준수 노력을 강화하도록 요구하며, 법적 및 항공 관련 지원 자원이 충실한 대규모 사업자에게 유리하게 작용합니다. 운용 규정이 더욱 예측 가능해질 때까지는 건설용 드론 시장이 엄격한 규제 환경 속에서 성장세가 둔화되는 상황이 지속될 것으로 보입니다.

부문별 분석

2025년 건설용 드론 시장에서 회전익 플랫폼은 71.17%의 점유율을 차지했습니다. 이는 도시 지역의 건설 현장, 제한된 이륙 구역 및 호버링 작업에 대한 높은 적합성을 반영한 것입니다. 이러한 시스템은 건물 주변, 가설 구조물 및 가동 중인 작업 구역에서 쉽게 설치할 수 있기 때문에 여전히 많은 건설업체에게 기본적인 선택지로 자리 잡고 있습니다. 건설용 드론 시장에서는 외관 검사, 진행 상황 기록, 그리고 국부적인 측량 분야에서 멀티로터의 유연성이 여전히 중요한 역할을 하고 있습니다. 건설용 드론 업계에서 이 방식은 많은 현장 팀이 이미 이해하고 있는 훈련 및 운영 관행과도 부합합니다. 이러한 확고한 호환성이 회전익 시스템이 신규 기체 도입의 기준으로 계속 자리 잡고 있는 이유 중 하나입니다.

고정익 플랫폼은 건설용 드론 시장에서 각기 다른 역할을 수행하고 있습니다. 특히, 호버링 성능보다 비행 지속 시간이 더 중요시되는 대규모 회랑이나 대지 규모의 작업에서 이러한 경향이 두드러집니다. 고속도로 노선, 파이프라인 경로, 연안 자산 등은 여전히 장거리 비행 경로에 적합합니다. 그렇긴 하지만, 여러 기체 등급에서 임무 효율이 향상됨에 따라 회전익기와 고정익기 활용 간의 격차는 점차 줄어들고 있습니다. 하이브리드 VTOL 플랫폼은 실용적인 현장 배치와 광범위한 커버 능력을 모두 갖추고 있어, 2031년까지 연평균 성장률(CAGR) 13.43%를 나타낼 것으로 예측됩니다. 건설용 드론 시장에서 이러한 조합은 이동 효율성과 근접 검사 능력 모두를 필요로 하는 교량, 댐, 재생 에너지 및 외딴 지역의 토목 프로젝트에 매력적인 솔루션입니다.

2025년 건설용 드론 시장에서 하드웨어가 57.64%를 차지하고 있으며, 이는 기체, 탑재체 및 지원 장비의 구비가 여전히 도입의 첫걸음임을 보여줍니다. 많은 기업이 여전히 프로그램 개발의 초기 단계에 있기 때문에 설비에 대한 투자가 총 수익에서 큰 비중을 차지하고 있습니다. 서비스 부문은 프로젝트 단위의 비행 업무, 데이터 수집 또는 규정 준수 지원을 외부에 위탁하려는 업체들에게 그 공백을 메우는 역할을 하고 있습니다. 따라서 건설용 드론 시장은 장기적인 가치가 다른 분야로 이동하고 있음에도 불구하고, 여전히 하드웨어가 시장 전체의 상당 부분을 차지하고 있습니다. 이러한 경향은 도입 대수가 여전히 증가하고 있으며, 도급업체의 규모에 따라 운영 모델이 크게 달라지는 시장에서 흔히 볼 수 있는 현상입니다.

소프트웨어 시장은 2031년까지 연평균 성장률(CAGR) 12.77%를 나타낼 것으로 예측되며, 건설용 드론 시장에서 가장 빠르게 성장하는 분야가 될 것입니다. 그 주된 이유는 가치가 데이터 처리, AI를 활용한 분석, 임무 계획, 그리고 프로젝트 시스템과의 통합으로 이동하고 있다는 점에 있습니다. 드론 및 디지털 트윈 워크플로우에 대한 조사 결과 또한 이러한 변화를 뒷받침하고 있습니다. 왜냐하면 실시간 동기화는 단순히 기체의 배치뿐만 아니라 데이터 처리와 모델 비교에 의존하고 있기 때문입니다. 프로그램이 성숙해짐에 따라 고객 유지는 기기의 브랜드뿐만 아니라 플랫폼의 사용 편의성과 워크플로 통합에 점점 더 좌우되고 있습니다. 건설용 드론 업계에서 소프트웨어는 장기적인 차별화 요소이자 지속적인 수익원으로 가장 확실한 요소입니다.

지역별 분석

2025년, 북미는 건설용 드론 시장 점유율의 37.56%를 차지하며 최대 지역 시장으로 부상했습니다. 이 지역은 대규모 건설 투자 기반, 대형 건설사의 적극적인 기술 도입, 그리고 디지털 프로젝트 워크플로의 광범위한 활용이라는 혜택을 누리고 있습니다. AGC의 보고서에 따르면, 미국 건설사의 26%가 2025년에 드론 투자를 늘릴 계획이며, 이는 시범 운영 단계에서 지속적인 예산 편성 단계로의 전환을 시사합니다. 또한 북미 건설용 드론 시장에서는 연방 정부 및 규제 대상 프로젝트의 조달 기준이 더욱 엄격해짐에 따라, 보안 및 규정 준수 측면에서 우수한 플랫폼에 대한 수요가 증가하고 있습니다.

유럽은 다른 많은 다자간 시장에 비해 규제 기반이 더욱 조화롭게 구축되어 있다는 점을 바탕으로, 건설용 드론 시장에서 성숙한 제2의 지역으로서의 위상을 유지하고 있습니다. 2025년 5월에 발효된 유럽항공안전청(EASA)의 규정(EU) 2019/947 제5차 개정안은 회원국 전체의 운영 기준을 정립하는 데 기여했습니다. 프랑스에서는 2026년 1월 기존 국내 기준에 따른 운영 시나리오가 종료됨에 따라 단기적인 규정 준수 부담이 발생했고, 사업자들은 DGAC(프랑스 민간항공청)의 감독 하에 EU 고유의 카테고리 인증으로의 전환을 불가피하게 맞이하게 되었습니다. 이러한 전환 비용이 있음에도 불구하고, 유럽의 건설용 드론 시장은 국경을 초월한 서비스의 가능성과 검사 및 진행 상황 모니터링에서의 지속적인 활용에 힘입어 성장하고 있습니다. 동 지역 내에서는 영국, 독일, 프랑스가 여전히 주요 도입 거점으로 자리 잡고 있습니다.

아시아태평양은 건설용 드론 시장에서 가장 빠르게 성장하고 있는 지역 부문으로, 2031년까지 연평균 성장률(CAGR)이 13.32%를 나타낼 것으로 전망됩니다. 중국과 인도가 주요 성장 동력이지만, 수요 패턴은 스마트 사이트로의 급속한 도입과 인프라 주도형 도입으로 나뉩니다. 일본은 운용 성숙도의 중요한 지표로 자리 잡고 있습니다. 2025년 3월, KDDI 스마트 드론과 오바야시구미는 가동 중인 댐 건설 현장에서 Skydio Dock for X10을 사용하여 완전 원격·자동 드론 점검 실증 실험을 완료했습니다. 또한 한국에서도 자율 운용으로의 전환이 예고되고 있으며, DJI 엔터프라이즈는 2026년 3월, SK건설이 겨울철 건설 현장 관리에 DJI Dock 3를 활용한 사례 연구를 발표했습니다. 남미, 중동 및 아프리카에서는 건설용 드론 시장 규모가 여전히 작은 임베디드니다. 그럼에도 불구하고, 대규모 인프라 회랑, 에너지 프로젝트 및 선별적인 스마트 시티에 대한 투자로 인해 측량, 토공 모니터링 및 점검 서비스에 대한 수요는 계속해서 증가하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the construction drones market size was valued at USD 7.22 billion in 2025, and is projected to grow from USD 8.06 billion in 2026 to USD 14.09 billion by 2031, growing at a CAGR of 11.81% from 2026 to 2031.

This report is Segmented by Type (Rotary-Wing, Fixed-Wing, and Hybrid), Component (Hardware, Software, and Services), Application (Land Surveying and Topographic Mapping, and More), End-User (Residential Construction Firms, Commercial Construction Contractors, and Industrial), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Construction Drones Market Trends and Insights

Rapid Adoption for Site Surveying and Mapping

Drone-based surveying has moved from a specialist task to a regular operating workflow across many project types in the construction drones market. Project teams are using aerial capture to generate point clouds and 3D survey outputs with less field effort than traditional manual approaches. Research on BIM-drone integration shows that drone-based reality capture improves monitoring and progress management by enabling direct comparison between site-generated 3D survey images and design models, making more frequent survey cycles practical and strengthening demand for recurring software subscriptions and managed data services across the construction drones market. It also raises owner expectations for as-built documentation, because weekly or even daily capture is easier to justify in terms of both cost and time. As those expectations spread through contract terms, the construction drones market gains a steadier stream of repeat usage rather than one-time aircraft purchases.

BIM Digital-Twin Integration Pull-Through

The construction drones market is seeing structural demand from BIM and digital twin workflows rather than solely from direct drone adoption campaigns. When drone-generated point clouds flow into digital project environments, teams can compare planned work with actual site conditions faster and with less manual checking. Peer-reviewed research confirms that digital-twin systems supported by drone reality capture improve real-time synchronization between virtual plans and physical construction progress. That means each new BIM requirement from a public client, lender, or standards-based supply chain also widens the addressable market for construction drones. Software providers benefit strongly from this pattern because the value shifts toward analytics, model comparison, and workflow integration rather than only toward aircraft capability. Hence, software growth is outpacing hardware growth in the construction drones market.

Stringent Airspace and Privacy Rules

Regulatory fragmentation remains one of the clearest limits on expansion in the construction drones market. Dense urban project areas often sit under controlled airspace, which makes approvals, waivers, and operating conditions more complex than the technology itself. In the US, the FAA published its BVLOS Notice of Proposed Rulemaking in August 2025, with a performance-based framework across multiple population-risk categories, and the comment process remained active into 2026. In Europe, EASA Amendment 5 to Regulation (EU) 2019/947 took effect in May 2025, and France ended its legacy national-standard scenarios from January 2026, requiring migration toward EU-specific-category authorization under DGAC oversight. These differences increase compliance effort for firms operating across borders or near sensitive sites, and they favor larger operators with stronger legal and aviation support resources. Until operating rules become more predictable, the construction drones market will continue to face slower scaling in more regulated environments.

Other drivers and restraints analyzed in the detailed report include:

- Autonomous Monitoring to Offset Labor Shortages

- Declining Sensor and Battery Costs

- Cyber-Security Vulnerabilities in COTS Drones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rotary-wing platforms held 71.17% of the 2025 construction drones market share, reflecting their strong fit for urban job sites, confined takeoff areas, and hovering tasks. These systems remain the default choice for many contractors because they are easier to deploy around buildings, temporary structures, and active work zones. The construction drones market still relies on multi-rotor flexibility for facade inspection, progress capture, and localized surveying. Within the construction drones industry, this format also aligns with training and operational practices that many field teams already understand. That installed familiarity helps explain why rotary-wing systems continue to set the baseline for new fleet adoption.

Fixed-wing platforms serve a different role in the construction drones market, especially on large corridor and land-scale assignments where endurance matters more than hover performance. Highway alignments, pipeline routes, and coastal assets remain better matched to longer-range flight profiles. Even so, the gap between rotary-wing and fixed-wing use is narrowing as mission efficiency improves across several aircraft classes. Hybrid VTOL platforms are expected to grow at a 13.43% CAGR through 2031 because they combine practical field deployment with broader area coverage. In the construction drones market, that mix is attractive for bridge, dam, renewable, and remote civil projects that need both transit efficiency and close inspection capability.

Hardware accounted for 57.64% of the construction drones market in 2025, indicating that fleet build-out still starts with aircraft, payloads, and supporting equipment. Many firms are still in the early stages of program development, so capital spending on equipment accounts for a significant share of total revenue. Services fill the gap for contractors that prefer outsourced flying, data capture, or compliance support on a project basis. The construction drones market, therefore, still has a strong front-end hardware profile even though long-term value is shifting elsewhere. This pattern is common where installed bases are still growing, and operating models vary widely by contractor size.

Software is forecast to grow at a 12.77% CAGR through 2031, making it the fastest-growing component in the construction drones market. The main reason is that value is moving toward data processing, AI-assisted analytics, mission planning, and integration with project systems. Research on drone and digital twin workflows supports this shift because real-time synchronization depends on data handling and model comparison, not just on aircraft deployment. As programs mature, customer retention is increasingly tied to platform usability and workflow integration rather than only to the aircraft brand. Within the construction drones industry, software is the clearest long-term source of differentiation and recurring revenue.

Geography Analysis

North America held 37.56% of the construction drones market share in 2025, making it the largest regional segment. The region benefits from a large construction spending base, active technology adoption among major contractors, and broad use of digital project workflows. AGC reported that 26% of US construction firms planned to increase drone investment in 2025, suggesting a shift from pilot programs to recurring budgets. The construction drones market in North America also reflects strong demand for secure and compliant platforms as federal and regulated project work becomes more selective on procurement standards.

Europe remains a mature secondary region in the construction drones market, supported by a more harmonized regulatory base than many other multi-country markets. EASA Amendment 5 to Regulation (EU) 2019/947 took effect in May 2025, which helped shape operating expectations across member states. France imposed a near-term compliance burden when legacy national-standard scenarios ended in January 2026, and operators had to move toward EU-specific category authorization under DGAC oversight. Even with that transition cost, the construction drones market in Europe remains supported by cross-border service potential and continued use in inspection and progress monitoring. The UK, Germany, and France remain the leading adoption centers within the region.

Asia-Pacific is the fastest-growing regional segment in the construction drones market, with a projected CAGR of 13.32% through 2031. China and India are the main scale drivers, though demand patterns differ between rapid smart-site deployment and infrastructure-led adoption. Japan is an important indicator of operational maturity. In March 2025, KDDI Smart Drone and Obayashi Corporation completed a fully remote, automated drone inspection demonstration at an active dam construction site using Skydio Dock for X10. South Korea also demonstrated the shift toward autonomous operations when DJI Enterprise published a March 2026 case study on SK Construction's use of DJI Dock 3 for remote construction site management during winter conditions. South America, the Middle East, and Africa remain smaller markets for construction drones. Still, large infrastructure corridors, energy projects, and selective smart-city investments continue to open demand for surveying, earthwork monitoring, and inspection services.

- SZ DJI Technology Co., Ltd.

- Asteria Aerospace Limited

- Parrot Drones SAS

- 3DR, Inc.

- Yuneec (ATL Drone)

- AeroVironment, Inc.

- Firmatek, LLC

- Skycatch, Inc.

- DroneDeploy Inc.

- Delair SAS

- Autel Robotics Co. Ltd.

- ideaForge Technology Ltd.

- Wingtra AG

- Flyability SA

- American Robotics, Inc.

- Garuda Aerospace Pvt. Ltd.

- Skydio, Inc.

- Aerodyne Group

- Multinnov

- Terra Drone Corporation

- Skyline Software Systems Inc.

- Donecle

- Energy Robotics GmbH

- Intertek Group plc

- NADAR Drone Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption for site surveying and mapping

- 4.2.2 Declining sensor and battery costs

- 4.2.3 Post-pandemic infrastructure stimulus

- 4.2.4 Building Information Modeling digital-twin integration pull-through

- 4.2.5 Insurer-led risk-monitoring mandates

- 4.2.6 Autonomous monitoring to offset labor shortages

- 4.3 Market Restraints

- 4.3.1 Stringent airspace and privacy rules

- 4.3.2 Shortage of licensed drone pilots

- 4.3.3 Cyber-security vulnerabilities in commercial-off-the-shelf (COTS) drones

- 4.3.4 High lifecycle maintenance costs of fleets

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Rotary-Wing

- 5.1.2 Fixed-Wing

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Application

- 5.3.1 Land Surveying and Topographic Mapping

- 5.3.2 Progress Monitoring and Documentation

- 5.3.3 Infrastructure Inspection

- 5.3.4 Security and Surveillance

- 5.3.5 Earth work and Volume Measurement

- 5.4 By End-User

- 5.4.1 Residential Construction Firms

- 5.4.2 Commercial Construction Contractors

- 5.4.3 Industrial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SZ DJI Technology Co., Ltd.

- 6.4.2 Asteria Aerospace Limited

- 6.4.3 Parrot Drones SAS

- 6.4.4 3DR, Inc.

- 6.4.5 Yuneec (ATL Drone)

- 6.4.6 AeroVironment, Inc.

- 6.4.7 Firmatek, LLC

- 6.4.8 Skycatch, Inc.

- 6.4.9 DroneDeploy Inc.

- 6.4.10 Delair SAS

- 6.4.11 Autel Robotics Co. Ltd.

- 6.4.12 ideaForge Technology Ltd.

- 6.4.13 Wingtra AG

- 6.4.14 Flyability SA

- 6.4.15 American Robotics, Inc.

- 6.4.16 Garuda Aerospace Pvt. Ltd.

- 6.4.17 Skydio, Inc.

- 6.4.18 Aerodyne Group

- 6.4.19 Multinnov

- 6.4.20 Terra Drone Corporation

- 6.4.21 Skyline Software Systems Inc.

- 6.4.22 Donecle

- 6.4.23 Energy Robotics GmbH

- 6.4.24 Intertek Group plc

- 6.4.25 NADAR Drone Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment