|

시장보고서

상품코드

2062061

아스팔트 싱글 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asphalt Shingles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

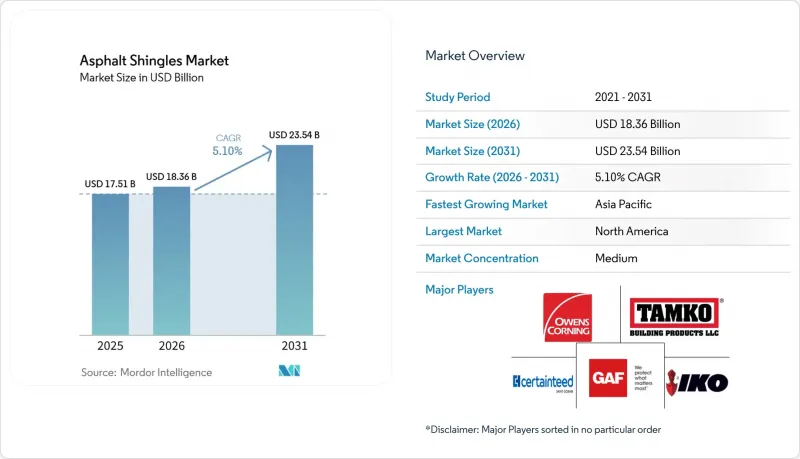

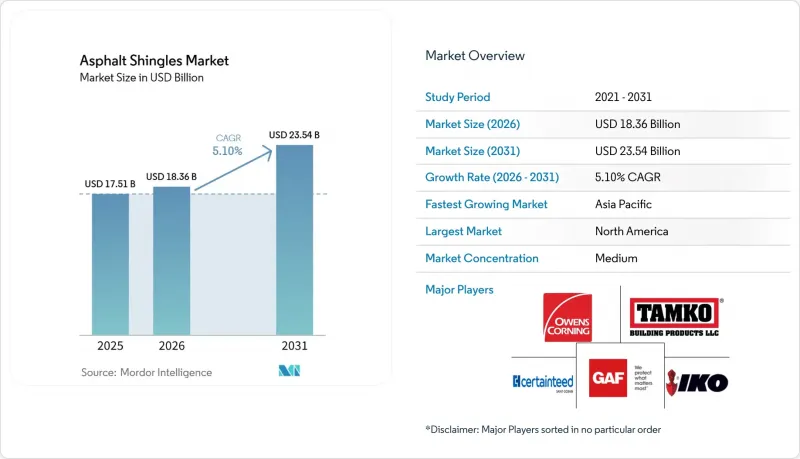

Mordor Intelligence에 의하면, 아스팔트 싱글 시장 규모는 2025년 175억 1,000만 달러, 2026년 183억 6,000만 달러에서 2031년까지 235억 4,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.10%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(3탭 싱글, 럭셔리/디자이너 싱글 등), 보강재(유리 섬유 매트 및 유기 매트), 유통 채널(업체 직접 판매 등), 용도(신축 주택 등), 그리고 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 아스팔트 싱글 시장 동향 및 분석

주택 건설 및 지붕 교체 수요의 확대

아스팔트 싱글 시장에서는 교체 수요가 주류를 이루고 있으며, 미국에서 연간 약 500만 건의 시공 중 85%를 지붕 교체 공사가 차지하고 있습니다. 또한, 기상 조건의 악화로 인해 평균 수명은 19년으로 단축되었습니다. 2025년에는 지붕 교체 사유 중 누수와 동일한 비율인 33%가 폭풍우로 인한 피해로 나타났으며, 이는 기후 변화의 심화가 설비 투자를 앞당기고 있음을 여실히 보여주고 있습니다. 인도의 도시화는 새로운 수요를 창출하고 있습니다. 정부의 주택 지원 프로그램과 지하철망 확충에 힘입어, 해당 국가의 지붕 자재 시장 규모는 2033년까지 117억 달러에 달할 것으로 전망됩니다. 노동력 부족으로 인해 임금이 상승하고 있으며, 2026년에는 북미 건설업체의 39%가 AI 기반 일정 관리 도구를 도입할 것으로 예측됩니다. 이러한 요인들이 복합적으로 작용함에 따라, 지붕 재시공 수요는 높은 수준을 유지할 것이며, 아스팔트 싱글 시장 전체에서 가격 안정성이 유지될 것입니다.

비용 대비 효과가 높은 시공과 수명 주기 경제성

아스팔트 싱글은 평방피트당 3.50-5.50달러에 시공할 수 있지만, 금속 패널은 7-14달러가 듭니다. 또한, 2인 1조로 작업할 경우 2,000제곱피트 규모의 지붕 공사를 단 2일 만에 완료할 수 있습니다. 이러한 신속한 시공 덕분에 2024년부터 2025년까지 8-12% 상승했던 인건비 급등 현상이 완화되고 있습니다. 100톤 이상의 대량 주문을 활용하는 구매자는 10-15%의 자재 비용 절감을 실현하여, 비용 면에서의 우위를 더욱 공고히 하고 있습니다. 금속 지붕의 수명은 40-70년이지만, 50년 동안 두 차례에 걸쳐 아스팔트 지붕을 교체하는 데 드는 총 비용은 여전히 금속 지붕보다 저렴한 수준이거나 그와 비슷한 수준을 유지하고 있어, 아스팔트 싱글 시장의 가치는 여전히 인정받고 있습니다.

기상 이변이나 풍압으로 인한 부상 위험

허리케인 이후의 조사에 따르면, 아스팔트 싱글 지붕의 결함 중 30-40%는 자재 결함이 아닌 시공 실수에 기인하며, 지은 지 10년 미만의 지붕에서 발생하고 있습니다. 인력 부족으로 인해 못 박기 패턴의 오류나 탭의 밀봉 불량이 발생할 가능성이 높아지고 있습니다. 플로리다주 등 일부 주에서는 연안 지역에 시속 110마일(약 177km/h)의 내풍 성능이 의무화되어 있어, 제조업체들은 접착 강도를 높이거나 고정 장치의 수를 늘려야 하는 상황에 직면해 있습니다. 이로 인해 원자재비가 최대 10% 증가했습니다.

부문별 분석

2025년 기준으로, 아키텍처럴 싱글과 라미네이트 싱글은 아스팔트 싱글 시장 전체의 57.8%를 차지했습니다. 클래스 4 규격 제품은 10-15% 더 비싸지만, 보험료 절감 효과 덕분에 7년 이내에 그 차액을 회수할 수 있다고 합니다. 고급/디자이너용 지붕 자재는 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 6.2%로 성장할 것으로 전망됩니다. 이는 북미와 유럽의 고소득층 구매자들이 50년 보증이 적용되는 슬레이트 스타일의 제품을 선호하기 때문입니다. 3탭 지붕 자재는 가격에 민감한 지역을 제외하고는 수요가 감소하는 추세이지만, 라틴아메리카나 동남아시아의 일부 지역에서는 여전히 예산 제약 조건을 충족시키고 있습니다.

성장 가능성은 발전 기능과 외관의 매력을 결합한 태양광 대응 라미네이트 제품에 집중되어 있습니다. GAF Energy사의 ‘Timberline Solar ES 2’와 CertainTeed사의 ‘Solstice Shingle’은 혁신이 어떻게 수요를 고수익 SKU로 이끌어내는지 보여주고 있습니다. 그 결과, 총 면적 증가세가 완만하더라도 라미네이트 제품으로 인해 아스팔트 싱글 시장 규모는 2031년까지 확대될 것으로 전망됩니다.

2025년에는 유리섬유 매트가 출하량의 78.5%를 차지했습니다. 이는 A급의 내화 성능과 경량성 덕분입니다. 유기 매트 시장 점유율은 동결-해동 주기에서 뛰어난 유연성이 유리하게 작용함에 따라, 2031년까지 연평균 성장률(CAGR) 6.1%로 확대되고 있습니다. 폴리머 개질 아스팔트는 이 두 기재 간의 성능 격차를 좁혀주고 있지만, 설비 투자의 관성으로 인해 북미 생산 라인의 대부분은 여전히 유리섬유용으로 조정되어 있습니다.

셀룰로오스 섬유는 재생 가능한 자원이기 때문에 지속가능성에 대한 관심이 높아짐에 따라 유기농 매트의 매력이 더욱 부각되고 있습니다. 그렇긴 하지만, 아스팔트 포화도가 높기 때문에 이산화탄소 배출 감축의 이점 중 일부는 상쇄되고 있습니다. 어느 소재도 시장을 전면적으로 대체할 정도에는 이르지 않을 것으로 보이기 때문에 아스팔트 싱글 시장은 예측 기간 동안 유리섬유와 유기 매트의 비율이 75 대 25 정도로 안정될 전망입니다.

지역별 분석

2025년, 북미는 전 세계 매출의 42.3%를 차지할 것으로 예상되며, 그 중심에는 미국 내 지붕 교체 공사의 85%를 차지하는 비중이 있습니다. 클래스 4 내충격성 싱글 제품은 이미 텍사스주, 오클라호마주, 콜로라도주에서 약 18%의 시장 점유율을 차지하고 있으며, 남동부 지역의 생산 능력 확충은 허리케인 피해 복구 수요가 정점에 달할 시기에 맞추어 진행되고 있습니다. 캐나다에서는 추운 주에서 유기 매트에 대한 수요가 집중되는 반면, 멕시코에서의 성장은 저경사 지붕에 대한 설치를 촉진하는 산업의 니어쇼어링과 연동되어 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 6.24%로, 가장 빠르게 성장하고 있는 지역입니다. 인도 시장 점유율만 보더라도, 도시로의 인구 이동이 합리적인 가격의 주택 수요를 견인하고 있어 확대가 예상됩니다. 중국 주택 시장의 둔화는 국내 전자상거래용 창고 건설로 상쇄되고 있으며, 또한 일본의 태풍 피해 위험 증가로 인해 클래스 4 폴리머 개질 적층재의 채택이 촉진되고 있습니다. 호주에서는 건축 기준에 ‘내재 탄소(제조 과정에서 배출되는 탄소)’ 보고가 포함되어 있으며, 2026년 이후 쿨 루프 및 순환형 아스팔트 솔루션의 도입이 촉진될 가능성이 있습니다.

유럽에서는 EU 규정에 따른 환경 제품 선언(EPD) 및 디지털 패스포트 도입으로 인해 2027년부터는 원자재의 투명성이 의무화되어, 고탄소 원료에 대한 압박이 강화되는 한편, 재활용 실증 사업을 수행하는 제조업체에게는 유리하게 작용할 것입니다. 스칸디나비아 국가들과 독일에서는 인프라 투자에 따른 완만한 성장이 예상되는 반면, 프랑스와 영국에서는 재정적 제약으로 인해 단기적인 수요가 억제될 전망입니다. 남미, 중동, 북아프리카의 신흥 시장은 점유율이 한 자릿수에 그치지만, 도시 인프라 및 기후 변화에 강한 지붕재에 관한 건축 기준과 관련하여 예상보다 높은 성장세를 보일 가능성이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the asphalt shingles market size is projected to expand from USD 17.51 billion in 2025 and USD 18.36 billion in 2026 to USD 23.54 billion by 2031, registering a CAGR of 5.10% between 2026 to 2031.

This report is Segmented by Product Type (Three-Tab Shingles, Luxury/Designer Shingles, and More), Reinforcement (Fiberglass Mat and Organic Mat), Distribution Channel (Direct-To-Contractors, and More), Application (Residential-New Build, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Asphalt Shingles Market Trends and Insights

Growing Residential Construction and Reroofing Demand

Replacement dominates the Asphalt shingles market, with reroofing representing 85% of roughly five million United States installations each year, and the mean service life sliding to 19 years because of more severe weather. Storm damage matched leaks at 33% of reroof triggers in 2025, underscoring how climate volatility is pulling capital spending forward. Urbanization in India is adding greenfield demand; government housing programs and metro expansions have pushed the national roofing segment toward USD 11.7 billion by 2033. Labor scarcity is elevating wages, prompting 39% of North American contractors to adopt AI scheduling tools in 2026. These factors combine to keep reroof volumes high and sustain price discipline across the Asphalt Shingles market.

Cost-Effective Installation and Life-Cycle Economics

Asphalt shingles install for USD 3.50-5.50 per square foot versus USD 7-14 for metal panels, and a two-person crew can finish a 2,000-square-foot roof in as little as two days. Rapid installation tempers rising labor rates, which climbed 8-12% between 2024 and 2025. Buyers leveraging bulk orders of 100-plus tons secure 10-15% material savings, reinforcing the cost advantage. Although metal roofs last 40-70 years, the total outlay over 50 years for two asphalt replacements still runs below or near the metal premium, preserving value perception in the Asphalt Shingles market.

Vulnerability to Extreme Weather and Wind Uplift

Post-hurricane audits show 30-40% of asphalt shingle failures occur on roofs under 10 years old because of installation errors rather than material faults. Labor shortages raise the likelihood of missed nailing patterns and under-sealed tabs. States such as Florida now require 110 mph ratings in coastal zones, driving manufacturers to boost adhesive strength and fastener counts, which raises bill-of-materials costs by up to 10%.

Other drivers and restraints analyzed in the detailed report include:

- Architectural Laminated Shingles Popularity

- Cool-Roof and Energy-Code Driven Demand

- Bitumen-Related Environmental and Disposal Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Architectural/laminated shingles contributed 57.8% to the overall Asphalt Shingles market share in 2025. Class-4 versions cost 10-15% more yet yield insurer savings that recover the premium within seven years. Luxury/Designer shingles are expected to grow at a CAGR of 6.2% during the forecast period (2026-2031) as upscale buyers in North America and Europe favor slate-look blends that offer 50-year guarantees. Three-tab shingles are fading outside price-sensitive regions but still meet budget constraints in parts of Latin America and Southeast Asia.

Upside potential centers on solar-ready laminates that merge energy generation with curb appeal. GAF Energy's Timberline Solar ES 2 and CertainTeed's Solstice Shingle illustrate how innovation steers demand toward higher-margin SKUs. As a result, the Asphalt shingles market size attributable to laminates is projected to widen through 2031 even if total square footage grows modestly.

Fiberglass mat dominated 78.5% of shipments in 2025, helped by its Class A fire rating and lower weight. Organic mat's market share is advancing at a 6.1% CAGR to 2031, where freeze-thaw cycles favor its bendability. Polymer-modified asphalt is shrinking the performance gap between the two substrates, yet capital inertia keeps most North American lines tuned for fiberglass.

Sustainability narratives are boosting organic mat's appeal because cellulose fibers are renewable. Nevertheless, higher asphalt saturation offsets some carbon benefits. With neither substrate poised for wholesale displacement, the Asphalt shingles market is likely to stabilize near a 75-25 fiberglass-organic split over the forecast window.

Geography Analysis

North America supplied 42.3% of worldwide revenue in 2025, anchored by an 85% reroof mix in the United States. Class-4 impact-resistant shingles already hold roughly 18% share across Texas, Oklahoma, and Colorado, and southeastern capacity additions are timed to meet hurricane recovery peaks. Canadian demand skews toward organic mat in colder provinces, while Mexican growth aligns with industrial nearshoring that drives low-slope installations.

Asia-Pacific is the fastest-growing region at 6.24% CAGR to 2031. India's market share alone is on track to expand as urban migration fuels affordable housing. China's residential slowdown is counterbalanced by warehouse construction for domestic e-commerce, and Japan's typhoon exposure is lifting adoption of Class-4 polymer-modified laminates. Australia is incorporating embodied-carbon reporting into its building code, which could spur uptake of cool-roof and circular asphalt solutions beginning in 2026.

In Europe, upcoming environmental product declarations and digital passports under EU regulation will oblige material transparency from 2027, pressuring high-carbon inputs yet favoring makers with recycling pilots. Scandinavia and Germany may see modest gains tied to infrastructure spending, whereas fiscal constraints in France and the United Kingdom temper short-term volume. Emerging markets in South America, the Middle East, and North Africa contribute single-digit shares but present upside tied to urban infrastructure and climate-resilient roofing codes.

- Atlas Roofing Corporation

- BP Canada (Building Products of Canada)

- Carlisle Construction Materials

- CertainTeed

- GAF Materials LLC

- Henry Company

- IKO Industries, Inc.

- Johns Manville

- Malarkey Roofing Products

- Owens Corning

- PABCO Roofing Products

- Polyglass U.S.A., Inc.

- Repsol

- Roofing Corp of America

- Sika AG

- Siplast Inc.

- Soprema Group

- TAMKO Building Products LLC

- Tarco Roofing

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing residential construction and reroofing demand

- 4.2.2 Cost-effective installation and life-cycle economics

- 4.2.3 Architectural laminated shingles popularity

- 4.2.4 Cool-roof and energy-code-driven demand

- 4.2.5 Climate-resilient Class-4 polymer-modified laminates

- 4.3 Market Restraints

- 4.3.1 Vulnerability to extreme weather and wind-uplift

- 4.3.2 Bitumen-related environmental and disposal concerns

- 4.3.3 Growing appeal of metal and composite substitutes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Three-tab Shingles

- 5.1.2 Architectural/Laminated Shingles

- 5.1.3 Luxury/Designer Shingles

- 5.1.4 Strip Shingles

- 5.2 By Reinforcement Material

- 5.2.1 Fiberglass Mat

- 5.2.2 Organic Mat

- 5.3 By Distribution Channel

- 5.3.1 Roofing-Supply Distributors

- 5.3.2 Direct-to-Contractors

- 5.3.3 Retail Home-Center Stores

- 5.3.4 E-commerce/Online

- 5.4 By Application

- 5.4.1 Residential-New Build

- 5.4.2 Residential-Reroofing

- 5.4.3 Commercial Low-Slope

- 5.4.4 Institutional and Public

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 Australia

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Atlas Roofing Corporation

- 6.4.2 BP Canada (Building Products of Canada)

- 6.4.3 Carlisle Construction Materials

- 6.4.4 CertainTeed

- 6.4.5 GAF Materials LLC

- 6.4.6 Henry Company

- 6.4.7 IKO Industries, Inc.

- 6.4.8 Johns Manville

- 6.4.9 Malarkey Roofing Products

- 6.4.10 Owens Corning

- 6.4.11 PABCO Roofing Products

- 6.4.12 Polyglass U.S.A., Inc.

- 6.4.13 Repsol

- 6.4.14 Roofing Corp of America

- 6.4.15 Sika AG

- 6.4.16 Siplast Inc.

- 6.4.17 Soprema Group

- 6.4.18 TAMKO Building Products LLC

- 6.4.19 Tarco Roofing

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Circular-Economy Asphalt Shingle Recycling

- 7.3 Solar-Ready Reflective Shingle Formats