|

시장보고서

상품코드

2062062

엔진 구동식 용접기 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Engine Driven Welders - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

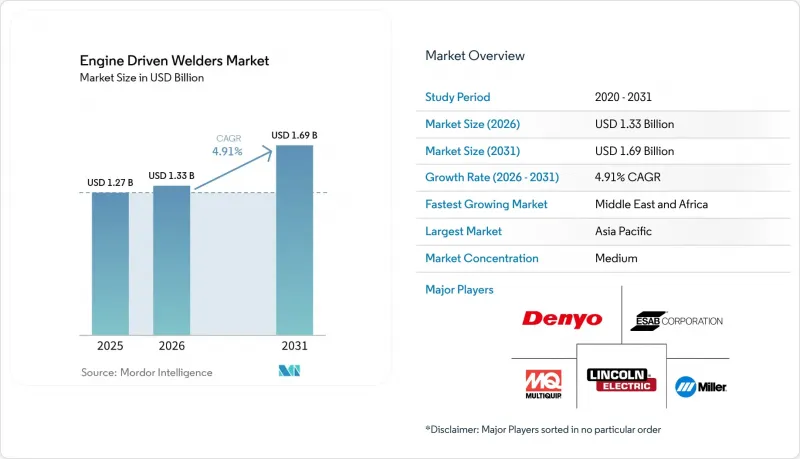

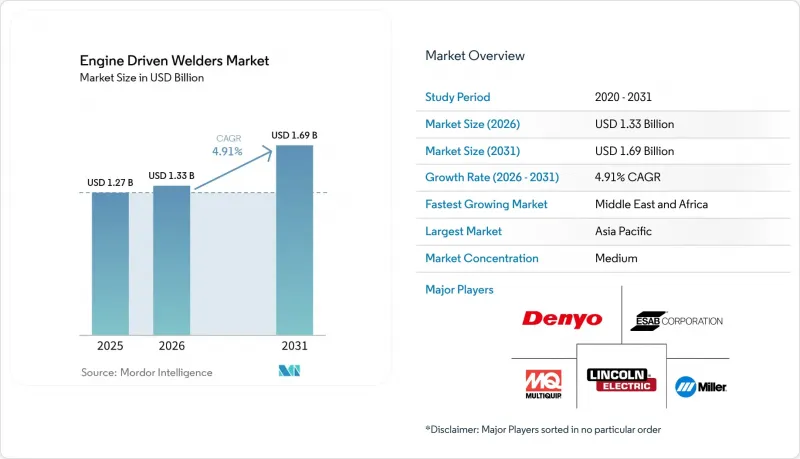

Mordor Intelligence에 의하면, 엔진 구동식 용접기 시장 규모는 2025년에 12억 7,000만 달러로 평가되었고, 2026년에 13억 3,000만 달러로 추정되고, 2031년까지 16억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 4.91%로 성장할 전망입니다.

본 보고서는 출력별(0-100A, 101-300A, 기타), 연료 유형별(가솔린, 디젤, 기타), 용접 공정별(아크 용접(SMAW), MIG 용접(GMAW), 기타), 최종 사용자 산업별(건설 인프라, 기타), 지역별(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 엔진 구동식 용접기 시장 동향 및 분석

석유 및 가스 파이프라인 인프라 확충

파이프라인 건설 주기는 수년에 걸친 프로젝트 기간 동안 자동 원주 용접에 필요한 재현성 있는 아크 안정성을 제공할 수 있는 고전류 및 정전압 엔진 구동형 플랫폼에 대해 여전히 지속적인 수요의 원동력이 되고 있습니다. INGAA 재단의 북미 장기 전망에 따르면, 2052년까지 약 14만 마일의 새로운 가스 수송 및 집약 능력이 추가될 것으로 강조되고 있으며, 이를 통해 각 작업 현장에서 이동식 용접 전원에 의존하는 부지 확보 작업의 기준선이 유지될 것입니다. 최근 활동 실적을 보면, 진행 중이거나 계획 중인 프로젝트의 총액은 수백억 달러 규모에 달하며, 그 예로 퍼미안 분지의 생산량을 멕시코만 연안으로 수송하기 위한 신규 노선, 지역 수요 거점을 지원하기 위한 캐나다의 수송 능력 확충 등을 들 수 있습니다. 이러한 건설 속도에 발맞추어, 변화하는 환경 조건 하에서 예열, 모따기 공차, 엄격한 공정 관리에 대응할 수 있는 용접 시스템에 대한 지속적인 수요가 발생하고 있습니다. 프로젝트 일정은 중류 부문의 경제 상황이나 하류 부문의 인수 조건에 쉽게 영향을 받기 때문에 착공일이 변경될 가능성이 있지만, 건설 단계에서 현장 용접 전원에 대한 구조적인 필요성이 사라지는 경우는 거의 없습니다. 자동화에 대응하는 듀티 사이클과 여유 있는 보조 전원을 갖춘 견고하고 고출력 모델을 표준화하는 설비 기획 담당자는 이러한 파이프라인의 수주 잔고 상황에서도 두꺼운 이음매나 장시간의 용접 작업 시에도 가동률을 확보할 수 있습니다.

원격지 및 지방에서의 건설 활동 확대

데이터센터 단지, 재생에너지 발전, 회랑 인프라와 관련된 작업량은 계속 증가하고 있으며, 초기 단계에서 전력망이 취약하거나 이용할 수 없는 지역으로 더 많은 활동이 이동하고 있습니다. 미국에서는 2026년 계획 문서가 전체 착공 건수의 완만한 증가를 시사하고 있으며, 민간 사무실 건설 분야에서는 높은 전력 용량과 장기간의 건설 공정이 필요한 하이퍼스케일 데이터센터가 주류를 이루고 있습니다. 이로 인해 용접 작업자들은 철골 프레임, 랙, 보조 구조물의 시공에 매달리게 됩니다. 엔진 구동식 용접기는 주전원으로부터 멀리 떨어진 장소에서도 안정적인 아크를 유지하면서 공구, 공기 압축기, 조명에 전력을 공급할 수 있어 이러한 작업을 뒷받침하고 있습니다. 도급업체는 서비스 트럭에 적재량에 최적화된 올인원 시스템을 중점적으로 도입함으로써 운영의 균형을 맞추고, 왕복 횟수를 줄이며, 설치 시간을 단축하고 있습니다. 이는 대규모의 분산된 현장에서 더욱 큰 가치를 발휘합니다. 자재비, 관세, 인허가 절차로 인해 공사 기간이 길어지는 경우도 있지만, 전력 소비량이 많은 시설을 분산된 장소에 건설해야 하기 때문에 구조물 용접과 MRO(유지보수·수리·정비) 용접 두 분야 모두에서 이동식 플랫폼이 선호되고 있습니다. 엔진 구동식 용접기의 성능 데이터를 일정 관리 및 인력 배치와 연동하는 도급업체는 가동률에 대한 인사이트를 얻을 수 있을 뿐만 아니라, 원격지 작업 현장에서 발생하는 연료비를 절감할 수 있습니다.

밀폐된 공간에서의 사용을 제한하는 배기가스 규제

용접과 관련된 일부 금속에 대해 유독성 대기 오염 물질로 지정됨에 따라, 밀폐된 공간에서 환기 없이 엔진을 가동하는 것이 제한되고 있으며, 이로 인해 좁은 실내 환경에서의 디젤 엔진 사용이 제한되고 있습니다. 규제가 적용되는 관할 구역에서는 배기가스 기준에 따라 디젤 엔진에 후처리 장치를 장착하고 정기적인 재생 주기를 이행해야 하므로, 유지보수 절차가 늘어나 장시간 근무 일정에 영향을 미치고 있습니다. 제조업체들은 상황에 따라 LPG/CNG 대체 연료를 채택하거나, 엔진 배기가스를 발생시키지 않고 아크 전원을 공급하는 배터리 하이브리드 시스템을 도입하는 등 이러한 제약 사항에 대응하고 있습니다. 지하 작업이나 밀폐된 공간에서의 현장 규정 또한 배기가스가 적고 설치 면적이 작은 장비에 대한 관심을 높이고 있습니다. 안전한 환기 및 흄 추출을 표준화하고, 장비를 대기질 요건에 부합하도록 하는 조직은 규정 준수를 유지하면서 생산성을 확보하고 있습니다. 이러한 추세는 엔진 구동 용접기 시장의 복합 기술 포트폴리오를 강화하고 있습니다.

부문별 분석

101-300암페어급은 2025년 매출의 44.67%를 차지했으며, 분산된 작업 현장의 파이프라인 작업자 및 경-중규모 구조물 제작의 주력으로서 여전히 중요한 위치를 차지하고 있습니다. 이러한 기계 유형은 휴대성과 일반적인 전극을 사용하면서도, 내장 발전기를 통해 보조 공구에 전력을 공급하기에 충분한 출력 여유를 갖추고 있어, 이를 통해 현장에서 소규모 팀의 생산성을 유지하고 있습니다. 구매자는 표면 상태가 변하는 강재에서 불리한 자세로 작업해야 하는 상황에 대비하여, 안정적인 아크 특성, 높은 듀티 사이클, 케이블 관리가 용이한 모델을 선정하고 있습니다. 이러한 용접기를 대규모로 도입하는 기업들은 장비의 성능을 규격에 확실히 부합하는 일관된 용접 결과로 이어지게 하기 위해, AWS의 구조물 및 파이프라인 규격에 관한 교육을 실시하는 경우가 많습니다. 이 출력 대역의 매력은 그 유연성에 있습니다. 엔진 구동식 용접기 시장에서 서비스 차량의 적재 중량을 적정 수준으로 유지하면서도 다양한 이용 사례에 대응할 수 있다는 점이 특징입니다.

500암페어 이상의 기계 유형의 경우, 중공업 및 조선소에서의 두꺼운 판재 용접 자동화가 진행되고 있으며, 콘크리트 및 철강 메가 프로젝트에서 더 높은 용접 속도가 요구됨에 따라 2031년까지 연평균 5.21%의 성장이 예상됩니다. 고성능 기계 모델의 가치 제안은 가혹한 작동 조건에서도 지속적인 출력을 유지하면서도 트럭이나 스키드에 탑재할 수 있는 컴팩트한 설치 면적을 실현했다는 점에 있으며, 이를 통해 작업 팀은 대형 현장 조립 작업에 산업용 수준의 성능을 적용할 수 있습니다. 또한 사용자들은 에어 아크 가우징에 대한 전력 공급 능력과 안정적인 스프레이 전송을 통해 더 굵은 와이어 직경을 사용할 수 있다는 점을 높이 평가하고 있으며, 이를 통해 용접 패스 수를 줄일 수 있습니다. 용접, 압축 공기, 보조 전원을 통합한 여러 모델은 사후 장착 작업을 간소화하고, 적재량과 적재 공간을 절약하는 단일 섀시 솔루션으로의 전환을 반영하고 있습니다. 이 플랫폼의 통합을 통해 장비의 분산을 줄일 수 있으며, 엔진 구동 용접기 시장에서 매일 다양한 철골 공사에 투입되는 작업팀의 준비 시간을 단축할 수 있습니다.

디젤 파워트레인은 내구성, 부하 시 연비, 전력망 지원이 없는 외딴 지역에서의 장시간 가동 능력이라는 강점을 바탕으로 2025년 세계 판매 점유율의 67.81%를 차지했습니다. 파이프라인 및 중장비 건설 도급업체들은 저회전 영역에서의 강력한 토크와 1급 현장에서의 안전한 운용 특성 때문에 디젤 엔진을 선호하며, 이를 통해 급유 시의 위험성이 줄어듭니다. 유지보수 용이성 또한 차별화 요소로 작용하며, 정기적인 정비가 가동 주기에 맞추어 이루어질 경우, 성숙한 부품 네트워크와 긴 엔진 수명을 확보할 수 있습니다. ESG 정책과 지역 배출 규제가 강화되는 가운데, 차량 소유주들은 연속 가동 능력을 저해하지 않으면서도 보다 친환경적인 운행을 실현하기 위해, 적절한 작업 시 LPG 혼합이 가능한 듀얼 연료 키트의 도입을 추진하고 있습니다. 이러한 하이브리드 방식은 공회전 관리 및 텔레매틱스를 활용한 유지보수와 결합함으로써, 엔진 구동 용접기 시장에서 소유자가 비용을 관리하면서도 현장 규정을 준수할 수 있도록 해줍니다.

LPG/CNG 대체 연료 시장은 연평균 5.78%의 성장률을 보일 것으로 예상되며, 대기질 규제가 엄격한 실내 및 도시 지역에서의 활용도가 높아지고 있습니다. 소유주는 질소산화물 및 미세먼지 배출을 줄이고, 밀폐된 공간에서의 디젤 엔진 사용이 제한된 현장에 대한 접근성을 확보하기 위해 이러한 솔루션을 도입하고 있습니다. 가솔린은 구매 가격이나 경량성이 장시간 가동 시의 효율보다 더 중요하게 여겨지는 초급 모델이나 경량 작업 용도, 특히 간헐적인 수리나 농업 용도에서 여전히 널리 사용되고 있습니다. 엔진과 배터리를 결합한 하이브리드 구성이 친환경적인 운전과 장시간 작업 사이의 격차를 해소하는 솔루션으로 등장하고 있으며, 소형 배터리 우선 모델은 이미 특정 밀폐 공간이나 전력 제한이 있는 환경에서 사용되고 있습니다. 주유 네트워크와 충전 인프라가 성숙해짐에 따라, 엔진 구동식 용접기 시장에서 규제 및 가동 주기가 허용하는 한, 하이브리드 및 대체 시스템이 디젤 기계를 계속해서 보완해 나갈 것으로 보입니다.

지역별 분석

아시아태평양은 강력한 제조거점과 다양한 기후 및 지형에 걸친 회랑, 에너지 자산, 산업 시설의 확장을 지속하는 대규모 유틸리티 프로그램을 배경으로, 2025년 매출의 48.21%를 차지했습니다. 조선, 자동차, 에너지, 대규모 인프라와 관련된 제조업은 일시적인 전력 공급이 필요한 지역에서 건설 및 MRO(유지보수·수리·정비) 업무 모두에서 이동식 용접기의 정기적인 사용을 뒷받침하고 있습니다. 해당 지역의 프로젝트 구성은 습도가 높거나 고온, 혹은 고지대 같은 환경에서도 안정적인 아크와 신뢰성 높은 보조 전원을 갖춘 장비를 선호하는 경향이 있습니다. 소유자가 디지털 모니터링 및 원격 파라미터 제어를 도입하는 사례가 늘어남에 따라, 텔레매틱스 기능을 갖춘 멀티프로세스 플랫폼이 서비스용 차량 전체에서 주목을 받고 있습니다. 배출 규제는 도시나 국가에 따라 다르기 때문에 실내나 규제가 엄격한 현장에서는 LPG나 하이브리드 장비가 선택적으로 도입되고 있지만, 엔진 구동식 용접기 시장에서는 야외 프로젝트에서 여전히 디젤 장비가 주류를 이루고 있습니다.

북미에서는 구조용 강재, 에너지 인프라, 그린필드 부지의 이동식 전원에 의존하는 데이터센터 사업의 확대에 힘입어 수요가 안정적인 추세를 보이고 있습니다. 건설업체들은 인력 부족 문제에 대응하기 위해, 설치 시간을 단축하고 소수의 작업 팀으로 1교대당 작업량을 늘릴 수 있는 통합형 용접기에 대한 투자를 확대되고 있습니다. 티어 4 최종 규제와 지역별 유해 대기 오염 물질 분류에 따라 밀폐된 공간에서의 디젤 사용이 제한됨에 따라, 실내 작업이나 주거지 인근에서의 야간 근무 시 LPG 및 하이브리드 옵션에 대한 관심이 높아지고 있습니다. 현장 수리나 유틸리티 분야에서는 원격지나 기상 조건의 영향을 쉽게 받는 환경에서 장시간 사용하기에 적합한 견고한 디젤식 장비가 여전히 선호되고 있습니다. 렌탈 업체와 차량 운영 사업자 사이에서 텔레매틱스 도입이 확대됨에 따라, 가동률 추적이 엔진 구동식 용접기 시장의 차량 교체 결정에 영향을 미치고 있습니다.

중동 및 아프리카은 각국이 메가 프로젝트를 추진하고, 에너지 및 석유화학 생산 능력을 확대하며, 공공 서비스 네트워크를 현대화함에 따라 7.21%라는 가장 높은 성장률을 나타낼 것으로 전망됩니다. 가혹한 환경 조건과 거점 간 장거리 이동으로 인해 내구성, 유지보수의 용이성, 신뢰성 높은 현지 부품 공급망의 중요성이 더욱 커지고 있습니다. 소유주는 가동 중단 위험을 줄이기 위해 보증 범위와 소모품 공급 체계를 갖춘 유통업체 네트워크를 보유한 세계 브랜드를 표준으로 채택하는 경우가 많습니다. 대규모 제조 현장이나 현장 팀은 전체 장비군에서 부품을 공통화할 수 있는 고출력 멀티 프로세스 용접기를 활용함으로써, 재고 관리 및 교육의 간소화라는 이점을 얻고 있습니다. 인프라 및 에너지 투자 분야의 장기적인 프로젝트 기간과 자본 집약성은 엔진 구동식 용접기 시장의 대형 용도 및 서비스 트럭 용도 장비 수요를 지속적으로 뒷받침하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the engine driven welders market size is projected to be USD 1.27 billion in 2025, USD 1.33 billion in 2026, and reach USD 1.69 billion by 2031, growing at a CAGR of 4.91% from 2026 to 2031.

This report is Segmented by Power Output (0-100 A, 101 - 300 A, and More), by Fuel Type (Gasoline, Diesel, and More), by Welding Process (Stick Welding (SMAW), MIG Welding (GMAW) and More), by End-User Industry (Construction & Infrastructure, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Engine Driven Welders Market Trends and Insights

Expansion of Oil and Gas Pipeline Infrastructure

The pipeline buildout cycle remains a durable demand engine for high-amperage, constant-voltage engine-driven platforms that can deliver repeatable arc stability for automated girth welding over multi-year project timelines. The INGAA Foundation's long-range outlook for North America highlights around 140,000 miles of new gas transmission and gathering capacity additions through 2052, which sustains a baseline of right-of-way work that depends on mobile welding power at every spread. Recent activity tallies track tens of billions of dollars in active and proposed projects, with examples that include greenfield routes designed to move Permian volumes to Gulf Coast egress and Canadian capacity expansions to support regional demand centers. The construction cadence brings recurring needs for welding systems that handle preheats, bevel tolerances, and strict procedure control in variable environmental conditions. Project timing remains sensitive to midstream economics and downstream offtake conditions, which can shift start dates but rarely eliminate the structural need for on-site welding power in the build phase. Equipment planners who standardize on rugged high-output models with automation-ready duty cycles and auxiliary power headroom protect utilization across thick-wall and long-duration joints in this pipeline backlog context.

Growing Construction Activity in Remote and Rural Areas

Workloads tied to data centre campuses, renewable generation, and corridor infrastructure continue to expand and are shifting more activity into locations where the grid is weak or unavailable during early phases. In the United States, 2026 planning documents point to modest overall start growth, with private office construction dominated by hyperscale data centers that demand high electrical capacity and long construction sequences, which keep welding crews busy across steel frames, racks, and auxiliary structures. Engine-driven welders support this motion because they can power tools, air compressors, and lighting while maintaining stable arcs away from mains power. Contractors balance deployment by emphasizing payload-optimized all-in-one systems on service trucks to cut trips and reduce setup time, which becomes more valuable on large, dispersed sites. Input costs, tariffs, and permitting have extended some timelines, yet the requirement to build out power-hungry facilities in dispersed locations favors mobile platforms for both structural and MRO welding scopes. Contractors that link engine-driven welder performance data to scheduling and labor allocation gain utilization insight and contain fuel overhead on remote work packages.

Emission Regulations Restricting Usage in Enclosed Spaces

Toxic air contaminant designations for several welding-related metals limit unvented engine operation in enclosed spaces, which has narrowed diesel use in tight indoor environments. In regulated jurisdictions, emission standards drive the adoption of aftertreatment and periodic regeneration cycles on diesel engines, adding maintenance steps and affecting scheduling on long shifts. Owners address these constraints with LPG/CNG alternatives in some settings and with battery-hybrid systems that supply arc power without continuous engine exhaust. Site rules in underground work and confined spaces have also accelerated interest in equipment with lower tailpipe emissions and smaller footprints. Organizations that standardize safe ventilation and fume extraction and match equipment to air-quality requirements maintain compliance while preserving productivity. This pattern is reinforcing a mixed-technology toolbox within the engine-driven welders market.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Mobile Welding and Maintenance Services

- Increasing Military and Defense Field Operations Requirements

- High Fuel Consumption and Operational Cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 101-300 ampere class captured 44.67% of 2025 revenue and remains the workhorse for pipeline crews and light-to-medium structural fabrication across dispersed job sites. These units balance portability with enough output headroom to run common electrodes and to power auxiliary tools through onboard generators, which keeps small teams productive in the field. Buyers select models with stable arc characteristics, strong duty cycles, and easy cable management to handle out-of-position work on steels with variable surface conditions. Companies that deploy these machines at scale often train on AWS structural and pipeline codes so that equipment capability translates into consistent, code-compliant welds. The appeal of this band is its flexibility, which covers a wide swath of use cases while keeping total truck payload in check for service vehicles in the engine-driven welders market.

Above 500 amperes, units are projected to grow at 5.21% through 2031 as heavy fabrication and shipyards automate thick-plate welding and as megaprojects in concrete and steel require higher deposition rates. The value proposition at the high end is sustained output under demanding duty cycles with a footprint that still allows truck or skid mounting, so teams can bring industrial-grade capability to large field assemblies. Users also value the ability to power air-arc gouging and to run larger wire diameters with stable spray transfer, which reduces pass counts. Several integrated models combine welding, compressed air, and auxiliary power to simplify upfits, reflecting the shift to single-chassis solutions that save payload and bed space. That platform consolidation reduces equipment sprawl and speeds setup for crews tasked with diverse steelwork on a given day in the engine-driven welders market.

Diesel powertrains held 67.81% of global sales in 2025 on the strength of durability, fuel efficiency under load, and the ability to run long hours on remote sites without grid support. Pipeline and heavy construction contractors prefer diesel because of robust torque at low RPM and safe handling characteristics on Tier 1 sites, which lowers hazards during refueling. Serviceability is also a differentiator, with mature parts networks and long engine lifecycles when maintenance is consistent and aligned to duty cycles. As ESG policies and local emission constraints tighten, fleet owners are piloting dual-fuel kits that allow LPG blending on appropriate jobs to achieve cleaner operation without losing continuous-duty power. That hybridized approach, paired with idle management and telematics-driven maintenance, allows owners to control costs while meeting site rules in the engine-driven welders market.

LPG/CNG alternatives are projected to expand at 5.78% per year, lifting their role in regulated indoor and urban applications where air-quality limits are tight. Owners adopt these solutions to reduce nitrogen oxide and particulate output and to gain access to sites that restrict diesel engines in enclosed areas. Gasoline continues to serve entry-level and light-duty use where purchase price and low weight matter more than long-hour efficiency, especially for intermittent repair and farm applications. Hybrid configurations that pair engines with batteries are emerging to bridge the gap between clean operation and long shifts, with compact battery-first models already serving certain confined or power-limited environments. As refueling networks and charging infrastructure mature, hybrid and alternative systems will continue to supplement diesel where rules and duty cycles permit in the engine-driven welders market.

Geography Analysis

Asia-Pacific held 48.21% of 2025 revenue on the back of strong manufacturing bases and large public works programs that continue to expand corridors, energy assets, and industrial facilities across diverse climates and terrains. Fabrication tied to shipbuilding, automotive, energy, and large-scale infrastructure sustains regular use of mobile welders for both construction and MRO tasks in areas where temporary power is necessary. The region's project mix favors equipment that can operate in humid, hot, or high-altitude conditions with stable arcs and reliable auxiliary power. As more owners layer in digital monitoring and remote parameter control, multiprocess platforms with telematics are gaining attention across service fleets. Emission constraints vary by city and country, which is prompting selective uptake of LPG and hybrid units for indoor or restricted sites, while diesel remains dominant on open-air projects in the engine-driven welders market.

North America shows stable demand patterns supported by structural steel, energy infrastructure, and expanding data center activity that relies on mobile power at greenfield sites. Contractors respond to labor shortages by investing in integrated welders that compress setup time and allow smaller crews to cover more tasks per shift. Tier 4 Final rules and local toxic air contaminant classifications limit diesel use in enclosed spaces, which lifts interest in LPG and hybrid options for indoor work or night shifts near residences. Field repair and utility work continue to favor robust diesel units for long-hour use in remote or weather-exposed settings. As telematics gain traction across rental and fleet operators, utilization tracking is influencing fleet renewal choices in the engine-driven welders market.

The Middle East and Africa region is projected to grow fastest at 7.21% as countries advance megaprojects, expand energy and petrochemical capacity, and modernize utility networks. Harsh environmental conditions and long distances between depots raise the value of ruggedness, simple maintenance access, and reliable local parts channels. Owners often standardize on global brands that maintain distributor networks with warranty coverage and consumable pipelines to reduce downtime risk. Large fabrication yards and field teams benefit from high-output multiprocess units that share components across fleets, which simplifies stocking and training. The long project horizons and capital intensity of infrastructure and energy investments continue to underpin equipment needs across heavy-duty and service-truck applications in the engine-driven welders market.

- Lincoln Electric Holdings Inc.

- Miller Electric Mfg LLC (ITW)

- ESAB Corp.

- Denyo Co., Ltd.

- Multiquip Inc.

- Vanair Manufacturing

- Hobart Brothers LLC

- MOSA S.p.A.

- Shindaiwa Ltd.

- Atlas Copco AB

- Doosan Portable Power

- Generac Power Systems

- Kohler Co. (Engines)

- Cummins Inc. (Onan Division)

- Briggs & Stratton (Vanguard)

- Harbor Freight (VULCAN Brand)

- AGG Power Solutions

- Yamaha Motor Co. (Industrial Engines)

- Oerlikon Welding (Air Liquide)

- Westinghouse Outdoor Power

- Kipor Power

- Daihen Corp.

- Riland Industrial Co.

- Rental Fleet Leaders (United Rentals, Sunbelt)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Oil and Gas Pipeline Infrastructure

- 4.2.2 Growing Construction Activity in Remote and Rural Areas

- 4.2.3 Rising Demand from Agricultural Equipment Manufacturing and Repair

- 4.2.4 Increasing Military and Defense Field Operations Requirements

- 4.2.5 Growth in Mobile Welding and Maintenance Services

- 4.2.6 Natural Disaster Recovery and Emergency Infrastructure Repair

- 4.3 Market Restraints

- 4.3.1 High Fuel Consumption and Operational Cost

- 4.3.2 Noise Pollution and Operator Discomfort

- 4.3.3 Frequent Maintenance Requirements and Downtime

- 4.3.4 Emission Regulations Restricting Usage in Enclosed Spaces

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Application-Driven Power Output Segmentation

- 4.9 Dual-Purpose Value Proposition Driving Premium Segment

5 Market Size & Growth Forecasts(Value, In USD)

- 5.1 By Power Output

- 5.1.1 0 - 100 A

- 5.1.2 101 - 300 A

- 5.1.3 301 - 500 A

- 5.1.4 Above 500 A

- 5.2 By Fuel Type

- 5.2.1 Gasoline

- 5.2.2 Diesel

- 5.2.3 LPG / CNG

- 5.2.4 Alternative & Hybrid Systems

- 5.3 By Welding Process

- 5.3.1 Stick Welding (SMAW)

- 5.3.2 MIG Welding (GMAW)

- 5.3.3 TIG Welding (GTAW)

- 5.3.4 Advanced Multi-Process (Pulse-MIG, Gouging)

- 5.4 By End-User Industry

- 5.4.1 Construction & Infrastructure

- 5.4.2 Oil & Gas / Pipeline

- 5.4.3 Mining & Quarrying

- 5.4.4 Shipbuilding & Marine

- 5.4.5 Power Generation & Utilities

- 5.4.6 Automotive and General Manufacturing

- 5.4.7 General Maintenance & Repair

- 5.4.8 Others (Agriculture & Farming, Rental & Leasing Companies, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Lincoln Electric Holdings Inc.

- 6.4.2 Miller Electric Mfg LLC (ITW)

- 6.4.3 ESAB Corp.

- 6.4.4 Denyo Co., Ltd.

- 6.4.5 Multiquip Inc.

- 6.4.6 Vanair Manufacturing

- 6.4.7 Hobart Brothers LLC

- 6.4.8 MOSA S.p.A.

- 6.4.9 Shindaiwa Ltd.

- 6.4.10 Atlas Copco AB

- 6.4.11 Doosan Portable Power

- 6.4.12 Generac Power Systems

- 6.4.13 Kohler Co. (Engines)

- 6.4.14 Cummins Inc. (Onan Division)

- 6.4.15 Briggs & Stratton (Vanguard)

- 6.4.16 Harbor Freight (VULCAN Brand)

- 6.4.17 AGG Power Solutions

- 6.4.18 Yamaha Motor Co. (Industrial Engines)

- 6.4.19 Oerlikon Welding (Air Liquide)

- 6.4.20 Westinghouse Outdoor Power

- 6.4.21 Kipor Power

- 6.4.22 Daihen Corp.

- 6.4.23 Riland Industrial Co.

- 6.4.24 Rental Fleet Leaders (United Rentals, Sunbelt)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment