|

시장보고서

상품코드

2062064

스트레치 및 수축 필름 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Stretch And Shrink Film - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

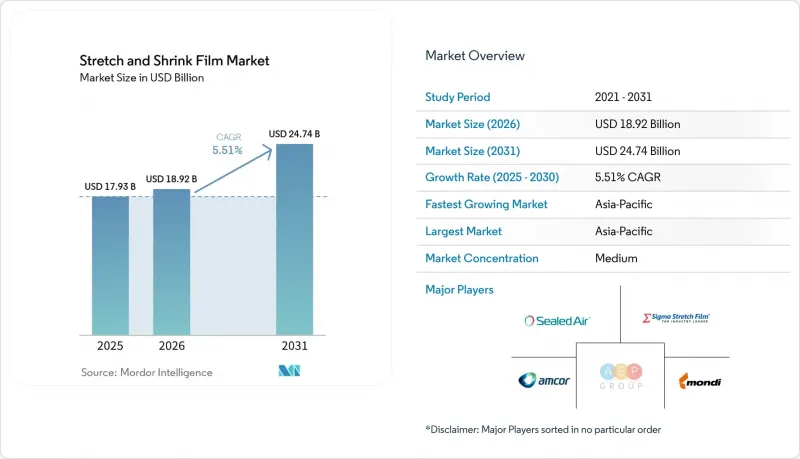

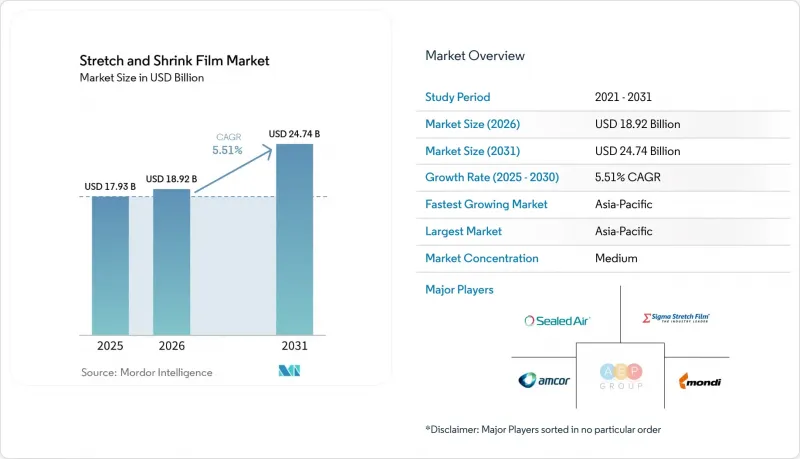

Mordor Intelligence에 의하면, 스트레치 및 수축 필름 시장 규모는 2025년 179억 3,000만 달러로 평가되었고, 2026년에는 189억 2,000만 달러로 추정되고, 2026-2031년 CAGR 5.51%로 성장을 지속할 전망이며, 2031년까지 247억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 필름 유형별(스트레치, 수축), 소재별(LLDPE, LDPE, MLLDPE, PVC 등), 두께별(15mm 이하, 15-25mm, 25mm 이상), 용도별(팔레트 포장, 슬리브 및 라벨, 위조 개봉 방지, 기타), 최종 사용자별(식품 및 음료, 제약, 전자, 제조, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러)으로 표시되어 있습니다.

세계의 스트레치 및 수축 필름 시장 동향과 인사이트

팔레트 유닛화 및 부정 개봉 방지 하역에 대한 수요 증가

경공업 생산 거점이 멕시코와 미국 남동부로 돌아오면서, 화물의 모서리 파손이나 적재물 이동을 방지하기 위한 안전한 복합 운송의 필요성으로 인해 팔레트화된 화물의 양이 증가했습니다. 2026년에는 북미의 소포 처리량이 250억 개를 넘어섰습니다. 무질서하게 적재된 상자 운송에서 팔레트 운송으로 전환하는 비율이 단 1%만 증가해도, 손해배상 청구 건수가 약 10% 감소할 것으로 예측됩니다. 특히 제약 및 전자기기 업계의 화주들 사이에서는 FDA의 21 CFR Part 11 전자 기록 규정에 따른 준수 요건으로 인해, 파단 스트립이 부착된 위변조 방지 랩에 대한 수요가 증가하고 있습니다. 인도에서는 시간당 200개의 팔레트를 처리할 수 있는 자동 스트레치 랩 시스템을 도입하여, 온도 및 습도 변동으로 인해 화물 고정 강화가 필요한 수출 노선의 과제를 해결하고 있습니다. 수작업에서 자동화 라인으로의 전환은 팔레트당 인건비를 최대 60% 절감하고 필름 사용량을 최대 35% 줄일 수 있다는 점에 힘입어, 임금 수준이 낮은 지역에서도 2년 이내에 투자 회수가 가능해졌습니다.

얇은 필름 개발 및 재활용 가능한 필름을 통한 지속가능성 추구

2030년까지 유럽연합(EU)의 '포장 및 포장 폐기물 규정'에 따라 연포장재에는 재활용 소재를 35% 포함해야 하며, 완전히 재활용 가능해야 합니다. 이를 위반할 경우, 기업의 연간 매출액의 최대 3%에 해당하는 벌금이 부과될 수 있습니다. 이에 대응하여 각 변환기 제조업체들은 수지 사용량을 약 50% 줄이면서도 내천자성을 갖춘 12마이크론 두께의 메탈로센계 스트레치 필름을 채택하고 있습니다. 또한, 7층 공압출 기술을 통해 모서리 유지 강도를 유지하면서 스트레치 후드 필름의 두께를 100μm에서 80μm로 얇게 만들 수 있게 되었습니다. 한편, 미국에서는 캘리포니아주의 SB 54법에 따라 2032년까지 일회용 플라스틱 포장을 25% 감축해야 합니다. 또한 해당 주는 재활용 인프라를 강화하기 위해 연간 최대 5억 달러에 달할 수 있는 수수료를 부과하고 있습니다. 이로 인해 각 브랜드에 재활용이 가능하고 가벼운 필름을 선택하도록 하는 압박이 더욱 거세지고 있습니다.

기계적 재생 PE 스트림의 오염

소매용 스트레치 필름 베일에는 라벨이나 접착제가 포함되어 있는 경우가 많아, 이로 인해 클린 플레이크의 수율은 60-75%로 떨어집니다. PVC나 폴리프로필렌이 극소량만 혼입되어도 새로운 필름 내에서 겔을 형성하여, 용융유동지수가 허용 범위를 벗어나는 원인이 됩니다. 인디애나주의 SYNDIGO 시설과 같은 폐쇄형 재활용 시설에서는 엄격한 선별 절차를 통해 85% 이상의 회수율을 달성하고 있지만, 대부분의 기계적 재활용 네트워크는 여전히 품질 편차 문제에 직면해 있습니다. 이러한 불균일성으로 인해 식품 접촉 용도나 고투명도 용도에 적합한 재생 소재의 비율이 제한되고 있습니다.

부문별 분석

2025년에는 스트레치 필름이 시장을 독점하며 총 매출의 63.11%를 차지했습니다. 이는 주로 시간당 최대 200개의 팔레트를 처리할 수 있는 자동 포장기의 광범위한 사용 덕분입니다. 이러한 성장은 전자상거래 물류센터 및 근해 공장에서 투명도가 높고 무단 개봉 방지 기능을 갖춘 유닛화 제품에 대한 수요가 증가함에 따라 주도되고 있습니다. 수지 사용량을 최소화하면서도 놀라운 300%의 프리 스트레치율을 실현하는 프리오리엔티드 나노 레이어 필름과 같은 혁신 기술이 이러한 성장을 뒷받침하고 있습니다. 또한, 최종 소비자들은 특히 농산물 유통 분야에서 습기 배출을 촉진하는 천공 스트레치 필름을 점점 더 선호하는 추세입니다.

2025년에는 수축 필름이 36.89%의 시장 점유율을 차지했으나, 2031년까지 연평균 5.89%의 성장률을 기록하며 스트레치 필름을 추월할 것으로 전망됩니다. 이러한 급증은 음료 멀티팩 및 슬리브 라벨에서 PVC에서 폴리올레핀으로의 전환에 기인한 것입니다. 폴리올레핀의 활성화 온도 범위인 200-275°F는 터널 내 체류 시간을 단축할 뿐만 아니라, 특히 2025년에 발효될 예정인 주 차원의 금지 조치를 고려할 때, PVC와 관련된 다이옥신 문제에 대한 우려에도 대응하고 있습니다. 또한, 투명도가 높은 배합은 현재 매장 내 수거 및 재활용 규정에 부합하고 있어, 각 브랜드별로 신속한 전환이 진행되고 있습니다. 또한, 동남아시아와 중동의 콜드체인 인프라 확충도 수축 필름 수요를 견인하고 있으며, 온도 변동 속에서도 밀봉 강도를 확보하고 있습니다.

LLDPE는 15-25%의 비용 경쟁력과 기존 압출기와의 폭넓은 호환성 덕분에 2025년 매출의 48.36%를 차지했습니다. LLDPE 스트레치 및 수축 필름 시장 점유율은 메탈로센 블렌드가 2031년까지 연평균 성장률(CAGR) 5.76%로 증가함에 따라 소폭 하락할 것으로 예측됩니다. 이는 운송 중량을 최대 30%까지 줄일 수 있는 얇은 두께 설계의 이점을 누리고 있기 때문입니다. 2025년, 전 세계 메탈로센 수지의 생산 능력은 연간 2,600만 톤을 넘어설 전망이며, 인도의 가공 제조업체들은 우수한 하중 유지력이 요구되는 수출 시장에 대응하기 위해 연평균 6.15%의 속도로 이 수지를 도입하고 있습니다.

기존에는 틈새 시장이었던 폴리올레핀 수축 필름은 유럽과 북미에서 재활용 규제가 강화됨에 따라 시장 규모가 급속히 확대되고 있습니다. 저밀도 폴리에틸렌(LLDPE)은 높은 밀착성과 광택이 요구되는 핸들 필름 용도에서 여전히 중요하지만, 광학적 특성과 강성이 중요한 특정 산업용 슬리브를 제외하면 PVC 시장 점유율은 계속해서 감소하고 있습니다. 각 브랜드 소유 기업들이 2030년까지 사용 후 플라스틱을 25-30% 함유하겠다고 약속함에 따라, 재생 폴리에틸렌의 성장세가 가속화되고 있습니다. SYNDIGO사의 재생 LLDPE는 내천자성 시험에서 동등한 성능이 입증됨에 따라, 비식품용 랩 시장에서 이미 버진 등급을 대체해 가고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 41.25%를 차지한 것으로 평가되었으며, 2031년까지 연평균 6.19%의 성장률을 보일 것으로 전망됩니다. 구자라트주와 카르나타카주에서 진행되는 224억 루피(2억 5,100만 달러) 규모의 생산 능력 확충은 걸프 국가 및 동남아시아로의 수출을 촉진할 것입니다. 중국은 최대공급량을 자랑하지만, 내수 소비의 둔화로 인해 가공업체들은 해외 시장으로 진출하고 있는 반면, 인도, 베트남, 태국에서는 다국적 기업의 고객 사양을 충족하기 위해 자동 스트레치 후딩 설비의 도입이 진행되고 있습니다. 일본, 한국, 호주 등 선진국에서는 재활용이 가능한 단층 필름과 생산 라인의 자동화 업그레이드에 주력하고 있습니다.

북미는 2025년에 2위를 차지했으며, 이 지역 최대의 수축 필름 플랫폼을 구축한 암콜과 베리의 합병이 이를 뒷받침했습니다. 시그마 플라스틱 그룹이 조지아주에서 진행하는 3,900만 달러 규모의 확장 사업을 통해 2026년 12월까지 15만 평방피트의 스트레치 필름 생산 능력이 추가될 예정이며, 이로 인해 켄튀르키예주와 캘리포니아주 거점 간공급 격차가 해소될 것으로 보입니다. 미국은 전자상거래 소포 처리량 증가와 남동부 지역으로의 니어쇼어링으로 인한 혜택을 누리고 있는 반면, 멕시코와 캐나다는 2024년 이후 발표된 400억 달러 규모의 제조업 투자를 바탕으로 자동차 및 전자기기 분야에서 스트레치 후드의 도입이 확대되고 있습니다.

유럽의 동향은 '포장 및 포장 폐기물 규정'에 의해 뒷받침되고 있으며, 이 규정에 따르면 2030년까지 재활용 소재 사용 비율을 35%로 의무화하고 있습니다. 독일, 영국, 프랑스, 이탈리아, 스페인은 성숙한 재활용 인프라와 야심 찬 브랜드 공약 덕분에 소비를 주도하고 있습니다. 동유럽 국가들은 낮은 인건비와 제조 클러스터와의 근접성을 활용해 새로운 필름 공장을 유치하고 있습니다. Coveris사는 2025년 독일 할레에 1,050만 달러를 투자하여 재활용 가능한 단층 필름의 생산 능력과 의료용 등급 생산 라인을 확장했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the stretch and shrink film market size is expected to grow from USD 17.93 billion in 2025 to USD 18.92 billion in 2026 and is forecast to reach USD 24.74 billion by 2031 at 5.51% CAGR over 2026-2031.

This report is Segmented by Film Type (Stretch, Shrink), Material (LLDPE, LDPE, MLLDPE, PVC, and More), Thickness (≤15 Mm, 15-25 Mm and More), Application (Pallet Wrapping, Sleeve/Label, Tamper-Evident, and More), End-User (F&B, Pharma, Electronics, Manufacturing, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). Market Forecasts are in Value (USD).

Global Stretch And Shrink Film Market Trends and Insights

Rising Demand for Pallet Unitization and Tamper-Proof Loads

As light manufacturing was reshored to Mexico and the U.S. Southeast, the volume of palletized freight increased, driven by the need for secure multi-modal transport to prevent edge tears and load shifting. In 2026, parcel traffic in North America exceeded 25 billion units. A shift of just one percentage point from loose cartons to palletized shipping is projected to reduce damage claims by approximately 10%. The demand for tamper-evident wraps with tear strips is growing, particularly among pharmaceutical and electronics shippers, due to compliance requirements with the FDA's 21 CFR Part 11 electronic-records regulations. In India, the installation of automated stretch-hooding systems, with a capacity of 200 pallets per hour, is addressing export lane challenges where temperature and humidity fluctuations require improved load retention. The transition from manual to automated lines is driven by the potential to lower labor costs by up to 60% per pallet and reduce film usage by as much as 35%, offering a return on investment within two years, even in regions with lower wage scales.

Sustainability Push for Downgauged and Recyclable Films

By 2030, the European Union's Packaging and Packaging Waste Regulation requires flexible packaging to contain 35% recycled content and be fully recyclable. Non-compliance could lead to penalties of up to 3% of a company's annual turnover. In response, converters are turning to a 12-micron metallocene-based stretch film, which offers puncture resistance while using nearly 50% less resin. Additionally, the seven-layer coextrusion technology has allowed for a reduction in stretch-hood film gauges from 100 µm to 80 µm, maintaining corner-hold strength. Meanwhile, in the U.S., California's SB 54 mandates a 25% cut in single-use plastic packaging by 2032. The state also imposes fees, potentially reaching USD 500 million annually, to bolster recycling infrastructure. This intensifies the push on brands to choose recyclable and lighter films.

Contamination in Mechanical-Recycled PE Streams

Retail stretch-film bales often include labels and adhesives, which reduce the yield of clean flake to 60-75%. Even small amounts of PVC or polypropylene can form gels in new film, causing melt-flow indices to fall outside acceptable limits. While closed-loop initiatives such as the SYNDIGO facility in Indiana have achieved yields above 85% through strict sorting protocols, much of the mechanical-recycling network continues to face variability. These inconsistencies limit the proportion of recycled content suitable for food-contact or high-clarity applications.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of F&B Cold-Chain Requiring High-Clarity Shrink Film

- Automation of Stretch-Hooding Lines in Emerging Markets

- High Capex for Multilayer Thin-Gauge Extrusion Upgrades

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, stretch film dominated the market, accounting for 63.11% of total revenue, largely due to its widespread use in automated wrappers capable of processing up to 200 pallets per hour. This growth is driven by the rising demand from e-commerce warehouses and nearshored factories for high-clarity, tamper-evident unitization. Innovations like pre-oriented nano-layer films, which offer a remarkable 300% pre-stretch ratio while minimizing resin usage, are fueling this expansion. Additionally, end users are increasingly favoring perforated stretch films, especially for produce distribution, as they facilitate moisture dissipation.

While shrink film accounted for the 36.89% market share in 2025, it's projected to surpass stretch film, growing at an annual rate of 5.89% until 2031. This surge is attributed to the shift from PVC to polyolefin in beverage multipacks and sleeve labels. Polyolefin's activation window of 200-275 °F not only reduces tunnel residence times but also addresses dioxin concerns associated with PVC, especially in light of state-level bans set to take effect in 2025. Furthermore, high-clarity formulations are now compliant with store drop-off recycling protocols, prompting a swift conversion among brands. The demand for shrink films is also bolstered by the cold-chain infrastructure developments in Southeast Asia and the Middle East, ensuring seal integrity amidst temperature fluctuations.

LLDPE held 48.36% of 2025 sales due to its 15-25% cost edge and broad compatibility with legacy extruders. The stretch and shrink film market share for LLDPE is expected to fall modestly as metallocene blends climb at a 5.76% CAGR through 2031, benefiting from downgauging that shaves freight weight by up to 30%. Global metallocene capacity topped 26 million tpa in 2025, and converters in India are adopting the resin at 6.15% yearly growth to serve export lanes that require superior load retention.

Polyolefin shrink films, traditionally a niche, are scaling quickly as recycling mandates bite in Europe and North America. Low-density polyethylene remains important in hand-film applications that rely on its high cling and gloss, while PVC's share continues to decline except in certain industrial sleeves where optics and stiffness are critical. Recycled polyethylene is gaining momentum as brand owners commit to 25-30% post-consumer content by 2030; SYNDIGO recycled LLDPE is already displacing virgin grades in non-food wraps after proving parity in puncture testing.

Geography Analysis

Asia-Pacific generated 41.25% of 2025 revenue and is projected to grow at 6.19% to 2031. Capacity additions worth Rs 2,240 crore (USD 251 million) in Gujarat and Karnataka will feed exports to Gulf and Southeast Asian corridors. China supplies the largest volume but slower domestic consumption is pushing converters toward overseas markets, while India, Vietnam, and Thailand are adding automated stretch-hooding to meet multinational client specifications. Developed economies such as Japan, South Korea, and Australia focus on recycling-ready mono-films and line automation upgrades.

North America ranked second in 2025, supported by the Amcor-Berry merger that created the region's largest shrink-film platform. Sigma Plastics Group's USD 39 million Georgia expansion will add 150,000 square feet of stretch-film capacity by December 2026, closing a supply gap between Kentucky and California operations. The United States demands benefits from e-commerce parcel volumes and Southeast nearshoring, while Mexico and Canada ride USD 40 billion of announced manufacturing investments since 2024 that favor stretch-hood adoption for automotive and electronics.

Europe's trajectory is anchored by its Packaging and Packaging Waste Regulation, which sets a 35% recycled-content requirement by 2030. Germany, the United Kingdom, France, Italy, and Spain dominate consumption thanks to mature recycling infrastructure and ambitious brand pledges. Eastern European countries attract greenfield film plants leveraging lower labor costs and proximity to manufacturing clusters. Coveris invested USD 10.5 million in Halle, Germany in 2025 to expand recyclable mono-film capacity and medical-grade production lines.

- AEP Industries Inc.

- Amcor plc

- Bonset America Corporation

- Charter Next Generation (CNG)

- Coveris

- Egeria

- Inteplast Group

- IPG

- Mondi

- Paragon Films

- Polifilm Group

- RKW Group

- SABIC

- Sealed Air

- Sigma Plastics Group

- Signode Industrial Group LLC

- Taghleef Industries

- UFlex Limited

- Winpak LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for pallet unitization and tamper-proof loads

- 4.2.2 Sustainability push for downgauged and recyclable films

- 4.2.3 Expansion of F&B cold-chain requiring high-clarity shrink film

- 4.2.4 Automation of stretch-hooding lines in emerging markets

- 4.2.5 Growth of pharma low-temperature distribution channels

- 4.3 Market Restraints

- 4.3.1 Volatility in polyolefin and PVC feedstock prices

- 4.3.2 Contamination in mechanical-recycled PE stream

- 4.3.3 High capex for multilayer thin-gauge extrusion upgrades

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Buyers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of Substitutes

- 4.5.4 Threat of New Entrants

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Film Type

- 5.1.1 Stretch Film

- 5.1.2 Shrink Film

- 5.2 By Material Type

- 5.2.1 Linear Low-Density Polyethylene (LLDPE)

- 5.2.2 Low Density Polyethylene (LDPE)

- 5.2.3 mLLDPE and Metallocene Blends

- 5.2.4 Polyvinyl chloride (PVC)

- 5.2.5 Polyolefin (POF)

- 5.2.6 Other Materials (EVOH, PLA, Recycled PE)

- 5.3 By Thickness

- 5.3.1 Less than or Equal to 15 µm

- 5.3.2 15-25 µm

- 5.3.3 Greater than 25 µm

- 5.4 By Application

- 5.4.1 Pallet Wrapping and Bundling

- 5.4.2 Sleeve and Label Packaging

- 5.4.3 Tamper-evident Overwraps

- 5.4.4 Food and Beverage Packs

- 5.4.5 Industrial Goods Protection

- 5.4.6 Other Applications

- 5.5 By End-user Industry

- 5.5.1 Food and Beverage

- 5.5.2 Pharmaceutical and Healthcare

- 5.5.3 Consumer Electronics and Appliances

- 5.5.4 Industrial Manufacturing

- 5.5.5 E-commerce and Third-Party Logistics

- 5.5.6 Other End-User Industries

- 5.6 By Geography

- 5.6.1 Asia-Pacific

- 5.6.1.1 China

- 5.6.1.2 India

- 5.6.1.3 Japan

- 5.6.1.4 South Korea

- 5.6.1.5 Australia

- 5.6.1.6 Rest of Asia-Pacific

- 5.6.2 North America

- 5.6.2.1 United States

- 5.6.2.2 Canada

- 5.6.2.3 Mexico

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle-East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 South Africa

- 5.6.5.3 Nigeria

- 5.6.5.4 Rest of Middle-East and Africa

- 5.6.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AEP Industries Inc.

- 6.4.2 Amcor plc

- 6.4.3 Bonset America Corporation

- 6.4.4 Charter Next Generation (CNG)

- 6.4.5 Coveris

- 6.4.6 Egeria

- 6.4.7 Inteplast Group

- 6.4.8 IPG

- 6.4.9 Mondi

- 6.4.10 Paragon Films

- 6.4.11 Polifilm Group

- 6.4.12 RKW Group

- 6.4.13 SABIC

- 6.4.14 Sealed Air

- 6.4.15 Sigma Plastics Group

- 6.4.16 Signode Industrial Group LLC

- 6.4.17 Taghleef Industries

- 6.4.18 UFlex Limited

- 6.4.19 Winpak LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment