|

시장보고서

상품코드

2062066

목공 기계 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Woodworking Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

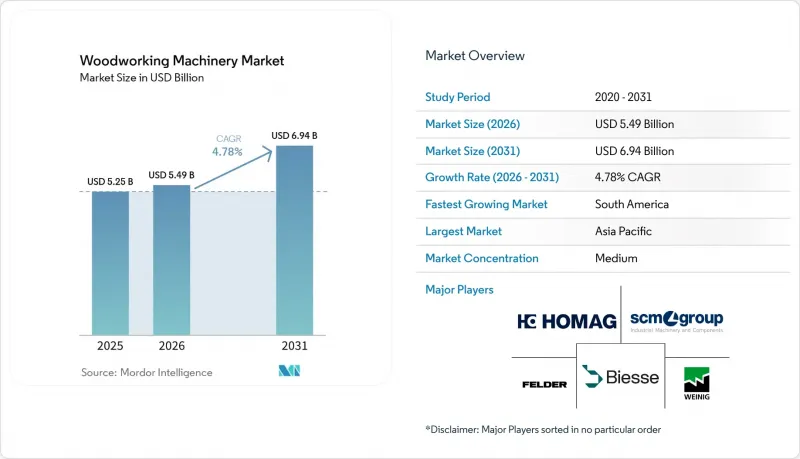

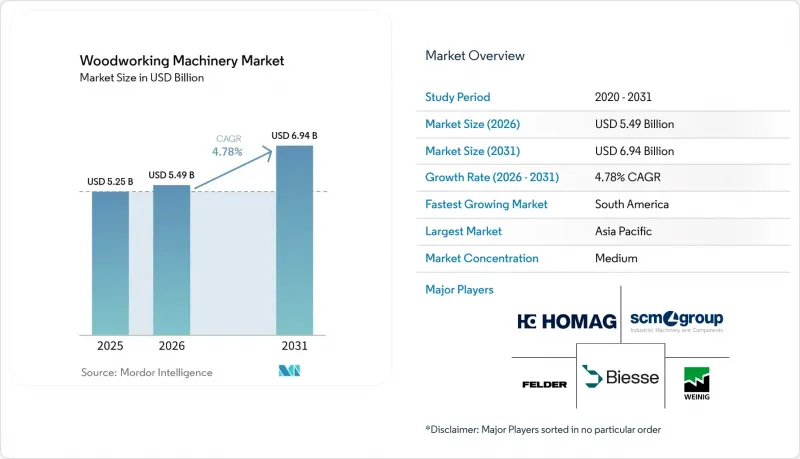

Mordor Intelligence에 의하면, 목공 기계 시장 규모는 2025년 52억 5,000만 달러, 2026년 54억 9,000만 달러에서 2031년까지 69억 4,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 4.78%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(CNC 라우터, 패널 톱 등), 작동 원리(기존/수동, 반자동, 전자동 CNC), 최종 사용자 산업(가구, 건설, 마루, 캐비닛, 기타), 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러)으로 제시되어 있습니다.

세계 목공 기계 시장 동향과 인사이트

세계 가구 제조 업계의 급성장

가구 및 인테리어 제품에 대한 수요가 증가함에 따라, 다품종 소량 생산에서 설비 전환 시간을 단축하고 폐기물을 최소화하는 CNC 라우터, 엣지 밴더, 마감 라인에 대한 투자가 확대되고 있습니다. 미국에서는 2026년 초 주택 건설의 호조가 정밀 목공 장비 및 네스팅 방식의 패널 가공에 의존하는 캐비닛, 목공 제품, 인테리어용 금속 부품 등의 수주 파이프라인을 강화하고 있습니다. 중국의 제조업체들은 고부가가치 엔지니어링 제품 및 수출 경로에 집중하고 있으며, 이에 따라 스크랩을 줄이고 가공 품질을 향상시키기 위해 정밀도가 더 높은 머시닝 센터로의 교체가 활발히 이루어지고 있습니다. 독일의 기계 제조업체들은 2024년의 생산 감소기를 겪은 후 안정세를 되찾았으며, 유연한 제조 요구 사항에 대응하기 위해 자동화 및 소프트웨어 기반 제어에 주력하고 있으며, 이는 중·대규모 공장의 설비 교체 주기를 뒷받침하고 있습니다. 이러한 추세가 맞물리면서, 수동 프로그래밍이 필요 없이 제품 구성을 공구 경로로 변환하는 CNC 호환 생산 셀 및 통합 소프트웨어에 대한 수요가 지속되고 있습니다. 목공 기계 시장이 합판, 소량 맞춤 제작, 디지털 추적성으로 진화함에 따라, 견고한 제어 시스템과 사후 서비스 체계를 갖춘 공급업체는 고부가가치 프로젝트를 수주할 유리한 위치에 있습니다.

모듈식 및 맞춤형 가구에 대한 수요 증가

모듈식 맞춤형 캐비닛 및 가구에 대한 고객의 기대는 목공 기계 시장을 유연한 네스팅, 고정밀 모서리 가공, 그리고 단발성 작업을 효율적으로 수행할 수 있는 소프트웨어 연동 워크플로로 계속해서 이끌고 있습니다. 각 공급업체들은 수주부터 생산 계획, 예측 유지보수에 이르기까지 모든 과정을 연계하는 통합 가공 셀과 커넥티드 플랫폼을 전시하고 있으며, 이를 통해 중견 제조업체들은 예기치 못한 가동 중단을 최소화하면서 더 많은 맞춤형 생산에 대응할 수 있게 됩니다. 모듈식 구조는 위험이 낮다고 할 수 있습니다. 왜냐하면 제조업체는 첫날부터 단일한 고정 구성에 얽매이지 않고, 주문의 복잡성이 증가함에 따라 자동화 공정이나 고성능 스핀들, 혹은 고속 자재 이송 시스템을 추가할 수 있기 때문입니다. 규정 준수에 대한 기대 또한 중요한 요소입니다. 유럽연합(EU)의 산림 파괴 규제로 인해, 2026년 말부터는 EU 시장에 유통되는 목재 제품에 대해 더욱 강력한 디지털 추적성이 요구될 것이기 때문입니다. 이는 문서 작성이나 로트 분류를 자동화할 수 있는 소프트웨어 통합형 공장에 유리하게 작용합니다. 준비가 완료된 제조업체는 이러한 기능을 활용하여 신속하게 견적을 산출하고, 로트 규모별로 작업을 계획하며, 장시간의 가동 중단 없이 작업을 전환할 수 있습니다. 목공 기계 시장은 이러한 ‘구성 가능한 처리량’에 대한 수요에 맞추어 변화하고 있으며, 소량 생산을 대규모로 유지하기 위한 제어 시스템, 공구 관리, 서비스 생태계로 가치가 이동하고 있습니다.

첨단 기계에 대한 막대한 설비 투자 필요성

첨단 CNC 설비는 막대한 초기 투자가 필요하기 때문에 차입 비용이 높고 현금 흐름이 어려운 중소기업의 도입을 지연시키고 있습니다. 각 공장에서는 5축 가공 기능 및 로봇 핸들링의 장점과, 설치, 공구, 소프트웨어, 집진 설비, 작업자 교육 등을 포함한 총 소유 비용(TCO) 간의 균형을 신중하게 검토하고 있습니다. 많은 구매자들은 반자동 공정부터 시작해 가동률이 향상됨에 따라 로더, 스캐너 또는 고속 드라이브를 추가하는 방식으로 자동화를 단계적으로 도입하고 있으며, 이를 통해 투자 비용을 수년까지 분산시키고 있습니다. 리퍼브 제품은 도입 비용을 절감할 수 있지만, 유지보수 부담이 늘어날 가능성이 있으며, 연결형 대시보드나 추적 기능을 기본으로 지원하는 최신 제어 시스템이 탑재되어 있지 않은 경우가 있습니다. 서비스 및 교육과 연계된 금융 상품을 제공하는 공급업체는 예측 가능한 월별 비용을 필요로 하는 소규모 구매자의 도입 위험을 줄이는 데 도움이 됩니다. 이러한 현실이 목공 기계 시장의 업그레이드 속도를 좌우하고 있으며, 특히 기술 지원이나 부품 조달을 확보하기 어려운 주요 제조 거점 이외의 지역에서 그 현상이 두드러집니다.

부문별 분석

CNC 라우터는 2025년에 36.1%의 시장 점유율을 차지해, 복잡한 형상의 가공 및 빈번한 설비 전환에 대응할 수 있는 유연한 시스템을 원하는 구매자들 수요에 힘입어 2031년까지 연평균 성장률(CAGR) 5.8%로 성장할 것으로 전망됩니다. 이 부문의 강점은 패널 수율을 향상시키는 네스팅 워크플로우와 소량 생산 사이의 가동 중지 시간을 줄여주는 자동 공구 관리 시스템에 있습니다. 패널 쏘는 구조가 간단하고 가격이 저렴하기 때문에 표준화된 절단 용도에서는 여전히 널리 사용되고 있지만, 다품종 생산을 하는 공장에서는 디지털 제어 방식으로의 전환이 꾸준히 진행되고 있습니다. 엣지 밴더, 표면 대패기, 와이드 벨트 샌더는 맞춤형 프로젝트와 대량 생산 프로젝트 모두에서 더 깔끔한 모서리, 더 엄격한 두께 공차, 균일한 마감이 요구되는 추세에 발맞추어 수요가 확대되고 있습니다. 드릴, 테너, 몰더, 밴드쏘, 선반, 모티저 등 기타 기계들은 설계 및 구조적 요건상 접합이나 선삭 가공이 주를 이루는 분야에서 전문적인 역할을 계속 수행하고 있습니다. 목공 기계 시장에서는 작업 내용이 다양해지는 상황에서 라우터가 선호되고 있습니다. 소프트웨어와 통합된 라우터 가공을 통해 인력을 대폭 늘리지 않고도 리드 타임을 단축할 수 있기 때문입니다. 각 라우터 제조업체는 신규 도입 시 가치 실현까지 걸리는 시간을 단축하기 위해 네스팅 소프트웨어와 교육을 패키지로 판매하고 있습니다. 그 결과, CNC 라우터와 관련된 목공 기계 시장 규모는 속도와 재료 효율성을 중시하는 소량 맞춤 제작 및 소프트웨어 중심의 워크플로우에 맞추어 확대될 전망입니다.

그 밖의 제품 분야에서는 처리 능력을 중시한 단일 용도 라인과, 전환 작업에 최적화된 유연한 플랫폼 사이에서 양극화가 진행되고 있습니다. 다품종 생산을 하는 기업은 인건비 절감과 특수 작업을 효율적으로 수행할 수 있다는 점에서 가격 대비 성능이 우수한 라우터를 도입하는 반면, 표준화된 제품의 대량 생산을 하는 기업은 여전히 대량 생산에 최적화된 전용 라인에 투자하고 있습니다. 구매자는 기계적 정밀도뿐만 아니라 에너지 소비량, 스핀들 속도, 제어 인터페이스의 개선도 중요하게 여기기 때문에 교체 주기는 생산성 향상에 맞추어 설정되어 있습니다. 커넥티드 콘솔 및 예측 유지보수 같은 새로운 기능들은 고속 드라이브, 고성능 진공 시스템, 경질 소재의 절삭을 안정적으로 수행하는 고토크 스핀들과 함께 도입되었습니다. 목공 기계 시장에서는 맞춤형 제품과 표준 제품 모두에서 마감 품질과 공차에 대한 기대가 높아짐에 따라, 제품 범주를 초월한 혁신 간의 상호 교류가 계속되고 있습니다. 앞으로 조각, 드릴링, 프로파일링을 결합한 다기능 시스템을 통해 통합 플랫폼으로의 전환이 더욱 가속화될 것입니다. 이에 따라 목공 기계 업계는 라우터, 에지 밴더, 마감 장비에 이르는 종단 간 워크플로우와 상호 운용성에 주력하고 있습니다.

지역별 분석

2025년, 아시아태평양은 세계 수요의 40.8%를 차지했습니다. 이는 중국의 패널 생산 능력, 인도의 수출 확대, 그리고 동남아시아의 수탁 생산이 주도한 결과입니다. 남미는 브라질의 합판 생산 기반 확대와 통화 동향에 따른 해외 투자 지원에 힘입어, 2031년까지 연평균 성장률(CAGR) 6.7%라는 가장 빠른 성장 궤도를 보이고 있습니다. 북미는 성숙한 도입 기반을 갖추고 있으며, 노동력 부족이 지속되는 가운데 설비 교체, 병목 현상 해소 및 자동화 고도화에 초점이 맞추어져 있습니다. 미국에서는 2026년 1월에 148만 7,000채의 주택 착공이 기록되었으며, 이는 캐비닛 및 목공 가공업체로부터 패널 가공 및 마감 시스템에 대한 안정적인 수주가 이어지고 있음을 보여줍니다. 유럽은 2024년과 2025년의 감소세를 겪은 후 안정화되고 있으며, 독일공급업체들은 생산량을 회복하기 위해 자동화 및 AI를 활용한 생산에 주력하고 있습니다. 이러한 변화는 제품 혁신과 부가가치 기능 강화로 이어지고 있습니다. 중국 제조업체들은 수익성이 낮은 부문의 생산 능력을 축소하고, 단위당 에너지 소비량과 인력을 줄이는 설비 현대화를 우선시하고 있으며, 이로 인해 고효율 생산 라인과 최신 제어 소프트웨어에 대한 수요가 뒷받침되고 있습니다.

베트남, 태국, 인도네시아를 포함한 동남아시아 거점들은 수출 분야에서 명성을 지속적으로 높여가고 있으며, 이에 따라 품질 관리, 서류 작성 및 일관된 마감에 대한 기대가 높아지고 있습니다. 남미의 성장세는 도입 규모가 작은 반면, 원자재의 강점과 도시 지역의 성장이 맞물려 신규 공장 건설을 뒷받침하고 있음을 반영하고 있습니다. 중동 및 아프리카에서는 인테리어 시공업체나 건축자재 제조업체를 중심으로 한 프로젝트 주도형 수요가 산발적으로 나타나고 있으나, 숙련된 인력 확보 문제와 수입 관세가 지속적인 수요 사이클을 저해하고 있습니다. 모든 지역에서 2026년 말에 시행될 산림 파괴 규제 하에, EU 수출 제품의 규정 준수 요건이 더욱 강화될 전망이며, 이에 따라 원자재의 원산지를 증명하고 로트의 완전성을 확보하는 시스템에 대한 수요가 높아질 것입니다. 이러한 상황이 변화하는 가운데, 목공 기계 시장에서는 강력한 서비스 네트워크와 시차를 극복하여 공장의 가동을 유지하는 원격 진단 기능을 갖춘 공급업체가 계속해서 우위를 점할 것입니다. 지역별 선호도는 제품 구성, 건축 기준, 인력 확보, 조달 경로의 차이를 반영하며, 이러한 요인들이 기계 선정 및 자동화 수준에 영향을 미칠 것으로 보입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the woodworking machinery market size is projected to expand from USD 5.25 billion in 2025 and USD 5.49 billion in 2026 to USD 6.94 billion by 2031, registering a CAGR of 4.78% between 2026 to 2031.

This report is Segmented by Product Type (CNC Routers, Panel Saws, and More), by Operating Principle (Conventional/Manual, Semi-Automatic, and Fully Automatic CNC), by End-User Industry (Furniture, Construction, Flooring, Cabinetry, and Other), and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Woodworking Machinery Market Trends and Insights

Booming Global Furniture Manufacturing Industry

Demand for furniture and interior products is reinforcing investment in CNC routers, edgebanders, and finishing lines that shorten setup time and minimize waste in variable-batch production. In the United States, residential construction momentum in early 2026 reinforces order pipelines for cabinetry, millwork, and interior fittings that depend on precision woodworking equipment and nesting-based panel processing. Chinese producers are consolidating around higher-value engineered products and export channels, encouraging upgrades to more precise machining centers to reduce scrap and improve finish quality. German machine builders stabilized after a 2024 production decline and are leaning into automation and software-driven control to serve flexible manufacturing requirements, which supports refresh cycles across medium and large plants. Together, these dynamics sustain demand for CNC-enabled production cells and integrated software that translate product configurations into tool paths without manual programming. As the woodworking machinery market evolves toward engineered wood, short-run customization, and digital traceability, suppliers with robust control systems and after-sales support networks are positioned to capture premium projects.

Growth in Modular and Customized Furniture Demand

Customer expectations for modular, made-to-fit cabinets and furniture continue to pull the woodworking machinery market toward flexible nesting, high-precision edge processing, and software-connected workflows that execute one-off jobs efficiently. Suppliers are displaying integrated machining cells and connected platforms that link order intake to production planning and predictive maintenance, which helps mid-market shops manage more customization with fewer unplanned stops. Modular architecture has a lower risk because manufacturers can add automation steps, smarter spindles, or faster material handling as order complexity rises rather than committing to a single, fixed configuration on day one. Compliance expectations also matter because the European Union Deforestation Regulation will require stronger digital traceability for wood products placed on the EU market at the end of 2026, which favors software-integrated shops that can automate documentation and batch segregation. Prepared manufacturers use these capabilities to quote fast, plan work by batch size, and transition jobs without lengthy downtime. The woodworking machinery market is aligning around this need for configurable throughput, with value tilted toward control systems, tool management, and service ecosystems that keep small lots moving at scale.

High Capital Investment Requirements for Advanced Machinery

Advanced CNC equipment requires meaningful upfront commitments, which slows adoption among small and mid-sized enterprises that face higher borrowing costs and tighter cash cycles. Shops balance the benefits of five-axis capability and robotic handling against the total cost of ownership, that include installation, tooling, software, dust collection, and operator training. Many buyers phase automation over time by starting with semi-automatic steps and then adding loaders, scanners, or faster drives as utilization rises, which spreads the investment across multiple years. Refurbished equipment provides a lower entry point but may require more maintenance and lack the newest control systems that support connected dashboards or traceability out of the box. Vendors that offer financing tied to service and training can help de-risk adoption for smaller buyers who need predictable monthly costs. These realities shape the pace of upgrades in the woodworking machinery market, especially outside major manufacturing corridors where technical support and parts logistics can be harder to secure.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Residential and Commercial Construction Activity

- Labor Cost Pressures and Productivity Enhancement Needs

- Raw Material Price Volatility and Timber Supply Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CNC routers held 36.1% share in 2025 and are projected to grow at a 5.8% CAGR through 2031 as buyers seek configurable systems that handle complex geometries and frequent changeovers. The segment's strength rests on nesting workflows that raise panel yield and automated tool management that reduces downtime between short runs. Panel saws remain common for standardized cutting because they are simpler and less expensive, although the shift toward digital control is persistent across higher-mix shops. Edgebanders, surface planers, and wide-belt sanders move in tandem with expectations for cleaner edges, tighter thickness tolerances, and uniform finishes on both custom and volume projects. Other machines like drills, tenoners, moulders, band saws, lathes, and mortisers keep specialized roles where joinery or turning are central to design or structural needs. The woodworking machinery market favors routers where work mixes are more variable, since software-integrated routing can compress lead times without major labor additions. Router vendors are also bundling nesting software and training to speed time to value in new installs. As a result, the woodworking machinery market size associated with CNC routers is set to expand in line with small-batch customization and software-centric workflows that prioritize speed and material efficiency.

The rest of the product landscape is bifurcating between single-purpose lines designed for throughput and flexible platforms tuned for changeovers. High-mix operations adopt routers that justify their price with labor savings and the ability to run unique jobs efficiently, while mass producers of standardized units still invest in dedicated lines optimized for volume. Replacement cycles are aligned to productivity gains because buyers weigh energy use, spindle speed, and control interface improvements in addition to mechanical precision. Emerging capabilities like connected consoles and predictive maintenance sit alongside faster drives, better vacuum systems, and higher-torque spindles that stabilize cuts on harder materials. The woodworking machinery market continues to cross-pollinate innovations across product categories because finish quality and tolerance expectations are rising on both custom and standard jobs. Over time, multifunctional systems that combine engraving, drilling, and profiling will further consolidate decisions around integrated platforms. This is driving the woodworking machinery industry to focus on end-to-end workflows and interoperability across routers, edgebanders, and finishing equipment.

Geography Analysis

Asia-Pacific accounted for 40.8% of global demand in 2025, anchored by China's panel capacity, India's expanding exports, and Southeast Asian contract manufacturing. South America shows the fastest trajectory at a 6.7% CAGR to 2031 as Brazil's engineered-wood base scales and currency dynamics support foreign investment. North America represents a mature installed base focused on replacement, debottlenecking, and higher automation as labor remains tight. The United States recorded 1.487 million housing starts in January 2026, which underscores steady orders from cabinet and millwork shops for panel processing and finishing systems. Europe is stabilizing after declines in 2024 and 2025, and German suppliers are leaning into automation and AI-assisted production to regain output, a shift that reinforces product innovation and value-added features. China's producers are trimming capacity in lower-margin segments and prioritizing upgrades that cut energy use and labor per unit, which supports demand for efficient lines and modern control software.

Southeast Asian hubs, including Vietnam, Thailand, and Indonesia, continue to build export reputations, and that raises expectations on quality control, documentation, and consistent finish. South America's momentum reflects a smaller installed base paired with raw-material strengths and urban growth that together support new plant builds. The Middle East and Africa show sporadic project-led demand from fit-out contractors and joinery firms, though skill availability and import duties temper sustained cycles. In all regions, compliance for EU-bound products is set to become more stringent under the deforestation regulation at the end of 2026, which will boost demand for systems that document material origin and ensure batch integrity. As these conditions evolve, the woodworking machinery market will continue to reward suppliers with strong service networks and remote diagnostics that keep plants running across time zones. Regional preferences will reflect differences in product mix, building codes, labor availability, and sourcing, which will influence machine choice and automation depth.

- HOMAG Group

- SCM Group

- Biesse Group

- Michael Weinig AG

- Felder Group

- Holz-Her

- Paolino Bacci

- IMA Schelling Group

- Timesavers

- Leadermac (Cantek)

- Anderson Group

- Grizzly Industrial

- Laguna Tools

- SawStop

- Festool

- Powermatic (JPW)

- JET (JPW)

- Makita Corp.

- Nanxing Machinery

- Shandong Baide

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming Global Furniture Manufacturing Industry

- 4.2.2 Growth in Modular and Customized Furniture Demand

- 4.2.3 Expansion of Residential and Commercial Construction Activity

- 4.2.4 Rising Popularity of Engineered Wood Products

- 4.2.5 Labor Cost Pressures and Productivity Enhancement Needs

- 4.2.6 Growing Wood-based Interior Design and Flooring Trends

- 4.3 Market Restraints

- 4.3.1 High Capital Investment Requirements for Advanced Machinery

- 4.3.2 Raw Material Price Volatility and Timber Supply Constraints

- 4.3.3 Shortage of Skilled Operators and Machine Programmers

- 4.3.4 Environmental Concerns and Sustainable Forestry Pressures

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Computer-controlled (CNC) evolution

- 4.8 Automation & Collaborative Robots

- 4.9 Additive & hybrid wood-metal processing

- 4.10 Industry Attractiveness - Porter?s Five Forces

- 4.10.1 Threat of New Entrants

- 4.10.2 Bargaining Power of Suppliers

- 4.10.3 Bargaining Power of Buyers

- 4.10.4 Threat of Substitutes

- 4.10.5 Industry Rivalry

5 Market Size & Growth Forecasts (Values, In USD)

- 5.1 By Product Type

- 5.1.1 CNC Routers

- 5.1.2 Panel Saws

- 5.1.3 Edgebanders

- 5.1.4 Surface Planers

- 5.1.5 Wide-belt Sanders

- 5.1.6 Other Machines (Drills, Tenoners, Milling Machines, Band Saws, Wood Lathes, Mortisers)

- 5.2 By Operating Principle

- 5.2.1 Conventional / Manual

- 5.2.2 Semi-Automatic

- 5.2.3 Fully Automatic CNC

- 5.3 By End-user Industry

- 5.3.1 Furniture Manufacturing

- 5.3.2 Construction & Millwork

- 5.3.3 Flooring

- 5.3.4 Cabinetry

- 5.3.5 Other Industrial Users (Plywood and Panel Manufacturing, Ship Building, Etc.)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Peru

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Kuwait

- 5.4.5.5 Turkey

- 5.4.5.6 Egypt

- 5.4.5.7 South Africa

- 5.4.5.8 Nigeria

- 5.4.5.9 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 HOMAG Group

- 6.4.2 SCM Group

- 6.4.3 Biesse Group

- 6.4.4 Michael Weinig AG

- 6.4.5 Felder Group

- 6.4.6 Holz-Her

- 6.4.7 Paolino Bacci

- 6.4.8 IMA Schelling Group

- 6.4.9 Timesavers

- 6.4.10 Leadermac (Cantek)

- 6.4.11 Anderson Group

- 6.4.12 Grizzly Industrial

- 6.4.13 Laguna Tools

- 6.4.14 SawStop

- 6.4.15 Festool

- 6.4.16 Powermatic (JPW)

- 6.4.17 JET (JPW)

- 6.4.18 Makita Corp.

- 6.4.19 Nanxing Machinery

- 6.4.20 Shandong Baide

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment