|

시장보고서

상품코드

2062067

재생 고무 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Reclaimed Rubber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

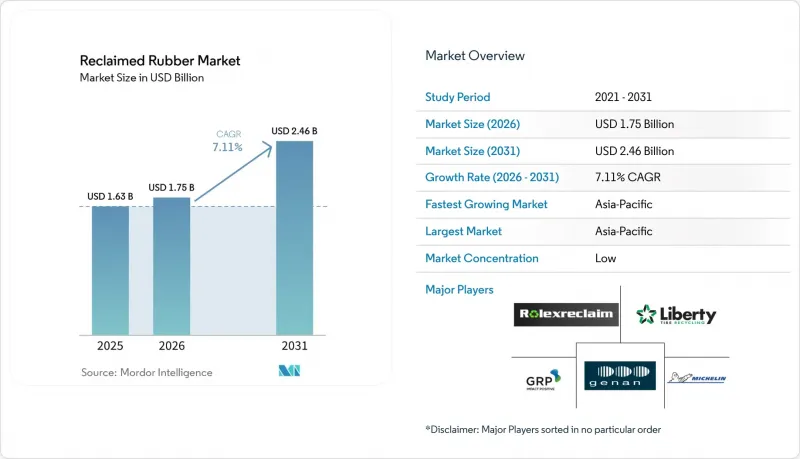

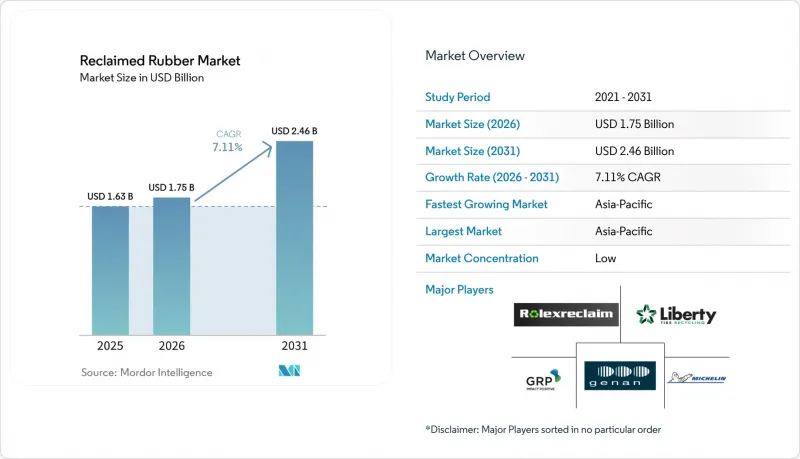

Mordor Intelligence에 의하면, 재생 고무 시장 규모는 2025년 16억 3,000만 달러, 2026년 17억 5,000만 달러에서 2031년까지 24억 6,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 7.11%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형(전체 타이어 재생(WTR), 부틸 재생 등), 공정(기계적 공정 및 화학적/탈황 공정), 용도(자동차·항공기 타이어, 고무 매트·바닥재 등), 최종 사용자 산업(자동차 및 운송, 건축 및 건설 등), 지역(아시아태평양, 북미, 유럽, 남미 등)에 따라 분류되어 있습니다.

세계 재생 고무 시장 동향 및 분석

버진 고무에 비해 비용 효율이 뛰어난 지속 가능한 대체재

2024년부터 2025년까지 재생 고무는 천연 고무 및 합성 엘라스토머보다 30-50% 저렴한 가격으로 책정되어, 비용 면에서 큰 우위를 보였습니다. 천연고무 가격이 톤당 1,800-2,100달러 선에서 형성되는 가운데, 타이어 전체를 재활용한 재생고무는 더 저렴한 800-1,200달러에 구입할 수 있었습니다. 이러한 구조적인 가격 차이가 발생하는 이유는 재생 고무가 농업 리스크 프리미엄과 석유화학 원료에 따른 가격 변동 모두를 피할 수 있기 때문입니다. 자동차 업계의 2차 공급업체들은 ISO 9001 품질 기준을 준수하면서, 바닥 매트, 머드플랩, 댐퍼 등의 제품에 20-40%의 재생 고무를 혼합하기 시작했습니다. 주목할 만한 움직임으로, 도요타 고세이는 2025년 12월, 토요타 RAV4에 재생 소재를 20% 배합한 웨더스트립을 도입했으며, 이 소재의 성능이 입증되었음을 강조했습니다. 건설 업계에서는 REGUPOL사가 연간 1억 1,500만 파운드의 폐고무를 처리함으로써 주목을 받고 있습니다. 이 회사의 노력 덕분에, ASTM D5603 충격 기준을 충족하는 바닥재에서 버진 EPDM을 사용할 때와 비교해 재료 비용을 40% 절감하는 데 성공했습니다. 게다가 EU 배출권 거래제가 폐기물 소각까지 대상 범위를 확대함에 따라, 탄소 가격 제도에서 재생 자재가 점점 더 우대받고 있습니다. 이는 주로 환경적인 이점 때문입니다. 매립지로 보내지는 타이어를 단 1톤만 줄여도, 약 2.5톤의 이산화탄소 환산 배출량을 줄일 수 있기 때문입니다.

전 세계 폐타이어 규제가 재활용 의무화를 가속화하고 있습니다.

2024년부터 2025년까지, 구속력 있는 법규에 따라 기업의 자발적인 노력이 강제력 있는 의무로 전환되었습니다. EU 폐기물 운송 규정 2024/1157은 회원국들에게 에너지 회수보다는 물질 재활용에 중점을 둘 것을 요구하고 있습니다. 2025년 1월에 시행된 아일랜드의 확대 생산자 책임(EPR) 프로그램은 타이어 제조업체에 대해 회수 비용 부담과 2027년까지 90%의 회수 목표 달성을 의무화하고 있습니다. 중국에서는 인증된 재활용 업체가 부가가치세의 70%를 환급받을 수 있으며, 비중요 타이어 컴파운드에 재생 재료를 사용하는 것이 의무화되어 있습니다. 이러한 규제 추진에 힘입어, 2024년 12월에 가동을 시작한 이창헝다리(Yichang Hengdali)의 연간 10만 톤 규모 플랜트 등의 시설이 설립되었습니다. 캘리포니아주의 SB 876 법안에 따르면, 주정부가 자금을 지원하는 도로용 아스팔트에 5% 이상의 크럼 고무를 혼합해야 하며, 이로 인해 기계적 재생 고무 수요가 증가하고 있습니다. ISO 14001 및 ISCC PLUS 인증을 취득한 가공업체는 우선 공급업체 지위를 획득하는 반면, 기준을 충족하지 못하는 업체는 거래에서 제외될 수 있습니다.

원료 품질의 편차가 컴파운드의 균일성을 저해합니다.

폴리머 함량 편차, 스틸 벨트, 도로 유래 오염 물질을 포함하는 폐타이어는 반입 시 엄격한 검사를 받습니다. 반입되는 자재의 최대 15%는 금속이나 화학 물질 잔류물이 과다하여 등급이 하향 조정되거나 완전히 반입이 거부됩니다. 이러한 편차를 해결하기 위해 다운스트림 공정 업체인 컴파운더는 추가적인 안정제를 사용할 수밖에 없으며, 이로 인해 비용이 5-8% 더 증가하여 재활용의 경제적 이점이 훼손되고 있습니다. 포드의 FLTM BN 108-01 규격을 준수하는 자동차 OEM 업체들은 인장 강도가 10MPa를 초과하고 연신율이 300%를 초과할 것을 의무화하고 있습니다. 이 규정에 따라, 제조업체가 고순도 원료 공급을 보장할 수 없는 한, 재생재의 배합 비율은 30% 이하로 제한됩니다. 2022년, 중국의 타이어 회수율은 52.73%에 그쳐 세계 평균보다 낮았습니다. 이러한 부족 현상은 품질 리스크를 증대시키는 비공식 회수 네트워크가 초래하는 문제를 여실히 드러내고 있습니다. 근적외선 선별 기술에 대한 투자는 이러한 불균일성을 완화할 가능성을 지니고 있지만, 라인당 최대 50만 달러의 설비 투자가 필요한 등 비용이 매우 높습니다.

부문별 분석

2025년, 전체 타이어 재생(WTR)은 재생 고무 시장의 47.12%를 차지했습니다. 예측에 따르면, 2031년까지 연평균 성장률(CAGR) 7.69%로 꾸준한 성장이 예상됩니다. 이러한 성장은 연간 10킬로톤의 처리 능력에 비해 200만-500만 달러라는 비교적 적은 설비 투자로 충분한 기계적 분쇄 공정에 의해 뒷받침되고 있습니다. WTR의 다양한 폴리머 블렌드는 진동 댐퍼, 머드플랩, 바닥 매트 등에 사용되고 있습니다. 이러한 용도는 2차 공급업체가 ISO 9001 규격 준수를 유지하면서 OEM이 요구하는 비용 절감을 실현하는 데 도움이 되고 있습니다.

부틸 및 EPDM 재생재에 대한 수요가 증가하고 있습니다. 이는 탄소 배출 감축 의무화로 인해 지붕용 시트나 자동차용 웨더 씰의 경우, 순수 원료만을 사용하는 사양에서 점차 전환되고 있기 때문입니다. WTR보다 15-20% 비싼 EPDM 재생 소재는 단층 지붕재에 필요한 오존 노화 요건을 충족하기 위해 탈황 공정을 채택하고 있습니다. High-Tech Reclaim사와 Swani Rubber사는 이러한 특수 등급 제품을 산업용 컴파운더에 공급하고 있습니다. 마이크로파법 및 기계화학적 공법이 지속적으로 개선됨에 따라, 버진 폴리머와의 성능 격차는 줄어들고 있으며, 이로 인해 잠재적인 최종 시장의 범위가 확대되고 있습니다.

2025년에는 혼합 원료의 처리 능력과 0.8-1.2 kWh/kg의 에너지 소비량 덕분에 기계적 분쇄 방식이 시장 점유율의 72.11%를 차지했습니다. 2025년 12월, Liberty Tire사는 단계적 성장 전략의 일환으로 140만 달러를 투자해 노스캐롤라이나주 시설을 확장하고, 연간 생산 능력을 3.3킬로톤 증대했습니다.

화학적 탈황 부문은 프리미엄 타이어에 사용되는 고순도 원료에 대한 OEM 수요에 힘입어 연평균 성장률(CAGR) 7.77%로 성장할 것으로 전망됩니다. 이 부문의 마이크로파 장치는 인장 강도의 최대 90%를 유지하면서 1.2-1.8 kWh/kg의 에너지를 소비합니다. 허난성에 위치한 샹청산산의 연산 5만 톤 규모의 공장은 재생 기술 발전에 주력하는 중국의 태도를 반영하고 있습니다. 이 부문의 설비는 현재 3년 미만의 투자 회수 기간을 달성하고 있으며, 고급 용도로 사용되는 재생 고무는 기계용 등급에 비해 10-15%의 가격 프리미엄을 실현하고 있습니다.

지역별 분석

2025년, 아시아태평양은 전 세계 매출의 46.22%를 차지해, 2031년까지 연평균 성장률(CAGR) 7.88%로 성장할 것으로 전망됩니다. 2024년, 중국의 재생 타이어 처리량은 900만 톤에 달했으며, 인증된 처리 업체를 대상으로 새로 도입된 70% 부가가치세(VAT) 환급 조치의 지원에 힘입어 전년 대비 20% 증가를 기록했습니다. 후베이성이나 산둥성 등에서는 2024년부터 2025년까지 연간 15만 톤 이상의 처리 능력을 확대했습니다. 한편, 인도의 Swani Rubber와 태국의 Green Rubber Energy는 자동차 산업 집적지 수요에 대응하기 위해 특수 제품 및 열분해 라인을 확충하고 있습니다.

북미는 여전히 중요한 위치를 차지하고 있습니다. 12억 달러 규모의 연방 인프라 자금이 폐기물 발전 프로젝트에 배정되어, 이는 원자재 가격에 영향을 미치고 있습니다. 동시에, 캘리포니아주의 SB 876과 같은 주 차원의 규제가 클램 고무 아스팔트 시장을 뒷받침하고 있습니다. 2023년, 미국에서는 3억 개의 폐타이어 중 2억 4,000만 개가 처리되었으며, 그중 7,500만 개는 분쇄 고무로 전환되었고, 9,600만 개는 에너지로 활용되었습니다. USMCA(미국·멕시코·캐나다 협정)의 자동차 공급망을 구성하는 캐나다와 멕시코는 이 지역 수요에 15-18%를 추가로 기여하고 있습니다.

유럽의 기여도는 의무적 회수 제도와 생산자책임확대(EPR) 체제를 통해 형성되고 있습니다. 연간 40만 톤의 분쇄 능력을 갖춘 Genan사는 덴마크, 포르투갈, 독일에서 사업을 전개하며 섬유 분획의 가치 제고에 힘쓰고 있습니다. 스웨덴에서 진행 중인 미슐랭의 열분해 이니셔티브는 유럽의 타이어 제조 공장에 통합된 폐쇄형 재생 카본블랙 공급 모델로 자리 잡고 있습니다. EU의 정책은 2030년까지 재생 원료의 평균 함유율을 23% 이상으로 높이는 것을 목표로 하고 있으며, 이는 고성능 재생 고무에 대한 수요 증가를 시사합니다.

남미에서는 브라질이 제조업체에 대한 회수 의무를 시행하고 있는 반면, 아르헨티나에서는 2025년 10월, 타이어 분말을 10% 배합한 고무 개질 포장 구간이 처음으로 도입되었습니다. 중동 및 아프리카에는 성장 잠재력이 있습니다. 사우디아라비아와 남아프리카공화국 양국은 매립 금지 조치 및 친환경 공공 조달 규제의 도입을 검토하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the reclaimed rubber market size is projected to expand from USD 1.63 billion in 2025 and USD 1.75 billion in 2026 to USD 2.46 billion by 2031, registering a CAGR of 7.11% between 2026 to 2031.

This report is Segmented by Product Type (Whole Tyre Reclaim (WTR), Butyl Reclaim, and More), Process (Mechanical Process and Chemical/Devulcanization Process), Application (Automotive and Aircraft Tires, Rubber Mats and Flooring, and More), End-User Industry (Automotive and Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and More).

Global Reclaimed Rubber Market Trends and Insights

Cost-Effective Sustainable Substitute for Virgin Rubber

In 2024-2025, reclaimed rubber showcased a significant cost advantage, being priced 30-50% lower than both virgin natural and synthetic elastomers. While natural rubber prices hovered between USD 1,800-2,100 per ton, whole tire reclaim was available at a more modest USD 800-1,200. This structural price gap arises because reclaimed rubber sidesteps both agricultural risk premiums and the volatility associated with petrochemical feedstocks. Tier-2 automotive suppliers have begun integrating 20-40% reclaimed content into products like floor mats, mud flaps, and dampers, all while adhering to ISO 9001 quality standards. In a notable move, Toyoda Gosei introduced weather-stripping featuring 20% recycled content for the Toyota RAV4 in December 2025, underscoring the material's validated performance. Over in the construction sector, REGUPOL is making waves by processing 115 million pounds of scrap rubber each year. Their efforts have led to a 40% reduction in material costs for flooring that meets ASTM D5603 impact standards, compared to using virgin EPDM. Additionally, with the EU Emissions Trading System expanding to cover waste incineration, carbon-pricing schemes are increasingly favoring reclaimed materials. This is largely due to the environmental benefit: diverting just 1 ton of tires from landfills can prevent the release of approximately 2.5 tons of CO2-equivalent emissions.

Global Waste-Tire Regulations Accelerating Recycling Mandates

In 2024-2025, binding legislation converted voluntary corporate initiatives into enforceable mandates. The EU Waste Shipment Regulation 2024/1157 requires member states to focus on material recycling instead of energy recovery. Ireland's Extended Producer Responsibility (EPR) program, implemented in January 2025, obligates tire producers to fund collections and achieve a 90% recovery target by 2027. In China, certified recyclers receive a 70% VAT rebate and must use recycled content in non-critical tire compounds. This regulatory push has driven the establishment of facilities such as Yichang Hengdali's 100 kiloton per annum plant, which began operations in December 2024. California's SB 876 law requires a 5% crumb-rubber minimum in state-funded road asphalt, increasing demand for mechanical reclaim. Processors with ISO 14001 and ISCC PLUS certifications gain preferred-supplier status, while non-compliant operators face potential exclusion.

Variability in Feedstock Quality Disrupting Compound Consistency

End-of-life tires, laden with mixed polymer ratios, steel belts, and road contaminants, face scrutiny upon arrival. Up to 15% of this incoming material gets downgraded or outright rejected due to excessive metal or chemical residues. To counteract this variability, downstream compounders resort to extra stabilizers, which inflate costs by an additional 5-8% and erode the economic advantage of reclamation. Automotive OEMs, adhering to Ford's FLTM BN 108-01 standard, mandate a tensile strength exceeding 10 MPa and an elongation surpassing 300%. This stipulation restricts reclaim loadings to below 30% unless manufacturers can guarantee high-purity streams. In 2022, China's tire-recovery rate stood at 52.73%, lagging behind the global average. This shortfall underscores the challenges posed by informal collection networks, which amplify quality risks. While investments in near-infrared sorting promise to mitigate this heterogeneity, they come at a steep price, demanding up to USD 0.5 million in capital per line.

Other drivers and restraints analyzed in the detailed report include:

- OEM Recycled-Content Targets for Premium Tire Lines

- Rapid Devulcanization Technology Scale-Up Slashing Energy Use

- Odor and VOC Compliance Limits for Consumer-Facing Goods

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Whole Tire Reclaim (WTR) accounted for 47.12% of the reclaimed rubber market. Projections indicate steady growth, with an expected CAGR of 7.69% through 2031. This growth is supported by the mechanical grinding process, which requires a relatively low capital investment of USD 2-5 million for a capacity of 10 kilotons per year. WTR's diverse polymer blend is utilized in vibration dampers, mud flaps, and floor mats. These applications help Tier-2 suppliers achieve cost reductions required by OEMs while maintaining compliance with ISO 9001 standards.

The demand for butyl and EPDM reclaims is increasing, driven by their use in roofing membranes and automotive weather-seals, which are shifting away from virgin-only material specifications due to carbon-reduction mandates. EPDM reclaim, priced 15-20% higher than WTR, uses devulcanization processes to meet the ozone-aging requirements necessary for single-ply roofing. High-Tech Reclaim and Swani Rubber supply these specialty grades to industrial compounders. As microwave and mechanochemical methods continue to improve, they are narrowing the performance gap with virgin polymers, which is expanding the range of potential end markets.

In 2025, mechanical grinding accounted for 72.11% of the market share due to its capability to process mixed feedstock and its energy requirement of 0.8-1.2 kWh/kg. In December 2025, Liberty Tire expanded its North Carolina facility with a USD 1.4 million investment, increasing capacity by 3.3 kilotons per year as part of its incremental growth strategy.

The chemical devulcanization segment is projected to grow at a CAGR of 7.77%, supported by the demand from OEMs for higher-purity feedstock used in premium tires. Microwave units in this segment consume 1.2-1.8 kWh/kg of energy while retaining up to 90% of tensile strength. Xiangcheng Sanshan's 50 kilotons per year plant in Henan reflects China's focus on advancing reclaim technology. Equipment in this segment now offers payback periods of less than three years, and reclaimed rubber used in premium applications achieves a 10-15% price premium compared to mechanical grades.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.22% of global revenue, projections indicate a growth rate of 7.88% CAGR extending to 2031. In 2024, China's recycled-tire volume reached 9 million tons, marking a 20% year-on-year increase, supported by a newly introduced 70% VAT rebate for certified processors. Provinces such as Hubei and Shandong expanded their capacities by over 150 kilotons annually during 2024-2025. Meanwhile, India's Swani Rubber and Thailand's Green Rubber Energy are increasing specialty and pyrolysis lines to address demand in automotive corridors.

North America maintains a significant position. Federal infrastructure funding of USD 1.2 billion is allocated to waste-to-energy projects, influencing feedstock pricing. At the same time, state regulations, such as California's SB 876, support the market for crumb-rubber asphalt. In 2023, the U.S. processed 240 million out of 300 million scrap tires, converting 75 million to ground rubber and utilizing 96 million for energy. Canada and Mexico, both part of the USMCA automotive chain, contribute an additional 15-18% to the regional demand.

Europe's contributions are shaped by mandatory take-back and Extended Producer Responsibility (EPR) frameworks. Genan, with a grinding capacity of 400 kilotons per year, operates across Denmark, Portugal, and Germany, and is advancing textile-fraction valorization. Michelin's pyrolysis initiative in Sweden serves as a model for a closed-loop recovered carbon black supply, integrated into European tire manufacturing plants. EU policies aim to increase the average recycled raw material content beyond 23% by 2030, indicating a rise in demand for high-spec reclaim.

In South America, Brazil enforces manufacturer take-back, while Argentina introduced its first rubber-modified highway section, incorporating 10% tire powder, in October 2025. The Middle East and Africa, present potential for growth. Both Saudi Arabia and South Africa are considering the implementation of landfill bans and green public procurement regulations.

- Balaji Rubber Industries (P) Ltd.

- ELGI Rubber

- Entech Inc.

- GENAN HOLDING A/S

- Green Rubber Global Ltd

- GRP LTD.

- High Tech Reclaim Pvt. Ltd.

- HUXAR

- Michelin

- Mitsubishi Chemical Group Corporation

- Liberty Tire Recycling

- Pirelli & CSpA

- Rolex Reclaim Pvt. Ltd.

- Star Polymer Inc

- Sun Exims Pvt. Ltd.

- Swani Rubber Industry

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cost-effective sustainable substitute for virgin rubber

- 4.2.2 Global waste-tire regulations accelerating recycling mandates

- 4.2.3 OEM recycled-content targets for premium tire lines (post-2026)

- 4.2.4 Rapid devulcanization technology scale-up slashing energy use

- 4.2.5 Surge in Renewable-Fuel Co-Processing Driving End-of-Life Tyre Feedstock Demand

- 4.3 Market Restraints

- 4.3.1 Variability in feedstock quality disrupting compound consistency

- 4.3.2 Odour and VOC compliance limits for consumer-facing goods

- 4.3.3 Competition from bio-based elastomers in high-performance uses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Whole Tire Reclaim (WTR)

- 5.1.2 Butyl Reclaim

- 5.1.3 Ethylene Propylene Diene Monomer (EPDM) Reclaim

- 5.1.4 Other Product Types (Natural Rubber Reclaim, Latex Reclaim, etc.)

- 5.2 By Process

- 5.2.1 Mechanical Process

- 5.2.2 Chemical/Devulcanisation Process

- 5.3 By Application

- 5.3.1 Automotive and Aircraft Tires

- 5.3.2 Rubber Mats and Flooring

- 5.3.3 Molded Industrial Goods

- 5.3.4 Rubber Compounds and Masterbatch

- 5.3.5 Other Applications (Footwear, etc.)

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation

- 5.4.2 Building and Construction

- 5.4.3 Consumer Goods

- 5.4.4 Industrial Manufacturing

- 5.4.5 Other End-user Industries (Energy and Utilities, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Balaji Rubber Industries (P) Ltd.

- 6.4.2 ELGI Rubber

- 6.4.3 Entech Inc.

- 6.4.4 GENAN HOLDING A/S

- 6.4.5 Green Rubber Global Ltd

- 6.4.6 GRP LTD.

- 6.4.7 High Tech Reclaim Pvt. Ltd.

- 6.4.8 HUXAR

- 6.4.9 Michelin

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 Liberty Tire Recycling

- 6.4.12 Pirelli & CSpA

- 6.4.13 Rolex Reclaim Pvt. Ltd.

- 6.4.14 Star Polymer Inc

- 6.4.15 Sun Exims Pvt. Ltd.

- 6.4.16 Swani Rubber Industry

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment