|

시장보고서

상품코드

2062070

폴리프로필렌 부직포 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Polypropylene Non-woven Fabric - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

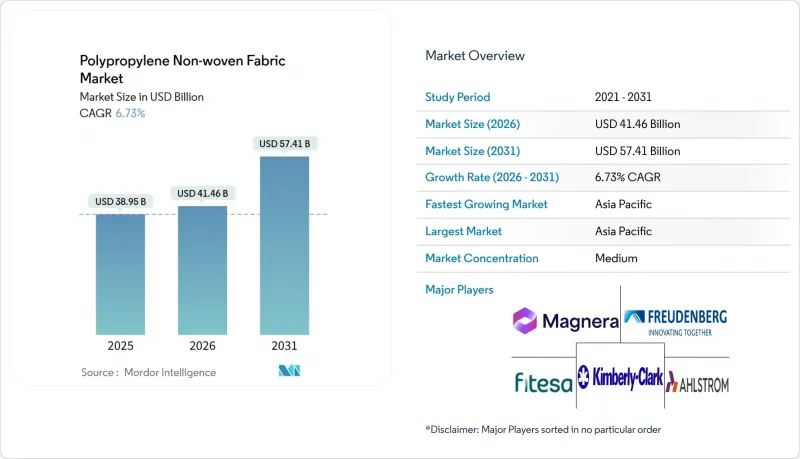

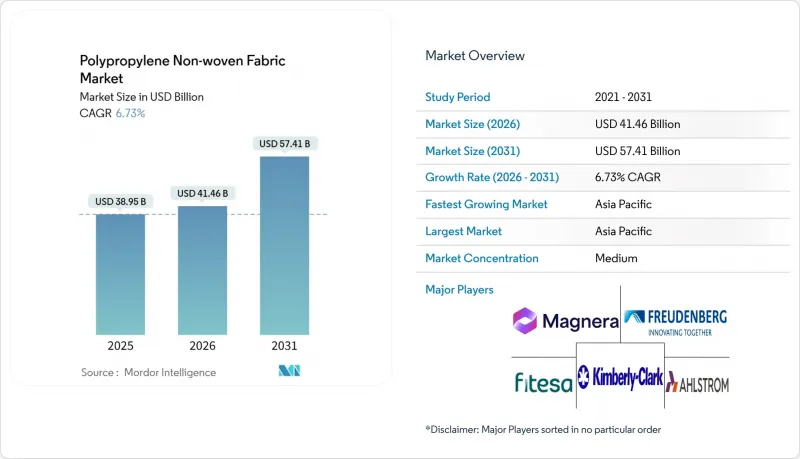

Mordor Intelligence에 의하면, 폴리프로필렌 부직포 시장 규모는 2025년 389억 5,000만 달러에서 2026년에는 414억 6,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 6.73%로 성장을 지속하여, 2031년까지 574억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제조 기술(스펀본드, 멜트블로우, SMS(스펀-멜트-스펀) 등), 용도(위생, 의료, 포장, 자동차, 여과, 기타 용도), 원료 유형(호모폴리머 및 코폴리머), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 폴리프로필렌 부직포 시장 동향 및 분석

위생 및 의료용 일회용 제품 수요 증가

신흥 경제국에서 기저귀, 여성 위생용품, 요실금용 제품이 보급되고, 병원 시스템에서 일회용 감염 관리 프로토콜이 정착됨에 따라 위생 및 의료용 일회용 제품의 판매량 증가세가 지속되고 있습니다. 폴리프로필렌 스펀본드 상부 시트는 약 1,868 mm/s의 통기성을 지닌 소수성 표면을 제공하여, 셀룰로오스계 대체재에 비해 액체의 침투 시간을 단축합니다. 2025년에 발표된 킴벌리-클라크사의 미국 내 여러 거점에서의 생산 계획은 브랜드 소유주들의 신뢰를 뒷받침하는 것이며, 국내 롤 원지 조달을 늘리고 있습니다. SMS 및 SMMS 복합 소재가 AAMI의 더 높은 보호 등급을 충족하고, 타이벡(Tyvek) 소재 멸균 포장재의 생산 능력 확대가 일회용 의료기기의 급증에 힘입으면서, 의료 분야 수요가 위생 분야 수요를 비율 기준으로 앞지르고 있습니다. 업계 리뷰에서는 가운의 차단 기준과 실제 환경에서의 병원체 지속성 사이에 차이가 있다는 점이 지적되면서, 검증된 항균성 폴리프로필렌 기판에 대한 관심이 높아지고 있습니다. 이러한 추세들이 맞물려 폴리프로필렌 부직포 시장의 기초 소비량을 끌어올리고 있습니다.

포장 업계에서의 용도 확대

각 브랜드 소유 기업들은 유럽의 2030년 재활용 목표를 준수하기 위해 단일 소재 구조로의 전환을 추진하고 있으며, 이에 따라 연포장재의 사양은 고순도의 단일 생산 거점에서 제조된 폴리프로필렌 부직포로 변화하고 있습니다. 보레알리스(Borealis)가 2026년에 계획하고 있는 ‘Borstar Nextension’ 등급의 생산 확대는 이러한 규정 준수 중심 수요에 부응하기 위한 것으로, 식품 접촉용 및 헬스케어용 파우치용으로 밀봉성과 기계적 재활용성을 향상시킨 제품을 제공할 예정입니다. 물류 분야에서는 통기성이 있는 스펀본드 백이 폴리에틸렌 필름의 대체재로 채택되고 있습니다. 이는 운송 중 발생하는 결로로 인한 손상을 줄이면서도, 브랜딩을 위한 인쇄 적합성을 유지할 수 있기 때문입니다. 포장 규제에 포함된 재사용 및 빈 공간 제한은 일부 일회용 제품 수요를 감소시킬 가능성이 있지만, 동시에 재사용 기준을 충족하는 내구성이 뛰어난 부직포 가방 시스템에 대한 수요 창출로 이어지고 있습니다. 식품 등급 재활용 폴리프로필렌의 단기 공급은 여전히 부족하며, 이에 따른 프리미엄 가격이 지속됨에 따라 폴리프로필렌 부직포 시장에서 버진 멜트블로운 및 스펀본드 롤 제품 간의 가격 격차가 더욱 확대되고 있습니다.

일회용 플라스틱에 대한 환경적·규제적 압력

2026년 8월에 발효되는 EU의 ‘포장 및 포장 폐기물 규정’에 따르면, 모든 포장 형태에 대해 2030년까지 최소한 C등급의 재활용 가능성, 2038년까지는 A등급 또는 B등급의 재활용 가능성을 충족해야 하며, 재생 재료 함유율 목표치는 해마다 상향 조정됩니다. 확대 생산자 책임 제도에 따른 수수료는 재활용이 어려운 복합 소재에 부과되며, 저중량 범용 스펀본드 소재 쇼핑백이나 일회용 식기에 직접적인 영향을 미칩니다. 2025년 9월에 발표된 또 다른 EU 초안에서는 연간 1,500톤 이상의 펠릿을 취급하는 시설에 대해 위험 완화 계획의 인증을 의무화하고 있으며, 위반 시 EU 내 매출액의 최대 3%에 해당하는 벌금이 부과될 수 있습니다. 북미의 각 주에서도 이와 유사한 비닐봉지 사용 금지 및 재생 소재 함유율에 관한 법률을 제정하며 규제를 강화하고 있습니다. 산업용, 자동차용, 지오텍스타일용 부직포는 대체로 영향을 받지 않지만, 소비자용 포장 분야의 가공업체들은 폴리프로필렌 부직포 시장에서 입지를 유지하기 위해 재활용 고려 설계(Design for Recycling) 노력을 가속화해야 합니다.

부문별 분석

스펀본드는 기저귀, 가방, 지오텍스타일에 적합한 고속 생산과 낮은 단가 덕분에 2025년 기준 폴리프로필렌 부직포 시장 점유율 55%를 유지했습니다. 스펀본드 등급 폴리프로필렌 부직포 시장 규모는 기준 연도에 210억 달러를 넘어섰으나, 시장 포화가 진행됨에 따라 그 예측 연평균 성장률(CAGR)은 틈새 기술에 뒤처지고 있습니다. 멜트블로우 시장은 연평균 6.87%의 성장이 예상되며, 직경 3μm 미만의 섬유가 필요한 N95 마스크, HVAC(공조 설비) 및 배터리 전극 분리막에 대한 규제 강화가 성장의 견인차 역할을 하고 있습니다. 복합 SMS 및 SMMS 구조는 스펀본드의 강도와 멜트블로우의 여과 성능을 결합하여, 병원용 가운 및 산업용 여과 분야 수요를 확보하고 있습니다. 북미, 튀르키예, 중국에서의 Reicofil 5 및 동급 생산 라인에 대한 투자는 자본 배분의 전환을 보여줍니다. 열풍 접착과 캘린더 접착을 번갈아 수행하는 하이브리드 라인은 평량 범위를 10-200 g/m²로 확대하여, 자동차 및 지붕재 시장 진출을 가능하게 하고 있습니다.

정책의 추진력이 기술적 동력을 더욱 강화하고 있습니다. 미국 에너지부의 HVAC 로드맵은 2035년까지 상업용 건물의 에너지 소비량을 50% 감축하는 것을 목표로 하고 있으며, 이는 고효율 멜트블로운 필터에 대한 수요를 촉진하고 있습니다. 한편, 중국의 2026년 실내 공기질 기준에서는 PM2.5를 35μg/m³로 제한하고 있어, 차량용 및 주택용 필터 수요를 촉진하고 있습니다. 2020년부터 2021년까지 공급 부족은 국내 멜트블로운 생산 능력의 필요성을 부각시켰으며, 인도, 인도네시아, 브라질 정부의 인센티브 조치를 정당화하는 요인이 되었습니다. 설비 공급업체들은 수주 파이프라인이 2028년까지 이어지고 있다고 보고하고 있으며, 이는 폴리프로필렌 부직포 시장의 견조한 수주 잔고를 뒷받침하고 있습니다.

지역별 분석

아시아태평양은 2025년에 전 세계 수요의 42.67%를 차지해, 중국과 인도가 3,500만 톤을 초과하는 폴리프로필렌 일괄 생산 능력을 가동함에 따라 2031년까지 연평균 성장률(CAGR) 6.91%를 기록할 전망입니다. 2030년 가동을 예정하고 있는 릴라이언스사의 연산 520만 톤 규모의 잠나가르 공장은 단독으로 연간 100억제곱미터 이상의 스펀본드 부직포를 공급할 수 있어, 지역의 자급률을 높이는 수입 대체 전략을 시사하고 있습니다. 중국의 푸젠 에버선(Fujian EverSun)사의 계획 프로젝트와 인도네시아의 투반 콤플렉스(Tuban Complex) 역시 마찬가지로, 아시아 지역 내 수지 공급망을 강화하여 운송 비용과 탄소 발자국을 줄일 것입니다. 각 변환기 제조업체들은 이를 활용하여 최종 시장 인근에 라이코필(Lycofil) 및 엘리콘(Elicon)의 생산 라인을 증설함으로써 리드 타임을 단축하고, 현지 사양에 맞춘 평량 포트폴리오를 구축하고 있습니다.

북미의 폴리프로필렌 부직포 시장은 OEM 제조업체들의 생산 거점 복귀 움직임의 혜택을 받고 있습니다. 킴벌리-클라크사의 20억 달러 규모에 달하는 여러 주에 걸친 프로그램과, 아브골사의 노스캐롤라이나주 내 Reicofil 5 도입은 공급망의 회복탄력성을 강화하고 아시아산 수입품에 대한 과도한 의존도를 줄여줍니다. 2026년 4분기에 예정된 아스트롬(Arstrom)사의 일리노이주 필터 미디어 설비 현대화 사업은 급증하는 HVAC 및 전기차용 필터 수요에 대응하기 위한 것이며, 국내 원자재 확보를 위한 구조적 전환을 강조하는 것입니다. 수지 가격 상승은 여전히 역풍으로 작용하고 있지만, 국내 물류 비용 절감과 관세 회피를 통해 원자재 비용 상승이 부분적으로 상쇄되고 있습니다.

유럽에서는 주로 재활용 가능한 솔루션을 요구하는 규제의 추진으로 인해 수요가 증가하고 있습니다. 보레알리스의 2026년 부르크하우젠 투자 계획은 PPWR(플라스틱 포장 규제)의 시행 시기와 맞물려 있으며, 단일 소재 파우치 및 멸균 가능한 의료용 랩 시장을 개척할 수 있는 등급의 제품을 제공할 것입니다. 2024년 독일의 폴리프로필렌 수입량 903kt는 EU 역내 및 중동산 원료에 대한 의존도를 보여줍니다. CBAM(탄소국경조정메커니즘)의 도입으로 인해 공급처가 더욱 저탄소인 공급업체로 전환될 가능성이 있습니다. 남미, 중동 및 아프리카는 여전히 신흥 시장이며, 브라질의 작물 보호 보조금과 튀르키예의 연간 100만 톤 규모 폴리프로필렌 생산 프로젝트 2건 덕분에 작물 보호용 및 건설용 패브릭의 지역적 적용 범위가 확대되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the polypropylene non-woven fabric market size is expected to grow from USD 38.95 billion in 2025 to USD 41.46 billion in 2026 and is forecast to reach USD 57.41 billion by 2031 at 6.73% CAGR over 2026-2031.

This report is Segmented by Production Technology (Spunbond, Meltblown, SMS (Spun-Melt-Spun), and More), Application (Hygiene, Medical, Packaging, Automotive, Filtration, and Other Applications), Raw Material Type (Homopolymer and Copolymer), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Polypropylene Non-woven Fabric Market Trends and Insights

Growing Demand in Hygiene and Medical Disposables

Hygiene and medical disposables continue to underpin volume growth as diaper, feminine care, and incontinence products proliferate in emerging economies while hospital systems institutionalize single-use infection-control protocols. Polypropylene spunbond topsheets provide hydrophobic surfaces with air permeability around 1,868 mm/s, reducing fluid strike-through time versus cellulosic alternatives. Kimberly-Clark's multi-site US manufacturing program, announced in 2025, underlines brand-owner confidence and increases domestic roll-goods procurement. Medical demand is outpacing hygiene on a percentage basis as SMS and SMMS composites achieve higher AAMI protection levels and as Tyvek sterilization wrap capacity additions support the surge in single-use medical devices. Industry reviews highlight a gap between gown barrier standards and real-world pathogen persistence, accelerating interest in validated antimicrobial polypropylene substrates. Collectively, these developments raise baseline consumption in the polypropylene non-woven fabric market.

Expanding Usage in Packaging Industry

Brand owners are shifting toward monomaterial structures to comply with Europe's 2030 recyclability targets, steering flexible packaging specifications toward high-purity, single-site polypropylene nonwovens. Borealis' 2026 scale-up of Borstar Nextension grades aims to supply this compliance-driven demand, offering improved sealing and mechanical recyclability for food contact and healthcare pouches. In logistics, breathable spunbond bags replace polyethylene films because they cut condensation damage during transport while maintaining printability for branding. Reuse and void-space caps embedded in the packaging regulation could depress some single-use volumes, yet they simultaneously create openings for durable nonwoven bag systems that satisfy reuse metrics. Near-term supply of food-grade recycled polypropylene remains tight, sustaining a premium that further differentiates virgin meltblown and spunbond rolls within the polypropylene non-woven fabric market.

Environmental and Regulatory Pressure on Single-Use Plastics

The EU Packaging and Packaging Waste Regulation, effective August 2026, obliges every pack format to meet at least grade C recyclability by 2030 and grade A or B by 2038, with recycled-content quotas escalating yearly. Extended producer responsibility fees penalize hard-to-recycle composites, directly affecting low-grammage commodity spunbond shopping bags and single-use tableware. A separate EU draft issued in September 2025 requires pellet-handling sites above 1,500 tons/year to certify risk-mitigation plans and exposes violators to fines up to 3% of Union turnover. North-American states are adopting analogous bag bans and recycled-content laws, tightening the policy vice. While industrial, automotive, and geotextile nonwovens remain largely untouched, converters serving consumer packaging segments must accelerate design-for-recycling initiatives to retain market access within the polypropylene non-woven fabric market.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight, Cost-Effective Material Economics

- Increasing Utilization in Agriculture

- Polypropylene Price Volatility Linked to Crude Oil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spunbond retained 55% of the polypropylene non-woven fabric market share in 2025 owing to high-speed output and low unit costs that suit diapers, bags, and geotextiles. The polypropylene non-woven fabric market size for spunbond grades exceeded USD 21 billion in the base year, yet its forecast CAGR lags niche technologies as saturation sets in. Melt-blown, projected to grow 6.87% annually, benefits from regulatory upgrades to N95 respirators, HVAC, and battery-electrode separators that demand fibers below 3 µm diameter. Composite SMS and SMMS structures marry spunbond strength with melt-blown filtration, capturing hospital gown and industrial filtration spend. Investments in Reicofil 5 and equivalent lines across North America, Turkey, and China illustrate the capital pivot. Hybrid lines that alternate hot-air and calender bonding extend the basis-weight range to 10-200 g/m2, enabling automotive and roofing penetration.

Policy momentum compounds technical drivers. The US Department of Energy HVAC roadmap targets 50% energy reductions in commercial buildings by 2035, incentivizing high-efficiency melt-blown media; meanwhile, China's 2026 indoor-air-quality standard caps PM2.5 at 35 µg/m3, spurring cabin-air and residential filter demand. Supply tightness during 2020-2021 underscored the necessity of domestic melt-blown capacity, justifying government incentives in India, Indonesia, and Brazil. Equipment suppliers report order pipelines stretching into 2028, supporting a healthy backlog for the polypropylene non-woven fabric market.

Geography Analysis

Asia-Pacific controlled 42.67% of global demand in 2025 and is on track for a 6.91% CAGR through 2031 as China and India commission over 35 mt of integrated polypropylene capacity. Reliance's 5.20 million tonnes per annum Jamnagar plant, slated for 2030, alone can feed more than 10 billion m2 of spunbond fabric yearly, signaling an import-replacement strategy that elevates regional self-sufficiency. China's Fujian Eversun pipeline and Indonesia's Tuban complex likewise tighten the intra-Asia resin loop, reducing freight costs and carbon footprints. Converters take advantage, adding Reicofil and Oerlikon lines near end-markets to cut lead times and tailor basis-weight portfolios for local specifications.

North America's polypropylene non-woven fabric market benefits from OEM reshoring moves. Kimberly-Clark's USD 2 billion multi-state program and Avgol's Reicofil 5 installation in North Carolina enhance supply resilience and reduce overreliance on Asian imports. Ahlstrom's filter-media upgrade in Illinois, set for Q4 2026, will meet surging HVAC and EV filtration demand, underlining a structural pivot to domestic raw-material security. Resin price premiums remain a headwind, but domestic logistics savings and tariff avoidance partially offset higher feedstock costs.

Europe adds demand mainly through regulatory push for recyclable solutions. Borealis' 2026 Burghausen investment lines up with PPWR deadlines, offering grades that unlock monomaterial pouches and sterilizable medical wrap markets. Germany's polypropylene imports of 903 kt in 2024 illustrate dependence on intra-EU and Middle Eastern feedstock; CBAM adjustments could further redirect flows toward lower-carbon suppliers. South America and the Middle East & Africa remain emerging pockets, with Brazil's protected-cultivation subsidies and Turkey's twin 1 million tonnes per annum polypropylene projects expanding regional applicability of crop-protection and construction fabrics.

- Ahlstrom

- Amcor plc

- Asahi Kasei Advance Corp.

- Avgol Nonwovens

- Dalian Ruiguang Nonwoven Group

- Don & Low Ltd.

- DuPont

- Fibertex Nonwovens A/S

- Fitesa S.A.

- Freudenberg Group

- Glatfelter Corp.

- Johns Manville

- Kimberly-Clark Worldwide, Inc.

- Kingsafe Group

- Lydall Performance Materials

- Magnera

- Mitsui Chemicals Inc.

- PFNonwovens Holding

- Sandler AG

- Schouw & Co. (Fibertex Personal Care)

- Shandong Kangjie Nonwovens

- Sunshine Nonwoven Fabric Co.

- Suominen Corp.

- Toray Advanced Materials Korea Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand in hygiene and medical disposables

- 4.2.2 Expanding usage in packaging industry

- 4.2.3 Lightweight, cost-effective material economics

- 4.2.4 Increasing utilization in agriculture

- 4.2.5 Antimicrobial PP nonwovens enabling reusable PPE

- 4.3 Market Restraints

- 4.3.1 Environmental and regulatory pressure on single-use plastics

- 4.3.2 Polypropylene price volatility linked to crude oil

- 4.3.3 EU carbon border adjustment raising import cost

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Production Technology

- 5.1.1 Spunbond

- 5.1.2 Meltblown

- 5.1.3 SMS (Spun-Melt-Spun)

- 5.1.4 SMMS (Spun-Melt-Melt-Spun)

- 5.1.5 Other Production Technologies

- 5.2 By Application

- 5.2.1 Hygiene

- 5.2.2 Medical

- 5.2.3 Packaging

- 5.2.4 Automotive

- 5.2.5 Filtration

- 5.2.6 Agriculture

- 5.2.7 Other Applications

- 5.3 By Raw Material Type

- 5.3.1 Homopolymer

- 5.3.2 Copolymer

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share (%)/Ranking Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Ahlstrom

- 6.3.2 Amcor plc

- 6.3.3 Asahi Kasei Advance Corp.

- 6.3.4 Avgol Nonwovens

- 6.3.5 Dalian Ruiguang Nonwoven Group

- 6.3.6 Don & Low Ltd.

- 6.3.7 DuPont

- 6.3.8 Fibertex Nonwovens A/S

- 6.3.9 Fitesa S.A.

- 6.3.10 Freudenberg Group

- 6.3.11 Glatfelter Corp.

- 6.3.12 Johns Manville

- 6.3.13 Kimberly-Clark Worldwide, Inc.

- 6.3.14 Kingsafe Group

- 6.3.15 Lydall Performance Materials

- 6.3.16 Magnera

- 6.3.17 Mitsui Chemicals Inc.

- 6.3.18 PFNonwovens Holding

- 6.3.19 Sandler AG

- 6.3.20 Schouw & Co. (Fibertex Personal Care)

- 6.3.21 Shandong Kangjie Nonwovens

- 6.3.22 Sunshine Nonwoven Fabric Co.

- 6.3.23 Suominen Corp.

- 6.3.24 Toray Advanced Materials Korea Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment