|

시장보고서

상품코드

2062071

스펀본드 부직포 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Spunbond Nonwovens - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

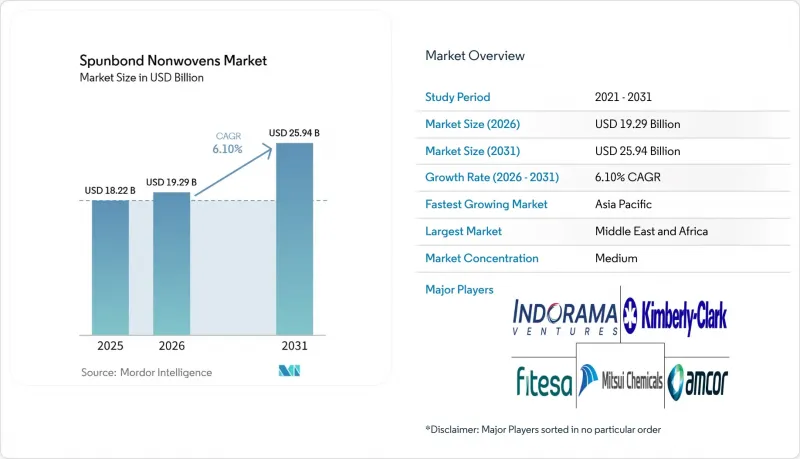

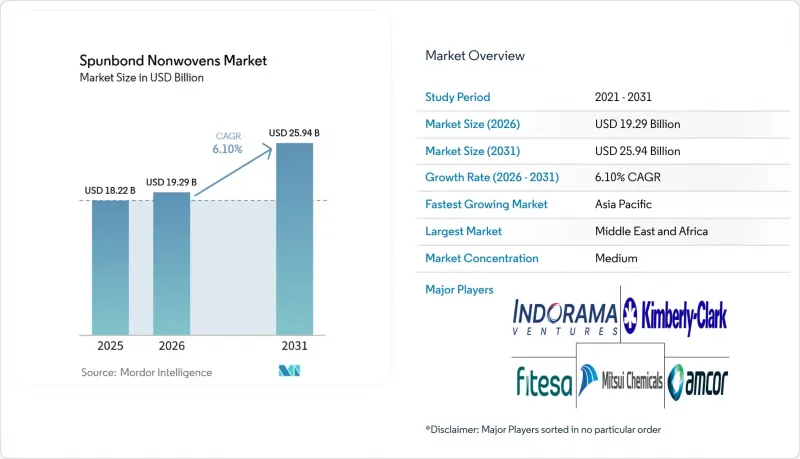

Mordor Intelligence에 의하면, 스펀본드 부직포 시장 규모는 2025년에 182억 2,000만 달러로 평가되었고, 2026년에 192억 9,000만 달러로 추정되며, 2031년까지 259억 4,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 6.10%로 성장할 것으로 전망됩니다.

본 보고서는 소재 유형별(폴리프로필렌, 폴리에스테르, 폴리에틸렌, 기타), 기능별(일회용 및 내구성), 용도별(퍼스널케어, 의료, 포장, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 스펀본드 부직포 시장 동향 및 분석

신흥국에서의 위생용 일회용 제품 수요 급증

인도의 기저귀 시장은 맞벌이 가구 증가, 전자상거래 접근성 확대, 지방 도시에서 일회용 제품 보급을 촉진하는 위생 프로그램의 영향으로 2025년 19억 9,600만 달러로 평가되었고, 2035년까지 82억 8,800만 달러로 성장할 것으로 전망됩니다. 인도네시아에서는 자카르타의 70%에 비해 농촌 지역의 기저귀 보급률이 25%에 불과하여, 비용에 민감한 소비자를 위해 최적화된 저중량 스펀본드 톱시트를 선호하는 양극화된 수요 패턴이 나타나고 있습니다. 2025년 Avgol이 노스캐롤라이나주 목스빌에 1억 달러를 투자해 멀티빔 라인을 설치하고 급성장하는 아시아 시장에 고급 위생용품을 공급하기 시작하면서, 북미는 수출 거점으로 부상하고 있습니다. 프록터 앤 갬블(Procter & Gamble)이나 킴벌리 클라크(Kimberly-Clark)와 같은 세계 기업들은 인도, 베트남, 태국에 현지 가공 거점을 구축하여 리드 타임을 단축하는 동시에, 지역별 취향에 맞추어 스펀본드 폴리프로필렌과 천연섬유를 조합한 SKU를 신속하게 출시할 수 있도록 하고 있습니다.

의료용 보호 장비 시장의 확대

병원의 조달 방침에 따르면, 수술 가운 발주 건수의 78%에 대해 독립 기관의 인증이 의무화되어 있으며, 이는 2024년의 62%에서 증가한 수치로, ANSI/AAMI PB70:2022 차단 규격의 강화된 기준을 반영한 것입니다. 2026년 3월에 출시된 듀폰(DuPont)의 '타이벡 APX 400' 커버올은 클린룸 및 제약 환경용으로 설계된, 통기성이 뛰어나면서도 높은 차단 성능을 갖춘 스펀본드 기반 라미네이트 소재로의 전환을 보여줍니다. 2025년 매출의 65%를, 출하 대수로는 고작 38%에 불과한 보강 SMS 가운이 차지하고 있으며, 이는 종양학과 이식 수술 분야의 감염 관리 프로토콜에 힘입은 프리미엄화 추세를 여실히 보여주고 있습니다. ISO 13485:2016 품질 경영 시스템 표준의 조화를 통해 아시아의 의료기기 제조업체들은 상호인정협정(MRA)에 따라 유럽 및 미국의 병원에 제품을 공급할 수 있게 되었으며, 이로 인해 국경 간 무역 및 제품 등록 절차가 가속화되고 있습니다.

폴리프로필렌에 대한 환경적 우려

프랑스, 독일, 네덜란드에서 시행 중인 확대 생산자 책임 제도에 따라, 현재 재활용이 불가능한 폴리프로필렌 제품에 대해 제품 가격의 최대 20%에 해당하는 환경 부담금이 부과되고 있으며, 이는 여전히 기존 스펀본드 소재에 의존하고 있는 가공업체들의 비용 증가로 이어지고 있습니다. 사용 후 위생용품의 기계적 재활용은 접착제나 고무가 용융 유동성을 저해하기 때문에 여전히 어려우며, 그 결과 대부분의 시판용 폴리프로필렌 등급에서 재생재 함유율은 5% 이하로 제한되고 있습니다. 프라운호퍼 연구소의 용제 기반 용해 공정은 이종 폴리머의 혼입을 80% 줄여 지오텍스타일에 충분한 강도를 지닌 실을 생산하지만, 자본 집약적인 용제 회수 요건이 그 보급을 저해하고 있습니다. 지원 단체는 ASTM D6400 퇴비화 기준이 180일 이내에 90%의 분해를 요구하고 있음을 강조하고 있습니다. 이는 기존 폴리프로필렌 스펀본드로는 달성할 수 없는 기준이며, 브랜드 소유주는 그린워싱이라는 비난에 직면할 위험이 있습니다.

부문별 분석

폴리프로필렌은 저렴한 원료 비용과 높은 생산 능력을 바탕으로 2025년 스펀본드 부직포 시장 규모에서 55.18%의 점유율을 유지했으나, 다른 소재들도 급속히 부상하고 있으며, PLA나 나일론 등은 2031년까지 연평균 성장률(CAGR) 7.24%를 나타낼 것으로 예측됩니다. 폴리에스터는 뛰어난 인장 성능 덕분에 내구성이 요구되는 틈새 시장을 독점하고 있으며, 20%의 가격 프리미엄이 있음에도 불구하고 자동차 내장재 및 지오텍스타일 부문에서 시장 점유율을 확대되고 있습니다. NatureWorks의 'Ingeo 6500D PLA'는 PP에 비해 탄소 발자국이 62% 낮아, 가공업체들이 PPWR(플라스틱 폐기물 감축) 인센티브를 추구하는 가운데 위생용품의 상단 시트에 채택되는 사례가 늘고 있습니다. 전 세계 PLA 생산 능력은 2026년까지 약 100만 톤으로 두 배로 증가할 것으로 예상되며, 과거 도입을 가로막았던 공급 부족에 대한 우려는 점차 사라지고 있습니다. 폴리프로필렌(PP) 부문에서는 보레알리스(Borealis)의 HG485FB 등급이 단일 소재 설계의 적용 범위를 확대하고 있어, 변환업체들이 비용이 많이 드는 설비 교체를 하지 않고도 재활용 관련 규제 요건을 선제적으로 충족할 수 있도록 지원하고 있습니다. 나일론 스펀본드는 여전히 틈새 시장 제품이지만, 삼사라 에코(Samsara Eco)의 공장과 같은 화학 재활용 사업이 2028년에 가동을 시작하면 시장 규모가 확대될 것으로 전망됩니다.

키파스나 멜템 킴야와 같은 2세대 기계적 재활용 업체들은 GRS 인증을 받은 rPET 칩의 원료 공급원을 개발하고 있으며, 스펀본드 제조업체들은 기계적 성능을 저하시키지 않으면서도 PPWR의 재생 소재 함유율 목표를 달성할 수 있게 되었습니다. 이러한 변화는 두 가지 경로로 이어지는 전망을 그려내고 있습니다. 즉, PP는 단기적으로는 비용 면에서 우위를 유지하겠지만, 규제와 소비자의 감시가 강화됨에 따라 바이오 및 재생 소재 대체품이 밸류체인의 상위 단계로 올라설 것이라는 전망입니다. 전반적으로, 폴리머의 다양화는 컨버터의 전환 비용을 증가시키며, 향후 공급 확보를 위해 수지 제조업체와 롤 제품 공급업체 간의 합작 투자가 더욱 활성화될 가능성이 있습니다.

지역별 분석

아시아태평양은 중국의 120만 톤 생산 능력과 인도의 두 자릿수 성장을 지속하는 기저귀 시장에 힘입어, 2025년에는 전 세계 매출의 39.10%를 차지했습니다. 중국 내 산업 재편이 진행되면서, 2024년 저장진안(Zhejiang Kingsafe)이 8억 4,000만 달러의 매출로 세계 8위에 오른 것은 산업이 범용 등급에서 수익성이 높은 의료용 및 여과용 틈새 시장으로 중심을 옮기고 있음을 보여줍니다. 일본 시장 환경은 2025년 이후 변화했습니다. Teijin Ltd(Teijin)와 Asahi Kasei Corp.(Asahi Kasei)가 테크니컬 텍스타일 부문을 통합한 반면, Toray Industries Inc.(Toray)는 비용 절감 프로그램 '다윈(Darwin)'의 일환으로, 적자 상태인 폴리프로필렌(PP) 생산 라인을 폐쇄했습니다. 동남아시아는 여전히 성장의 최전선이며, 인도네시아와 베트남의 지방 지역에서는 기저귀 보급률이 30% 미만인 만큼, 지역 공급업체들은 기저귀를 처음 사용하는 소비자를 확보하기 위해 평량(basis weight)을 최적화한 제품 라인을 확대되고 있습니다.

북미의 동향은 수직 통합과 니어쇼어링에 의해 형성되고 있습니다. 아브골사의 목스빌 공장은 국내 위생용품 수요를 충족시킬 뿐만 아니라, 미국의 물류 강점을 활용해 아시아로 수출도 진행하고 있습니다. FDA의 수술용 가운 관련 규제로 인해, 병원 구매 담당자들은 ISO 13485 인증을 취득한 현지 또는 상호 인정 공급업체를 선택하는 경향이 있어, 중요한 의료용 등급의 저가 아시아산 수입품 시장 침투는 제한되고 있습니다. 캐나다와 멕시코는 USMCA에 따라 보조 허브 역할을 수행하고 있으며, 미국 브랜드는 관세 없이 가공된 제품을 트럭 운송을 통해 3일 이내에 조달할 가능성이 있습니다.

유럽에서는 2026년 8월부터 PPWR(플라스틱 포장 규제)이 시행됨에 따라 규제 강화 움직임이 급속히 진행되고 있습니다. 보레알리스, 파이버텍스, 수오미넨은 규정을 준수하는 단일 소재 생산 라인에 자금을 투자하고 있으며, 독일의 OEM 기업들은 사용 후 플라스틱 수지의 사용을 보장하기 위해 공급망을 면밀히 검토하고 있습니다. 인프라용 지오텍스타일 수요가 북유럽 국가들로 이동하고 있으며, 연안 보호 프로젝트가 과거 러시아 고객들이 구매하던 스펀본드 롤을 대량으로 흡수하고 있습니다. 중동 및 아프리카는 2031년까지 연평균 성장률(CAGR) 7.04%를 기록할 전망이며, 가장 빠르게 성장하고 있는 지역입니다. 이는 '비전 2030'의 철도 회랑과, 스펀본드 소재의 기층재를 지정하는 해수 담수화 플랜트, 그리고 굴산이 연간 4만 톤의 생산 능력을 가동하고 있는 이집트의 급성장하는 위생용품 산업에 힘입은 것입니다. 남미는 규모는 작지만 성장이 가속화되고 있습니다. 브라질과 아르헨티나에서는 농촌 지역의 위생용품 보급률이 낮은 반면, 정부 주도의 위생 개선 캠페인이 진행되고 있으며, 피테사(Fitesa)사의 12억 달러 매출은 이 지역의 성장 잠재력을 입증하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the spunbond nonwovens market size is projected to be USD 18.22 billion in 2025, USD 19.29 billion in 2026, and reach USD 25.94 billion by 2031, growing at a CAGR of 6.10% from 2026 to 2031.

This report is Segmented by Material Type (Polypropylene, Polyester, Polyethylene, and Other Material Types), Function (Disposable and Durable), Application (Personal Hygiene, Medical, Packaging, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Spunbond Nonwovens Market Trends and Insights

Surging Demand for Hygiene Disposables in Emerging Economies

India's diaper market is projected to grow from USD 1.996 billion in 2025 to USD 8.288 billion by 2035, driven by dual-income families, increased e-commerce access, and sanitation programs that are promoting disposable products in smaller cities. In Indonesia, rural areas lag behind with only 25% diaper penetration compared to 70% in Jakarta, creating a two-tiered demand pattern that favors low-basis-weight spunbond topsheets optimized for cost-sensitive consumers. North America is emerging as an export hub after Avgol installed a USD 100 million multi-beam line in Mocksville, North Carolina, in 2025 to supply premium hygiene materials to fast-growing Asian markets. Global players such as Procter & Gamble and Kimberly-Clark have localized converting operations in India, Vietnam, and Thailand, reducing lead times and enabling rapid SKU rollouts that combine spunbond polypropylene with natural fibers to cater to regional preferences.

Expansion of Medical Protective-Gear Market

Hospital procurement policies now require independent certification for 78% of surgical gown orders, up from 62% in 2024, reflecting stricter ANSI/AAMI PB70:2022 barrier standards. DuPont's Tyvek APX 400 coveralls, launched in March 2026, demonstrate a shift toward breathable yet high-barrier spunbond-based laminates designed for clean-room and pharmaceutical environments. Reinforced SMS gowns accounted for 65% of 2025 revenue despite representing only 38% of shipped units, highlighting a premiumization trend driven by infection-control protocols for oncology and transplant surgeries. Harmonized ISO 13485:2016 quality-system standards have enabled Asian converters to serve Western hospitals under mutual-recognition agreements, accelerating cross-border trade and product registration timelines.

Environmental Concerns over Polypropylene

Extended producer responsibility schemes in France, Germany, and the Netherlands now impose eco-modulation fees of up to 20% of product value on non-recyclable polypropylene items, increasing costs for converters still reliant on conventional spunbond. Mechanical recycling of post-consumer hygiene products remains challenging because adhesives and elastics degrade melt flow, keeping recycled-content inclusion below 5% in most commercial polypropylene grades. Fraunhofer's solvent-based dissolution process reduces foreign-polymer contamination by 80% and produces yarns strong enough for geotextiles, but its capital-intensive solvent recovery requirements hinder widespread adoption. Advocacy groups emphasize that ASTM D6400 compostability standards require 90% degradation within 180 days, a benchmark traditional polypropylene spunbond cannot meet, exposing brand owners to accusations of greenwashing.

Other drivers and restraints analyzed in the detailed report include:

- Cost- and Performance-Advantage over Woven Fabrics

- Brand-Owner Shift to Mono-Material PP Packaging

- Volatility in Propylene Feedstock Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene retained a 55.18% share of the spunbond nonwovens market size in 2025 on the back of low raw-material costs and high throughput, yet other material types are moving quickly, with PLA, nylon, etc. forecast at a 7.24% CAGR to 2031. Polyester commands the durable niche because of its elevated tensile performance, winning share in automotive interiors and geotextiles, even at a 20% price premium. NatureWorks' Ingeo 6500D PLA, which carries a 62% lower carbon footprint than PP, is being adopted for hygiene topsheets as converters pursue PPWR incentives. With global PLA capacity expected to double to roughly 1 million tons by 2026, availability fears that once dampened adoption are fading. On the polypropylene side, Borealis' HG485FB grade is expanding the mono-material design window, helping converters keep ahead of recyclability mandates without costly equipment upgrades. Nylon spunbond remains niche but could scale once chemical-recycling ventures such as Samsara Eco's plant come on-stream in 2028.

Second-generation mechanical recyclers like Kipas and Meltem Kimya are opening feedstock taps for GRS-certified rPET chips, letting spunbond producers hit PPWR recycled-content targets without surrendering mechanical performance. These shifts frame a two-track outlook: PP holds near-term cost advantage; bio-based and recycled alternatives climb the value chain as regulation and consumer scrutiny tighten. Overall, polymer diversification raises switching costs for converters and could spur more joint ventures between resin makers and roll-goods suppliers to secure forward offtake.

Geography Analysis

Asia-Pacific locked in 39.10% of global revenue in 2025, supported by China's 1.2 million-ton installed capacity and India's double-digit diaper growth. Chinese consolidation, Zhejiang Kingsafe ranked eighth worldwide with USD 840 million sales in 2024, signals an industry pivot from commodity grades to higher-margin medical and filtration niches. Japan's landscape shifted after 2025, when Teijin and Asahi Kasei merged technical-textile units, while Toray closed unprofitable PP lines under its Darwin cost-saving program. Southeast Asia remains the frontier; Indonesia and Vietnam boast rural diaper penetration below 30%, so regional suppliers are adding basis-weight-optimized lines to capture first-time users.

North American dynamics are shaped by vertical integration and nearshoring. Avgol's Mocksville plant addresses domestic hygiene needs but also exports to Asia, leveraging U.S. logistics resilience. FDA surgical-gown regulations steer hospital buyers toward ISO-13485-certified local or mutual-recognition suppliers, limiting penetration by low-cost Asian imports in critical medical grades. Canada and Mexico act as auxiliary hubs under USMCA, giving U.S. brands tariff-free, three-day truck access to converted goods.

Europe is firmly in regulatory overdrive as PPWR applicability arrives in August 2026. Borealis, Fibertex, and Suominen are pouring funds into compliant mono-material lines, and German OEMs are scrutinizing supply chains to guarantee post-consumer resin inclusion. Infrastructural geotextile demand is shifting toward Nordic countries, where coastal-protection projects soak up spunbond rolls that Russian customers would previously have taken. Middle-East and Africa is the fastest-growing region at a 7.04% CAGR through 2031, buoyed by Vision 2030 rail corridors and desalination plants that specify spunbond underlayers, and by Egypt's burgeoning hygiene complex where Gulsan runs 40,000 tons per year of installed capacity. South America is smaller but accelerating: Brazil and Argentina combine low rural hygiene penetration with state-backed sanitation drives, and Fitesa's USD 1.2 billion sales underline the region's scaling potential.

- Ahlstrom

- Amcor plc

- Asahi Kasei Corporation

- Avgol Industries Ltd

- DuPont de Nemours, Inc.

- Fibertex Nonwovens A/S

- First Quality Nonwovens

- Fitesa S.A.

- Freudenberg Performance Materials

- Ginni Filaments Ltd.

- Hainan Huachen Nonwovens

- Indorama Ventures Public Company Limited

- Jofo Nonwoven Co., Ltd.

- Johns Manville

- KCWW

- Kolon Industries, Inc.

- Mitsui Chemicals, Inc.

- Mogul Nonwovens

- PFNonwovens (Pegas)

- RadiciGroup

- Shandong Ruxing Nonwovens

- Suominen Corporation

- Toray Industries, Inc.

- Xingshifa Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Hygiene Disposables in Emerging Economies

- 4.2.2 Expansion of Medical Protective-gear Market

- 4.2.3 Cost- and Performance-advantage over Woven Fabrics

- 4.2.4 Adoption of Spunbond Geotextiles in Climate-Resilient Infrastructure

- 4.2.5 Brand-owner Shift to Mono-material PP Packaging

- 4.3 Market Restraints

- 4.3.1 Environmental Concerns over Polypropylene

- 4.3.2 Volatility in Propylene Feedstock Pricing

- 4.3.3 Machine-width Limits for High-loft Furniture Grades

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Polypropylene (PP)

- 5.1.2 Polyester (PET)

- 5.1.3 Polyethylene (PE)

- 5.1.4 Other Material Types (Nylon, PLA, etc.)

- 5.2 By Function

- 5.2.1 Disposable

- 5.2.2 Durable

- 5.3 By Application

- 5.3.1 Personal Hygiene

- 5.3.2 Medical

- 5.3.3 Packaging

- 5.3.4 Other Applications (Automotive, Filtration, Agriculture, Furniture, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Ahlstrom

- 6.4.2 Amcor plc

- 6.4.3 Asahi Kasei Corporation

- 6.4.4 Avgol Industries Ltd

- 6.4.5 DuPont de Nemours, Inc.

- 6.4.6 Fibertex Nonwovens A/S

- 6.4.7 First Quality Nonwovens

- 6.4.8 Fitesa S.A.

- 6.4.9 Freudenberg Performance Materials

- 6.4.10 Ginni Filaments Ltd.

- 6.4.11 Hainan Huachen Nonwovens

- 6.4.12 Indorama Ventures Public Company Limited

- 6.4.13 Jofo Nonwoven Co., Ltd.

- 6.4.14 Johns Manville

- 6.4.15 KCWW

- 6.4.16 Kolon Industries, Inc.

- 6.4.17 Mitsui Chemicals, Inc.

- 6.4.18 Mogul Nonwovens

- 6.4.19 PFNonwovens (Pegas)

- 6.4.20 RadiciGroup

- 6.4.21 Shandong Ruxing Nonwovens

- 6.4.22 Suominen Corporation

- 6.4.23 Toray Industries, Inc.

- 6.4.24 Xingshifa Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment