|

시장보고서

상품코드

2062072

아연 도금 강철 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Galvanized Steel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

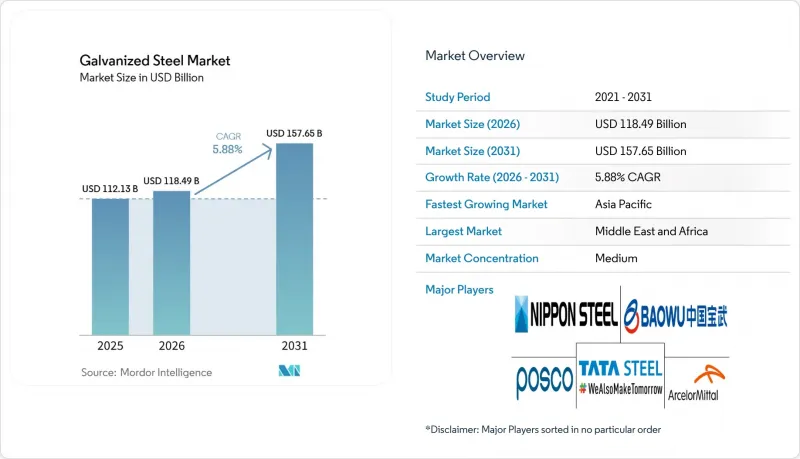

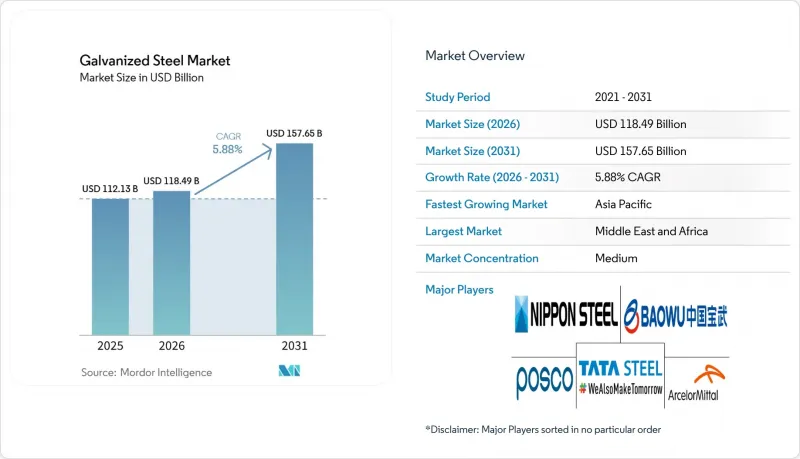

Mordor Intelligence에 의하면, 아연 도금 강철 시장 규모는 2025년 1,121억 3,000만 달러, 2026년 1,184억 9,000만 달러에서 2031년까지 1,576억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 5.88%를 나타낼 것으로 예측됩니다.

본 보고서는 유형(용융 아연 도금 강철 등), 형태(코일·시트, 파이프·튜브, 와이어·로드), 용도(건설, 자동차, 산업용 기기·기계 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 아연 도금 강철 시장 동향 및 분석

건설 및 인프라 분야 수요 증가

사우디아라비아의 ‘비전 2030’ 및 UAE의 다각화 전략에 기반한 대규모 교통 회랑 및 복합 애플리케이션 개발이 피복 강재 수요 증가를 이끌고 있습니다. 이는 SeAH GSI의 2억 4,000만 달러 규모 사우디아라비아 공장 건설과 EMSTEEL의 6억 2,500만 디르함 규모 UAE 사업 확장에서 잘 드러나고 있습니다. 이집트의 수에즈 운하 부교 건설에는 2025년에 8,000톤 이상의 용융 아연 도금 형강이 사용되었으며, 이 자재가 해양 환경에 적합하다는 사실이 입증되었습니다. 인도의 고속도로 및 지하철 개발 계획이 내수 수요를 견인하고 있는 반면, 중국의 ‘일대일로’ 이니셔티브에 따라 코일과 강판이 동남아시아 및 아프리카로 수출되고 있습니다. 중간 소득 국가에서는 내구성이 뛰어나다는 점 때문에 아연 도금 보와 지붕 자재가 계속해서 선호되고 있으며, 2026년 정부의 경기 부양책 예산에 힘입어 향후 수년까지 프로젝트 파이프라인이 확보될 것으로 전망됩니다. 이러한 요인들이 복합적으로 작용하여 아연도금 강재 시장의 지속적인 성장을 뒷받침하고 있습니다.

자동차의 내식성 요건

북미와 유럽에서는 현재 표준으로 자리 잡은 12년 내식성 보증에 따라, 화이트 바디 부품에는 60 g/m² 이상의 아연 도금 두께가 의무화되어 있습니다. 알루미늄에 비해 비용을 40%, 이산화탄소 배출량을 30% 줄일 수 있는 티센크루프의 ‘selectrify’ 배터리 하우징과 같은 혁신적인 제품들이 전기차(EV) 플랫폼에서 인기를 끌고 있습니다. 슈나이더 일렉트릭은 2025년, 산업용 환경에 맞추어 설계된 실외용 충전기용 전기 아연 도금 케이스를 출시했습니다. 태국의 전기차 생산 대수는 2025년에 20% 증가할 것으로 예상되며, 이는 동남아시아 공급망 내 전기 아연 도금 강철 수요를 견인하고 있습니다. 충돌 안전성을 저해하지 않으면서 배터리 무게를 상쇄하기 위해 고강도 아연도금 강종도 활용되고 있으며, 이는 자동차 분야의 아연도금 강 시장 전망을 뒷받침하고 있습니다.

아연 및 철강 원자재 가격 변동

2026년 1분기, 아연 가격은 톤당 평균 3,280-3,650달러를 기록하며 전년 대비 12%-18% 상승했습니다. 이러한 상승으로 인해 아연 도금 업체의 이익률은 200-300베이시스포인트 감소했습니다. 유럽의 열연 코일 가격은 에너지 비용 상승과 할당 규제 강화를 배경으로 2026년 3월에는 톤당 713.57유로에 달했습니다. 제철소가 수익성이 높은 자동차용 강판을 우선시함에 따라, 관재의 리드타임이 35일까지 연장되었습니다. 헤지 능력이 없는 소규모 아연 도금 업체들은 울타리 제품 등 수익성이 낮은 부문에서 철수하고 있습니다. 가격 조항이 어느 정도 위험을 완화하고는 있지만, 가격 변동은 여전히 아연도금 강철 시장의 과제로 남아 있습니다.

부문별 분석

전기 아연 도금 강철 시장 규모는 2031년까지 연평균 성장률(CAGR) 6.21%로 성장하여, 아연 도금 강철 시장 전체의 평균 성장률을 상회할 것으로 예측됩니다. 이러한 성장은 자동차 제조업체들이 노출 패널이나 배터리 하우징에 더 얇고 매끄러운 코팅을 원하고 있기 때문입니다. 2025년, 용융 아연 도금 강철은 비용 효율성이 뛰어나고 건설 용도에 적합한 두꺼운 코팅 덕분에 아연 도금 강철 시장 점유율의 73.26%를 차지했습니다. 전기 아연 도금 강철 시장은 슈나이더 일렉트릭의 실외 충전기 케이스와 동남아시아 지역의 전기차(EV) 생산 증가에 힘입어 성장하고 있습니다. 알루미늄·아연 합금 코팅은 아르셀로미탈의 ‘옵티갈(Optigal)’ 제품 출시를 계기로, 태양광 발전 및 선박용 지붕재 등 고급 용도 분야에서 보급이 확대되고 있습니다. 합금 및 전기 아연 도금 부문이 서로 어우러져 아연 도금 강철 산업의 다양화에 기여하고 있습니다.

전기 아연 도금 강철은 용접성과 도료의 밀착성이 우수하여 선호되고 있으며, 이는 아연 도금량 40-100 g/m²의 DX51D-S220GD 등급을 필요로 하는 가전제품 분야 수요를 견인하고 있습니다. 가전 제조업체들은 특히 습도가 높은 지역에서 이 소재의 성형성과 내식성의 균형을 높이 평가했습니다. 용융 아연 도금은 80-120 g/m²의 도금 두께가 비용 효율이 높은 솔루션을 제공하는 보와 지붕 자재 분야에서 여전히 표준으로 자리 잡고 있습니다. 북미와 유럽에서는 갈바륨의 사용이 증가하고 있지만, 인도와 동남아시아에서는 그 속도가 여전히 완만합니다. 그 결과, 아연 도금 강철 시장에서는 고부가가치의 정밀 도금과 대량 생산형인 기존 도금 방식이 동시에 성장하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 55.18%를 차지하고 있으며, 이는 중국의 99만 톤 생산 능력 증설과 2026년에 계획된 추가 80만 톤에 기인한 것입니다. 중국 바오우(China Baowu)와 HBIS 등 주요 제조업체들은 규모의 경제 효과를 누리며 전 세계 코팅 코일의 약 70%를 공급하고 있습니다. 슈강(Shougang)의 새로운 Zn-Mg-Al 생산 라인은 EU 배출 기준을 준수하면서 50% 이상의 고철을 활용해 연안 지역 인프라 프로젝트를 지원하고 있습니다. 인도의 지하철 및 고속도로 확충으로 인해 2024년부터 2025년까지 해당국의 아연도금 강철 시장이 확대되었습니다. 한편, 동남아시아에서는 베트남의 150만 톤 수요와 인도네시아의 500억 달러 규모 인프라 계획에 힘입어 소비가 증가했습니다. RCEP(지역종합적경제동반자협정)에 따른 관세 인하로 인해 역내 무역이 더욱 활성화되고 있습니다.

중동 및 아프리카는 사우디아라비아와 UAE의 메가 프로젝트를 원동력으로 삼아, 2031년까지 연평균 성장률(CAGR) 6.19%라는 가장 높은 성장률을 기록하며 확대될 것으로 예측됩니다. SeAH GSI의 2억 4,000만 달러 규모 파이프 공장 및 EMSTEEL의 UAE 내 연간 20만 톤 규모 확장 등 다양한 투자가 현지 공급을 뒷받침하고 있습니다. East Pipes Integrated의 코팅 라인에 대한 7,850만 사우디 리얄(SAR) 투자와 이집트의 운하 교량 프로젝트는 선박용 강재 수요 증가를 여실히 보여주고 있습니다. 남아프리카에서는 에너지 가격 급등이 나타나고 있지만, 철탑 및 울타리 수주가 안정감을 가져다주며 해당 지역 시장 점유율 확대에 기여하고 있습니다.

북미에서는 Nucor의 웨스트버지니아주 생산 라인과 California Steel의 2027년 가동 개시를 필두로, 600만 숏톤 이상의 신규 생산 능력이 추가되고 있습니다. 아세롤 미탈의 앨라배마주 12억 달러 규모 전기강판 공장과, US 스틸의 연산 100만 톤 규모 빅 리버 2 아연도금 라인은 ‘바이 아메리카’ 정책에 힘입은 리쇼어링(국내 생산 복귀) 노력을 반영하고 있습니다. 캐나다 해밀턴의 전기로(EAF) 계획은 7년 이내에 이산화탄소 배출량을 60% 감축하는 것을 목표로 하고 있습니다. 이러한 움직임은 공급원의 다각화와 탄소국경조정세(CBAM)에 대한 대응으로 이어지며, 해당 지역의 아연도금 강철 시장을 강화하고 있습니다.

유럽에서는 2025년 말까지 톤당 80-85유로의 탄소 가격과 사상 최고치인 29%에 달하는 수입 점유율에 직면할 것으로 보입니다. 아르셀로미탈은 2029년까지 저탄소강을 생산할 13억 유로 규모의 덩케르크 전기로(EAF) 프로젝트와 크라쿠프에서 4,000만 즈워티 규모의 옵티갈(Optigal) 설비 현대화를 통해 이에 대응하고 있습니다. 할당량 감축과 할당 초과분에 대한 50% 관세가 수입을 제한하는 한편, EUROFER는 2025년 소비량이 2.4% 회복될 것으로 전망하고 있습니다. 이러한 조치는 현지 시장 시장 역학을 보호하기 위한 것입니다.

남미는 여전히 소규모 시장이며, 브라질이 주도적인 역할을 하고 있습니다. 해당 국가에서는 게르다우사가 가전용 강판 생산 라인을 업그레이드하고 있습니다. 아르헨티나의 불안정한 경제 상황이 수입을 제한하고 있어, 바이어들은 국내 제조업체로 눈을 돌리고 있습니다. 많은 생산자들은 건축용 지붕 자재나 농업 기계용으로 배치식 아연 도금 업체에 의존하고 있습니다. 장기적인 성장은 경제 안정화와 인프라 투자에 달려 있지만, 현재 상황에서는 시장이 여전히 분산된 상태입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the galvanized steel market size is projected to expand from USD 112.13 billion in 2025 and USD 118.49 billion in 2026 to USD 157.65 billion by 2031, registering a CAGR of 5.88% between 2026 to 2031.

This report is Segmented by Type (Hot-Dip Galvanized Steel, and More), Form (Coils and Sheets, Pipes and Tubes, Wires and Rods), Application (Construction, Automotive, Industrial Equipment and Machinery, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Galvanized Steel Market Trends and Insights

Growing Demand from Construction and Infrastructure

Large-scale transport corridors and mixed-use developments under Saudi Arabia's Vision 2030 and the UAE's diversification strategies are driving increased demand for coated steel, as evidenced by SeAH GSI's USD 240 million Saudi plant and EMSTEEL's AED 625 million UAE expansion. Egypt's Suez Canal floating bridge utilized over 8,000 tons of hot-dip galvanized sections in 2025, showcasing the material's suitability for marine environments. India's highway and metro development programs are boosting domestic demand, while China's Belt and Road Initiative is exporting coils and sheets to Southeast Asia and Africa. Middle-income economies continue to prefer galvanized beams and roofing for their durability, and government stimulus budgets in 2026 are expected to secure multi-year project pipelines. These factors collectively support sustained growth in the galvanized steel market.

Automotive Corrosion-Resistance Requirements

Twelve-year corrosion warranties, now standard in North America and Europe, mandate zinc coating weights of 60 g/m2 or higher on body-in-white components. Innovations like Thyssenkrupp's selectrify battery housing, which offers a 40% cost and 30% CO2 reduction compared to aluminum, are gaining popularity in electric vehicle (EV) platforms. Schneider Electric introduced electro-galvanized enclosures for outdoor chargers in 2025, designed for industrial environments. Thailand's EV production increased by 20% in 2025, driving demand for electro-galvanized sheets in Southeast Asian supply chains. High-strength galvanized grades are also being utilized to offset battery weight without compromising crash safety, reinforcing the market outlook for galvanized steel in the automotive sector.

Zinc and Steel Raw-Material Price Volatility

In the first quarter of 2026, zinc prices averaged USD 3,280-3,650 per ton, representing a 12%-18% increase compared to the previous year. This rise reduced galvanizer margins by 200-300 basis points. European hot-rolled coil prices reached EUR 713.57 per ton in March 2026, driven by energy cost inflation and stricter quota regulations. Lead times for tubing extended to 35 days as mills prioritized higher-margin automotive sheets. Smaller galvanizers without hedging capabilities are exiting low-margin segments such as fencing products. While price clauses provide some risk mitigation, volatility continues to challenge the galvanized steel market.

Other drivers and restraints analyzed in the detailed report include:

- Renewable-Energy Structures (Solar Frames, Wind Towers)

- Uptake of Lightweight Modules in Modular Housing

- Carbon-Border-Adjustment Tariffs on High-Emission Mills

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electro-galvanized steel grades are anticipated to grow at a 6.21% CAGR through 2031, exceeding the average growth rate of the galvanized steel market. This growth is attributed to automakers' demand for thinner and smoother coatings for exposed panels and battery housings. In 2025, hot-dip galvanized steel captured 73.26% of the galvanized steel market share due to its cost-effectiveness and thicker coatings, which are well-suited for construction applications. The market for electro-galvanized sheets is supported by Schneider Electric's outdoor charger enclosures and the increasing production of electric vehicles (EVs) in Southeast Asia. Aluminum-zinc alloy coatings are gaining traction in premium applications such as solar and marine roofing, driven by ArcelorMittal's Optigal product launch. Together, the alloy and electro-galvanized segments are contributing to a more diversified galvanized steel industry.

Electro-galvanized steel is preferred for its weldability and paint adhesion, which drive its demand in appliances requiring DX51D to S220GD grades with 40-100 g/m2 zinc coatings. Appliance manufacturers value its balance of formability and corrosion resistance, particularly in humid regions. Hot-dip galvanizing remains the standard for beams and roofing, where 80-120 g/m2 coatings provide cost-effective solutions. While Galvalume adoption is increasing in North America and Europe, it remains slower in India and Southeast Asia. Consequently, the galvanized steel market is experiencing simultaneous growth in high-value precision coatings and high-volume traditional coatings.

Geography Analysis

Asia-Pacific accounted for 55.18% of 2025 revenue, driven by China's 990-kiloton capacity addition and an additional 800 kilotons planned for 2026. Major producers like China Baowu and HBIS supply approximately 70% of global coated coil, benefiting from economies of scale. Shougang's new Zn-Mg-Al line supports coastal infrastructure projects while utilizing over 50% scrap, aligning with EU emission standards. India's metro and highway expansions boosted the local galvanized steel market in 2024-2025, while Southeast Asia saw increased consumption due to Vietnam's 1.5 million-ton demand and Indonesia's USD 50 billion infrastructure plan. RCEP tariff reductions further enhance intra-regional trade.

The Middle-East and Africa are expected to grow at the fastest rate of 6.19% CAGR through 2031, driven by megaprojects in Saudi Arabia and the UAE. Investments such as SeAH GSI's USD 240 million pipe mill and EMSTEEL's 200,000-tpy UAE expansion support localized supply. East Pipes Integrated's SAR 78.5 million investment in coating lines and Egypt's canal bridge project highlight marine-grade demand. Despite energy inflation in South Africa, tower and fencing orders provide stability, contributing to the region's growing market share.

North America is adding over 6 million short tons of new capacity, led by Nucor's West Virginia lines and California Steel's 2027 startup. ArcelorMittal's USD 1.2 billion electrical-steel plant in Alabama and U.S. Steel's 1 million-ton Big River 2 galvanizing line reflect reshoring efforts supported by Buy America policies. Canada's EAF proposals in Hamilton aim to reduce CO2 emissions by 60% within seven years. These developments diversify supply and address carbon-border risks, strengthening the region's galvanized steel market.

Europe faces EUR 80-85 per-tonne carbon prices and a record 29% import share in late 2025. ArcelorMittal is responding with a EUR 1.3 billion Dunkirk EAF producing low-CO2 steel by 2029 and a PLN 40 million Optigal upgrade in Krakow. Quota reductions and 50% over-quota duties limit import access, while EUROFER forecasts a 2.4% consumption recovery in 2025. These measures aim to protect local market dynamics.

South America remains a smaller market, led by Brazil, where Gerdau is upgrading lines for appliance sheets. Economic volatility in Argentina limits imports, pushing buyers toward domestic mills. Many producers rely on batch galvanizers to serve construction roofing and farm machinery. Long-term growth depends on economic stabilization and infrastructure investments, but current conditions keep the market fragmented.

- AHMSA

- ArcelorMittal

- China Baowu Steel Group Corp., Ltd.

- Cleveland-Cliffs Inc.

- Gerdau S/A

- Hoa Sen Group

- Hyundai Steel

- JFE Steel Corp.

- Jindal Steel & Power

- JSW Steel Ltd.

- Liberty Steel Group

- NIPPON STEEL CORPORATION

- Nucor Corporation

- POSCO

- Salzgitter Flachstahl GmbH

- Severstal

- Shougang Group

- Tata Steel

- Thyssenkrupp AG

- United States Steel Corporation

- voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from construction and infrastructure

- 4.2.2 Automotive corrosion-resistance requirements

- 4.2.3 Renewable-energy structures (solar frames, wind towers)

- 4.2.4 Uptake of lightweight modules in off-site and modular housing

- 4.2.5 AI-driven predictive-maintenance coating-quality systems

- 4.3 Market Restraints

- 4.3.1 Zinc and steel raw-material price volatility

- 4.3.2 Alternative metallic coatings (Al-Zn, Zn-Mg-Al)

- 4.3.3 Carbon-border-adjustment tariffs on high-emission mills

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Hot-Dip Galvanized Steel

- 5.1.2 Electro-Galvanized Steel

- 5.1.3 Galvalume/Al-Zn Alloy-Coated Steel

- 5.2 By Form

- 5.2.1 Coils and Sheets

- 5.2.2 Pipes and Tubes

- 5.2.3 Wires and Rods

- 5.3 By Application

- 5.3.1 Construction

- 5.3.2 Automotive

- 5.3.3 Industrial Equipment and Machinery

- 5.3.4 Home Appliances and HVAC

- 5.3.5 Energy and Utilities

- 5.3.6 Agriculture, Fencing and Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AHMSA

- 6.4.2 ArcelorMittal

- 6.4.3 China Baowu Steel Group Corp., Ltd.

- 6.4.4 Cleveland-Cliffs Inc.

- 6.4.5 Gerdau S/A

- 6.4.6 Hoa Sen Group

- 6.4.7 Hyundai Steel

- 6.4.8 JFE Steel Corp.

- 6.4.9 Jindal Steel & Power

- 6.4.10 JSW Steel Ltd.

- 6.4.11 Liberty Steel Group

- 6.4.12 NIPPON STEEL CORPORATION

- 6.4.13 Nucor Corporation

- 6.4.14 POSCO

- 6.4.15 Salzgitter Flachstahl GmbH

- 6.4.16 Severstal

- 6.4.17 Shougang Group

- 6.4.18 Tata Steel

- 6.4.19 Thyssenkrupp AG

- 6.4.20 United States Steel Corporation

- 6.4.21 voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Galvanized Steel in EV Charging Stations and Battery Enclosures

- 7.3 Closed-Loop Recycling and "Green-Galv" Premiums