|

시장보고서

상품코드

2062092

미국의 용접 소모품 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Welding Consumables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

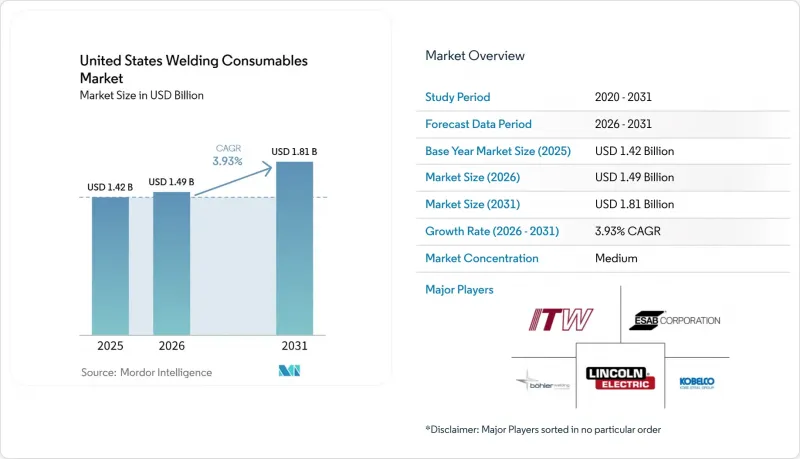

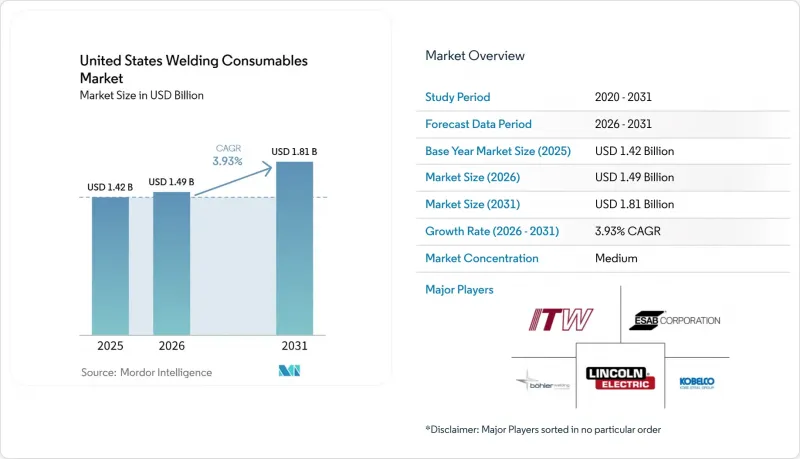

Mordor Intelligence에 의하면, 미국의 용접 소모품 시장 규모는 2025년 14억 2,000만 달러로 평가되었고, 2026년에는 14억 9,000만 달러로 추정되고, 2026-2031년 CAGR 3.93%로 성장을 지속할 전망이며, 2031년까지 18억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형별(봉형 전극, 플럭스 함유 와이어 등), 용접 공정별(아크 용접(SMAW, GMAW, GTAW, FCAW), 저항 용접 등), 최종 이용 산업별(건설 및 인프라, 자동차 및 운송, 에너지 등), 지역별(북동부, 중서부, 남부, 서부)로 분류되어 있습니다. 시장 전망은 금액 단위로 제시되어 있습니다.

미국의 용접 소모품 시장 동향 및 분석

인프라 투자 및 현대화법 시행

연방 정부의 인프라 지출은 교량 및 고속도로 건설과 같이 철강을 대량으로 사용하는 공사를 뒷받침하며, 교량 및 구조물의 규격을 충족하는 구조용 용접 소모재에 대한 안정적인 수요를 지탱하고 있습니다. '인프라 투자 및 고용법'은 연방도로청을 통해 다년간의 예산 배분을 지속적으로 실시하고 있으며, 이를 통해 주 차원의 교량 계획 및 관련 철강 가공 수요를 예측할 수 있게 되었습니다. 건축자재 가격 상승으로 당분간 물리적 공급은 제한되고 있지만, 자금 조달 전망은 여전히 양호하여 2026년까지의 작업량을 뒷받침하고 있습니다. 이는 교량 및 대형 토목 철골 구조물 프로젝트에 필수적인 저수소 피복봉, 솔리드 와이어, 플럭스 함유 와이어에 있어 특히 중요한 사항입니다. 공기 압박으로 인해 도급업체들이 재현성과 일관된 용접 비드 품질을 보장하는 자동화 대응 용접 자재를 채택하게 되면, 미국의 용접 자재 시장은 그 혜택을 누리게 될 것입니다. 연방 정부의 배정액에 주 정부의 교통 계획이 더해짐에 따라, 강철 거더의 제조 및 현장 조립 수주 잔고는 안정적인 상태를 유지하고 있으며, 이는 예측 기간 동안 용접 자재 수요를 뒷받침하고 있습니다.

중공업 및 금속 가공의 국내 복귀

각 제조업체는 반도체, 배터리 및 첨단 기기의 국내 생산 능력을 확대하고 있으며, 이에 따라 스테인리스, 니켈, 알루미늄 등 다양한 등급의 특수 용가재에 대한 중기적 수요가 증가하고 있습니다. 미국의 용접 소모품 시장에서는 OEM 제조업체들이 고부가가치 공정의 현지화를 추진함에 따라, 팹 및 배터리 시설에서 추적성 및 클린룸 대응이 가능한 소모품을 요구하는 사양이 증가하고 있습니다. 자동차 공급망에서는 남부 및 남서부에 신설되는 시설에서 재가공을 줄이고, 대규모 프로젝트의 기술 격차 해소에 기여할 수 있도록 자동화에 적합한 와이어 및 공정 제어와 설비 선정을 조화시키고 있습니다. 또한, 미국의 용접 소모품 시장은 이중 인증 및 문서화된 절차의 인정을 권장하는 보다 광범위한 공급업체 품질 프레임워크의 혜택을 받고 있으며, 이로 인해 규제 환경 하에서 프리미엄 등급의 역할이 더욱 중요해지고 있습니다. 자본 프로젝트가 발표 단계에서 설치 단계로 넘어가는 사례가 늘어남에 따라, 용접 소모품의 구매 주기는 더욱 예측 가능해졌으며, 현지 재고와 기술 지원을 갖춘 공급업체가 유리한 입지를 점하고 있습니다.

고령화되는 용접공과 제한된 후계자층

용접공의 연령 중앙값은 일반 노동력보다 높아, 이로 인해 이용 가능한 노동력 풀이 부족해지고 고용주의 교육 부담이 증가하고 있습니다. 많은 제조업체들은 이에 대응하여 자동화, 로봇 셀, 그리고 기술적 편차를 줄이는 표준화된 절차를 도입하고 있으며, 이에 따라 소모품 선정이 안정적인 아크 점화 및 재현성 있는 용접 비드 형상을 지원하는 제품으로 전환되고 있습니다. 따라서 미국의 용접 소모품 시장에서는 자동화 공법에 적합한 엄격한 공차 기준을 충족하고 성능이 입증된 와이어와 플럭스에 대한 관심이 높아지고 있습니다. 교육 방식도 변화하고 있어, 로봇 아크 용접이나 저항 용접에 대응할 수 있는 자격 취득이 더욱 중요시되며, 더 짧은 기간 내에 작업자의 역량을 넓힐 수 있도록 하고 있습니다. 예측 기간 동안 이러한 인구 통계학적 요인은 일부 용도에서는 공정 대체를 촉진하는 한편, 아크 용접을 계속 사용하는 다른 용도에서는 고품질 소모품에 대한 수요를 뒷받침하게 될 것입니다.

부문별 분석

미국의 용접 소모품 시장에서 2025년 매출의 37.12%를 차지하는 봉형 전극이 가장 큰 점유율을 유지하고 있는 반면, 플럭스 함유 와이어는 2031년까지 연평균 성장률(CAGR) 5.76%로 가장 빠르게 성장할 것으로 전망됩니다. 봉형 전극은 휴대성, 설치 속도 및 표면 상태에 대한 적응성 덕분에, 연속 와이어 공정의 생산성 향상보다 현장 수리, 구조물 프로젝트 및 유지보수 작업에서 여전히 널리 사용되고 있습니다. 미국의 용접 소모품 시장에서는 에너지 관련 분야나 토목 현장의 파이프라인 연결 공사, 외딴 지역의 건설 및 보수 작업에서 저수소형 및 셀룰로오스계 스틱 용접봉에 대한 의존도가 여전히 높습니다. 한편, 플럭스 함유 와이어는 수직 및 상향 용접 시 높은 용접 속도를 구현할 수 있어 시장 점유율을 확대되고 있습니다. 이는 1피트당 인건비가 중요한 교량 건설, 고층 건축 및 모듈식 조선에 적합합니다. 구조용 강재에 관한 규격의 개정과 품질 관리 체제 덕분에, 봉재 및 플럭스 함유 와이어 양쪽 형태 모두에서 인증된 용접 재료에 대한 수요가 유지되고 있으며, 이는 공장 내 및 현장에서의 용도에 걸친 균형 잡힌 제품 구성을 뒷받침하고 있습니다.

플럭스 함유 와이어는 재현성과 처리량을 우선시하는 대규모 프로젝트나 로봇 셀에서의 자동화에 적합하며, 이는 2031년까지 주도적인 성장 추세를 뒷받침하고 있습니다. 솔리드 와이어는 안정적인 아크 특성과 표준 GMAW 시스템과의 호환성 덕분에 자동차, 중장비 및 일반 가공 분야에서 꾸준한 중저가 시장용 선택지로 자리매김하고 있습니다. SAW용 플럭스 및 와이어는 압력 용기, 송유관 공장 및 대형 구조 부재 분야에서 확고한 틈새 시장을 유지하고 있습니다. 이는 일관된 기계적 특성과 제어된 열입력으로 인해, 플럭스 처리 및 공정 관리에 대한 설비 투자가 정당화되기 때문입니다. TIG 용접봉 및 브레이징 합금은 항공우주, 제약용 배관, 식품용 스테인리스 가공 분야의 고순도 또는 박판 용도에 사용되며, 이들은 고가 제품군에 속하며 엄격한 문서화 요건이 적용됩니다. 미국의 용접 소모품 업계에서는 작업 내용에 따른 제품 선정의 최적화가 앞으로도 지속될 것으로 예상되며, 이에 따라 현장 작업에서의 아크 용접봉 수요가 유지될 뿐만 아니라, 구조물 및 모듈식 건축 분야에서 플럭스 함유 와이어 제품 시장 평균을 상회하는 성장이 뒷받침될 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the united states welding consumables market size is expected to grow from USD 1.42 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 1.81 billion by 2031 at 3.93% CAGR over 2026-2031.

This report is Segmented by Product Type (Stick Electrodes, Flux-Cored Wires, and More), by Welding Process (Arc (SMAW, GMAW, GTAW, FCAW), Resistance Welding, and More), by End-Use Industry (Construction & Infrastructure, Automotive & Transportation, Energy, and More), and by Geography (Northeast, Midwest, South, and West). The Market Forecasts are Provided in Terms of Value (USD Billion).

United States Welding Consumables Market Trends and Insights

Infrastructure Investment and Modernization Act Implementation

Federal infrastructure spending has raised the floor for steel-intensive work in bridges and highways, supporting steady demand for structural welding consumables that meet bridge and structural codes. The Infrastructure Investment and Jobs Act continues to funnel multi-year allocations through the Federal Highway Administration, which provides visibility into state-level bridge programs and related steel fabrication needs. While inflation in construction inputs has tempered the immediate physical delivery, the funding horizon remains robust, supporting workloads through 2026. This is particularly pertinent for low-hydrogen stick electrodes, solid wires, and flux-cored wires, all essential for bridges and heavy civil steel projects. The United States welding consumables market benefits when schedule pressure pushes contractors toward automation-ready consumables that support repeatability and consistent bead quality. State transportation plans layered on federal allocations keep backlogs steady for steel girder fabrication and field assembly, which supports consumables offtake throughout the forecast window.

Onshoring of Heavy Manufacturing and Metal Fabrication

Manufacturers are increasing domestic capacity in semiconductors, batteries, and advanced equipment, which reinforces medium-term demand for specialized filler metals across stainless, nickel, and aluminum grades. The United States welding consumables market is seeing more specifications that call for traceability and cleanroom-compatible consumables in fabs and battery facilities as OEMs localize high-value steps. In automotive supply chains, new facilities in the South and Southwest are aligning equipment selection with automation-friendly wires and process controls that reduce rework and help bridge skill gaps on large projects. The United States welding consumables market is also benefiting from broader supplier quality frameworks that encourage dual certification and documented procedure qualification, which deepens the role of premium grades in regulated environments. As more capital projects move from announcement to installation, purchasing cycles for welding consumables become more predictable and favor suppliers with local inventories and technical support.

Aging Welder Workforce with Limited Replacement Pipeline

The median age of welders is higher than the broader workforce, which tightens the available labor pool and raises training burdens for employers. Many fabricators respond by adopting automation, robotic cells, and standardized procedures that reduce skill variability, which shifts consumables selection toward products that support consistent arc starts and repeatable bead geometry. The United States welding consumables market is thus seeing stronger interest in wires and fluxes with tight tolerances and documented performance for automated processes. Training pathways are also evolving, with more emphasis on certifications that align with robotic arc welding and resistance welding to broaden operator capabilities in shorter timeframes. Over the forecast period, this demographic pressure encourages process substitution in some applications while supporting premium-grade consumables in others that remain arc-based.

Other drivers and restraints analyzed in the detailed report include:

- Natural Gas Pipeline Network Expansion and Replacement

- Commercial Construction Boom in Sunbelt States

- Raw Material Price Volatility for Steel Wire and Flux

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stick electrodes held the largest share at 37.12% of 2025 revenue within the United States welding consumables market, while flux-cored wires are projected to grow fastest at a 5.76% CAGR through 2031. Stick remains entrenched in field repairs, structural projects, and maintenance tasks where portability, setup speed, and tolerance to surface conditions outweigh the productivity gains of continuous-wire processes. The United States welding consumables market continues to rely on low-hydrogen and cellulosic stick grades for pipeline tie-ins, remote construction, and repair work across energy and civil sites. In parallel, flux-cored wires are gaining share because they deliver high deposition rates in vertical and overhead positions, suiting bridge erection, high-rise construction, and modular shipbuilding, where labor cost per linear foot matters. Code updates and quality frameworks in structural steel maintain the need for certified consumables in both stick and flux-cored formats, which supports a balanced product mix across shop and field uses.

Flux-cored wires are aligned with automation on large projects and in robotic cells that prioritize repeatability and throughput, which fuels their leading growth profile through 2031. Solid wires remain a steady mid-market option for automotive, heavy equipment, and general fabrication due to their stable arc characteristics and compatibility with standard GMAW systems. SAW flux and wire hold a durable niche in pressure vessels, line pipe mills, and heavy structural sections because consistent mechanical properties and controlled heat input justify capital investment in flux handling and process controls. TIG rods and brazing alloys serve high-purity or thin-wall applications in aerospace, pharmaceutical piping, and food-grade stainless work, which carry premium pricing and strict documentation needs. The United States welding consumables industry is expected to see continued optimization of product selection by job context, which sustains stick volumes in field work and supports above-market growth for flux-cored products in structural and modular builds.

List of Companies Covered in this Report:

- Lincoln Electric Holdings Inc.

- ESAB Corporation

- Illinois Tool Works Inc. (Hobart Brothers)

- voestalpine Bohler Welding USA

- Kobe Steel Ltd. (Kobelco Welding of America)

- Air Liquide Welding

- Sandvik Materials Technology (Exaton)

- Messer Group

- Wire Wizard Welding Products

- Harris Products Group

- Washington Alloy Co.

- Weldcote Metals

- Eutectic Castolin

- Select-Arc Inc.

- Alcotec Wire Corp.

- Arcon Welding Equipment

- Blue Demon Welding Products

- Fronius USA LLC

- Praxair (Linde) Filler Metals

- McKay (Lincoln Electric)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure Investment and Modernization Act Implementation

- 4.2.2 Onshoring of Heavy Manufacturing and Metal Fabrication

- 4.2.3 Natural Gas Pipeline Network Expansion and Replacement

- 4.2.4 Commercial Construction Boom in Sunbelt States

- 4.2.5 Shipbuilding and Naval Vessel Construction Uptick

- 4.2.6 Maintenance and Repair Activities in Oil and Gas Sector

- 4.3 Market Restraints

- 4.3.1 Aging Welder Workforce with Limited Replacement Pipeline

- 4.3.2 Raw Material Price Volatility for Steel Wire and Flux

- 4.3.3 Shift Toward Alternative Joining Methods in Automotive

- 4.3.4 Economic Sensitivity to Construction and Manufacturing Cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Distributor Network Consolidation Through Private Equity Activity

- 4.9 Growing Demand for Stainless Steel Consumables in Food Processing

5 Market Size & Growth Forecasts (Values, In USD Billion)

- 5.1 By Product Type

- 5.1.1 Stick Electrodes

- 5.1.2 Solid Wires

- 5.1.3 Flux-Cored Wires

- 5.1.4 SAW Flux & Wire

- 5.1.5 TIG Rods & Brazing Alloys

- 5.2 By Welding Process

- 5.2.1 Arc

- 5.2.1.1 SMAW (Stick)

- 5.2.1.2 GMAW / MIG

- 5.2.1.3 GTAW / TIG

- 5.2.1.4 FCAW

- 5.2.2 Resistance Welding

- 5.2.3 Laser & Hybrid Welding

- 5.2.1 Arc

- 5.3 By End-Use Industry

- 5.3.1 Construction & Infrastructure

- 5.3.2 Automotive & Transportation

- 5.3.3 Energy (Oil, Gas & Power)

- 5.3.4 Shipbuilding & Offshore

- 5.3.5 Heavy Equipment & Industrial Machinery

- 5.3.6 Others

- 5.4 By Region

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 South

- 5.4.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Lincoln Electric Holdings Inc.

- 6.4.2 ESAB Corporation

- 6.4.3 Illinois Tool Works Inc. (Hobart Brothers)

- 6.4.4 voestalpine Bohler Welding USA

- 6.4.5 Kobe Steel Ltd. (Kobelco Welding of America)

- 6.4.6 Air Liquide Welding

- 6.4.7 Sandvik Materials Technology (Exaton)

- 6.4.8 Messer Group

- 6.4.9 Wire Wizard Welding Products

- 6.4.10 Harris Products Group

- 6.4.11 Washington Alloy Co.

- 6.4.12 Weldcote Metals

- 6.4.13 Eutectic Castolin

- 6.4.14 Select-Arc Inc.

- 6.4.15 Alcotec Wire Corp.

- 6.4.16 Arcon Welding Equipment

- 6.4.17 Blue Demon Welding Products

- 6.4.18 Fronius USA LLC

- 6.4.19 Praxair (Linde) Filler Metals

- 6.4.20 McKay (Lincoln Electric)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment