|

시장보고서

상품코드

2062099

무연탄 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Anthracite - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

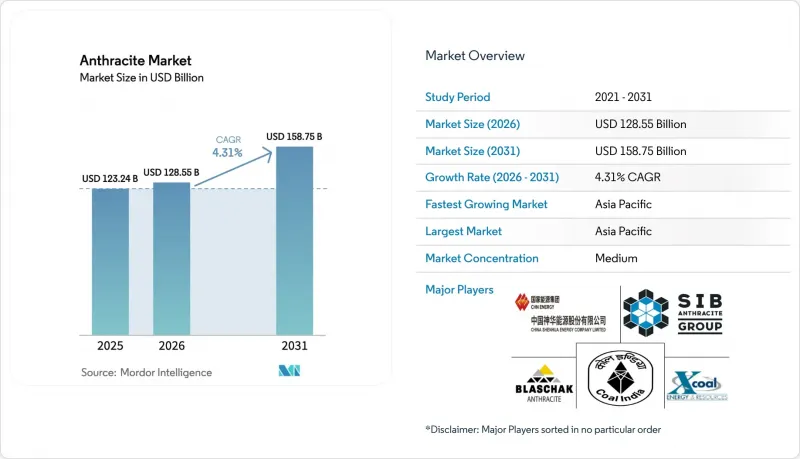

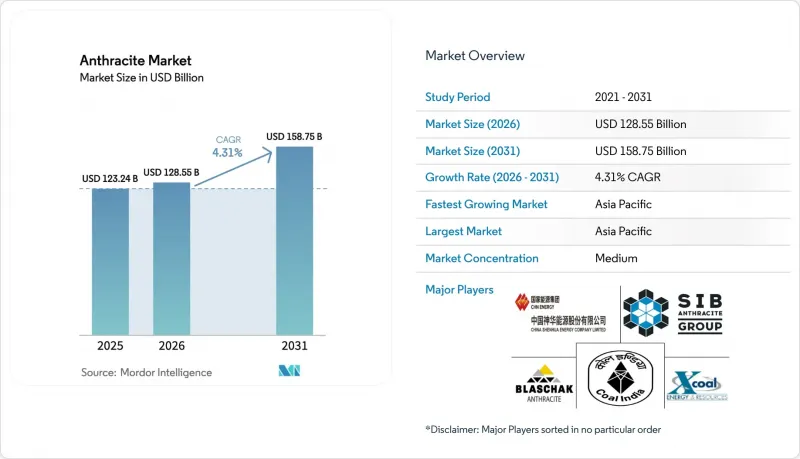

Mordor Intelligence에 의하면, 무연탄 시장 규모는 2025년에 1,232억 4,000만 달러로 평가되었고, 2026년 1,285억 5,000만 달러로 추정되고, 2031년까지 1,587억 5,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.31%를 나타낼 전망입니다.

본 보고서는 등급별(표준 등급, 초고품위(UHG), 소성 및 전기 소성 등급), 용도별(야금, 물 및 폐수 여과 등), 최종 사용자 산업별(철강 및 야금, 화학제품 및 석유화학제품, 수처리 사업 등), 지역별(아시아태평양, 북미 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 무연탄 시장 동향 및 분석

그린 스틸 제강 공정에서 초저회분 탄소 첨가제의 의무화

수소 DRI나 전기 아크로로로의 전환을 추진하는 철강 제조업체들은 슬래그 발생량을 최소화하고 용융욕의 화학 성분을 유지하기 위해, 회분 8% 미만이며 황분 0.4% 이하인 탄소 첨가제가 필요합니다. 펜실베이니아주에서 최근 이루어진 인수 건은 미국과 유럽의 전기로(EAF) 확장 수요를 충족하기 위해 이러한 초고품질 광상을 명확한 목표로 삼고 있습니다. 중국이 2030년까지 전기 아크로 시장 점유율을 20%로 끌어올릴 계획인 만큼, 저휘발분 원료를 둘러싼 세계적 경쟁이 치열해지고 있으며, 중품질 열용 무연탄이 천연가스 DRI나 바이오카본으로 대체되고 있는 상황에서도 프리미엄 가격을 유지하고 있습니다.

지자체에서의 듀얼 미디어(안트라사이트+모래) 여과층으로의 전환

북미 및 유럽의 유틸리티체들은 기존의 모래 여과 장치에 거친 입자의 무연탄 캡을 추가하는 개조 작업을 진행하고 있으며, 이를 통해 가동 기간을 최대 50% 연장하고 역세척 비용을 절감하고 있습니다. 새크라멘토시의 2025년 계약 수정안과 워터 리서치 재단(WRF)이 추진하는 50만 달러 규모의 PFAS 프로젝트는 이러한 수요가 장기적인 주기를 따르며 사양 중심적이라는 점을 여실히 보여주고 있습니다. 이러한 운영 비용 절감을 통해 조달 예산은 가격 변동의 충격으로부터 보호받으며, 무연탄 시장의 한 축을 견고하게 지탱하고 있습니다.

석유 코크스 및 바이오카본 가격 할인

2024-2026년, 고황 함유 미국 멕시코만 연안산 석유 코크스는 톤당 60달러라는 저가에 거래되고 있으며, 시멘트 가마 및 산업용 보일러 시장에서 무연탄의 점유율을 잠식하고 있습니다. 스웨덴의 전기로(EAF)에서 진행 중인 파일럿 규모의 바이오카본 시험은 탄소 중립을 약속하는 것으로, 공급망이 성숙되면 대체 과정을 가속화할 가능성이 있습니다. 생산자들은 계약 기간을 연장하고, 가격이 아닌 품질이 채택 여부를 좌우하는 무연탄의 저회분 및 저휘발분 특성을 강조함으로써 이에 대응하고 있습니다.

부문별 분석

2025년, 표준 등급은 기존의 수처리, 주택용 난방 및 중규모 제철 수요에 힘입어 무연탄 시장에서 47.12%의 점유율을 유지했습니다. 그러나 시멘트 가마 및 보일러 용도에서 석유 코크스에 가격 면에서 밀리면서, 이 하위 부문의 이익률은 감소했습니다. 반면, 소성 등급 및 전기 소성 등급은 2031년까지 연평균 성장률(CAGR) 5.12%를 나타낼 것으로 예측되며, 고정 탄소 함량 95% 이상을 중시하는 리튬 이온, 나트륨 이온 및 연료전지용 음극재 수주를 확보할 전망입니다. 중국 배터리 제조업체와 펜실베이니아주 및 시베리아의 생산자 간에 체결된 초기 단계공급 계약은 예측 기간 동안 소성용 등급에 할당될 무연탄 시장 전체 규모를 끌어올릴 것으로 보이며, 이는 꾸준한 수요 증가를 시사합니다.

고정 탄소분 92% 이상이자 휘발분 5% 이하로 정의되는 초고품위(UHG) 무연탄은 가장 높은 가치를 지니며, 표준 제품에 비해 20-40% 높은 프리미엄 가격에 거래되고 있습니다. 2025년 메나 사가 스프링레이크 탄광을 인수함에 따라, 수출용 품질의 UHG 원료가 연간 72만 톤이 세계 공급량에 추가되었습니다. 엄격한 규격 범위 덕분에 UHG는 페로합금의 환원 및 전기 아크로(EAF) 주입 과정에서 필수적인 소재로 자리매김했으며, 저급 석탄에 비해 운임 급등이나 규제 비용에 대한 내성이 강하기 때문에 해당 틈새 시장은 견고하게 유지되고 있습니다.

지역별 분석

아시아태평양은 2025년 수요의 53.24%를 차지했으며, 무연탄 시장을 주도하고 있으며, 중국의 석탄 화학 사업 확대와 인도의 2028-2029년도 10억 톤 생산 목표에 힘입어, 2031년까지 연평균 성장률(CAGR) 4.47%를 기록할 전망입니다. 중국 신화그룹이 350억 달러 규모로 13개 자회사를 인수하는 구조조정은 광산에서 항만에 이르는 공급망을 효율화할 수 있는 물류 및 전력 자산을 확보하는 동시에 매장량을 25% 확대하는 것입니다. 아세안 국가들, 특히 인도네시아와 베트남에서는 석탄 화력 발전 및 클링커 생산 능력 확충이 계속되고 있으며, 수입 무연탄의 높은 발열량과 적은 불순물 함량 덕분에 국내산 갈탄에 비해 경쟁 우위를 점하고 있습니다.

북미의 무연탄 시장은 펜실베이니아주의 100년 이상의 역사를 지닌 탄전에 의존하고 있습니다. 이 지역에서는 2024년 델타 두니아가 애틀랜틱 카본 그룹을 인수하여 4개의 초고급 탄광을 1억 2,240만 달러에 자회사로 매입했습니다. 유럽 및 아시아로의 수출은 2014년 이후 두 자릿수 성장률을 기록하며 확대되고 있으며, 이는 휘발성 성분 함량 및 저유황 함량과 같은 차별화 요소를 반영한 결과입니다. 재생에너지와 저렴한 천연가스가 발전 용량을 잠식함에 따라 국내 화력 발전 수요는 감소하고 있지만, 여과재와 특수 탄소의 틈새 시장이 기본적인 처리량을 지탱하고 있습니다.

유럽에서는 화력 수요가 감소하고 있음에도 불구하고, 특수 석탄 부문은 호황을 누리고 있습니다. EU의 탄소국경조정제도(CBAM)에 따라 수입업체들은 인증된 저탄소 석탄으로의 전환을 촉진받고 있으며, 이로 인해 광산 현장에서의 효율성을 입증할 수 있는 미국 및 남아프리카공화국 공급업체들에게 시장 기회가 열리고 있습니다. 동유럽의 지역 난방 시설과 북유럽의 수처리 시설은 계속해서 현물 구매를 진행하고 있지만, 장기적인 거래량은 석탄 단계적 폐지 정책의 진행 상황에 달려 있습니다. 브라질을 비롯한 남미 지역에서는 환율 변동과 운임 변동에 따라 시장이 요동치고 있습니다. 러시아산 석탄 공급이 지정학적 장벽에 부딪힌 후, 2025-2026년 호주산 석탄의 점유율은 30%까지 급증했습니다. 아프리카의 중심지는 남아프리카이며, 메나사의 확장을 통해 이 지역은 수출 지향적인 초고품질 핵심 거점을 확보하게 되었습니다. 한편, 트랜스넷 개혁을 통해 제3자를 위한 철도 운송 물량이 개방됨에 따라, FOB 비용 절감과 무연탄 시장으로공급량 확대가 기대됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the anthracite market size was valued at USD 123.24 billion in 2025 and is estimated to grow from USD 128.55 billion in 2026 to reach USD 158.75 billion by 2031, at a CAGR of 4.31% during the forecast period (2026-2031).

This report is Segmented by Grade (Standard Grade, Ultra-High Grade (UHG), and Calcined and Electrically-Calcined Grade), Application (Metallurgy, Water and Waste-Water Filtration, and More), End-User Industry (Steel and Metallurgy, Chemicals and Petrochemicals, Water Treatment Utilities, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Anthracite Market Trends and Insights

Mandates for Ultra-Low-Ash Carbon Additives in Green-Steel Processes

Steelmakers moving toward hydrogen DRI and electric arc furnaces need carbon additives with less than 8% ash and below 0.4% sulfur to minimize slag volumes and maintain bath chemistry. Recent acquisitions in Pennsylvania explicitly target these ultra-high-grade deposits to supply U.S. and European EAF expansions. China's plan to raise EAF share to 20% by 2030 intensifies global competition for low-volatile feedstocks, sustaining premium pricing even as mid-grade thermal anthracite faces substitution from natural-gas DRI and bio-carbon.

Municipal Shift to Dual-Media (Anthracite + Sand) Filtration Beds

North American and European utilities are retrofitting conventional sand filters with a coarse anthracite cap that extends run length up to 50% and cuts backwash costs. Sacramento's 2025 contract amendment and the Water Research Foundation's USD 500,000 PFAS project underscore the long-cycle, specification-driven nature of this demand. The operational savings shield procurement budgets from price shocks, anchoring a resilient slice of the anthracite market.

Petroleum-Coke and Bio-Carbon Price Discounting

High-sulfur U.S. Gulf Coast petcoke has traded as low as USD 60 per tonne in 2024-2026, slicing into anthracite's share of cement kilns and industrial boilers. Pilot-scale bio-carbon trials in Swedish EAFs promise net-zero emissions and could accelerate displacement if supply chains mature. Producers counter by lengthening contract tenors and highlighting anthracite's low ash and volatile-matter specs, where quality, not price, governs adoption.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Electrically-Calcined Anthracite in Li-Ion Anodes

- High-Density Carbon-Brick Demand from Refractory Retrofits

- Seaborne Freight-Rate Volatility and Red-Sea Rerouting Premiums

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard grade retained 47.12% share of the anthracite market in 2025, buoyed by traditional water-treatment, residential heating, and mid-tier metallurgy demand. The sub-segment's margin, however, narrowed as petcoke undercut it in cement kilns and boilers. By contrast, calcined and electrically-calcined grades are forecast to rise at a 5.12% CAGR through 2031, capturing lithium-ion, sodium-ion, and fuel-cell anode orders that value fixed-carbon levels above 95%. Early-stage supply agreements between Chinese cell makers and Pennsylvanian and Siberian producers point to steady uptake that will lift the overall anthracite market size allocated to calcined grades during the forecast window.

Ultra-High Grade (UHG) anthracite, defined by ≥92% fixed carbon and ≤5% volatiles, sits at the apex of the value ladder and trades at premiums of 20-40% over Standard Grade. Menar's Springlake Colliery purchase in 2025 added 720,000 tons per year of export-quality UHG material to global supply. Tight spec ranges make UHG indispensable in ferroalloy reduction and EAF injection, safeguarding a niche that absorbs freight shocks and regulatory costs better than lower-grade peers.

Geography Analysis

Asia-Pacific dominated the anthracite market with 53.24% of 2025 demand and will post a 4.47% CAGR through 2031, propelled by China's coal-to-chemicals rollouts and India's 1 billion-tonne production target for FY 2028-29. China Shenhua's restructuring, adding 13 subsidiaries for USD 35 billion, secures logistics and power assets that streamline supply from mine to port while expanding reserves by 25%. ASEAN states, notably Indonesia and Vietnam, continue to sanction coal-fired power and clinker capacity where imported anthracite's high calorific value and low impurity profile confer advantages over domestic lignite.

North America's anthracite market leans on Pennsylvania's century-old basin, where Delta Dunia's 2024 purchase of Atlantic Carbon Group united four ultra-premium mines under a USD 122.4 million umbrella. Exports to Europe and Asia have expanded at double-digit rates since 2014, reflecting points of differentiation in volatile-matter content and low sulfur. Domestic thermal demand wanes as renewables and cheap gas capture utility capacity, but the filter-media and specialty-carbon niches sustain baseline throughput.

Europe witnesses contracting thermal demand yet retains a vibrant specialty segment. The EU's Carbon Border Adjustment Mechanism nudges importers toward certified-low-emission cargoes, opening space for U.S. and South African suppliers able to document mine-site efficiencies. Eastern European district heating and Nordic water-treatment plants continue spot purchases, but long-run volumes hinge on the pace of coal phase-out policies. South America, led by Brazil, oscillates with currency swings and freight costs; Australian cargoes surged to 30% share in 2025-2026 after Russian supply faced geopolitical barriers. Africa's epicenter is South Africa, where Menar's expansion gives the region an export-oriented, ultra-high-grade anchor, even as Transnet reforms open third-party rail slots that could lower FOB costs and grow volumes into the anthracite market.

- Atlantic Carbon Group

- Blaschak Anthracite

- BUMA International Group

- Carbones Holding GmbH

- CHINA SHENHUA

- Coal India Limited

- Feishang Anthracite Resources Limited

- Guess & Co

- JINERGY

- Lehigh Anthracite

- Reading Anthracite Company

- Sadovaya Group

- Sibanthracite Group

- Xcoal Energy & Resources

- Yanzhou Coal Mining Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandates for ultra-low-ash carbon additives in green-steel processes

- 4.2.2 Municipal shift to dual-media (anthracite + sand) filtration beds

- 4.2.3 Growth of electrically-calcined anthracite in Li-ion anodes

- 4.2.4 High-density carbon-brick demand from refractory retrofits

- 4.2.5 Autonomous long-wall mining boosting cost-competitiveness

- 4.3 Market Restraints

- 4.3.1 Petroleum-coke and bio-carbon price discounting

- 4.3.2 Seaborne freight-rate volatility and Red-Sea rerouting premiums

- 4.3.3 Impending EU Carbon-Border Adjustment on embedded coal carbon

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Standard Grade

- 5.1.2 Ultra-High Grade (UHG)

- 5.1.3 Calcined and Electrically-Calcined Grade

- 5.2 By Application

- 5.2.1 Metallurgy (Steel, Ferro-alloys, Refractories)

- 5.2.2 Water and Waste-Water Filtration

- 5.2.3 Thermal Power Generation and CHP

- 5.2.4 Chemical Feedstock and Carbon Products

- 5.2.5 Other Applications (Ceramics, Fuel Cells, etc.)

- 5.3 By End-user Industry

- 5.3.1 Steel and Metallurgy

- 5.3.2 Chemicals and Petrochemicals

- 5.3.3 Water Treatment Utilities

- 5.3.4 Energy and Power

- 5.3.5 Other End-user Industries (Construction Materials, Carbon Products, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Atlantic Carbon Group

- 6.4.2 Blaschak Anthracite

- 6.4.3 BUMA International Group

- 6.4.4 Carbones Holding GmbH

- 6.4.5 CHINA SHENHUA

- 6.4.6 Coal India Limited

- 6.4.7 Feishang Anthracite Resources Limited

- 6.4.8 Guess & Co

- 6.4.9 JINERGY

- 6.4.10 Lehigh Anthracite

- 6.4.11 Reading Anthracite Company

- 6.4.12 Sadovaya Group

- 6.4.13 Sibanthracite Group

- 6.4.14 Xcoal Energy & Resources

- 6.4.15 Yanzhou Coal Mining Company Limited

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Surging Clean-fuel Demand across Emerging APAC Economies