|

시장보고서

상품코드

2062100

펜타클로로페놀 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Pentachlorophenol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

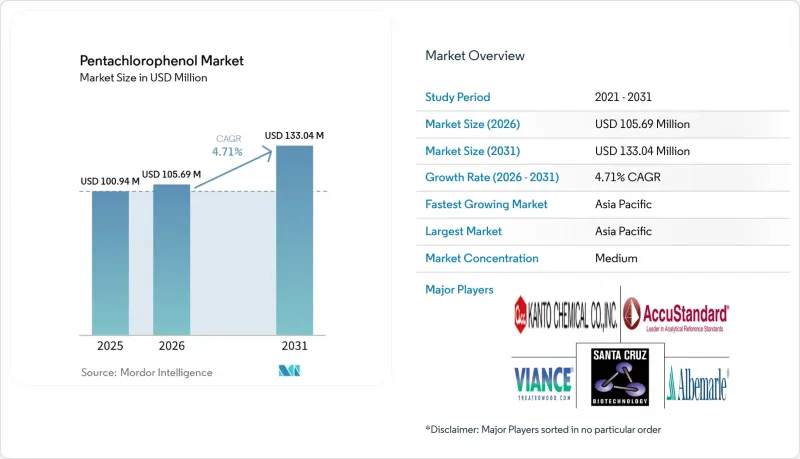

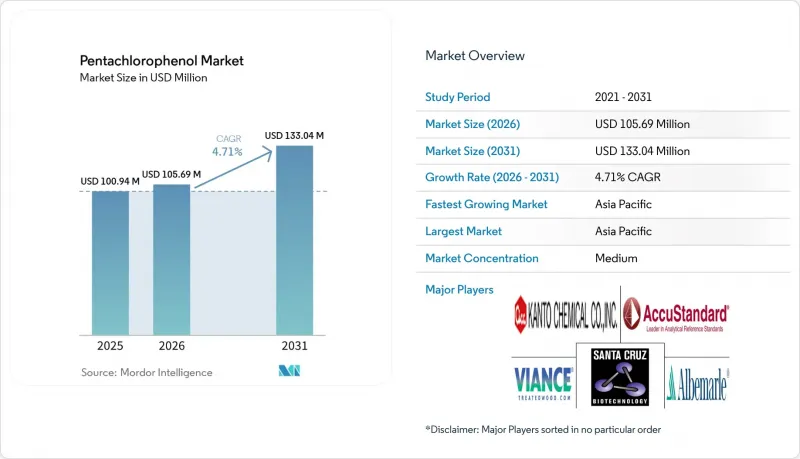

Mordor Intelligence에 의하면, 펜타클로로페놀 시장 규모는 2025년 1억 94만 달러, 2026년 1억 569만 달러에서 2031년까지 1억 3,304만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 4.71%를 나타낼 것으로 예측됩니다.

본 보고서는 등급(산업용 등급 및 분석용 등급), 용도(목재 방부제, 농약 및 제초제 등), 최종 사용자 산업(건설, 전력 사업 등), 그리고 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 펜타클로로페놀 시장 동향 및 분석

신흥국에서의 인프라 확충

아시아 전역에서 진행 중인 수백 건에 달하는 도로, 철도, 유틸리티 메가 프로젝트를 통해, 흰개미 피해가 발생하기 쉬운 기후 조건에서 수성 화학 물질보다 뛰어난 성능을 발휘하는 심층 침투형 방부제에 대한 지속적인 수요가 창출되고 있습니다. 중국의 제14차 5개년 계획에서는 4조 2,000억 달러가 교통 회랑 및 산업 단지에 투입되었으며, 환경 규제 집행이 여전히 미흡한 지역에서는 산업용 등급의 펜타클로로페놀이 계속해서 지정되어 있습니다. 인도 북부 국경 인근에서 진행 중인 34억 달러 규모의 전략적 철도 확장 계획 역시 몬순 기후 조건에서 곰팡이로 인한 부식에 견딜 수 있도록 처리된 침목에 의존하고 있습니다. 아세안 전역에서 2024년 366억 달러 규모로 전망되는 조립식 목조 주택 시장에서 습도가 높은 연안 지역의 50년 구조 보증을 충족하기 위해서는 장수명 방부제가 필수적입니다. 나프텐산 구리계 방부제 시스템은 공급 기준 가격이 약 50% 더 비싸기 때문에 가격에 민감한 건설업체들은 계속해서 펜타클로로페놀을 발주하고 있으며, 유럽과 미국에서는 규제가 단계적으로 폐지될 예정임에도 불구하고 펜타클로로페놀에 대한 시장 수요를 계속 지탱하고 있습니다.

산업용 살충제 및 제초제의 지속적인 사용

산업용 살균제는 펜타클로로페놀에 있어 틈새 시장이면서도 꾸준한 판매처를 유지하고 있습니다. 특히 발전소나 정유시설의 고온 냉각 시스템에서는 이소티아졸리논계 대체 물질이 급속히 분해되기 때문에 펜타클로로페놀 수요가 유지되고 있습니다. 남미나 동남아시아 일부 지역의 가죽 무두질 공장에서도 크롬 프리 처리법을 사용할 수 없는 경우, 보관 중인 가죽에 미생물이 번식하는 것을 막기 위해 이 화학 물질이 사용되고 있습니다. 2024년 이후 전 세계 농업용 수요량은 급격히 감소했으나, 스톡홀름 협약의 적용 대상이 아닌 지역에서는 여전히 목본성 잡초 방제를 위해 펜타클로로페놀이 함유된 제초제의 사용이 허용되고 있습니다. 이 분야는 소박하지만 예측 가능한 수익원이 되어, 시장 전체의 변동을 완화하는 역할을 하고 있습니다.

친환경 대체품의 구할 수 있는 여부

2024년 EPA의 제조 중단 조치 이후, 구리 아졸, 알칼리성 구리 4급 염, 미분화 구리 아졸 및 DCOI가 북미 주택용 목재 수요의 70% 이상을 차지하고 있습니다. 2025년 래스우드(Rasswood)사가 인수한 SiooX 등의 규산염계 시스템은 목재 표면을 광물화시켜 유해 폐기물을 발생시키지 않습니다. 이는 LEED 크레딧 요건을 충족하며, 유지 관리 비용을 고려할 때 수명 주기 비용을 절감합니다. 중국의 주요 배합 제조업체들이 나프텐산 구리의 생산 규모를 확대함에 따라 가격 프리미엄은 축소되고 있으며, 대체 움직임이 가속화되고 있습니다. 이러한 환경의 변화는 규제와 녹색 금융 기준이 일치하는 지역에서 펜타클로로페놀 시장 점유율을 잠식하고 있습니다.

부문별 분석

2025년 매출의 78.15%를 산업용 등급이 차지하고 있으며, 6-12파운드/입방피트의 유지력을 필요로 하는 전신주나 해양 말뚝 등 고하중 용도에서의 그 역할이 부각되고 있습니다. 펜타클로로페놀 부문의 우위는 기존의 가압 실린더 및 용제 회수 루프에 기인하며, 이를 수성 구리 시스템에 적용하려면 100만-300만 달러의 개조 비용이 필요하기 때문입니다. 분석용 등급 시장은 연구소, 규제 당국, 컨설팅 업체들이 EPA 메서드 8540 키트나 ppm 미만의 검출 기술을 활용한 현장 평가를 확대함에 따라 2031년까지 연평균 성장률(CAGR) 4.88%로 성장하고 있습니다. 머크 KGaA와 바이오신세(BioSynth)의 인증 표준 물질이 이러한 규정 준수 수요의 급증에 기여하고 있으며, 이 하위 부문은 2031년까지 꾸준한 성장이 예상됩니다.

EPA의 단계적 폐지 시한이 다가오고 있음에도 불구하고, 신흥 아시아 국가들은 인프라 구축을 위해 산업용 등급 제품을 계속 주문하고 있어 전 세계 판매량 감소세를 완화하고 있습니다. 그러나 인도와 중국에서는 나프텐산 구리와 산업용 펜타클로로페놀의 가격 차이가 점차 좁혀지고 있어, 이익률에 압박을 가하고 있습니다. 분석용 등급은 바로 이러한 규제 변화의 혜택을 받고 있습니다. 단계적 폐지가 진행됨에 따라 모니터링용 시약에 대한 수요가 증가하면서, 총 매출에서 펜타클로로페놀이 차지하는 업계 점유율이 확대되고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 39.22%를 차지하며, 2031년까지 연평균 성장률(CAGR) 5.16%로 성장하고 있습니다. 이는 중국의 4조 2,000억 달러 규모의 교통 인프라 확충과 인도의 전략적 철도 및 광대역 프로젝트에 힘입은 것입니다. 베트남, 인도네시아, 필리핀의 가공업체들은 풍부한 현지 목재와 낮은 규정 준수 비용의 혜택을 누리고 있으며, 이로 인해 펜타클로로페놀이 구리 아졸에 비해 가격 경쟁력을 확고히 하고 있습니다. 북미에서는 구조적인 축소 추세를 보이고 있습니다. 2024년에 발효되는 EPA(미국 환경보호청)의 제조 금지 조치로 인해 신규 공급이 중단되며, 2027년 2월까지는 기존 재고만 사용할 수 있습니다. 캘리포니아주 유틸리티위원회는 2028년까지 신규 오염화페놀 처리 전주의 사용을 금지할 방침이며, 이에 따라 시장 규모가 축소되는 추세가 가속화될 것으로 보입니다.

유럽의 상황은 복잡합니다. 크레오소트 사용 중단으로 인해 처리 업체들이 나프테네이트 구리로 전환하는 한편, 펜타클로로페놀로의 전환도 진행되면서 일시적으로 수요가 증가하고 있지만, 소비재에 적용되는 REACH 규정의 5ppm 상한선이 장기적인 성장을 억제하고 있습니다. 남미, 중동 및 아프리카에서는 규제 집행이 완만하고 비용에 대한 민감도가 높아, 수요는 분산되어 있지만 여전히 견조한 임베디드니다. 그러나 그린 파이낸스 기준이 강화됨에 따라 방부 처리 목재의 수출이 제한되어, 2030년 이후에는 해당 지역 시장이 위축될 가능성이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the pentachlorophenol market size is projected to expand from USD 100.94 million in 2025 and USD 105.69 million in 2026 to USD 133.04 million by 2031, registering a CAGR of 4.71% between 2026 to 2031.

This report is Segmented by Grade (Industrial Grade and Analytical Grade), Application (Wood Preservatives, Pesticides and Herbicides, and More), End-User Industry (Construction, Power Utilities, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Pentachlorophenol Market Trends and Insights

Expanding Infrastructure in Emerging Economies

Hundreds of road, rail, and utility mega-projects in Asia are unlocking sustained demand for deep-penetration preservatives that outperform water-borne chemistries in termite-prone climates. China's 14th Five-Year Plan channels USD 4.2 trillion into transportation corridors and industrial parks, a pipeline that continues to specify industrial-grade pentachlorophenol where environmental enforcement remains patchy. India's USD 3.4 billion strategic railway build-out near its northern border similarly leans on treated sleepers that resist fungal decay under monsoon exposure. Across ASEAN, prefab timber housing valued at USD 36.6 billion in 2024 relies on long-life preservatives to satisfy 50-year structural warranties in humid coastal markets. Because copper-naphthenate systems cost about 50% more on a delivered basis, price-sensitive contractors continue to order pentachlorophenol, propping up pentachlorophenol market demand even as regulatory sunsets loom in the West.

Continued Use in Industrial Pesticides and Herbicides

Industrial biocides remain a niche but resilient outlet for pentachlorophenol, especially in high-temperature cooling systems at power plants and refineries where isothiazolinone alternatives break down rapidly. Leather tanneries in South America and parts of Southeast Asia also employ the chemical to prevent microbial attack on hides during storage when chromium-free processes are unavailable. Although global agricultural volumes have fallen sharply post-2024, jurisdictions outside the Stockholm Convention still allow pentachlorophenol herbicide formulations for woody weed control. The segment anchors a predictable if modest revenue stream that tempers overall market volatility.

Availability of Eco-Friendly Alternatives

Copper azole, alkaline copper quaternary, micronized copper azole, and DCOI have captured more than 70% of North American residential-lumber demand since the 2024 EPA manufacturing cutoff. Silicate-based systems such as SiooX, acquired by Russwood in 2025, mineralize the wood surface and generate no hazardous waste, aligning with LEED credits and lowering life-cycle costs once tracking fees are considered. As large Chinese formulators scale copper naphthenate, price premiums shrink, accelerating substitution. This eco-pivot slices into the pentachlorophenol market share in regions where regulations and green-finance criteria converge.

Other drivers and restraints analyzed in the detailed report include:

- Creosote Withdrawal Driving Substitution

- Rural Broadband Roll-Outs Using Timber Masts

- Rising Disposal Costs for Hazardous Treated Wood

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Industrial grade generated 78.15% of 2025 revenue, underscoring its role in high-load applications like utility poles and marine pilings that demand 6-12 lb/ft3 retention rates. The pentachlorophenol segment's advantage stems from legacy pressure cylinders and solvent-recovery loops that would require USD 1-3 million in retrofits to handle aqueous copper systems. Analytical grade is rising at a 4.88% CAGR through 2031 as laboratories, regulators, and consultants expand site assessments using EPA Method 8540 kits and sub-ppm detection technologies. Certified reference materials from Merck KGaA and Biosynth support this compliance boom, positioning the sub-segment for steady growth through 2031.

Despite EPA phase-out deadlines, emerging Asia keeps ordering industrial grade for infrastructure corridors, cushioning global volume declines. However, price parity between copper naphthenate and industrial pentachlorophenol is approaching in India and China, pressuring margins. Analytical grade benefits from that very regulatory churn; as phase-outs bite, demand for monitoring reagents intensifies, expanding its pentachlorophenol industry share within total revenue.

Geography Analysis

Asia-Pacific accounted for 39.22% of 2025 revenue and is advancing at a 5.16% CAGR through 2031, underpinned by China's USD 4.2 trillion transport build-out and India's strategic rail and broadband projects. Treaters in Vietnam, Indonesia, and the Philippines benefit from abundant local timber and lower compliance costs, locking in pentachlorophenol's price edge over copper azole. North America is in structural decline; the EPA manufacturing ban, effective 2024, halts new supply, and only stockpiles may be used until February 2027. California's Public Utilities Commission is set to ban new pentachlorophenol poles by 2028, accelerating contraction.

Europe exhibits a mixed profile: creosote withdrawal temporarily lifts demand as treaters switch to pentachlorophenol while upgrading for copper naphthenate, but REACH limits of 5 ppm in consumer articles cap long-term growth. South America and the Middle-East and Africa offer fragmented yet resilient demand thanks to lax enforcement and cost sensitivity; however, rising green-finance criteria may curtail exports of treated wood, narrowing the market in these regions post-2030.

- AccuStandard

- Albemarle Corporation

- Biosynth

- Cabot Corporation

- Chem Service Inc.

- KANTO KAGAKU

- Koppers Inc.

- Merck KGaA

- Pure Water Products, LLC

- Santa Cruz Biotechnology Inc.

- Troy Corporation

- Viance

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding infrastructure in emerging economies

- 4.2.2 Continued use in industrial pesticides and herbicides

- 4.2.3 Creosote withdrawal driving substitution

- 4.2.4 CLT structural panels requiring deep-penetration preservatives

- 4.2.5 Rural broadband roll-outs using timber masts

- 4.3 Market Restraints

- 4.3.1 Availability of eco-friendly alternatives

- 4.3.2 ESG-driven insurer and investor restrictions on utilities

- 4.3.3 Rising disposal costs for hazardous treated wood

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Industrial Grade

- 5.1.2 Analytical Grade

- 5.2 By Application

- 5.2.1 Wood Preservatives

- 5.2.2 Pesticides and Herbicides

- 5.2.3 Leather Preservation

- 5.2.4 Industrial Biocides

- 5.2.5 Other Applications (e.g., Antimicrobial Agents)

- 5.3 By End-user Industry

- 5.3.1 Construction

- 5.3.2 Power Utilities (Poles and Cross-arms)

- 5.3.3 Agriculture and Forestry

- 5.3.4 Leather and Textiles

- 5.3.5 Other End-user Industries (Coating, Pulp, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AccuStandard

- 6.4.2 Albemarle Corporation

- 6.4.3 Biosynth

- 6.4.4 Cabot Corporation

- 6.4.5 Chem Service Inc.

- 6.4.6 KANTO KAGAKU

- 6.4.7 Koppers Inc.

- 6.4.8 Merck KGaA

- 6.4.9 Pure Water Products, LLC

- 6.4.10 Santa Cruz Biotechnology Inc.

- 6.4.11 Troy Corporation

- 6.4.12 Viance

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment