|

시장보고서

상품코드

2062101

미분화 금속 분말 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Atomizing Metal Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

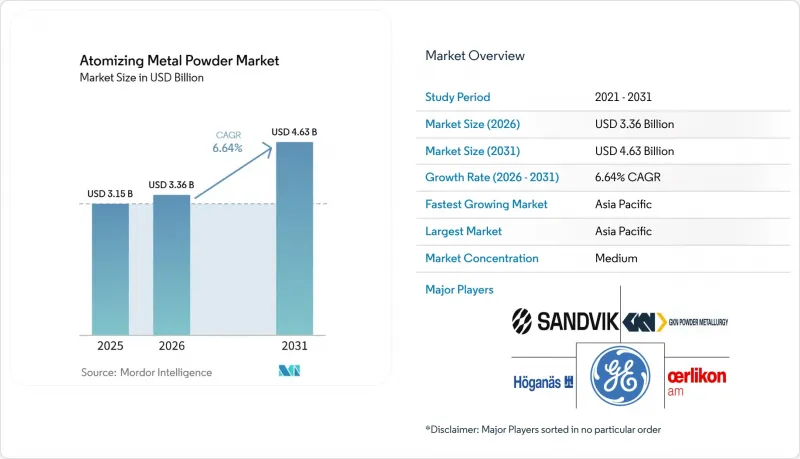

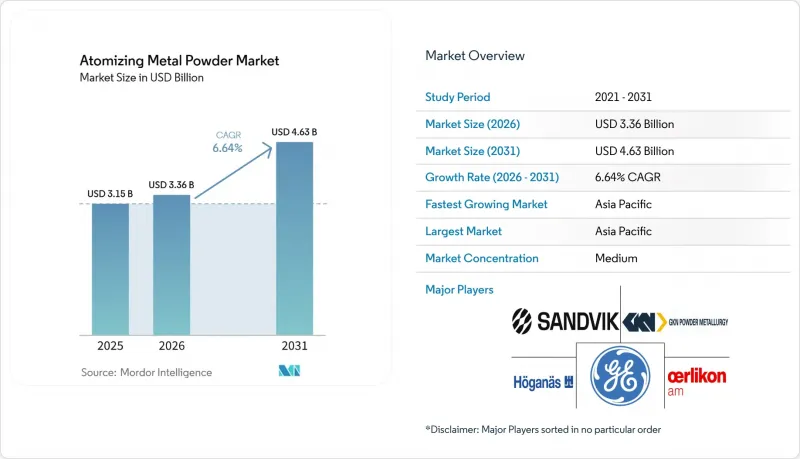

Mordor Intelligence에 의하면, 미분화 금속 분말 시장 규모는 2025년 31억 5,000만 달러로 평가되었고, 2026년 33억 6,000만 달러로 추정되고, 2031년까지 46억 3,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 6.64%를 나타낼 것으로 예측됩니다.

본 보고서는 분무 공정별(가스 분무 등), 금속 유형별(스테인리스 스틸 분말 등), 용도별(적층 가공 등), 최종 사용자 산업별(에너지, 자동차 및 전기차 제조 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 미분화 금속 분말 시장 동향 및 분석

항공우주 및 전기차(EV) 분야의 고성능 PM 부품 수요 증가

민간 항공기 제조업체는 GE9X 터보팬 엔진에 300개 이상의 적층 가공 부품을 적용하여, 이를 통해 엔진 무게를 줄이고 연료 소비량을 10% 절감하고 있습니다. 미국의 가스터빈 제조업체들은 최대 75%의 수소 혼합 연료에 대한 검증을 진행 중이며, 산소 함량 300ppm 미만의 기준을 충족하는 니켈 기 초합금의 분말 소비량이 증가하고 있습니다. 전기차(EV) 플랫폼에서는 kW시당 중량을 줄이기 위해 주조 브라켓을 소결강 및 알루미늄 부품으로 대체하고 있으며, 이러한 변화는 2024년 북미의 알루미늄 분말 출하량이 22.6% 급증한 점에서도 확인할 수 있습니다. 의료기기 제조업체는 2026년 1분기에만 척추 및 안면악용 티타늄 임플란트에 대한 승인을 5건 획득하며 적층 가공의 성장세를 더욱 공고히 하고 있습니다. 이러한 요인들이 복합적으로 작용하여, 분무 금속 분말 시장의 성장 전망에 약 2%의 상승 요인으로 작용하고 있습니다.

고순도 티타늄, 니켈 및 HEA 분말에 대한 수요 급증

FAA(연방항공청)의 RPD(Rapid Plasma Deposition) 티타늄 구조물 승인 및 에어버스와 GE 간의 1,000톤 규모 티타늄 원료 공급 계약은 고품질 합금이 산업 분야에서 널리 받아들여지고 있음을 입증하고 있습니다. 2025년에는 3개의 전문 공급업체가 카탈로그에 고엔트로피 합금 분말의 상용 등급을 등재함에 따라, 초음속 항공기 및 극저온 펌프용 합금 라인업이 확대되었습니다. 산드빅은 AS9100D 인증을 바탕으로 영국과 스웨덴에서 생산 능력을 확대하고, 산소 함량이 제어된 니켈 및 티타늄 등급 제품을 공급했습니다. TEKNA의 플라즈마 아토마이징 공법을 통한 티타늄 생산량은 2025년 말까지 누적 1,000톤을 넘어설 전망이며, 이는 해당 기술의 성숙도를 입증하고 있습니다. 이러한 합금에 대한 수요는 금속 분말 분무 시장의 성장률을 1.5%p 끌어올리고 있습니다.

입자 크기 분포, 형태, 유동성에 대한 엄격한 품질 관리

ISO 52907 및 새로운 ASTM 분말 분석 표준에 따르면, 모든 배치에 대해 레이저 회절법, 홀 플로우 시험, CT 이미징을 통과해야 하며, 이로 인해 품질 관리 비용이 톤당 최대 1,500달러 증가했습니다. 위성 입자는 유동성을 최대 30%까지 저하시키기 때문에 추가적인 체질 공정이 필요하며, 이로 인해 수율이 85%에서 65%로 떨어지게 되어 생산 능력의 전략적 제한으로 이어집니다. 이는 2024년 호가나스가 정격 생산 능력 50만 톤에 비해 41만 2,000톤을 생산한 사례에서 볼 수 있듯이 그렇습니다. 같은 해, OEM(원청 브랜드 제조업체)이 공급업체의 재현성 향상이 입증될 때까지 발주를 연기함에 따라 북미로의 원료 출하량은 10% 감소했습니다. 이러한 요인으로 인해 예측 연평균 성장률(CAGR)은 0.7% 하락했습니다.

부문별 분석

가스 분무법은 비용 면에서의 우위 덕분에 2025년 생산량의 57.12%를 계속 차지했습니다. 한편, 수분 분무법은 가격에 민감한 철분이나 공구강 분말 수요에 부응했습니다. 플라즈마 분무법은 항공우주 및 의료 분야 구매자들이 300ppm 미만의 산소 농도를 요구하고 있어 연평균 성장률(CAGR) 6.88%로 증가할 것으로 예상되며, 이는 전체 금속 분말 분무 시장의 평균 성장률을 상회할 전망입니다.

플라즈마 공법이 지닌 비표준 입도 조절의 유연성은 PyroGenesis사가 45-106 마이크로미터 크기의 Ti-6Al-4V 원료에 대해 보잉사의 인증을 획득함으로써 입증되었습니다. 가스 분무법은 스테인리스 스틸이나 알루미늄 등급에서 여전히 필수적이지만, 품질 규격의 강화와 헬륨 가격의 안정화에 따라 금속 분말 분무 시장에서의 그 우위는 점차 약화될 것입니다.

2025년 매출에서 스테인리스 스틸 분말이 30.11%를 차지했으나, 티타늄 및 니켈 초합금은 2031년까지 연평균 성장률(CAGR) 7.03%로 시장 점유율을 확대해 나갈 전망입니다. GE Additive가 에어버스사와 체결한 다년 계약에 따라 1,000톤의 티타늄 분말을 공급함에 따라, 티타늄 부문만으로도 분무 금속 분말 시장 규모가 크게 성장할 것으로 전망됩니다.

니켈계 분말은 6K-지멘스와의 제휴를 통해 91%의 탄소 배출 감축을 달성했으며, 2031년까지 두 자릿수 시장 점유율을 달성할 것으로 전망됩니다. 스테인리스 스틸은 316L 및 17-4PH 등급이 비용 및 내식성 요건을 충족하는 자동차용 소결 부품 분야에서 확고한 입지를 유지하고 있으나, 예측 기간 동안 분무 금속 분말 시장에서의 점유율은 하락할 가능성이 있습니다. 고엔트로피 합금은 여전히 틈새 시장이지만, 높은 가격을 유지하고 있어 취급량이 적더라도 수익을 뒷받침하고 있습니다.

지역별 분석

아시아태평양은 2025년 분무 금속 분말 시장의 39.56%를 차지한 것으로 평가되었으며, CNPC Powder, Avimetal, Epson Atmix가 2026년 말까지 총 1만 톤 이상의 신규 생산 능력을 추가할 예정인 만큼, 2031년까지 연평균 성장률(CAGR) 7.12%로 급성장하고 있습니다. 중요 광물에 대한 각국의 수출 규제로 인해 해당 지역에서는 자체 재활용 공장 건설이 진행되고 있으나, 헬륨 조달 및 수소 대응 품질 기준에 대해서는 여전히 과제가 남아 있습니다.

북미에서는 전기차 수요를 배경으로 알루미늄 분말 출하량이 22.6% 급증했으며, 방위 분야의 기계 가공 수요로 인해 텅스텐 카바이드 수요도 증가했습니다. 우크라이나의 직접 투자를 바탕으로 Velta사가 미국의 티타늄 제조 시설에 6,000만 달러를 투자한 것은 지정학적 공급 리스크를 줄이기 위한 전략적인 생산 재편을 반영한 것입니다. 6K Additive사가 연간 생산량을 200톤에서 1,000톤으로 확대하기 위해 받은 '국방생산법 제3조'에 근거한 2,340만 달러의 보조금은 연방 정부가 국내 니켈 합금 및 티타늄 분말 생산 능력을 우선시하고 있음을 강조하고 있습니다.

2025년 유럽 시장 점유율은 15개 생산 거점에 걸친 호가나스의 연간 50만 톤 생산 능력에 힘입어 유지되고 있으며, 2026년까지 화석 석탄의 20%를 바이오차으로 대체하기 위한 인프라 투자와 2026년 중국 내 생산 거점 이전 완료가 예정되어 있습니다. 샌드빅(Sandvik)이 영국 니스에 가스 분무탑 2기를 추가로 가동하고, 스웨덴 산드비켄에 AS9100D 인증을 획득한 티타늄 및 니켈 합금 전용 신규 공장을 건설함에 따라, 유럽 내 항공우주 및 의료기기 OEM 제조업체에 서비스를 제공할 수 있는 체제가 갖춰졌습니다.

남미와 중동 및 아프리카의 합산 시장 점유율은 비교적 작지만, 자동차 및 석유화학 분야 수요는 평균을 상회하고 있으며, 해당 지역의 재활용 공급망이 성숙해지면 급속히 추격자로 부상할 가능성이 있음을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the atomizing metal powder market size is projected to expand from USD 3.15 billion in 2025 and USD 3.36 billion in 2026 to USD 4.63 billion by 2031, registering a CAGR of 6.64% between 2026 and 2031.

This report is Segmented by Atomization Process (Gas Atomization, and More), Metal Type (Stainless Steel Powders, and More), Application (Additive Manufacturing, and More), End-User Industry (Energy, Automotive and EV Manufacturing, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Atomizing Metal Powder Market Trends and Insights

Expanding Demand for High-Performance PM Parts in Aerospace and EVs

Commercial airframe builders deploy more than 300 additive-manufactured components in the GE9X turbofan, cutting engine weight and lowering fuel burn by 10%. United States gas-turbine makers validate hydrogen blends up to 75%, raising consumption of nickel-based superalloy powders qualified to sub-300 ppm oxygen limits. Electric-vehicle platforms replace cast brackets with sintered steel and aluminum parts to trim mass per kilowatt-hour, a change mirrored in the 22.6% jump in North American aluminum powder shipments during 2024. Medical suppliers received five titanium spinal and maxillofacial implant clearances in Q1 2026 alone, reinforcing additive-manufacturing traction. These combined pulls add almost two percentage-points to the Atomizing metal powder market growth outlook.

Surging Need for Advanced Titanium, Nickel, and HEA Powders

FAA (Federal Aviation Administration) clearance of rapid-plasma-deposited titanium structures and Airbus-GE supply deals for 1,000 tons of titanium feedstock confirm industrial acceptance of premium alloys. Commercial volumes of high-entropy alloy powders entered the catalogs of three specialty suppliers in 2025, widening alloy menus for hypersonic vehicles and cryogenic pumps. Sandvik expanded capacity in the United Kingdom and Sweden, under AS9100D certification, to deliver oxygen-controlled nickel and titanium grades. Plasma-atomized titanium production exceeded 1,000 tons cumulative at TEKNA by late 2025, underscoring maturity. Demand for these alloys lifts the Atomizing metal powder market trajectory by 1.5 percentage-points.

Stringent QC on Particle-Size Distribution, Morphology, and Flowability

ISO 52907 and new ASTM powder-analysis standards require every batch to pass laser diffraction, Hall flow, and CT imaging, raising quality-control overhead by up to USD 1,500 per tonne. Satellite particles reduce flowability by up to 30%, forcing extra sieving that cuts yield from 85% to 65% and drives strategic throttling of capacity, as seen when Hoganas produced 412,000 tons against 500,000 tons nameplate in 2024. North American feedstock shipments fell 10% the same year because OEMs (original equipment manufacturers) delayed orders until suppliers proved tighter reproducibility. These requirements shave 0.7 percentage-points off forecast CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Decentralized Micro-Atomization for On-Demand Supply

- Ultra-Low-Oxygen Powders for Hydrogen Turbines and Energy Systems

- Helium Price Volatility for Plasma and Gas Atomization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gas atomization retained 57.12% of 2025 volume owing to cost advantages, while water atomization served price-sensitive iron and tool-steel powders. Plasma atomization is projected to rise at a 6.88% CAGR, outstripping the Atomizing Metal Powder market average because aerospace and medical buyers demand oxygen below 300 ppm.

Plasma's non-standard cut flexibility was proven when PyroGenesis won Boeing qualification for 45-106 µm Ti-6Al-4V feedstock. Gas atomization remains critical for stainless steel and aluminum grades, but its dominance in the Atomizing metal powder market will gradually erode as quality specifications tighten and helium pricing stabilizes.

Stainless steel powders commanded 30.11% of 2025 sales, yet titanium and nickel superalloys will capture incremental share at a 7.03% CAGR through 2031. The titanium category alone is set to climb substantially in the Atomizing Metal Powder market size as GE Additive supplies 1,000 tons of titanium powder to Airbus under a multi-year deal.

Nickel-based powders benefit from the 6K-Siemens alliance, delivering 91% carbon cuts and will likely reach double-digit share before 2031. Stainless steel keeps a foothold in automotive sintered parts where 316L and 17-4PH grades meet cost and corrosion targets, but its Atomizing metal powder market share may dip below over the forecast horizon. High-entropy alloys remain niche but command premium pricing that bolsters revenue even at low tonnage.

Geography Analysis

Asia-Pacific dominated 39.56% of the Atomizing Metal Powder market in 2025 and is racing ahead at a 7.12% CAGR to 2031 as CNPC Powder, Avimetal, and Epson Atmix together add more than 10,000 tons of new capacity by end-2026. Local export controls on critical minerals push the region to build in-house recycling plants, yet helium sourcing and hydrogen-ready quality standards remain open challenges.

In North America, aluminum powder volumes surged 22.6% on electric-vehicle demand, and tungsten carbide climbed on defense machining requirements. Velta's USD 60 million investment in a United States titanium manufacturing facility, backed by Ukrainian foreign direct investment, reflects strategic reshoring to reduce geopolitical supply risk. 6K Additive's USD 23.4 million Defense Production Act Title III grant to scale from 200 metric tons per year to 1,000 metric tonnes per year underscores federal prioritization of domestic nickel-alloy and titanium powder capacity.

Europe's market share in 2025 is anchored by Hoganas' 500,000 tons per year capacity across 15 production sites, with biochar infrastructure investment to replace 20% of fossil coal by 2026 and China relocation completion in 2026. Sandvik's commissioning of two additional gas-atomization towers at Neath, United Kingdom, and a new plant in Sandviken, Sweden, for titanium and nickel alloys under AS9100D certification positions Europe to serve aerospace and medical-device OEMs.

South America and the Middle East-Africa together account for a relatively small market share yet display above-average automotive and petrochemical demand, suggesting a potential fast-follower pattern once regional recycling supply chains mature.

- 6K Inc.

- AMETEK Specialty Metal Powders

- Aubert & Duval

- CRS Holdings, LLC

- EOS GmbH

- Eramet-MATI Shanghai

- ERASTEEL

- Forged Solutions Group

- General Electric Company

- GKN Powder Metallurgy

- Hoganas

- Metalysis

- Oerlikon Management AG

- PyroGenesis Additive

- Rio Tinto

- Sandvik AB

- TEKNA

- Xi'an Sailong Metal

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding demand for high-performance PM parts (aerospace, EV)

- 4.2.2 Surging need for advanced alloys (Ti, Ni-based, HEA)

- 4.2.3 Decentralized micro-atomization for on-demand supply

- 4.2.4 Ultra-low-oxygen powders for hydrogen turbines and energy

- 4.2.5 Battery-grade spherical Cu and AI powders for Li-ion and solid-state cells

- 4.3 Market Restraints

- 4.3.1 Stringent QC on PSD, morphology and flowability

- 4.3.2 Helium supply price volatility for plasma/gas atomization

- 4.3.3 Limited closed-loop recycling for reactive/critical powders

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Atomization Process

- 5.1.1 Gas Atomization

- 5.1.2 Plasma Atomization

- 5.1.3 Water Atomization

- 5.1.4 Centrifugal Atomization

- 5.1.5 Other Methods (e.g., ultrasonic)

- 5.2 By Metal Type

- 5.2.1 Stainless Steel Powders

- 5.2.2 Titanium and Superalloy Powders

- 5.2.3 Aluminum Powders

- 5.2.4 Copper and Copper-Alloy Powders

- 5.2.5 Nickel-based Alloys

- 5.2.6 Other Metals and Alloys

- 5.3 By Application

- 5.3.1 Additive Manufacturing (AM/3DP)

- 5.3.2 Powder-Metallurgy Components/Parts

- 5.3.3 Cutting Tools and Wear Parts

- 5.3.4 Coatings and Thermal-Spray Materials

- 5.3.5 Other Industrial Applications

- 5.4 By End-user Industry

- 5.4.1 Aerospace and Defense

- 5.4.2 Automotive and EV Manufacturing

- 5.4.3 Medical and Dental Devices

- 5.4.4 Industrial Machinery and Tooling

- 5.4.5 Energy (turbines, oil and gas)

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 6K Inc.

- 6.4.2 AMETEK Specialty Metal Powders

- 6.4.3 Aubert & Duval

- 6.4.4 CRS Holdings, LLC

- 6.4.5 EOS GmbH

- 6.4.6 Eramet-MATI Shanghai

- 6.4.7 ERASTEEL

- 6.4.8 Forged Solutions Group

- 6.4.9 General Electric Company

- 6.4.10 GKN Powder Metallurgy

- 6.4.11 Hoganas

- 6.4.12 Metalysis

- 6.4.13 Oerlikon Management AG

- 6.4.14 PyroGenesis Additive

- 6.4.15 Rio Tinto

- 6.4.16 Sandvik AB

- 6.4.17 TEKNA

- 6.4.18 Xi'an Sailong Metal

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment