|

시장보고서

상품코드

2062102

고체 유황 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Solid Sulphur - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

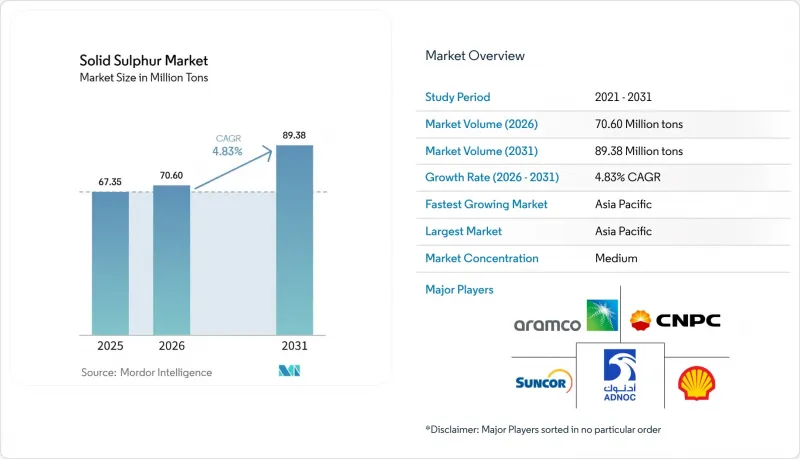

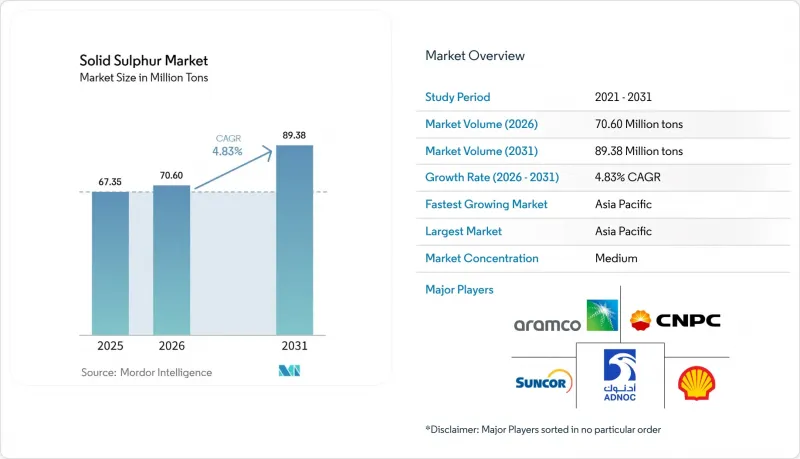

Mordor Intelligence에 의하면, 고체 유황 시장 규모는 2025년 6,735만 톤으로 평가되었습니다. 2026년 7,060만 톤으로부터, 2031년까지 8,938만 톤으로 확대되어 2026-2031년에 걸쳐 CAGR은 4.83%를 나타낼 것으로 예측됩니다.

본 보고서는 형태(입상 유황, 덩어리 유황, 분말 유황), 용도(비료, 고무 가공, 광업 및 야금, 석유 정제, 화학제품 제조, 농약·살균제, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

세계의 고체 유황 시장 동향 및 분석

초저유황 연료 규제의 확대

선박용 및 육상용 디젤 연료에 대한 규제가 강화됨에 따라, 정유사들은 탈황 설비를 추가하거나 업그레이드할 수밖에 없게 되었고, 더 깨끗한 연료를 판매하는 한편 고체 유황의 생산량은 급격히 증가했습니다. KIPIC의 알-주르 정유시설는 2024년부터 2025년에 걸쳐 73만 2,000톤의 입상 유황을 생산하여 저유황 연료유 생산을 가능하게 함으로써, 연간 1억 달러의 비용 절감을 실현했습니다. 저유황 연료에 대한 수요가 증가함에도 불구하고 원소 유황공급량이 늘어나는 이러한 역설적인 상황은 비료 수요가 둔화될 때마다 주기적으로 가격 하락을 초래하는 요인이 됩니다. 이에 반해, 북미의 주요 기업들은 클라우스 공정 설비의 최적화에 힘써, 현재는 황화수소의 99% 이상을 회수할 수 있게 되었습니다. 이로 인해 과거에는 부담이었던 요소가 수익원으로 전환되었으나, 자본 집약적인 특성상 이 방식은 통합형 기업으로 한정됩니다.

비철금속 제련 능력 확대

구리, 니켈, 아연 프로젝트로 인해 황산 사용량은 계속 증가하고 있습니다. 인도네시아의 배터리용 니켈 HPAL 공장은 황 원료의 약 75%를 중동에서 수입하고 있어, 페르시아만 지역의 물류 지연이 발생할 때마다 전 세계의 수급 균형이 위태로워집니다. 칠레의 구리 침출 사업에서는 2025년에 820만 톤의 황산이 소비되었는데, 이는 광석 품위의 저하에 따라 급격히 증가한 것입니다. 한편, 페루의 티아 마리아 프로젝트는 2027년 이후 국내 황산 수요를 연간 80만 톤 증가시킬 것으로 전망됩니다. 중앙아프리카의 구리 지대에서는 코발트와 산화구리의 침출 처리를 위해 연간 200만 톤에 가까운 고체 유황을 수입하고 있으며, 호르무즈 해협에서 공급 차질이 발생할 경우 이 지역의 생산량은 영향을 받기 쉬운 상황에 놓여 있습니다.

변동이 심한 원유·천연가스의 생산량

고체 유황공급은 탄화수소 관련 활동 상황에 따라 달라집니다. 2025년, 북미의 가스 시추가 축소됨에 따라 퍼미안 분지와 마르셀러스층의 탈황 플랜트에서 생산량이 감소했습니다. 또한, 탈황 설비가 가동되지 않은 상태였음에도 불구하고, OPEC+의 감산 조치로 인해 중동산 제품공급도 부족해졌습니다. 독립계 유황 광산이 사실상 존재하지 않기 때문에 비료나 야금용 구매자가 갑자기 주문량을 늘려도 시장은 신속하게 대응할 수 없어, 만성적인 수급 불균형이 고착화되어 있습니다.

부문별 분석

2025년, 입상 등급이 고체 유황 시장 점유율의 57.11%를 차지했습니다. 이는 비료 혼합 업체들이 분진 발생이 없는 공기 이송에 적합한 2-6mm 크기의 구형 입자를 선호하기 때문입니다. IPCO의 싱글 패스 드럼 기술은 액체 유황을 냉각 및 코팅하여 SUDIC 기준을 충족하는 과립으로 가공함으로써, 황화수소 노출과 관련된 더욱 엄격한 산업위생 기준을 충족하고 있습니다.

분말 형태의 제품은 현재 시장 점유율이 낮지만, 미세 분말 형태의 살균제 스프레이와 높은 표면적이 필요한 역가황용 원료에 힘입어 2031년까지 연평균 성장률(CAGR) 5.25%를 나타낼 것으로 전망됩니다. 포도밭에서는 유황 분말을 유기 실리콘계 계면활성제와 혼합하면 흰가루병 방제 효과가 향상된다는 보고가 있어, 이에 따라 특수 작물 재배에 이 방법이 널리 채택되고 있습니다. 덩어리 형태의 유황은 용해 속도가 느린 특성 덕분에 알칼리성 토양에 적합한 틈새 용도로 여전히 사용되고 있지만, 불규칙한 입자 크기로 인해 자동 혼합이 어려워 향후 시장 점유율은 축소될 전망입니다.

지역별 분석

아시아태평양은 2025년에 고체 유황 시장 점유율의 41.34%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 5.42%를 나타낼 것으로 전망됩니다. 인도네시아의 HPAL 니켈, 중국의 토양 유황 고갈, 인도의 제련소 개보수가 이 지역의 성장 동력이 되고 있습니다. 인도네시아는 유황의 75%를 중동에서 조달하고 있으며, 그 공급 균형은 페르시아만 수송 위험에 노출되어 있습니다. 중국의 황산암모늄 생산 확대에 따라 농업 종사자들은 질소 수출 할당량을 피할 수 있게 되었지만, 인도의 새로운 탈황 설비는 수입품을 국내산 제품으로 점차 대체해 나갈 전망입니다.

북미는 여전히 중요한 공급원입니다. 캐나다의 오일샌드는 2025년에 약 300만 톤을 생산하여 국내 생산량의 63%를 차지했으나, 산코사는 용융 제품과 프리일 제품으로 80만 톤 이상을 판매했습니다. 가격이 높은 수준을 유지한다면, 기존 블록을 재용해하여 2030년까지 150만 톤이 추가로 공급될 가능성이 있지만, 신규 시설이 본격적으로 가동되는 것은 2026년 이후가 될 것입니다. 미국의 생산량은 멕시코만 연안 정유시설의 가동 상황과 퍼미안 분지의 가스 시추에 좌우되기 때문에 공급은 원유와 가스 가격 변동에 민감합니다.

유럽에서는 노후화된 제련소의 폐쇄와 원유 성분의 경질화에 따라 국내 생산이 줄어들고 있습니다. 독일, 프랑스, 이탈리아는 카타르, 사우디아라비아, 러시아로부터의 수입량을 늘리고 있지만, 순환형 경제 솔루션에 대한 정책적 초점이 황계 폴리머 시범 프로젝트를 뒷받침하고 있습니다. 남미의 상황은 칠레의 구리와 브라질의 비료로 특징지어집니다. 칠레는 제련소의 가동 중단으로 인해 2025년에 380만 톤의 황산을 수입했습니다. 또한, 2025년 12월 모자이크사가 브라질에서의 SSP 생산을 중단했을 때, 황의 현물 가격이 전년 대비 3배로 급등하면서 가격 리스크가 부각되었습니다. 중동은 여전히 수출의 거점이며, ADNOC의 루와이스 터미널은 처리 능력을 하루 2만 7,000톤으로 확대했고, KIPIC의 알-주르는 2025년 1월 사상 최대인 5만 2,000톤을 선적했습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the solid sulphur market size is projected to expand from 67.35 Million tons in 2025 and 70.60 Million tons in 2026 to 89.38 Million tons by 2031, registering a CAGR of 4.83% between 2026 to 2031.

This report is Segmented by Form (Granular Sulphur, Lump Sulphur, and Powdered Sulphur), Application (Fertilizers, Rubber Processing, Mining and Metallurgy, Petroleum Refining, Chemical Manufacturing, Pesticides and Fungicides, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Solid Sulphur Market Trends and Insights

Growth in Ultra-Low-Sulphur-Fuel Regulations

Tighter marine and on-road diesel limits have compelled refiners to add or upgrade desulphurization units, dramatically lifting solid sulphur output even as they sell cleaner fuels. KIPIC's Al-Zour refinery produced 732,000 tons of granular sulphur across 2024-2025, saving USD 100 million annually by enabling low-sulphur fuel-oil production. This paradox of lower-sulphur fuels but higher elemental supply periodically depresses prices when fertilizer demand softens. North American majors responded by optimizing Claus units that now capture more than 99% of hydrogen sulphide, turning a former liability into a revenue stream, although capital intensity restricts the practice to integrated players.

Expansion of Non-Ferrous Metal Smelting Capacity

Copper, nickel, and zinc projects continue to increase sulphuric-acid intensity. Indonesia's battery-grade nickel HPAL plants import roughly 75% of their sulphur feedstock from the Middle East, tightening global balances whenever Persian Gulf logistics slow. Chile's copper leach operations consumed 8.2 million tons of acid in 2025, up sharply as ore grades declined, while Peru's Tia Maria project will lift national acid demand by 800,000 tons per year after 2027. The Central African Copperbelt imports close to 2 million tons of solid sulphur annually for cobalt and oxide copper leaching, leaving regional output exposed to any Strait of Hormuz disruption.

Volatile Crude-Oil and Gas Recovery Volumes

Solid sulphur supply mirrors hydrocarbon activity. North American gas drilling retrenched in 2025, curbing output from sweetening plants in the Permian and Marcellus. OPEC+ production cuts also tightened Middle Eastern by-product availability even though desulphurization capacity was idle. With virtually no stand-alone sulphur mines, the market cannot respond quickly when fertilizer or metallurgical buyers suddenly increase orders, embedding chronic supply-demand mismatches.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Asphalt Modification Uses

- Commercialization of Lithium-Sulphur Batteries

- Slow Ramp-Up of Blue-Hydrogen Claus Output

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Granular grades commanded 57.11% of the solid sulphur market share in 2025 as fertilizer blenders favor their 2-6 mm spheres for dust-free pneumatic conveying. IPCO's single-pass drum technology now cools and coats liquid sulphur into SUDIC-compliant granules, meeting stricter occupational health limits on hydrogen-sulphide exposure.

Powdered material, though smaller today, is projected to grow at a 5.25% CAGR through 2031, buoyed by micronized fungicide sprays and inverse-vulcanization feedstocks that require high surface area. Vineyards report better powdery-mildew control when sulphur powders are mixed with organosilicone surfactants, broadening adoption across specialty crops. Lump sulphur retains niche uses where slow dissolution suits alkaline soils, yet its irregular size complicates automated blending, reducing future share.

Geography Analysis

Asia-Pacific held 41.34% of solid sulphur market share in 2025 and is projected to grow at 5.42% CAGR through 2031. Indonesia's HPAL nickel, China's soil-sulphur depletion, and India's refinery upgrades underpin regional momentum. Indonesia sources 75% of its sulphur from the Middle East, exposing its balances to Persian Gulf shipping risks. China's ammonium-sulphate boom lets farmers sidestep nitrogen export quotas, while India's new desulphurization units will gradually substitute imports with domestic by-product.

North America remains a pivotal supplier. Canada's oil-sands produced about 3 million tons in 2025, 63% of national output, while Suncor marketed more than 800,000 tons as molten and prilled product. Historical block remelting could add 1.5 million tons by 2030 if prices stay elevated, yet new facilities will not be fully online until 2026. U.S. output hinges on Gulf Coast refinery runs and Permian gas drilling, making supply sensitive to crude and gas price cycles.

Europe faces shrinking domestic production as aging refineries close and crude slates lighten. Germany, France, and Italy import growing volumes from Qatar, Saudi Arabia, and Russia, while policy focus on circular-economy solutions is spurring pilot projects in sulphur-based polymers. South America's profile is shaped by Chilean copper and Brazilian fertilizers: Chile imported 3.8 million tons of sulphuric acid in 2025 after smelter outages, and Mosaic's December 2025 shutdown of SSP production in Brazil highlighted pricing risk when spot sulphur tripled year-over-year. The Middle East remains the export hub, with ADNOC's Ruwais terminal lifting capacity to 27,000 tons per day and KIPIC's Al-Zour sending a record 52,000-ton shipment in January 2025.

- ADNOC

- aglobis

- Chemtrade Logistics

- CNPC

- Formosa Plastics Corporation, U.S.A

- Hindustan Petroleum Corporation Limited

- Indian Oil Corporation Ltd.

- Jordan Sulphur

- KIPIC (Kuwait Petroleum Corporation)

- QatarEnergy

- RAM SHREE CHEMICALS

- Rhenus Logistics SE & Co. KG

- Saudi Arabian Oil Co.

- Shell plc

- Suncor Energy Inc.

- Tengizchevroil LLP

- TotalEnergies

- Valero

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in ultra-low-sulphur-fuel regulations

- 4.2.2 Expansion of non-ferrous metal smelting capacity

- 4.2.3 Increasing asphalt modification uses

- 4.2.4 Commercialization of lithium-sulphur batteries

- 4.2.5 Circular-economy push for sulphur-based polymers

- 4.3 Market Restraints

- 4.3.1 Volatile crude-oil and gas recovery volumes

- 4.3.2 Slow ramp-up of blue-hydrogen Claus output

- 4.3.3 Logistics bottlenecks in molten-sulphur transport

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Form

- 5.1.1 Granular Sulphur

- 5.1.2 Lump Sulphur

- 5.1.3 Powdered Sulphur

- 5.2 By Application

- 5.2.1 Fertilizers

- 5.2.2 Rubber Processing

- 5.2.3 Mining and Metallurgy

- 5.2.4 Petroleum Refining

- 5.2.5 Chemical Manufacturing

- 5.2.6 Pesticides and Fungicides

- 5.2.7 Other Applications (Pharmaceuticals, Water Treatment, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 ADNOC

- 6.4.2 aglobis

- 6.4.3 Chemtrade Logistics

- 6.4.4 CNPC

- 6.4.5 Formosa Plastics Corporation, U.S.A

- 6.4.6 Hindustan Petroleum Corporation Limited

- 6.4.7 Indian Oil Corporation Ltd.

- 6.4.8 Jordan Sulphur

- 6.4.9 KIPIC (Kuwait Petroleum Corporation)

- 6.4.10 QatarEnergy

- 6.4.11 RAM SHREE CHEMICALS

- 6.4.12 Rhenus Logistics SE & Co. KG

- 6.4.13 Saudi Arabian Oil Co.

- 6.4.14 Shell plc

- 6.4.15 Suncor Energy Inc.

- 6.4.16 Tengizchevroil LLP

- 6.4.17 TotalEnergies

- 6.4.18 Valero

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Research and Development Momentum in Lithium-sulphur Batteries