|

시장보고서

상품코드

2062107

수직 밀링 머신 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vertical Milling Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

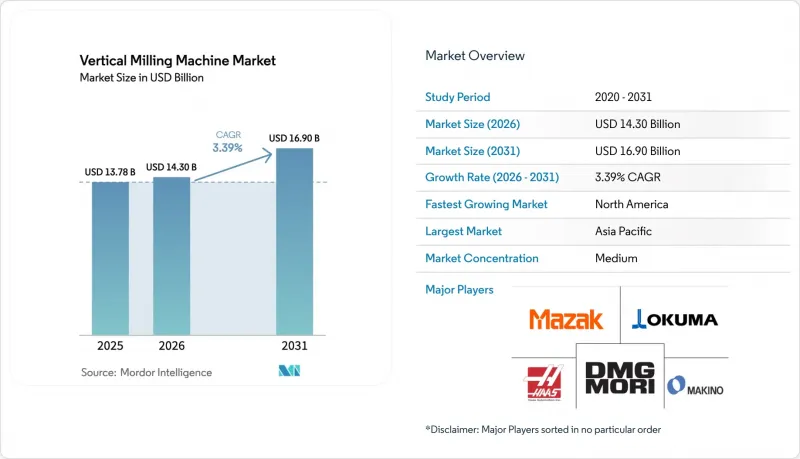

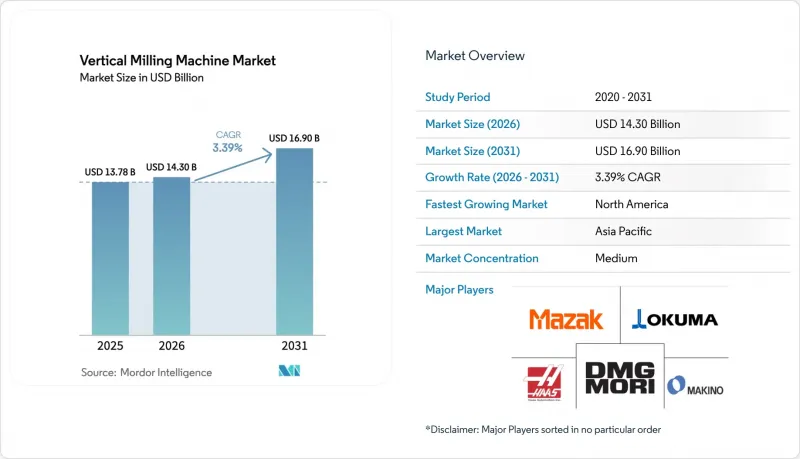

Mordor Intelligence에 의하면, 수직 밀링 머신 시장 규모는 2025년에 137억 8,000만 달러로 평가되었고 2026년 143억 달러에서 2031년까지 169억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 3.39%를 나타낼 전망입니다.

본 보고서는 제품 유형별(터렛식, 베드식 등), 축 구성별(3축, 4축, 5축 이상), 제어 기술(CNC, 기존 방식/수동), 최종 사용자 산업(자동차, 항공우주 및 방위, 기타), 지역(북미, 남미, 유럽, 아시아태평양, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 수직 밀링 머신 시장 동향 및 분석

항공우주 및 방위 분야에서의 제조 활동 확대

항공우주 및 방위 산업에서는 여전히 정밀도, 재현성, 가동률에 대한 요구가 높으며, 티타늄이나 고니켈 합금 가공 시 한 번의 세팅으로 가공이 가능한 5축 수직 밀링 머신이 선호되고 있습니다. 록히드 마틴은 2025년에 F-35 191대를 납품하며, 정밀 구조 부품 및 착륙 장치 가공 능력에 대한 수요를 뒷받침하는 강력한 프로그램 수행 능력을 입증했습니다. 에어버스는 2025년에 793대의 민간 항공기를 인도하고, 2026년에는 870대 인도를 목표로 하고 있으며, 이러한 수주 잔고는 향후 몇 년간의 생산량을 뒷받침할 것으로, 수직 가공 셀용 대형 금형, 지그 및 주익용 공구에 대한 투자를 뒷받침하고 있습니다. 다층적인 공급망은 기체, 엔진, 착륙 장치 시스템 전반에 걸친 리드타임 및 형상 요건을 충족하기 위해 3축 및 5축 가공 방식 모두에서 생산 능력을 확충함으로써 대응하고 있습니다. 국내 에너지 및 산업 공급망을 강화하기 위한 연방 정부와 민간 부문의 투자 또한, 더 정밀한 형상을 갖춘 이중용도 부품 생산을 위한 미국의 가공 인프라를 강화하고 있습니다. 이러한 요인들이 복합적으로 작용하여, 항공우주 프로그램이 생산 규모를 확대하고 기체를 교체하며 복잡한 예비 부품 공급 체계를 유지하는 가운데, 수직 밀링 머신 시장은 수년 동안 안정적인 기반을 유지해 왔습니다.

자동차 경량화 이니셔티브의 확대

자동차 제조업체들은 차량의 중량, 비용, 성능 간의 균형을 지속적으로 추구하고 있으며, 이는 수직 가공 플랫폼에서 가공되는 알루미늄 및 첨단 강재용 금형에 대한 수요를 뒷받침하고 있습니다. NHTSA(미국 도로교통안전국)가 발표한 최신 ‘SAFE Vehicles Rule III’ 초안에는 금형 및 지그 설계에 영향을 미치는 경량화 수준과 소재 전략이 상세하게 규정되어 있으며, 이는 다중 캐비티 금형 및 배터리 부품용 금형을 위한 수직 밀링 가공 능력에 대한 추가 투자를 촉진하고 있습니다. 각 OEM 업체들은 클로저 시스템, 차체 구조 및 섀시 부품의 최적화를 추진하고 있으며, 이는 알루미늄과 강철 금형의 병용을 촉진하는 동시에 베드형 시스템에서 신속한 소재 전환과 견고한 진동 제어의 필요성을 높이고 있습니다. 전기차(EV) 플랫폼은 모터 하우징, 배터리 트레이, e-액슬 부품과 같은 새로운 가공 작업량을 발생시키고 있으며, 이러한 부품들은 고강성 수직 가공 설비에 가장 적합합니다. EPA의 ‘2025년 자동차 동향 보고서’는 차량의 평균 중량이 증가하고 있음을 뒷받침하고 있으며, 이에 따라 설계 중심의 경량화에 대한 시급성은 여전히 유지되고 있어, 업데이트된 금형, 지그 및 정밀 지그에 대한 수주가 증가하고 있습니다. 이러한 사업 환경은 제조업체와 1차 공급업체로 하여금 동일한 셀 내에서 경량용 및 중하중용 공구강 모두를 처리할 수 있는 새로운 수직 밀링 머신 시장 규모를 확보하도록 촉진하고 있습니다.

초기 설비 투자 비용이 많이 듭니다.

엔트리급 3축 수직 밀링 머신과 대형 5축 플랫폼 간의 가격 차이는 여전히 크며, 이로 인해 구매 여부는 재무 상태나 신용 상황에 따라 좌우되고 있습니다. 미국의 제조 기술 관련 수주는 2025년 12월에 월간 사상 최고치를 기록했으며, 연간으로는 22.5% 증가한 것으로 마감되었으나, 최첨단 수직 가공기는 단가가 높기 때문에 체계적인 자금 조달과 수년까지 계획이 필요합니다. 리스는 운전자금을 확보하고 현금 흐름을 안정화시키는 동시에, 기계의 사용 연수에 걸친 계약 조건을 통해 접근성 격차 해소에서 더 큰 역할을 하고 있습니다. 2026년의 설비 및 소프트웨어 투자 증가율은 2025년의 급증에 비해 둔화될 것으로 예측됩니다. 이는 여전히 꾸준한 업데이트 주기를 뒷받침하는 요소이지만, 소규모 공장에서 5축 구성으로의 전환을 제한할 가능성이 있습니다. 이러한 자금 조달 동향에 힘입어 수직 밀링 머신 시장은 계속해서 성장하고 있지만, 도입 추세는 설비의 전면적인 교체보다는 단계적인 업그레이드나 자동화 부가 기능 도입으로 전환되고 있습니다. 따라서 구매자가 시범 도입 단계에서 다중 셀 구축 단계로 넘어가기 위해서는 비용의 가시화와 총소유비용(TCO) 벤치마킹이 매우 중요합니다.

부문별 분석

2025년 수직 밀링 머신 시장에서 베드형 시스템은 40.31%의 점유율을 차지했습니다. 이는 사용자가 중절삭, 간헐 절삭 및 대형 공작물을 처리할 수 있도록 구조적 강성과 진동 감쇠를 우선시했기 때문입니다. 이 입지는 자동차 금형 라인 및 항공우주 구조물에 대한 수요 덕분에 더욱 공고해지고 있습니다. 이러한 분야에서는 여러 교대 근무에 걸친 작업에서 마감 품질을 보장하기 위해 긴 스트로크와 강성이 필수적이기 때문입니다. 이러한 기계들은 공구강 및 기타 경질 합금 가공 시, 예측 가능한 칩 배출, 열적 안정성, 그리고 일관된 정밀도가 요구되는 생산 현장의 핵심을 담당하고 있습니다. 또한, 수직 밀링 머신 시장은 자동화에 대응하고 팔레타이징을 지원하는 베드형 플랫폼의 이점도 누리고 있으며, 이를 통해 다품종 생산 일정에서 스핀들의 가동률이 향상됩니다. 알루미늄 금형과 경화강 공구의 교체가 필요한 공장의 경우, 베드형은 대량 생산 목표에 부합하는 신속한 공구 교환과 공정 재현성을 갖춘 안정적인 기반을 제공합니다. 이러한 안정성 덕분에 생산 능력, 가공 가능한 부품 크기 범위, 가동 시간의 균형을 추구하는 사용자들에게 있어, 2026년 설비 투자 계획에서도 베드형 구성이 여전히 중심적인 위치를 차지할 것입니다.

갠트리형 또는 브리지형 구성은 도입 대수는 적지만, 사용자들이 초대형 부품의 원셋업 가공을 추구함에 따라 2031년까지 연평균 성장률(CAGR) 4.78%라는 가장 높은 성장률을 기록했습니다. 풍력 터빈의 허브, 대형 프레임, 긴 하우징 등의 경우, 단일 세팅으로 가공하는 것이 중요하며, 갠트리형의 넓은 작업 공간 덕분에 재고정 없이 다면 가공이 가능합니다. 터렛형 및 니형은 세팅 속도와 직접적인 수동 제어를 중시하는 공구실, 시제품 제작 및 소량 생산 분야에서 여전히 중요한 역할을 하고 있습니다. 이러한 용도로 인해 수직 밀링 머신 시장은 제품 유형별로 다양성을 유지하고 있으며, 브리지의 강성과 상부 여유 공간이 초기 투자 비용을 상회하는 분야에서는 갠트리 형식이 확대되고 있습니다. 또한, 사용자는 대형 수직 밀링 머신을 자동화 셀과 결합하여 넓은 가공 영역 전체에서 처리량을 안정화하고 가동 중지 시간을 최소화하고 있습니다. 대형 베드형 셀과 확대되는 갠트리 가공의 조합이 꾸준한 시장 점유율 추이와 견실한 성장세를 뒷받침하고 있습니다.

2025년 기준으로, 3축 가공기는 수직 밀링 머신 시장의 일반적인 가공 용도에서 가장 친숙하고 비용 면에서도 합리적인 형태로 54.78%의 점유율을 차지했습니다. 이 도입 기반은 프로그래밍의 간편함, 운영자의 풍부한 경험, 그리고 공구와 워크홀더의 폭넓은 생태계 덕분에 여전히 견고합니다. 이 방식은 매력적인 비용으로 다양한 부품을 처리할 수 있으며, 고도의 운동학이 필요 없이 가동률을 높일 수 있는 팔레트 체인저를 통한 자동화를 지원합니다. 직육면체 형상의 부품을 다루는 사용자들은 재현성이 높고 예측 가능한 생산을 실현하기 위해 여전히 3축 밀링 머신에 의존하고 있으며, 이 분야는 공장 운영의 경제성 측면에서 여전히 핵심적인 위치를 차지하고 있습니다. 또한, 이 부문은 안정성과 공구 경로의 부드러움을 향상시키는 제어 시스템의 업데이트와, 셋업 시간을 단축하는 프로빙 워크플로의 이점도 누리고 있습니다.

5축 이상의 구성은 가장 빠르게 성장하고 있으며, 2031년까지 연평균 성장률(CAGR)은 5.61%로 예측됩니다. 이는 수직형 밀링 머신 시장에서 공장이 여러 세팅을 하나의 가공 공정에 통합함으로써 불량을 줄이고, 시작부터 완료까지의 시간을 단축하고 있기 때문입니다. 항공우주용 브라켓, 임펠러, 정형외과용 임플란트 등은 정밀도, 재현성 및 생산성 향상을 위해 현재 수직형 5축 가공 셀로 전환되고 있는 부품의 예입니다. 많은 사용자들이 프로그래밍 부담을 줄이기 위해 대화형 인터페이스나 템플릿화된 툴 경로를 채택하고 있으며, 이는 5축 가공기를 처음 도입하는 사용자들이 3축 가공에서 전환하는 데 도움이 되고 있습니다. 4축 가공기는 아직 완전한 동시 윤곽 가공이 필요하지 않은 여러 면에 대한 인덱스 가공에서 여전히 실용적인 중간 단계로 자리 잡고 있습니다. 팔레트 및 로봇을 갖춘 5축 셀의 무인 운전 신뢰도가 높아짐에 따라, 공장은 인력을 1대1로 늘리지 않고도 생산 능력을 확대되고 있습니다. 이러한 도입 패턴은 예측 기간 동안 기존 설비 구성의 안정적인 재분배에 기여하고 있습니다.

지역별 분석

아시아태평양은 2025년에 47.89%를 차지하며, 수직 밀링 머신 시장에서 여전히 가장 큰 시장 기반을 형성하고 있습니다. 중국, 일본, 한국, 인도, 동남아시아의 전자기기 및 자동차 제조 거점들은 기계 가동률을 높은 수준으로 유지하고 있는 반면, 공급망은 수출 수요에 부응하기 위해 생산 능력을 확대되고 있습니다. 현지 제조업체와 세계 브랜드가 소형, 중형, 대형 등 다양한 규격에서 경쟁하고 있으며, 이로 인해 자동화 지원이 가능한 수직형 플랫폼에 대한 접근성이 향상되고 있습니다. 수탁 제조 및 잡샵 분야에서 APAC의 강점은 부품의 다양성에 대응하기 위한 3축 및 4축 수직 가공기의 도입을 뒷받침하고 있습니다. 지역별 교육 및 인증 프로그램은 기술 격차를 해소하기 위해 확대되고 있으며, 인력 양성을 위한 하이브리드 접근 방식으로서 수동 및 CNC 플랫폼 모두의 필요성을 더욱 강조하고 있습니다. 이러한 추세에 따라 APAC 지역은 다양한 수직 밀링 머신의 활용 사례를 보유한 핵심 수요 시장으로 자리매김하고 있습니다.

북미는 리쇼어링, 인프라 확충, 그리고 전략적 부품의 국내 생산을 촉진하는 인센티브 덕분에 2031년까지의 예측 지역 연평균 성장률(CAGR)이 5.21%로 가장 높은 성장률을 기록했습니다. 미국 에너지부는 에너지 및 산업 공급망을 강화하기 위한 연방 정부와 민간 부문의 투자를 강조하고 있으며, 이에 따라 수직형 플랫폼의 정밀 가공 능력에 대한 지역 수요가 증가하고 있습니다. 미국의 제조 기술 수주액은 2025년 12월에 사상 최고치를 기록했으며, 연간으로는 22.5% 증가한 것으로 마감했습니다. 이는 기계 설비의 지속적인 현대화를 반영한 것으로, 자동화 대응형 수직 가공 센터의 도입을 촉진하고 있습니다. 캐나다와 멕시코는 자동차, 항공우주, 전자 분야 프로그램을 뒷받침하는 통합 공급망을 통해 참여하고 있습니다. 이 지역의 각 공장에서는 설비 통합을 위해 5축 가공 셀의 규모를 확대하고 있으며, 숙련된 인력 부족 문제를 해결하기 위해 팔레트와 로봇을 활용하고 있습니다. 이러한 움직임에 따라, 해당 지역의 제조거점은 복잡한 부품 가공에 대응할 준비가 갖춰져 리드 타임을 단축할 수 있게 됩니다.

유럽에서는 자동차 금형, 항공우주, 에너지 분야에서 고정밀 수직 밀링 머신에 대한 확고한 도입 실적과 정교한 수요 동향이 유지되고 있습니다. 2026년 1월 DN Solutions가 HELLER를 인수한 사례와 같이, 유럽의 서비스 및 지원 네트워크를 통합하는 재편 움직임은 복잡한 수직형 플랫폼의 가동률과 수명 주기 성능에 필수적인 지역 생태계를 강화하고 있습니다. 독일, 이탈리아, 프랑스, 영국의 정밀 가공 사용자들은 형상 정밀도와 재현성 요건을 충족하기 위해 높은 강성, 열 제어, 첨단 제어 기능을 갖춘 수직 가공기를 계속해서 선호하고 있습니다. 또한, 유럽의 정책 체계는 최신 스핀들, 고압 절삭유, 그리고 사이클 타임을 단축하는 공구 경로 전략과 조화를 이루며, 에너지 효율이 높은 생산을 장려하고 있습니다. 이러한 특성은 단일 설정을 통한 정밀도와 자동화의 이점을 누릴 수 있는 고부가가치이며 검증된 작업을 중시함으로써 수직 밀링 머신 시장에 기여하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the vertical milling machine market size was valued at USD 13.78 billion in 2025 and is estimated to grow from USD 14.30 billion in 2026 to reach USD 16.90 billion by 2031, at a CAGR of 3.39% during the forecast period (2026-2031).

This report is Segmented by Product Type (Turret, Bed-Type, and More), by Axis Configuration (3-Axis, 4-Axis, 5-Axis & Above), by Control Technology (CNC, Conventional/Manual), by End-User Industry (Automotive, Aerospace & Defense, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Vertical Milling Machine Market Trends and Insights

Growing Aerospace and Defense Manufacturing Activity

Aerospace and defense maintain a high requirement for accuracy, repeatability, and uptime that favors single-setup vertical five-axis mills on titanium and high-nickel alloys. Lockheed Martin delivered 191 F-35 aircraft in 2025, demonstrating strong program execution that sustains demand for precision structural parts and landing gear machining capacity. Airbus reported 793 commercial aircraft deliveries in 2025 and targeted 870 deliveries in 2026, while its backlog supported years of production cover that underpins investment in large-format molds, fixtures, and wing tooling for vertical mill cells. Tiered supplier networks are responding by adding capacity in both three-axis and five-axis formats to meet lead time and geometry requirements across airframe, engine, and landing systems. Federal and private investments to strengthen domestic energy and industrial supply chains are also reinforcing U.S. machining infrastructure for dual-use components with higher precision profiles. Together, these forces keep the vertical milling machine market on a steady multi-year footing as aerospace programs scale output, refresh fleets, and maintain complex spares pipelines.

Expansion of Automotive Lightweighting Initiatives

Automakers continue to balance vehicle mass, cost, and performance, which sustains demand for aluminum and advanced steel tooling machined on vertical platforms. The latest SAFE Vehicles Rule III proposal from NHTSA details mass-reduction levels and material strategies that influence die and fixture design, supporting more investment in vertical milling capacity for high-cavity dies and battery component tooling. OEMs are optimizing closure systems, body structures, and chassis parts, which drives a mix of aluminum and steel dies, and raises the need for quick material changeover and robust vibration control on bed-type systems. Electric vehicle platforms add new machining workloads for motor housings, battery trays, and e-axle components that fit well with high-rigidity vertical setups. The EPA's 2025 Automotive Trends Report confirms rising average vehicle weight, which maintains urgency around design-driven mass reduction and supports orders for updated dies, fixtures, and precision jigs. This operating context encourages manufacturers and tier suppliers to secure new vertical milling machine market capacity that addresses both lightweight and heavy-duty tool steels in the same cell.

High Initial Capital Investment Requirements

The cost gap between entry-level three-axis vertical mills and large-format five-axis platforms remains material, which segments purchasing by balance sheet and credit access. U.S. manufacturing technology orders set a new monthly record in December 2025 and ended the year up 22.5%, yet the most advanced vertical machines carry high unit prices that require structured financing and multi-year planning. Leasing plays a greater role in closing the access gap, with terms that extend across machine life while preserving working capital and smoothing cash flows. Equipment and software investment growth in 2026 is projected to moderate versus 2025's surge, which will still support steady replacement cycles but could limit step-ups to five-axis configurations for smaller shops. These financing dynamics keep the vertical milling machine market expanding, but they tilt adoption curves toward phased upgrades and automation add-ons rather than wholesale fleet changes. Cost visibility and total cost of ownership benchmarks are therefore critical to move buyers from trials to multi-cell deployments on vertical platforms.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Precision Medical Devices and Implants

- Increasing Adoption of CNC and Multi-Axis Machining

- Shortage of Skilled Machine Operators and Programmers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bed-Type systems held 40.31% share in 2025 within the vertical milling machine market as users prioritized structural rigidity and vibration damping for heavy, interrupted cuts and large workpieces. That position is reinforced by demand from automotive die lines and aerospace structures, where long travel and stiffness are critical to finish quality across multi-shift operations. These machines anchor production floors that need predictable chip evacuation, thermal stability, and consistent accuracy in tool steels and other hard alloys. The vertical milling machine market also benefits from bed-type platforms that are automation-ready and support palletization, which raises spindle utilization for high-mix schedules. For plants that must switch between aluminum dies and hardened steel tools, bed-type provide a stable base with quick tool changes and process repeatability that fits volume production targets. This stability profile keeps bed-type configurations central to capital planning in 2026 for users seeking a balance of capacity, part size range, and uptime.

Gantry or bridge-type configurations hold a smaller installed base yet posted the fastest growth with a 4.78% CAGR through 2031 as users pursue single-setup machining for extreme-scale parts. Wind turbine hubs, large frames, and long housings make one-setup access valuable, and gantry clearances enable multi-sided milling without re-fixturing. Turret and knee-type remain in play for toolrooms, prototyping, and small-batch jobs that prioritize setup speed and direct manual control. These roles keep the vertical milling machine market diversified across product types, with gantry formats expanding where bridge rigidity and overhead clearance outweigh higher capex. Users are also pairing large vertical mills with automation cells to stabilize throughput and to minimize idle time across large work envelopes. The mix of heavy-duty bed-type cells and expanding gantry work underpins steady share dynamics and a resilient growth path.

Three-axis machines commanded 54.78% share in 2025 as the most familiar and cost-accessible format across general machining applications in the vertical milling machine market. This installed base remains strong due to simpler programming, abundant operator experience, and a wide ecosystem of tooling and workholding. The format addresses a broad set of parts at attractive cost points and supports automation with pallet changers that can move utilization higher without advanced kinematics. Users with prismatic parts continue to rely on three-axis mills for repeatable, predictable production, which keeps the category central to shop economics. The segment also benefits from control updates that improve stability, toolpath smoothness, and probing workflows that cut setup time.

Five-axis and above configurations were the fastest growing, with a projected 5.61% CAGR through 2031, as shops consolidate multiple setups into one pass to cut defects and compress start-to-finish time in the vertical milling machine market. Aerospace brackets, impellers, and orthopedic implants are among the parts that now move to vertical five-axis cells to gain accuracy, repeatability, and higher throughput. Many users are adopting conversational interfaces and templated toolpaths to lower the programming burden, which helps first-time five-axis buyers migrate from three-axis routes. Four-axis machines remain a practical middle step for indexed milling on multiple faces where full simultaneous contouring is not yet necessary. As confidence grows in unattended shifts on five-axis cells with pallets and robots, shops expand capacity without one-for-one increases in labor. These adoption patterns are contributing to a steady reweighting of the installed base over the forecast period.

Geography Analysis

Asia-Pacific captured 47.89% in 2025 and remains the largest regional base for the vertical milling machine market. Electronics and automotive manufacturing footprints across China, Japan, South Korea, India, and Southeast Asia keep machine utilization high, while supplier networks expand capacity to serve export demand. Local builders and global brands compete across small, mid, and large formats, and that improves access to automation-ready vertical platforms. APAC's strength in contract manufacturing and job shops also supports three-axis and four-axis vertical installs that handle high part variability. Regional training and certification programs are expanding to address skills gaps, and they reinforce the need for both manual and CNC platforms as a blended approach to grow the workforce. These dynamics keep APAC a demand anchor with a broad mix of vertical milling use cases.

North America recorded the fastest projected regional CAGR at 5.21% through 2031 due to reshoring, infrastructure buildout, and incentives that favor domestic production of strategic components. The U.S. Department of Energy highlighted federal and private investments that strengthen energy and industrial supply chains, which are increasing local demand for precision machining capacity on vertical platforms. U.S. manufacturing technology orders reached a record high in December 2025 and closed the year up 22.5%, which reflects the continued modernization of the machine base and supports the adoption of automation-ready vertical centers. Canada and Mexico participate through integrated supply chains that support automotive, aerospace, and electronics programs. Shops across the region are scaling five-axis cells to consolidate setups and are using pallets and robots to address skilled labor gaps. These moves enhance the readiness of the regional base to take on complex parts and to reduce lead times.

Europe maintains a deep installed base and a sophisticated demand profile for high-accuracy vertical mills in automotive tooling, aerospace, and energy. Consolidation moves that integrate European service and support networks, such as DN Solutions acquiring HELLER in January 2026, reinforce local ecosystems that are essential to uptime and lifecycle performance on complex vertical platforms. Precision users across Germany, Italy, France, and the UK continue to favor vertical machines with strong rigidity, thermal control, and control sophistication to meet geometry and repeatability requirements. Policy frameworks in Europe also encourage energy-efficient production that aligns with modern spindles, high-pressure coolant, and toolpath strategies that shorten cycle times. These attributes contribute to the vertical milling machine market by emphasizing high-value, audited work that benefits from single-setup accuracy and automation.

- Haas Automation

- DMG MORI

- Yamazaki Mazak

- Okuma Corporation

- Makino Milling Machine

- Hurco Companies

- DN Solutions (Doosan)

- FANUC Corporation

- Siemens AG (Sinumerik)

- GF Machining Solutions

- Fives Group

- JTEKT Corporation

- EMAG GmbH

- Brother Industries

- Hardinge Inc.

- Shenyang Machine Tool

- HELLER Group

- Chiron Group

- Ace Micromatic

- SMTCL

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Aerospace and Defense Manufacturing Activity

- 4.2.2 Expansion of Automotive Lightweighting Initiatives

- 4.2.3 Rising Demand for Precision Medical Devices and Implants

- 4.2.4 Increasing Adoption of CNC and Multi-Axis Machining

- 4.2.5 Growth in Contract Manufacturing and Job Shop Operations

- 4.2.6 Infrastructure Development and Construction Equipment Demand

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Investment Requirements

- 4.3.2 Shortage of Skilled Machine Operators and Programmers

- 4.3.3 Long Lead Times for Machine Delivery and Installation

- 4.3.4 Competition from Alternative Machining Technologies

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter?s Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Regional Manufacturing Ecosystem Maturity

- 4.9 Financing and Leasing Models Evolution

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Product Type

- 5.1.1 Turret

- 5.1.2 Bed-Type

- 5.1.3 Knee-Type

- 5.1.4 Gantry / Bridge-Type

- 5.1.5 Others (turn-mill, specialized, etc.)

- 5.2 By Axis Configuration

- 5.2.1 3-Axis

- 5.2.2 4-Axis

- 5.2.3 5-Axis & Above

- 5.3 By Control Technology

- 5.3.1 CNC Vertical Milling Machines

- 5.3.2 Conventional/ Manual Vertical Milling Machines

- 5.4 By End-User Industry

- 5.4.1 Automotive

- 5.4.2 Aerospace & Defense

- 5.4.3 Electronics & Semiconductor

- 5.4.4 Medical Devices

- 5.4.5 Energy & Power

- 5.4.6 Others (General Manufacturing, Job Shops, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Haas Automation

- 6.4.2 DMG MORI

- 6.4.3 Yamazaki Mazak

- 6.4.4 Okuma Corporation

- 6.4.5 Makino Milling Machine

- 6.4.6 Hurco Companies

- 6.4.7 DN Solutions (Doosan)

- 6.4.8 FANUC Corporation

- 6.4.9 Siemens AG (Sinumerik)

- 6.4.10 GF Machining Solutions

- 6.4.11 Fives Group

- 6.4.12 JTEKT Corporation

- 6.4.13 EMAG GmbH

- 6.4.14 Brother Industries

- 6.4.15 Hardinge Inc.

- 6.4.16 Shenyang Machine Tool

- 6.4.17 HELLER Group

- 6.4.18 Chiron Group

- 6.4.19 Ace Micromatic

- 6.4.20 SMTCL

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment