|

시장보고서

상품코드

2062108

사이버 훈련장 및 시뮬레이션 플랫폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2030년)Cyber Ranges And Simulation Platforms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

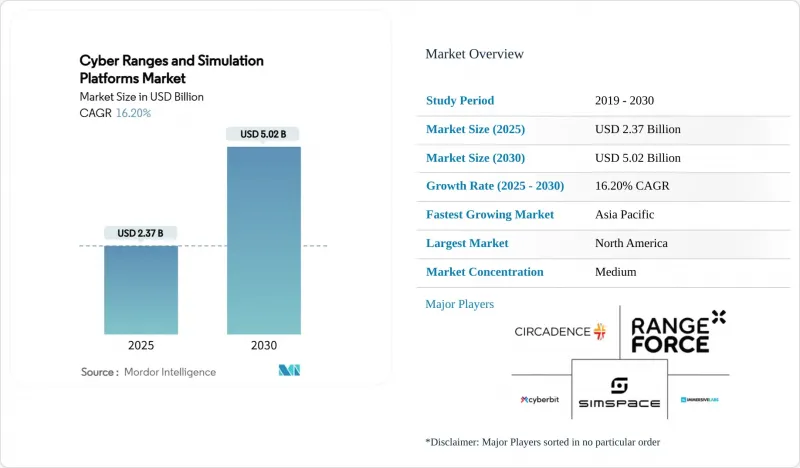

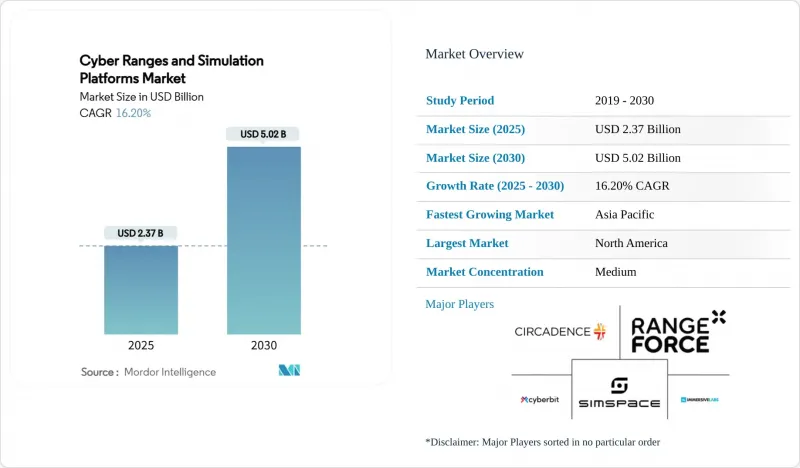

Mordor Intelligence에 의하면, 사이버 훈련장 및 시뮬레이션 플랫폼 시장 규모는 2025년에 23억 7,000만 달러로 평가되었습니다. 2030년까지 50억 2,000만 달러로 확대되어 CAGR 16.2%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 레인지 유형(시뮬레이션 레인지, 에뮬레이션 레인지 등), 도입 형태(On-Premise, 클라우드 기반, 하이브리드), 최종 사용자(국방·치안 기관, BFSI 등), 용도(교육 및 인증, 위협 인텔리전스 및 분석 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 사이버 훈련장 및 시뮬레이션 플랫폼 시장 동향 및 인사이트

중요 인프라에 대한 사이버 공격 빈도의 급증

제조, 에너지, 운송 분야의 각 사업자들은 현재 사상 최대 규모의 랜섬웨어 공격에 직면해 있으며, 싱가포르 사이버보안청은 2023년에 주로 산업 환경을 표적으로 한 132건의 사고를 기록했습니다. 이러한 사태가 심각해짐에 따라, 실제 컨트롤러와 센서 네트워크를 통합한 운영 기술(OT) 제품군에 대한 수요가 증가하고 있습니다. 아이다호 국립연구소의 확장된 ICS 프로그램은 실제 장비가 시나리오의 사실성을 어떻게 높이는지를 보여주고 있습니다. ‘Liberty Eclipse’나 ‘GridEx VII’와 같은 훈련은 사이버 대응팀과 전력망 운영자 간의 협력 미비를 여실히 드러내고 있으며, 다분야에 걸친 시뮬레이션의 필요성을 더욱 강조하고 있습니다. 에너지 사업자들은 현재 사이버 훈련을 안전상의 필수 사항으로 간주하고 있습니다. 왜냐하면 사이버 공격의 실패가 물리적 혼란을 초래할 가능성이 있기 때문입니다. 미국 에너지부의 CyTRICS 이니셔티브는 전용으로 구축된 시험장에서 에너지 관련 부품에 대한 내구성 시험을 실시함으로써 이러한 추세를 뒷받침하고 있습니다.

규제 당국이 의무화한 사이버 대응 훈련 강화

금융 감독 당국은 단순한 정책 체크리스트가 아닌, 실증에 기반한 훈련을 요구하고 있습니다. 뉴욕주의 개정된 23 NYCRR 500은 은행에 대해 매년 침투 테스트와 사고 시뮬레이션을 실시할 것을 의무화하고 있습니다. 유럽의 DORA는 지역 전체에 걸쳐 통일된 업무 복원력 테스트를 의무화하고 있습니다. FINRA의 2025년 감독 보고서는 AI를 활용한 피싱을 가장 큰 위험 요인으로 지적하며, 가맹 기업들에게 대응 훈련을 위해 테스트 환경을 활용할 것을 권고했습니다. 이러한 규제로 인해 참가자의 지표를 기록하고 감사에 대응할 수 있는 증거를 생성하는 플랫폼에 대한 지속적인 수요가 발생하고 있으며, 구매 기준이 기능 목록에서 성과 문서화로 전환되고 있습니다.

몰입형 물리 레인지에 필요한 막대한 초기 투자

실제 스위치, PLC, SCADA 장비를 활용한 물리적 테스트 환경 구축에는 100만 달러 이상의 비용이 소요될 수 있습니다. HP의 Wolf Security 보고서에 따르면, 구매자의 60%가 장비 조달 시 보안 문제를 간과하고 있으며, 그 결과 사후 개선 예산이 급증하고 있는 것으로 나타났습니다. 산업 분야의 구매자는 전력, 냉각 및 보안 대책이 마련된 시설에 대한 자금도 확보해야 하므로, 순수한 물리적 구축은 많은 기업에게 현실적이지 않습니다. 가상화된 레인지는 비용을 절감해 주지만, 전력망의 장애 전환과 같은 특정 동적 시나리오에서는 여전히 물리적 장비가 필요합니다. 그 결과, 기업들은 투자를 미루거나 범위를 제한한 시범 도입에 그치고 있어, 사이버 훈련장 및 시뮬레이션 플랫폼 시장의 단기적인 성장을 저해하고 있습니다.

부문별 분석

소프트웨어 엔진은 2024년 매출의 57.3%를 차지하며, 리얼리즘 구축 과정에서 하이퍼바이저, 오케스트레이션 계층 및 분석 대시보드가 수행하는 역할을 부각시켰습니다. 이 분야에서는 AI를 활용한 위협 생성 및 드래그 앤 드롭 방식의 네트워크 빌더를 통해 시나리오 작성에 소요되는 시간이 단축되고 있습니다. 그러나 기업들은 이러한 고된 업무를 외부에 위탁하는 경향이 강해지고 있습니다. 서비스 부문은 연평균 성장률(CAGR) 18.1%로 성장을 지속하고, 있으며, 이는 구매자들이 턴키 방식의 커리큘럼 설계, 실시간 코칭, 실습 후 수정 지침을 선호하기 때문입니다. 매니지드 프로바이더는 매주 시나리오를 업데이트하는 지속적인 학습 주기를 운영하고 있어, 사내 인력의 부담을 늘리지 않으면서도 시나리오의 관련성을 확보하고 있습니다. 이러한 변화는 사이버 훈련장 및 시뮬레이션 플랫폼 시장이 제품 중심의 경제에서 성과 중심의 경제로 성숙해 가고 있음을 보여줍니다.

실제로 Cloud Range와 같은 제공업체는 상용 SIEM, 방화벽, EDR 스택을 서비스 범위에 통합하여, 블루팀이 실제 운영 환경에서 사용하는 것과 동일한 도구를 활용해 훈련을 진행할 수 있도록 하고 있습니다. 사후 분석을 통해 성능 데이터는 ‘감지까지의 평균 시간(MTD)’과 같은 경영진 차원의 지표로 변환됩니다. 이러한 인사이트가 리스크 대시보드에 반영됨에 따라, 더 많은 CISO가 구독 갱신을 정당화할 수 있게 되었으며, 시장의 안정을 뒷받침하는 지속적인 수익원이 강화되고 있습니다.

가상 시뮬레이션 환경은 도입 비용이 저렴하고 선형적인 확장성을 갖추고 있어, 2024년 시장 점유율의 44.3%를 차지했습니다. 대학에서는 물리적 랙 없이도 수백 개의 학생용 포드를 동시에 구축하고 있는 반면, 기업에서는 실제 환경에 대한 접근 권한을 부여하기 전에 시뮬레이션을 통해 신입 사원의 자격을 평가했습니다. 그러나 가상 레이어와 특정 물리적 자산을 결합한 하이브리드 설계가 연평균 성장률(CAGR) 17.3%라는 가장 빠른 속도로 확대되고 있습니다. 예를 들어, 대형 석유 및 가스 기업들은 실제 PLC 랙을 가상 파이프라인에 통합하여 센서의 지연이나 신호 노이즈를 시뮬레이션하고 있습니다. 이러한 조합을 통해 실험실에 플랜트 전체를 구축하지 않고도 높은 정확도의 시뮬레이션이 가능해집니다.

오버레이 및 에뮬레이션 분야는 패킷의 타이밍이나 디바이스 펌웨어의 미세한 차이가 미션 크리티컬한 영향을 미치는 틈새 프로토콜 수준 테스트를 지원합니다. 절대 금액으로 보면 규모는 작지만, 이러한 틈새 시장에서는 특수한 장비나 컨텐츠가 필요하기 때문에 종종 프리미엄 가격이 책정됩니다.

지역별 분석

북미는 넉넉한 연방 예산과 엄격한 주 차원의 규제의 뒷받침을 받아 2024년 매출의 38.3%를 차지했습니다. 에너지부의 OTDefender 펠로우십 프로그램은 졸업생들을 유틸리티체로 파견함으로써, OT에 특화된 테스트 환경에 대한 지역 내 수요를 확대되고 있습니다. 또한, 클라우드 도입을 위한 준비가 전반적으로 잘 갖춰져 있어 상업적 도입을 더욱 촉진하고 있으며, 중견 기업에서 SaaS를 신속하게 도입할 수 있게 하고 있습니다. 캐나다와 멕시코는 국경을 초월한 전력망 보안 프로그램을 통해 참여하고 있지만, 그 비중은 미국에 비해 낮은 임베디드니다.

아시아태평양은 2030년까지 연평균 성장률(CAGR)이 17.0%로, 가장 빠르게 성장하고 있는 지역입니다. 싱가포르 사이버 방어 시험 평가 센터는 학계, 군, 민간 부문의 팀들에게 협력적인 접근 기회를 제공합니다. 일본의 ‘CyberKONGO2025’ 훈련에는 17개국이 참여했으며, 이는 연합 간 상호운용성에 대한 지역의 높은 관심을 보여주고 있습니다. 한편, 인도와 중국은 독자적인 통신 스택을 반영한 국가 주권형 훈련장에 국가 안보 투자를 집중하고 있어, 사이버 훈련장 및 시뮬레이션 플랫폼 시장에서 현지화의 필요성을 부각시키고 있습니다.

유럽에서는 DORA(사이버 방어 지침) 준수, 공동 사이버 훈련, 그리고 각국의 사이버 훈련장 확충을 통해 꾸준한 추진력이 유지되고 있습니다. 독일과 프랑스는 국방 용도를 우선시하는 반면, 영국은 금융 부문을 대상으로 한 훈련을 가속화하고 있습니다. ECSO의 기능 체크리스트는 공급업체 간 비교를 촉진하고, 시장을 상호 운용성으로 이끌고 있습니다. 그 밖의 지역에서는 중동 및 아프리카의 바이어들이 에너지 및 통신 분야의 인재 양성을 중시하고 있으며, 걸프 국가들과 남아프리카공화국의 정부 지원 프로그램을 활용하여 현지 인재 양성 체계를 구축하는 속도를 높이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the cyber ranges and simulation platforms market size reached USD 2.37 billion in 2025 and is forecast to advance to USD 5.02 billion by 2030, posting a sturdy 16.2% CAGR.

This report is Segmented by Component (Software and Services), Range Type (Simulation Range, Emulation Range, and More), Deployment Mode (On-Premises, Cloud-Based, and Hybrid), End-User (Defense and Security Agencies, BFSI, and More), Application (Training and Certification, Threat Intelligence and Analysis, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cyber Ranges And Simulation Platforms Market Trends and Insights

Surging Cyber-Attack Frequency Across Critical Infrastructure

Manufacturing, energy, and transport operators now experience record ransomware volumes, with Singapore's Cyber Security Agency logging 132 incidents in 2023 that mainly struck industrial environments. This escalation propels demand for operational-technology ranges embedding real controllers and sensor networks. Idaho National Laboratory's expanded ICS programs illustrate how authentic equipment enriches scenario fidelity. Exercises such as Liberty Eclipse and GridEx VII underline coordination gaps between cyber teams and grid operators, reinforcing the need for multi-disciplinary simulations. Energy utilities now view cyber training as a safety imperative because failures can trigger physical disruptions. The U.S. Department of Energy's CyTRICS initiative confirms the trend by stress-testing energy components inside purpose-built ranges.

Escalating Regulatory-Mandated Cyber-Readiness Drills

Financial watchdogs require evidence-based drills rather than policy checklists. New York's updated 23 NYCRR 500 forces banks to run penetration tests and incident simulations each year. Europe's DORA imposes harmonised operational-resilience testing across the bloc. FINRA's 2025 oversight report flags AI-enabled phishing as a top risk and advises member firms to use ranges for response rehearsals. These rules generate continuous demand for platforms that log participant metrics and produce audit-ready evidence, shifting buying criteria from feature lists to outcome documentation.

High Capital Outlay for Immersive Physical Ranges

Building physical ranges with real switches, PLCs, and SCADA equipment can top USD 1 million. HP's Wolf Security report shows that 60% of buyers overlook security during device procurement, inflating retrofit budgets. Industrial buyers must also fund power, cooling, and secure facilities, making pure physical builds untenable for many. Virtualised ranges reduce spend, yet certain kinetic scenarios-such as power-grid failovers-still require tangible gear. Organisations therefore delay investment or adopt limited-scope pilots, restraining near-term growth in the cyber ranges and simulation platforms market.

Other drivers and restraints analyzed in the detailed report include:

- Defense Digital-Twin Adoption for Mission Rehearsal

- Cloud-Native Range Delivery Lowers TCO for SMEs

- Shortage of Skilled Cyber-Range Content Developers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software engines delivered 57.3% of 2024 revenue, underscoring the role of hypervisors, orchestration layers, and analytics dashboards in building realism. Within this domain, AI-assisted threat generation and drag-and-drop network builders reduce scenario lead times. However, enterprises increasingly outsource the heavy lifting. The services segment is tracking an 18.1% CAGR as buyers prefer turnkey curriculum design, live coaching, and post-exercise remediation guidance. Managed providers operate continuous-learning cycles where scenarios update weekly, ensuring relevance without internal headcount strain. This pivot signals that the cyber ranges and simulation platforms market is maturing from a product to an outcome economy.

In practice, providers like Cloud Range embed commercial SIEM, firewall, and EDR stacks inside their ranges so that blue teams rehearse using the same tooling seen in production. Post-event analytics translate performance data into board-level metrics such as mean-time-to-detect. As these insights feed risk dashboards, more CISOs justify subscription renewals, fortifying recurring revenue streams that underpin market stability.

Virtual simulation ranges held 44.3% of the 2024 share thanks to their low entry cost and linear scalability. Universities deploy hundreds of concurrent student pods without physical racks, while enterprises use simulation to certify new hires before granting production access. Yet hybrid designs that marry virtual layers with select physical assets are scaling fastest at 17.3% CAGR. Oil-and-gas majors, for instance, insert actual PLC racks into virtual pipelines to emulate sensor latency and signal noise. The combination supports high-fidelity rehearsals without building entire plants in a lab.

Overlay and emulation ranges cater to niche, protocol-level testing where packet timing or device firmware nuances are mission-critical. Although smaller in absolute dollars, these niches often command premium pricing because of specialised equipment and content.

Geography Analysis

North America generated 38.3% of 2024 revenue, anchored by generous federal budgets and stringent state-level regulations. The Department of Energy's OTDefender fellowship funnels graduates into utilities, amplifying local demand for OT-focused ranges. Commercial adoption is further propelled by widespread cloud readiness, enabling rapid SaaS onboarding across mid-market firms. Canada and Mexico participate through cross-border grid-security programmes, though their share is modest relative to the United States.

Asia-Pacific is the fastest-growing theatre at 17.0% CAGR to 2030. Singapore's Cyber Defence Test and Evaluation Centre offers federated access to academic, military, and private-sector teams. Japan's CyberKONGO2025 exercise spans 17 nations and demonstrates regional appetite for coalition interoperability. Meanwhile, India and China channel national-security investments into sovereign ranges that reflect unique telecommunications stacks, underscoring localisation imperatives within the cyber ranges and simulation platforms market.

Europe maintains steady momentum under DORA compliance, joint cyber exercises, and national range build-outs. Germany and France prioritise defence applications, while the UK accelerates financial-sector drills. ECSO's feature checklist fosters vendor comparison, nudging the market towards interoperability. Elsewhere, Middle East and Africa buyers emphasise energy and telecom protection, leveraging government-funded programmes in the Gulf and South Africa to jump-start local talent pipelines.

- SimSpace Corporation

- Cyberbit Ltd.

- RangeForce Inc.

- Immersive Labs Ltd.

- Circadence Corporation

- ThreatGEN LLC

- Offensive Security Services, LLC

- Raytheon Intelligence and Space

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- CAE Inc.

- L3Harris Technologies, Inc.

- IBM Corporation

- Airbus Defence and Space SAS

- Atos SE

- Science Applications International Corp.

- Leidos Holdings, Inc.

- Thales Group

- Mandiant (a Google LLC company)

- Palo Alto Networks, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging cyber-attack frequency across critical infrastructure

- 4.2.2 Escalating regulatory-mandated cyber-readiness drills

- 4.2.3 Defense digital-twin adoption for mission rehearsal

- 4.2.4 Cloud-native range delivery lowers TCO for SMEs

- 4.2.5 Generative-AI powered threat emulation accelerators

- 4.2.6 Integration with 5G/OT testbeds for converged security

- 4.3 Market Restraints

- 4.3.1 High capital outlay for immersive physical ranges

- 4.3.2 Shortage of skilled cyber-range content developers

- 4.3.3 Inter-operability gaps between proprietary range stacks

- 4.3.4 Data-sovereignty concerns in cross-border range sharing

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Range Type

- 5.2.1 Simulation Range

- 5.2.2 Emulation Range

- 5.2.3 Hybrid Range

- 5.2.4 Overlay Range

- 5.3 By Deployment Mode

- 5.3.1 On-Premises

- 5.3.2 Cloud-Based

- 5.3.3 Hybrid

- 5.4 By End-user

- 5.4.1 Defense and Security Agencies

- 5.4.2 BFSI

- 5.4.3 IT and Telecom

- 5.4.4 Healthcare

- 5.4.5 Industrial and Critical Infrastructure

- 5.4.6 Academic and Training Institutes

- 5.4.7 Other End-users

- 5.5 By Application

- 5.5.1 Training and Certification

- 5.5.2 Threat Intelligence and Analysis

- 5.5.3 Research and Development / Testing

- 5.5.4 Compliance and Assessment

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Singapore

- 5.6.4.7 Malaysia

- 5.6.4.8 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 SimSpace Corporation

- 6.4.2 Cyberbit Ltd.

- 6.4.3 RangeForce Inc.

- 6.4.4 Immersive Labs Ltd.

- 6.4.5 Circadence Corporation

- 6.4.6 ThreatGEN LLC

- 6.4.7 Offensive Security Services, LLC

- 6.4.8 Raytheon Intelligence and Space

- 6.4.9 Lockheed Martin Corporation

- 6.4.10 Northrop Grumman Corporation

- 6.4.11 CAE Inc.

- 6.4.12 L3Harris Technologies, Inc.

- 6.4.13 IBM Corporation

- 6.4.14 Airbus Defence and Space SAS

- 6.4.15 Atos SE

- 6.4.16 Science Applications International Corp.

- 6.4.17 Leidos Holdings, Inc.

- 6.4.18 Thales Group

- 6.4.19 Mandiant (a Google LLC company)

- 6.4.20 Palo Alto Networks, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment