|

시장보고서

상품코드

2062115

은 페이스트 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Silver Paste - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

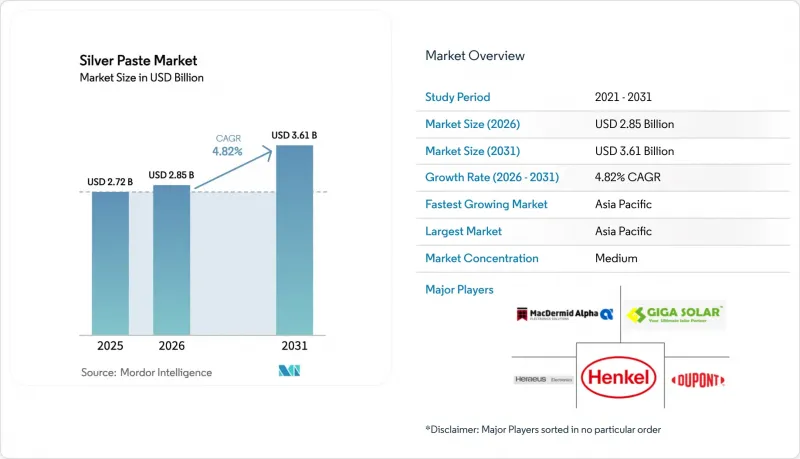

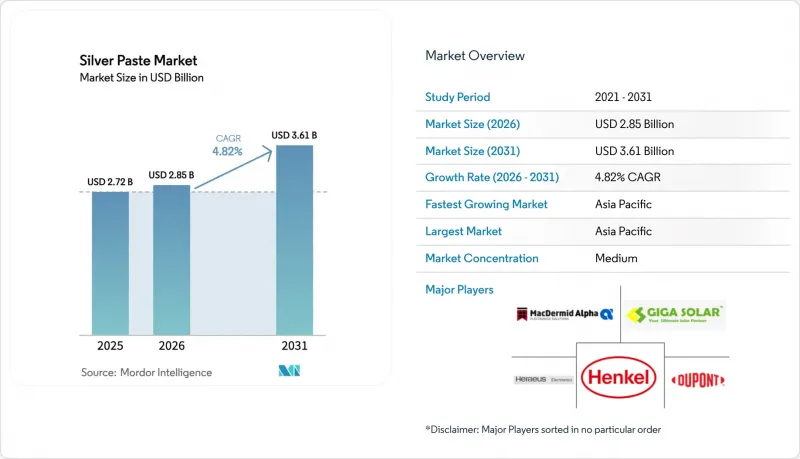

Mordor Intelligence에 의하면, 은 페이스트 시장 규모는 2025년에 27억 2,000만 달러로 평가되었고 2026년 28억 5,000만 달러에서 2031년까지 36억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.82%를 나타낼 전망입니다.

본 보고서는 기판(세라믹, 유리, 금속, 폴리머), 조성(은 플레이크, 은 나노 입자, 은 분말, 기타 조성), 용도(태양광 발전, 자동차용 전자기기 및 EV 파워 모듈, 소비자용 전자기기, 집적 회로, 기타 용도), 지역(아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 은 페이스트 시장 동향 및 인사이트

자동차 및 전기차 분야의 파워 일렉트로닉스 통합 확대

2025년까지 배터리 전기자동차(BEV)의 은 소비량이 내연기관(ICE) 차량을 넘어섰습니다. 현재, IATF 16949의 신뢰성 기준을 충족하는 소결 은 접합부는 -40°C에서 175°C 범위 내에서 수천 회의 열 사이클을 견딜 수 있습니다. 2025년 6월, LG화학과 노리타케는 상온에서 안정된 나노 은 페이스트를 발표했습니다. 이 획기적인 기술 덕분에 페이스트의 유통기한이 불과 몇 주에서 몇 달로 연장되어 콜드체인 물류의 필요성이 사라졌습니다. 그 결과, 1차 공급업체들은 금속 선물 시세에 연동된 다년 계약을 점점 더 많이 선택하고 있으며, 이는 은 페이스트 분야의 새로운 전략입니다. 또한, 가혹한 사이클 시험 후에도 전단 강도가 유지된다는 사실이 입증됨에 따라, 구동용 인버터에 SiC를 채택하는 사례가 급격히 증가하고 있습니다. 이러한 발전은 자동차용 은 페이스트 수요를 견인하며, 유능한 공급업체들에게 안정적인 이익률 성장을 뒷받침하고 있습니다.

인쇄 및 플렉서블 전자 제품 제조의 급성장

웨어러블 의료용 패치, 곡면 디스플레이 및 폴리머 기판은 현재 보호를 위해 150°C 미만의 온도에서 경화되는 전도성 트레이스에 의존하고 있습니다. 투명 은 페이스트는 140°C에서 20분간 경화시켜 낮은 시트 저항을 구현함으로써, 인셀 OLED 드라이버의 통합을 용이하게 합니다. 한편, 구리-은 코어-쉘 잉크는 은의 사용량을 대폭 줄이면서도 거의 동등한 수준의 전도성을 달성하고 있습니다. 이러한 변화로 인해, 배합 설계자들은 순은계 시스템을 성능이 최우선인 설계에만 한정하여 사용하고 있습니다. 은 페이스트 시장은 고성능 틈새 분야에 힘입어 가치가 상승하고 있지만, 재료 효율의 향상으로 인해 그 수량 증가세는 디바이스 생산량 증가세를 따라잡지 못하고 있습니다. 스마트 패키징, 구조용 센서, 폴더블 스마트폰의 생산 대수가 급증했음에도 불구하고, 톤수 기준 증가는 미미한 수준에 그치고 있습니다. 그러나 평균 판매 가격의 상승에 힘입어 매출 증가율은 톤수 기준 증가율을 상회하고 있습니다.

저비용 구리(Cu)/알루미늄(Al) 전도성 소재와의 경쟁

중국의 태양전지 제조업체는 은도금 구리의 시범 생산을 실험실에서 생산 라인으로 전환하여, 효율을 저하시키지 않으면서 TOPCon 웨이퍼 1장당 은 사용량을 줄이는 데 성공했습니다. LONGi가 핑거(finger) 부분에 완전 구리 도금을 채택한 것은 모듈 1장당 은 사용량이 줄어들 가능성이 있음을 시사합니다. 마찬가지로 RFID 기술, 터치스크린, 일회용 센서 분야에서도 전기적 기준을 충족하면서도 비용을 대폭 절감할 수 있는 구리 하이브리드 잉크로의 전환이 진행되고 있습니다. 태양광 발전 분야에서는 매출이 직접적으로 감소하고 있는 한편, 더 광범위한 은 페이스트 시장도 영향을 받고 있어, 배합 제조업체들은 현재 혁신을 추구할 것인지, 아니면 상품화 위험에 직면할 것인지라는 중대한 선택의 기로에 서 있습니다.

부문별 분석

2025년에는 200 W/m*K를 초과하는 본딩 라인의 전도성이 필요한 직접 본딩 구리 파워 모듈에 대한 견조한 수요에 힘입어, 세라믹이 매출의 45.11%를 차지했습니다. 이 부문은 2025년 은 페이스트 시장 점유율에서 선두를 차지했습니다. 한편, 폴리머 기판은 플렉서블 센서, 스마트 텍스타일, 폴더블 디스플레이 분야에서 차지하는 역할 덕분에 2026년부터 2031년까지의 예측 기간 동안 기판 부문 중 가장 높은 연평균 성장률(CAGR)인 5.33%를 기록했습니다.

250°C를 넘는 온도를 견디고 최대 10kV의 전기 절연성을 제공하는 세라믹는 전기차(EV)용 인버터 및 산업용 드라이브 분야에서 확고한 입지를 다지고 있습니다. 그러나 폴리이미드 및 폴리에틸렌 테레프탈레이트(PET)의 형태에 대한 혁신을 통해, 기존의 후막 하이브리드 회로 분야를 뛰어넘는 새로운 시장이 개척되었습니다. 배합 제조업체가 저온 경화형 화학 기술을 도입함에 따라, 건전한 이익률을 유지하면서도 폴리머의 사용량이 크게 증가했습니다. 이러한 성장은 특히 플렉서블 전자 분야를 중심으로 은 페이스트 시장에 뚜렷한 혜택을 가져다주고 있습니다.

지역별 분석

2025년, 아시아태평양은 은 페이스트 시장을 주도하며 매출의 64.11%를 차지하고, 6.33%의 성장률을 보일 것으로 전망됩니다. 2025년, 차세대 TOPCon 라인으로의 전환에 힘입어 중국의 은 페이스트 국내 판매량이 급격히 증가했습니다. 2029년까지 은 분말의 생산 능력이 상당한 수준에 도달할 것으로 예상에 따라, 해당 지역은 공급 회복력을 강화하는 한편, 지정학적 리스크 증가에도 직면하게 될 것입니다.

기술 혁신 측면에서는 일본이 주도적인 입장에 있습니다. 독자적인 분무화 기술을 활용하는 주요 기업들이 시장을 독점하고 있으며, 전 세계 태양광용 은 분말의 50% 이상을 공급하고 있습니다. 동시에, 교세라, 타나카, 아사히 화학 등 업계 선도 기업들이 최전선에 나서, 240 W/m*K를 넘는 열전도율을 지닌 특수 페이스트를 제공합니다. 한국에서는 LG화학과 노리타케의 제휴가, 국내에서 확대되고 있는 전기차 배터리 시장을 배경으로 자동차용 SiC 부착 부품 분야 진출을 목표로 하고 있습니다. 한편, 인도와 아세안(ASEAN) 국가들은 범용 태양광 페이스트의 경제적인 조립 거점 역할을 하고 있지만, 고순도 나노 파우더 수입에 대한 의존도가 높기 때문에 당분간 업스트림 공정에서의 다각화 여지는 제한적임이 드러나고 있습니다.

북미는 혁신적인 발전을 통해 입지를 다지고 있습니다. 인듐 코퍼레이션과 맥더미드 알파는 제품 포트폴리오를 확대하고 무가압 소결 기술을 도입했습니다. 한편, 헨켈은 스코프 3 지속가능성 기준을 준수하는 재활용 은을 사용한 잉크를 도입했습니다. 유럽은 보다 신중한 입장을 취하고 있으며, 화장품에 나노 은의 사용을 금지하고 있고, 유럽식품안전청(EFSA)이 발표한 E 174에 관한 경고를 유념하고 있습니다. 이러한 규제 움직임은 직장에서의 광범위한 노출을 억제하는 것을 목적으로 하며, EU 공급업체들에게 ‘설계 단계부터의 안전성 확보(safe-by-design)’ 전략의 도입을 촉구하고 있습니다. 보쉬(Bosch)와 ZF의 인버터 제품 라인에 힘입어 독일은 유럽 내 주요 양산 업체로 부상하고 있습니다. 반면, 남미와 중동에서는 태양광 발전 사업에서 주로 수입 페이스트에 의존하고 있습니다. 이 지역들은 향후 성장이 기대되지만, 현재로서는 은 페이스트 시장에 큰 수익적 영향을 미치고 있지 않습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the silver paste market size was valued at USD 2.72 billion in 2025 and is estimated to grow from USD 2.85 billion in 2026 to reach USD 3.61 billion by 2031, at a CAGR of 4.82% during the forecast period (2026-2031).

This report is Segmented by Substrate (Ceramic, Glass, Metal, and Polymer), Composition (Silver Flakes, Silver Nanoparticles, Silver Powders, and Other Compositions), Application (Photovoltaics, Automotive Electronics and EV Power Modules, Consumer Electronics, Integrated Circuits, and Other Applications), and Geography (Asia-Pacific, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Silver Paste Market Trends and Insights

Expansion of Automotive and Electric Vehicle Power-Electronics Integration

By 2025, battery-electric vehicles (BEVs) outpaced their internal-combustion engine (ICE) counterparts in silver consumption. Sintered-silver joints, now meeting IATF 16949 reliability standards, endure thousands of thermal cycles, spanning from -40 °C to 175 °C. In June 2025, LG Chem and Noritake introduced a room-temperature-stable nano-silver paste. This breakthrough extends the paste's shelf life from mere weeks to several months, negating the necessity for cold-chain logistics. Consequently, Tier 1 suppliers are increasingly opting for multi-year offtake agreements tied to metal futures - a fresh strategy in the silver paste arena. Moreover, with shear-strength retention proving resilient post-rigorous cycling, there is a marked surge in SiC adoption for traction inverters. These advancements are propelling the demand for automotive silver paste and bolstering consistent margin growth for adept suppliers.

Boom in Printed and Flexible Electronics Manufacturing

Wearable medical patches, curved displays, and polymer substrates now depend on conductive traces that cure at temperatures below 150 °C for their protection. Transparent silver pastes, after a 20-minute cure at 140 °C, achieve low sheet resistance, facilitating in-cell OLED driver integration. Meanwhile, copper-silver core-shell inks reach nearly identical conductivity levels but with a marked reduction in silver usage. This shift encourages formulators to reserve pure-silver systems for designs prioritizing performance. Although the silver paste market has seen a value boost from high-performance niches, its volume growth has not kept pace with device output, thanks to strides in material efficiency. Even as unit counts have surged in smart packaging, structural sensors, and foldable smartphones, leading to only modest tonnage increases, revenue growth has outstripped tonnage, fueled by rising average selling prices.

Competition from Lower-Cost Cu/Al Conductive Materials

Chinese cell manufacturers have transitioned silver-coated copper pilots from laboratories to production lines, successfully reducing silver usage per TOPCon wafer without compromising efficiency. LONGi's adoption of fully copper-electroplated fingers indicates a potential reduction in silver usage per module. Similarly, RFID technology, touch screens, and disposable sensors are shifting toward copper-hybrid inks, meeting electrical standards while significantly reducing costs. While photovoltaics experience a direct revenue dip, the broader silver paste market is also impacted - formulators now face a critical choice between pursuing innovation and confronting the risk of commoditization.

Other drivers and restraints analyzed in the detailed report include:

- Shift to Sintered-Silver Attach in SiC/GaN Power Devices

- Emergence of Low-Temperature Ag2O Pastes for Wearables and µLEDs

- Supply-Chain Risk from Limited Silver-Paste Recycling Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, ceramics, driven by robust demand for direct-bonded-copper power modules requiring bondline conductivity exceeding 200 W/m*K, accounted for 45.11% of the revenue. This segment led the silver paste market share in 2025. Meanwhile, polymer substrates, due to their roles in flexible sensors, smart textiles, and foldable displays, recorded a 5.33% compound annual growth rate (CAGR) - the highest among substrates during the forecast period of 2026-2031.

Withstanding temperatures exceeding 250 °C and offering electrical isolation up to 10 kV, ceramics have cemented their position in electric vehicle (EV) inverters and industrial drives. However, innovations in form factors for polyimide and polyethylene terephthalate (PET) have tapped into a new market, surpassing the conventional thick-film hybrid-circuit sector. As formulators introduced low-temperature curing chemistries, polymer adoption increased significantly, all while maintaining healthy profit margins. This growth has notably benefited the silver paste market, particularly in the flexible electronics segment.

Geography Analysis

In 2025, the Asia-Pacific region dominated the silver paste market, accounting for 64.11% of the revenue and projecting a growth rate of 6.33%. In 2025, driven by advancements to next-generation TOPCon lines, China's domestic sales of silver paste saw a notable surge. By 2029, as silver-powder production capacity is set to reach significant levels, the region not only solidifies its supply resilience but also faces heightened geopolitical risks.

Japan leads in technological innovations. A prominent company, utilizing proprietary atomization, dominates the market, supplying over 50% of the global PV-grade silver powder. Simultaneously, industry leaders like Kyocera, TANAKA, and Asahi Kagaku are at the forefront, offering specialty pastes with conductivity levels surpassing 240 W/m*K. In South Korea, LG Chem and Noritake's partnership is eyeing the automotive SiC attachment, leveraging the country's expanding EV battery landscape. While India and ASEAN nations act as economic assembly centers for commodity solar pastes, their dependence on imports for high-purity nanopowders highlights a limited scope for upstream diversification in the foreseeable future.

North America is establishing its presence through innovative strides. Indium Corporation and MacDermid Alpha have expanded their portfolios to include pressureless sintering. Meanwhile, Henkel has introduced inks with recycled silver, aligning with Scope 3 sustainability benchmarks. Europe adopts a more cautious stance, implementing bans on nano-silver in cosmetics and heeding the European Food Safety Authority's warnings about E 174. This regulatory push aims to curtail broader workplace exposures, prompting EU suppliers to adopt 'safe-by-design' strategies. Germany, fortified by Bosch and ZF's inverter lines, emerges as Europe's dominant volume player. Conversely, South America and the Middle-East predominantly depend on imported pastes for their photovoltaic initiatives. Although these regions hold promise for future growth, they currently lack significant revenue impact on the silver paste market.a

- ANP CORPORATION

- artience Co., Ltd

- Bando Chemical Industries Ltd.

- CAPLINQ Corporation

- DAIKEN CHEMICAL

- DuPont

- Dycotec Materials Ltd.

- Giga Solar Materials Corp.

- Henkel AG & Co. KGaA

- Heraeus Electronics

- Indium Corporation

- Jiangsu Hoyi Technology Co. Ltd.

- Kyocera Corporation

- LEED-INK

- LG Chem

- MacDermid Alpha Electronics Solutions

- NORITAKE CO., LIMITED

- Shanghai EqualOcean Technology Co., Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of automotive and Electric Vehicle power-electronics integration

- 4.2.2 Boom in printed and flexible electronics manufacturing

- 4.2.3 Shift to sintered-silver attach in SiC/GaN power devices

- 4.2.4 Emergence of low-temperature Ag2O pastes for wearables and µLEDs

- 4.2.5 Circular-economy push for silver-paste recovery and recycling

- 4.3 Market Restraints

- 4.3.1 Competition from lower-cost Cu/Al conductive materials

- 4.3.2 Supply-chain risk from limited silver-paste recycling capacity

- 4.3.3 Stringent environmental regulations on nano-silver emissions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Substrate

- 5.1.1 Ceramic

- 5.1.2 Glass

- 5.1.3 Metal

- 5.1.4 Polymer

- 5.2 By Composition

- 5.2.1 Silver Flakes

- 5.2.2 Silver Nano Particles

- 5.2.3 Silver Powders

- 5.2.4 Other Composition

- 5.3 By Application

- 5.3.1 Photovoltaics (Solar Cells)

- 5.3.2 Automotive Electronics and EV Power Modules

- 5.3.3 Consumer Electronics (displays, wearables)

- 5.3.4 Integrated Circuits and Semiconductors

- 5.3.5 Other Applications (RFID, LEDs, medical devices)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ANP CORPORATION

- 6.4.2 artience Co., Ltd

- 6.4.3 Bando Chemical Industries Ltd.

- 6.4.4 CAPLINQ Corporation

- 6.4.5 DAIKEN CHEMICAL

- 6.4.6 DuPont

- 6.4.7 Dycotec Materials Ltd.

- 6.4.8 Giga Solar Materials Corp.

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Heraeus Electronics

- 6.4.11 Indium Corporation

- 6.4.12 Jiangsu Hoyi Technology Co. Ltd.

- 6.4.13 Kyocera Corporation

- 6.4.14 LEED-INK

- 6.4.15 LG Chem

- 6.4.16 MacDermid Alpha Electronics Solutions

- 6.4.17 NORITAKE CO., LIMITED

- 6.4.18 Shanghai EqualOcean Technology Co., Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment