|

시장보고서

상품코드

2062121

녹 제거게 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Rust Remover - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

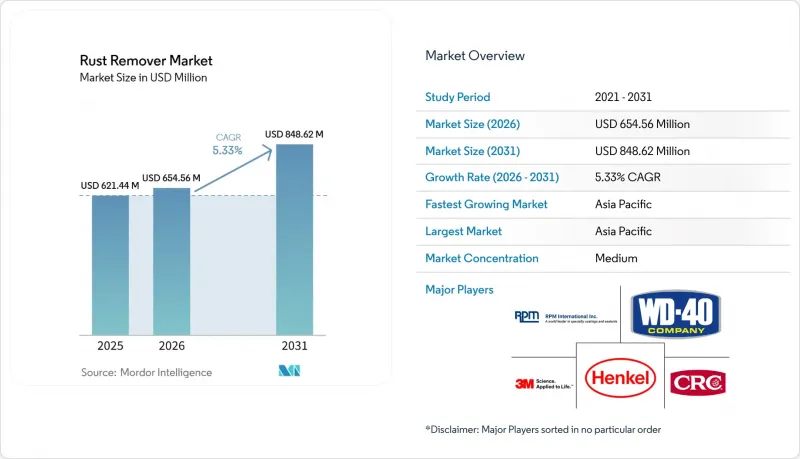

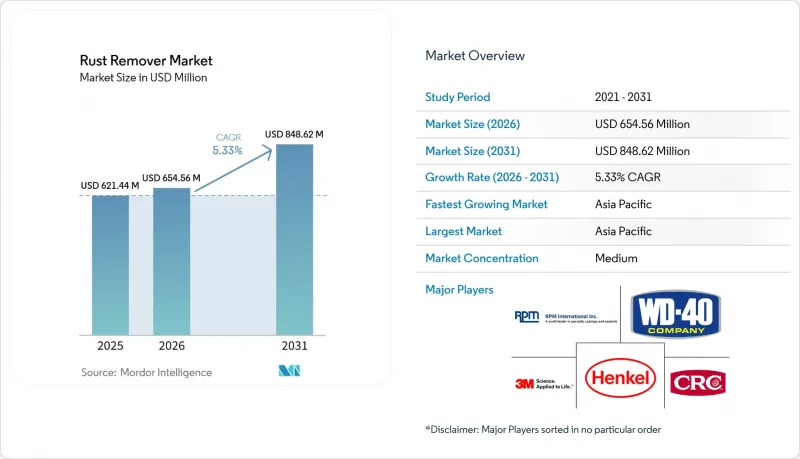

Mordor Intelligence에 의하면, 녹 제거게 시장 규모는 2025년 6억 2,144만 달러에서 2026년에는 6억 5,456만 달러로 확대되어 2031년까지 8억 4,862만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 5.33%로 성장할 전망입니다.

본 보고서는 유형별(산성 녹 제거제, 중성 pH/킬레이트계 녹 제거제, 바이오계 녹 제거제), 형태별(액체, 젤, 스프레이, 와이프), 최종 사용자 산업별(자동차, 건설, 산업용 기계·설비 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 녹 제거제 시장 동향 및 인사이트

신흥국에서의 제조업 확대와 인프라 구축

인도, 베트남, 인도네시아, 멕시코에서의 산업 확장은 예방적 표면 처리 시장의 성장으로 이어지고 있습니다. 인도에서는 고속도로, 지하철, 항만 프로젝트에서 철근 및 거더의 부식 방지 대책이 의무화되어 있습니다. 이로 인해 현장에서 사용되는 이동식 분무 장치에 적합한 액상 농축제에 대한 안정적인 수요가 발생하고 있습니다. 베트남의 전자 산업 단지에서는 염분이 포함된 습기를 차단하기 위해 폴리우레아 배리어가 도입되었습니다. 그러나 정기적인 가동 중단 시에는 여전히 화학적 녹 제거가 필요합니다. 이 지역이 경제에 영향을 미치는 심각한 부식 관련 손실에 직면해 있다는 점을 고려할 때, 이는 매우 중요합니다. 멕시코에서는 니어쇼어링의 추세에 따라 공구 및 금형 유지보수 수요가 증가하고 있습니다. 한편, 브라질에서는 국산 농업 기계에 대한 세제 혜택 덕분에 수리 공장에는 젤 제품이 충분히 비축되어 있습니다. 이러한 겔은 대형 주물에도 흘러내리지 않고 밀착되기 때문에 특히 유용합니다. 이러한 동향들이 맞물려 녹 제거제 시장을 공고히 하고 있으며, 상품 가격이 하락하는 국면에서도 판매량 성장을 견고하게 뒷받침하고 있습니다.

저VOC 및 바이오 화학물질에 대한 규제 추진

2025년 1월, 미국 환경보호청(EPA)은 새로운 에어로졸 도료 규정을 도입했습니다. 이 규정은 부식 변환제의 제품 가중 반응성을 제한하며, 일정 기준치를 초과하는 휘발성 유기 화합물(VOC)이 존재하는 경우 이를 전자적으로 공개하도록 의무화하고 있습니다. 용매가 목록에 기재되어 있지 않은 경우, 자동으로 막대한 벌금이 부과되므로 기존의 많은 탄화수소계 용매의 사용은 현실적으로 불가능해집니다. 한편, 옥수수나 카사바의 당분을 원료로 하는 구연산계 시스템은 동등한 밀 스케일 제거 효과를 얻을 수 있습니다. 이 시스템은 연기가 거의 발생하지 않으며, 잔탄검과 혼합하면 흘러내리지 않는 겔을 형성하여 수직면에 한 번만 도포하기에 적합합니다. 한편, 유럽연합(EU)의 화학물질 등록·평가·허가·제한(REACH) 규정과 중국 생태환경부의 기준에 따른 규제 강화는 전 세계 공급업체에 더 큰 압박을 가하고 있습니다. 공급업체들은 다양한 관할권의 요구 사항을 충족할 수 있는 통합된 배합 포트폴리오로 점차 전환하고 있습니다. 이러한 변화는 경쟁 구도를 재편하고 있습니다. 오늘날에는 확실한 분석 보고서, 철저한 휘발성 유기 화합물 추적, 그리고 바이오 원료에 대한 접근성이 리터당 가격만큼이나 필수적입니다.

기계적 및 코팅 기반의 대안

전기차 배터리 케이스에는 휘발성 유기 화합물(VOC)을 전혀 배출하지 않고 폐기물도 거의 발생하지 않는 분체 도장이 점점 더 많이 채택되고 있습니다. 이러한 변화로 인해 자동차 제조업체들은 기존의 녹 제거와 재도장이라는 순차적 공정에서 벗어나도록 요구받고 있습니다. 악소노벨(AkzoNobel)이 제조업체를 대상으로 실시한 조사에 따르면, 상당수의 전기차 제조업체가 현재 분체 도장을 지정하고 있으며, 그 도입률은 자동차 업계 전체의 도입률보다 약간 높은 것으로 나타났습니다. 플라즈마트리트(Plasmatreat)사의 ‘AntiCorr’는 플라즈마 강화 변환 코팅으로, 기존의 화학 약품 욕조를 완전히 배제하고 얇은 실록산 층을 직접 형성합니다. 아연 도금 강판 및 알루미늄의 사용이 확대됨에 따라, 과거 녹 제거제 시장의 주류를 이루던 일반 철판의 재고가 감소하고 있으며, 시장의 기준이 되는 판매량도 줄어들고 있습니다.

부문별 분석

산성 녹 제거제는 2025년 매출의 52.12%를 차지했으나, 기존 방식은 기존의 유지보수 매뉴얼의 기반이 되고 있으며 두꺼운 녹 제거에 적합합니다. 한편, 환경 규제로 인한 규정 준수 비용 증가로 인해 구매자들은 미국 농무부(USDA)로부터 완전 바이오 인증을 획득한 구연산계 시스템으로 점차 전환하고 있습니다. 바이오 솔루션 시장은 2026년부터 2031년 사이에 연평균 성장률(CAGR) 5.81%로 성장할 것으로 전망됩니다. 수소 취성을 우려하는 항공우주 정비 기지들은 부식 제거제 시장에서의 점유율을 서서히 확대되고 있습니다. 여전히 틈새 시장인 것은 사실이지만, 중성 pH의 킬레이트제는 문화재 보존 및 전자기기 조립 분야에서 고수익 계약을 수주하고 있으며, 이러한 분야에서는 금속 표면의 정밀도가 요구되기 때문에 반응 속도가 느린 단점이 상쇄되고 있습니다.

예측 기간 동안, 녹 제거제 내 킬레이트제 배합 시장 규모는 비록 소규모 기반에서 출발하긴 하지만, 꾸준히 확대될 것으로 전망됩니다. 중장비 개조 분야에서는 여전히 산성 제품이 주류를 이루고 있지만, 입찰 비교 과정에서 추가적인 개인보호구(PPE), 배연 설비, 유해 폐기물 관리에 드는 비용이 부각되면서 총소유비용(TCO)의 격차가 점차 좁혀지고 있습니다. 현재 각 공급업체들은 성능과 규제 준수 사이의 균형을 맞추기 위해, 산을 이용한 예비 세척과 킬레이트제를 이용한 마무리 세척을 결합한 하이브리드 키트를 제공하고 있으며, 업계에서 강산만을 사용하는 방식에서 벗어나도록 촉진하고 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 45.12%를 차지하고 있으며, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.11%를 나타낼 것으로 전망됩니다. 용접과 전착 도장 공정 사이에 인라인 분무 인산 처리를 도입한 중국의 자동차 생산 라인에서는 매일 막대한 양의 약제가 소비되고 있습니다. 바이오산으로의 전환이 미미하더라도, 사용량 증가로 이어집니다. 인도에서는 구간별로 대량의 철근을 사용하는 바라트마라 고속도로 회랑의 시공사가 도로교통부의 지침을 준수하기 위해 방청 처리를 의무화하고 있습니다. 부식으로 인한 경제적 손실이 막대한 베트남에서는 해사 분야에서 중성 pH 겔에 대한 수요가 증가하고 있습니다. 이 젤들은 선체 유지보수 시 잠수 작업 시간을 단축시켜 줍니다. 한편, 동남아시아국가연합(ASEAN)의 외국인 직접 투자 우대 조치가 부품 공급업체들을 끌어들이고 있습니다. 이 공급업체들은 저휘발성 유기화합물(VOC) 함유 액상 제제를 도입함으로써 유럽 수출을 위한 체제를 구축하고, 지역 간 배합 조화를 추진하고 있습니다.

북미에서는 미국 환경보호청(EPA)의 전자 보고 의무화로 인해 시장 점유율이 구연산, 글루콘산 및 기타 저자극성 산으로 이동하고 있습니다. 멕시코만 해양 시설 해체 입찰에서는 전체 수명 주기의 배출량이 고려되게 되면서, 리터당 비용이 높아지더라도 킬레이트제 수요가 증가하고 있습니다. 게다가, 미국 내 DIY 문화의 확산으로 인해 소셜 미디어에 올라온 방청 팁 영상들이 주말 소매 판매 활성화로 이어지고 있습니다.

유럽은 성숙한 시장임에도 불구하고, 여전히 순환형 경제 지표에 중점을 두고 있습니다. 『Journal of Coatings Technology and Research』지의 조사에 따르면, 프로젝트 지출의 대부분은 건강·안전·환경(HSE) 관련 비용이 차지하고 있는 것으로 지적되고 있습니다. 이러한 추세에 따라 자산 소유자들은 개입 빈도를 줄일 수 있고 내구성이 뛰어나며 유지보수 부담이 적은 도료로 점차 전환하고 있습니다. 부식 방지 효과에 더해 플래시(급격한 부식) 방지 기능까지 제공하는 공급업체는 경쟁 우위를 확보하고 있으며, 비계 설치 주기를 한 번 줄일 수 있다는 점은 유럽연합(EU) 입찰에서 큰 강점이 됩니다.

남미, 중동 및 아프리카는 시장 점유율은 작지만 급속한 성장이 예상되는 지역입니다. 브라질에서는 대두 수확기가 부식성 비료 분진으로 인한 문제에 직면해 있습니다. 한편, 사우디아라비아에서는 해수 담수화 플랜트에서 염분 농도가 높은 환경 하의 스테인리스 배관을 관리하고 있습니다. 정치적 리스크나 환율 변동으로 인해 예측하기 어렵지만, 현지 블렌딩 플랜트의 도입이 해결책이 될 것입니다. 이러한 플랜트는 수입 관세와 리드 타임을 줄여주어, 기동성이 뛰어난 기업들에게 더 큰 경쟁 우위를 제공합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the rust remover market size is expected to increase from USD 621.44 million in 2025 to USD 654.56 million in 2026 and reach USD 848.62 million by 2031, growing at a CAGR of 5.33% over 2026-2031.

This report is Segmented by Type (Acid-Based Rust Removers, Neutral PH/Chelate-Based Rust Removers, and Bio-Based Rust Removers), Form (Liquid, Gel, Spray, and Wipes), End-User Industry (Automotive, Construction, Industrial Machinery and Equipment, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Rust Remover Market Trends and Insights

Expansion of Manufacturing and Infrastructure Rehabilitation in Emerging Economies

Industrial expansions in India, Vietnam, Indonesia, and Mexico are broadening the market for preventive surface treatments. In India, highway, metro, and port projects mandate corrosion protection for steel rebar and girders. This creates a consistent demand for liquid concentrates compatible with mobile spray rigs at job sites. Vietnam's electronics hubs deploy polyurea barriers to combat salt-laden humidity. However, they still require chemical rust removal during scheduled shutdowns. This is crucial, considering the region faces significant corrosion-related losses impacting its economy. In Mexico, the trend of near-shoring boosts the demand for tooling and mold maintenance. Meanwhile, in Brazil, tax incentives for domestically produced farming equipment ensure repair shops are well-stocked with gel products. These gels are particularly advantageous as they adhere to large castings without runoff. Together, these trends are strengthening the rust removers market, ensuring volume growth even amidst softening commodity prices.

Regulatory Push Toward Low-VOC and Bio-Based Chemistries

In January 2025, the United States Environmental Protection Agency introduced a new aerosol-coatings rule. This rule limits the product-weighted reactivity for rust converters and requires any volatile organic compound present above a certain threshold to be disclosed electronically. If a solvent is not listed, it automatically incurs a significant penalty, making many traditional hydrocarbon carriers impractical. On the other hand, citric-acid systems, derived from corn or cassava sugar, can achieve similar mill-scale removal. These systems produce minimal fumes and, when combined with xanthan gum, create drip-resistant gels suitable for a single vertical coat application. Meanwhile, tightening regulations under the European Union's Registration, Evaluation, Authorization, and Restriction of Chemicals and China's Ministry of Ecology and Environment standards further push global suppliers. They are increasingly moving towards unified formula portfolios that can meet the demands of various jurisdictions. This shift is reshaping the competitive landscape: now, having robust analytical reporting, meticulous volatile organic compound tracking, and access to biobased feedstocks are just as vital as pricing per liter.

Mechanical and Coating-Based Substitutes

Electric-vehicle battery enclosures are increasingly opting for powder coatings, which offer a zero-volatile organic compound application and generate nearly zero waste. This shift is enticing original equipment manufacturers to move away from traditional methods of sequential rust removal and repainting. A survey by AkzoNobel, encompassing manufacturers, revealed that a significant portion of electric vehicle producers now specify powder coatings, slightly outpacing the adoption rate seen in the broader automotive sector. Plasmatreat's AntiCorr, a plasma-enhanced conversion coating, directly applies thin siloxane layers, completely sidestepping traditional chemical baths. With the growing adoption of galvanized steel and aluminum, the once-dominant inventory of bare ferrous surfaces central to the rust removers market has diminished, eroding the market's baseline volume.

Other drivers and restraints analyzed in the detailed report include:

- Refurbishment of Decommissioned Offshore Oil and Gas Platforms

- Pre-Treatment Demand for Green-Hydrogen Electrolyzer Components

- Geopolitical Volatility in Phosphoric and Citric Acid Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acid-Based Rust Removers maintained a 52.12% slice of 2025 revenue, while traditional methods anchor legacy maintenance manuals and facilitate heavy-scale removal, rising compliance costs tied to environmental regulations are steering buyers towards citric systems, proudly boasting a certification as fully biobased by the United States Department of Agriculture. Bio-based solutions are projected to expand at 5.81% CAGR between 2026 and 2031. Aerospace maintenance depots, wary of hydrogen embrittlement, are progressively boosting their share of the rust removers market. While still a niche, neutral-pH chelates are securing high-margin contracts in heritage preservation and electronics assembly, where the need for bare-metal precision compensates for their slower kinetics.

Over the forecast period, the market for chelate formulations in rust removers is projected to grow steadily, albeit from a modest base. While acid products continue to dominate heavy machinery refurbishment, the visible costs of additional personal protective equipment, fume extraction, and hazardous waste management are becoming evident in bid comparisons, tightening total cost of ownership gaps. Suppliers are now offering hybrid kits, combining acid pre-wash with chelate polish, to balance performance with regulatory comfort, easing the industry's shift away from a strong-acid-only approach.

Geography Analysis

Asia-Pacific accounted for 45.12% of 2025 revenue and is on track for a 6.11% CAGR between 2026 and 2031. Chinese automotive production lines, which employ inline spray phosphates between welding and e-coating, drain significant volumes daily. Even a small shift towards bio-acids leads to an increase in volume. In India, contractors on the Bharatmala highway corridors, which use large amounts of reinforcing bar per stretch, specify rust treatments to align with the Ministry of Road Transport guidelines. Vietnam, dealing with substantial corrosion losses as a share of its economy, witnesses growing demand in its maritime sector for neutral-pH gels. These gels reduce diver time during hull maintenance. Meanwhile, foreign direct investment incentives from the Association of Southeast Asian Nations attract component suppliers. By adopting low-volatile organic compound liquids, these suppliers position themselves for European exports, advancing cross-regional formulation harmonization.

In North America, the Environmental Protection Agency's electronic-reporting mandate shifts market shares towards citric, gluconic, and other benign acids. Offshore decommissioning bids in the Gulf of Mexico now account for total lifecycle emissions, driving up chelate demands, even at a higher per-liter cost. Furthermore, a strong do-it-yourself culture in the United States sees social-media rust-hack videos translating into active weekend retail sales.

Europe, despite its maturity, remains focused on circular-economy metrics. A study from the Journal of Coatings Technology and Research pointed out that health, safety, and environmental access expenses dominate project spending. This trend nudges asset owners towards durable, low-maintenance coatings that reduce intervention frequency. Suppliers who offer rust removal alongside flash-inhibition gain a competitive edge, saving an extra scaffold cycle a significant advantage in European Union bidding.

While South America and the Middle-East and Africa command smaller market shares, they exhibit areas of rapid growth. In Brazil, soy harvesters face challenges with corrosive fertilizer dust. Meanwhile, in Saudi Arabia, desalination plants manage high-salinity stainless piping. Although political risks and currency fluctuations complicate forecasting, the emergence of localized blending plants offers a solution. These plants reduce import duties and lead times, granting nimble players incremental advantages.

- 3M

- Advanced Protective Technologies, LLC.

- AkzoNobel NV

- BASF

- Capella Solutions Group

- Chempace

- CRC Industries

- Fuchs Petrolub SE

- GUNK

- Henkel AG & Co. KGaA

- JENOLITE

- Kao Corporation

- Permatex

- Rodda Paint, Co.

- RPM International Inc

- Star brite Inc.

- Turtle Wax Inc.

- WD-40

- Zep Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of manufacturing and infrastructure rehab in emerging economies

- 4.2.2 Regulatory push toward low-VOC and bio-based chemistries

- 4.2.3 Refurbishment of decommissioned offshore oil and gas platforms

- 4.2.4 Pre-treatment demand for green-hydrogen electrolyzer components

- 4.2.5 Robotic/laser in-line rust-removal adoption in smart factories

- 4.3 Market Restraints

- 4.3.1 Mechanical and coating-based substitutes

- 4.3.2 Geopolitical volatility in phosphoric/citric acid supply

- 4.3.3 Rise of micro-abrasive and dry-ice cleaning technologies

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Acid-Based Rust Removers

- 5.1.2 Neutral pH/Chelate-Based Rust Removers

- 5.1.3 Bio-Based Rust Removers

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Gel

- 5.2.3 Spray

- 5.2.4 Wipes

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Construction

- 5.3.3 Marine

- 5.3.4 Industrial Machinery and Equipment

- 5.3.5 Household/Consumer

- 5.3.6 Aerospace

- 5.3.7 Oil and Gas

- 5.3.8 Others

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Advanced Protective Technologies, LLC.

- 6.4.3 AkzoNobel NV

- 6.4.4 BASF

- 6.4.5 Capella Solutions Group

- 6.4.6 Chempace

- 6.4.7 CRC Industries

- 6.4.8 Fuchs Petrolub SE

- 6.4.9 GUNK

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 JENOLITE

- 6.4.12 Kao Corporation

- 6.4.13 Permatex

- 6.4.14 Rodda Paint, Co.

- 6.4.15 RPM International Inc

- 6.4.16 Star brite Inc.

- 6.4.17 Turtle Wax Inc.

- 6.4.18 WD-40

- 6.4.19 Zep Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment