|

시장보고서

상품코드

2062126

인듐 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Indium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

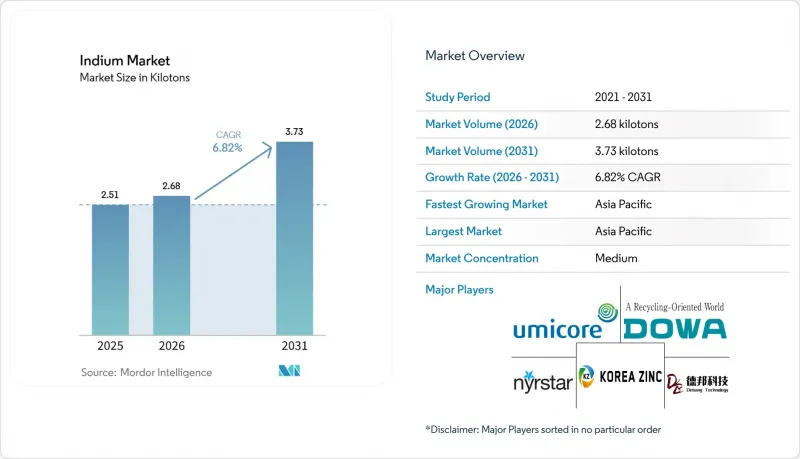

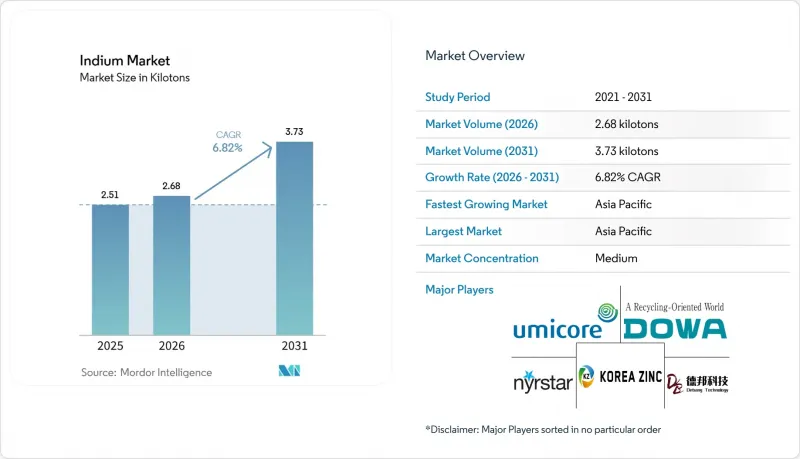

Mordor Intelligence에 의하면, 인듐 시장 규모는 2025년에 2.51 킬로톤으로 평가되었고, 2026년에 2.68 킬로톤이으로 추정되고, 2031년까지 3.73 킬로톤에 이를 것으로 예측되며, 2026-2031년 CAGR 6.82%로 성장할 전망입니다.

본 보고서는 원료별(1차 원료(아연 잔류물 정제) 및 2차 원료/재활용), 형태별(고순도 인듐 화합물 등), 용도별(평판 및 플렉서블 디스플레이 등), 최종 사용자 산업별(전자 및 반도체 등), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

세계 인듐 시장 동향 및 분석

차세대 플렉서블 및 폴더블 디스플레이에서 ITO의 활용 확대

플렉서블 OLED 및 폴더블 스마트폰 패널 분야에서는 타의 추종을 불허하는 투명성과 전도성을 갖춘 ITO(인듐 주석 산화물)가 여전히 선호되고 있습니다. 저온 스퍼터링 및 사후 어닐링 공정을 통해 굽힘 반경 5mm 미만에서도 표면 저항을 15Ω/sq 이하로 억제할 수 있게 되었으며, 다층 스택의 보급에 따라 패널당 인듐 사용량이 증가하고 있습니다. 삼성디스플레이와 BOE(베이징 동방전자)는 2025년에 각각 6세대 AMOLED(액티브 매트릭스 유기 LED) 생산 라인의 양산을 시작했으나, 이 생산 라인들은 기존의 경질 디스플레이에 비해 약 20-30% 더 많은 ITO 타겟 재료를 소비합니다. 고급 태블릿 및 자동차용 센터 정보 디스플레이에 ITZO(인듐·주석·아연 산화물) 및 ITO-은 메쉬 구조를 채택함에 따라, 낮은 공정 온도에서의 결정화를 억제하기 위해 인듐 사용량이 5-8% 더 증가했습니다. 접이식 기기의 출하 대수는 2025-2028년 3배로 증가할 것으로 예상되며, 현재의 가동률이 유지된다면 인듐의 연간 수요는 80-100톤 증가하게 될 것입니다.

첨단 패키징 및 이종 통합 분야에서 저온 인듐 합금의 확대

플립칩 볼 그리드 어레이(FPGA) 및 대형 AI 가속기 패키지에는 열전도율 71-86 W/m·K를 달성하고 1,000회의 열 사이클을 견딜 수 있는 인듐 및 인듐-은 열 인터페이스 재료가 채택되어 있습니다. SAC-In 솔더는 리플로우 온도를 15-20°C 낮추어, 복잡한 칩렛 어셈블리에서 발생하는 뒤틀림을 줄여줍니다. 파운드리 업체들은 2.5D 및 3D 스택의 보급에 따라 인듐 기반 마이크로 범프 본딩의 연간 수요가 2028년까지 40-50톤에 달할 것으로 전망하고 있습니다. 인텔과 TSMC의 로드맵에서는 저온 본딩이 수율 향상의 핵심 요소로 강조되고 있으며, 이는 해당 수요 전망을 간접적으로 뒷받침하고 있습니다.

대체 투명 전도체의 활용 가능성(그래핀, Ag-NW, CNT, IGZO)

2025년부터 시행된 중국의 인듐 화합물에 대한 미국의 관세 조치로 인해, 북미 및 유럽에서 그래핀 및 은 나노와이어(Ag-NW) 필름의 채택이 촉진되었습니다. 현재 Cambrios사와 C3Nano사의 제품은 플렉서블 기판 위에서 90% 이상의 투과율을 유지하면서도 10Ω/sq 미만의 저항값을 실현하고 있습니다. 레이저 어닐링 처리를 거친 산화 그래핀은 뛰어난 기계적 순응성을 보이지만, 비용은 스퍼터링 ITO보다 여전히 3-5배 더 비쌉니다. IGZO(산화 인듐-갈륨-아연) 백플레인은 별도의 투명 전도층이 필요 없기 때문에 패널당 인듐 사용량을 최대 20%까지 줄일 수 있습니다. 디스플레이 제조 공장은 이미 정착된 ITO 공정 흐름에 의존하고 있기 때문에 이러한 대체재 시장 점유율은 2031년까지 15% 전후에서 정체될 것으로 보입니다.

부문별 분석

2025년 기준으로 1차 생산량은 인듐 시장 규모의 67.78%를 차지했으나, 아연 광산의 품위가 정체 상태에 접어들었고 중국의 새로운 수출 허가 제도의 영향으로 성장이 억제되고 있습니다. Korea Zinc사의 74억 달러 규모 테네시 복합 시설은 지난 20년 동안 서반구에서 처음으로 이루어지는 대규모 증설 프로젝트이지만, 가동은 2029년 이후에 시작될 전망입니다. 2차 공급은 가속화되고 있으며, 중국에서는 전년 대비 268% 증가한 것으로 보고되었고, 전 세계 회수율은 15%에 육박하고 있습니다. 인듐 코퍼레이션, DOWA, 미쓰이 금속은 현재 사용 후 스퍼터링 타겟의 회수율 90%를 보장하고 있으며, 이는 순환형 경제에 따른 프리미엄이 주류로 자리 잡고 있음을 보여줍니다.

2차 원료 및 재활용 원료공급량은 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 7.22%로 증가할 것으로 예상되며, 이는 1차 원료의 2배에 달하는 속도입니다. 또한, 2031년까지 회수 효율이 50-60%에 달할 가능성이 있습니다. 바젤 협약에 따른 전자 폐기물 수출 규제와 EU 및 캘리포니아주의 확대 생산자 책임 제도로 인해, 더 많은 스크랩이 인가를 받은 정제 업체로 유입되고 있습니다. 스베르돌프사가 모델링한 200-300톤의 잠재량이 실현된다면, 재활용 흐름은 예측 수요의 약 5분의 1을 충족하게 되어 인듐 시장 규모에 가해지는 부담을 완화하는 동시에, 수명 주기 배출량을 감축하게 될 것입니다.

고순도 인듐 화합물은 2025년 인듐 시장 점유율의 45.22%를 차지한 것으로 평가되었으며, InP 레이저, InGaAs 광검출기 및 InSb 적외선 어레이에 대한 수요 급증에 힘입어 2031년까지 연평균 성장률(CAGR) 7.03%를 기록할 전망입니다. 루멘텀사의 24만 평방피트 규모의 그린즈버러 공장은 2028년에 6인치 InP 웨이퍼 양산을 시작할 예정이며, 6N-7N 등급 원료에 대한 안정적인 수요를 창출할 것으로 전망됩니다. IMEC의 'Smart Cut' 웨이퍼 회수 플랫폼은 기판 손실을 10분의 1로 줄이고, 장기적으로 금속 사용량을 절감할 것으로 기대됩니다.

잉곳, 스틱 및 합금 부문은 여전히 아연의 경제 동향에 연동되어 LME 아연 가격과 밀접하게 연동되어 거래되고 있으나, 화합물 가격은 반도체 클린룸용 순도 프리미엄(30-50%)을 반영하고 있습니다. 최대 86 W/m*K의 열전도율을 구현하는 인듐-은 합금은 AI 가속기 열 관리 분야에서 점유율을 확대되고 있습니다. 이러한 양극화된 가격 동향은 특수 광전자 부품이 인듐 시장을 순수한 금속 가격의 주기적 변동으로부터 격리시키고 있음을 여실히 보여주고 있습니다.

지역별 분석

아시아태평양은 2025년에 인듐 시장 규모의 48.66%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 7.43%를 기록하며 지역별 가장 빠른 성장세를 유지할 전망입니다. 정제 생산량의 대부분은 중국이 차지하고 있지만, 한국아연(Korea Zinc)의 국내 제련 및 윈난 주석(Yunnan Tin)의 ITO 타겟 분야에서의 기술적 진전이 공급 측면에서의 주도적 지위를 공고히 하고 있습니다. 일본의 DOWA와 미쓰이 금속은 고순도 및 재활용 제품에 주력하고 있어, 이로 인해 아연 가격 변동의 영향을 덜 받고 있습니다.

북미는 순수한 수입국에서 일부 생산국으로 전환되고 있습니다. 2029년부터 가동을 시작하는 한국아연의 클라크스빌 복합 시설과 루멘텀의 InP 레이저 제조 공장이 시너지를 발휘하여, 안정적인 지역 공급망의 기반을 마련하게 될 것입니다. 중국의 인듐 화합물에 부과된 제301조 관세(실질 세율 약 54%)는 국내 조달을 더욱 촉진하는 요인이 되고 있습니다.

유럽의 '중요 원자재법'은 지역 내 10%의 채굴과 40%의 가공을 의무화하고 있으며, 이에 따라 이탈리아는 200톤 규모의 국가 비축을 위해 4억 5,000만 유로(5억 870만 달러)를 예산에 반영했습니다. 2026년 2월에 가동을 시작한 Imec의 NanoIC 파일럿 라인은 7N 인듐 화합물에 대한 하류 수요를 더욱 촉진할 것입니다. 남미 및 중동 및 아프리카의 합계 점유율은 여전히 10% 미만이지만, 브라질과 남아프리카공화국의 유휴 아연 자산은 가격이 1kg당 500달러를 계속 상회할 경우, 필요 시 가동 가능한 유동 생산 능력이 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the indium market size is projected to be 2.51 kilotons in 2025, 2.68 kilotons in 2026, and reach 3.73 kilotons by 2031, growing at a CAGR of 6.82% from 2026 to 2031.

This report is Segmented by Source (Primary (Refined From Zinc Residues) and Secondary/Recycled), Form (High-Purity Indium Compounds, and More), Application (Flat-Panel and Flexible Displays, and More), End-User Industry (Electronics and Semiconductors, and More), and Geography (Asia Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Global Indium Market Trends and Insights

Growing Usage of ITO in Next-Gen Flexible and Foldable Displays

Flexible OLED (Organic Light Emitting Diode) and foldable smartphone panels continue to favor ITO (Indium Tin Oxide) for its unmatched transparency and conductivity. Low-temperature sputtering and post-annealing now hold sheet resistance below 15 Ω/sq at bend radii under 5 mm, raising indium intensity per panel as multilayer stacks proliferate. Samsung Display and BOE (Beijing Oriental Electronics) each ramped Gen-6 AMOLED (Active-Matrix Organic Light-Emitting Diode) lines in 2025 that consume about 20-30% more ITO target material than rigid equivalents. Adoption of ITZO (Indium-Tin-Zinc Oxide) and ITO-silver mesh architectures in premium tablets and automotive center-information displays drives an additional 5-8% indium uptake to suppress crystallization at low process temperatures. Foldable-device shipments are expected to triple between 2025 and 2028, implying 80-100 tons of incremental annual indium demand if current utilization rates persist.

Expansion of Low-Temperature Indium Alloys in Advanced Packaging and Heterogeneous Integration

Flip-chip ball-grid arrays and large-body AI accelerator packages adopt indium and indium-silver thermal interface materials that reach thermal conductivities of 71-86 W/m*K while surviving 1,000 thermal cycles. SAC-In solders lower reflow temperatures by 15-20°C, mitigating warpage in complex chiplet assemblies. Foundries expect indium-based micro-bump bonding to reach 40-50 tons of annual demand by 2028 as 2.5D and 3D stacks proliferate. Intel and TSMC roadmaps highlight low-temperature bonding as a yield enabler, indirectly validating this consumption outlook.

Availability of Alternative Transparent Conductors (Graphene, Ag-NW, CNT, IGZO)

U.S. tariffs on Chinese indium compounds, in place since 2025, boosted the adoption of graphene and silver-nanowire films in North America and Europe. Cambrios and C3Nano products now reach sub-10 Ω/sq resistances at over 90% transmittance on flexible substrates. Graphene oxide reduced by laser annealing offers superior mechanical compliance, though costs remain three to five times higher than sputtered ITO. IGZO (Indium Gallium Zinc Oxide) backplanes eliminate a separate transparent-conductor layer, cutting indium usage per panel by up to 20%. Market share of these alternatives is likely to plateau near 15 % by 2031 because display fabs rely on entrenched ITO process flows.

Other drivers and restraints analyzed in the detailed report include:

- Critical-Raw-Material Resilience Policies Boosting European Strategic Stockpiles

- Increasing Production of High-Efficiency Solar Panels Globally

- Chronic Occupational-Health Concerns Driving Stricter Exposure Limits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Primary output supplied 67.78% of the Indium market size in 2025, but growth is capped by plateauing zinc-mine grades and fresh Chinese export licensing. Korea Zinc's USD 7.4 billion Tennessee complex will be the first large-scale Western Hemisphere addition in two decades, yet commissioning will not start before 2029. Secondary supply is accelerating with 268% year-on-year gains reported in China, and global recovery yields approaching 15%. Indium Corporation, DOWA, and Mitsui Kinzoku now guarantee 90% reclaim rates on spent sputtering targets, signaling that circular-economy premiums are becoming mainstream.

Secondary/Recycled volumes are forecast to expand at a 7.22% CAGR during the forecast period (2026-2031), a rate twice that of primary material, and could touch 50-60% recovery efficiency by 2031. Basel Convention controls on e-waste exports and extended-producer-responsibility schemes in the EU and California funnel more scrap to licensed refiners. If Sverdrup's modeled 200-300 tons potential is realized, recycled flows would meet roughly one-fifth of forecast demand, easing pressure on the Indium market size while lowering life-cycle emissions.

High-purity indium compounds held 45.22% of the indium market share in 2025 and are tracking a 7.03% CAGR through 2031, buoyed by surging demand for InP lasers, InGaAs photodetectors, and InSb infrared arrays. Lumentum's 240,000 sq ft Greensboro fab begins ramping six-inch InP wafers in 2028, creating a steady pull for 6N-7N feedstock. Imec's Smart Cut wafer-reclaim platform expects to reduce substrate losses by a factor of ten, moderating long-run metal intensity.

Ingot, stick, and alloy segments remain tied to zinc economics and trade closely with LME zinc, whereas compound prices reflect semiconductor clean-room purity premiums of 30-50%. Indium-silver alloys that deliver up to 86 W/m*K are gaining share in AI accelerator thermal management. The bifurcated pricing landscape underscores how specialized optoelectronics keep the Indium market insulated from purely cyclical metals swings.

Geography Analysis

Asia Pacific controlled 48.66% of Indium market size in 2025 and will maintain the fastest regional expansion at 7.43% CAGR to 2031. China accounts for the majority of refined output, while Korea Zinc's domestic smelting and Yunnan Tin's breakthroughs in ITO targets solidify supply leadership. Japan's DOWA and Mitsui Kinzoku focus on high-purity and recycled streams, which shield them from zinc-price volatility.

North America is shifting from a pure importer to a partial producer. Korea Zinc's Clarksville complex, operational from 2029, and Lumentum's InP laser fab will together anchor a secure regional supply chain. Section 301 duties on Chinese indium compounds, effective net rates near 54%, further encourage domestic sourcing.

Europe's Critical Raw Materials Act compels 10% extraction and 40% processing within the bloc, leading Italy to budget EUR 450 million (USD 508.7 million) for a 200-ton national reserve. Imec's NanoIC pilot line, opened in February 2026, adds downstream pull for 7N indium compounds. South America and the Middle East-Africa together remain below 10% of volume, but idle zinc assets in Brazil and South Africa represent a callable swing capacity should prices stay above USD 500 kg.

- DOWA HOLDINGS CO., LTD.

- 5N Plus

- AIM Solder

- Belmont Metals

- Changsha Santech Materials Co., Ltd.

- Guangxi Debang Technology Co. Ltd.

- Indium Corporation

- Indium Corporation (Suzhou) Co., LTD

- KOREAZINC

- Nyrstar

- PPM Pure Metals GmbH

- Teck Resources Limited

- Umicore

- Vital Materials

- Young Poong Co. Ltd.

- Yunnan Tin Industry Co. Ltd.

- Zhuzhou Keneng New Material

- Zhuzhou Smelting Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing usage of ITO in next-gen flexible and foldable displays

- 4.2.2 Expansion of low-temperature indium alloys in advanced packaging and heterogeneous integration

- 4.2.3 Critical-raw-material resilience policies boosting European strategic stockpiles

- 4.2.4 Increasing production of high-efficiency solar panels globally

- 4.2.5 Demand surge for InGaN micro-LEDs in AR/VR headsets

- 4.3 Market Restraints

- 4.3.1 Availability of alternative transparent conductors (graphene, Ag-NW, CNT, and IGZO)

- 4.3.2 Chronic occupational-health concerns driving stricter exposure limits

- 4.3.3 ESG-driven decarbonisation pressure on indium recovery smelters

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Source

- 5.1.1 Primary (Refined from zinc residues)

- 5.1.2 Secondary/Recycled

- 5.2 By Form

- 5.2.1 Indium Ingot and Stick

- 5.2.2 Indium Alloy (In-Sn, In-Ag, In-Ga)

- 5.2.3 Indium Oxide/ITO Sputtering Target

- 5.2.4 High-purity Indium Compounds (InP, InSb, and InAs)

- 5.3 By Application

- 5.3.1 Flat-Panel and Flexible Displays

- 5.3.2 Photovoltaics (CIGS and Perovskite)

- 5.3.3 Semiconductor and Optoelectronic Devices

- 5.3.4 Solders and Thermal Interface Materials

- 5.3.5 Others (Nanotechnology, Research)

- 5.4 By End-user Industry

- 5.4.1 Electronics and Semiconductors

- 5.4.2 Energy

- 5.4.3 Automotive and Transportation

- 5.4.4 Aerospace and Defence

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 Asia Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 South Korea

- 5.5.1.4 India

- 5.5.1.5 Rest of Asia Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 DOWA HOLDINGS CO., LTD.

- 6.4.2 5N Plus

- 6.4.3 AIM Solder

- 6.4.4 Belmont Metals

- 6.4.5 Changsha Santech Materials Co., Ltd.

- 6.4.6 Guangxi Debang Technology Co. Ltd.

- 6.4.7 Indium Corporation

- 6.4.8 Indium Corporation (Suzhou) Co., LTD

- 6.4.9 KOREAZINC

- 6.4.10 Nyrstar

- 6.4.11 PPM Pure Metals GmbH

- 6.4.12 Teck Resources Limited

- 6.4.13 Umicore

- 6.4.14 Vital Materials

- 6.4.15 Young Poong Co. Ltd.

- 6.4.16 Yunnan Tin Industry Co. Ltd.

- 6.4.17 Zhuzhou Keneng New Material

- 6.4.18 Zhuzhou Smelting Group Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment