|

시장보고서

상품코드

2062134

BLDC 팬 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)BLDC Fan - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

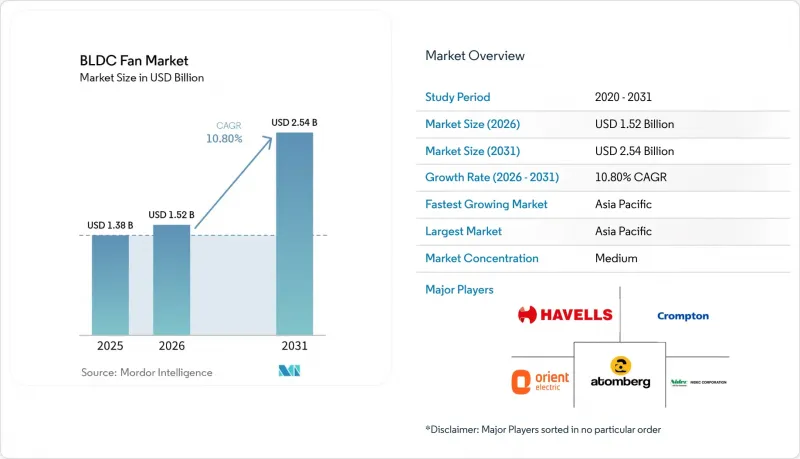

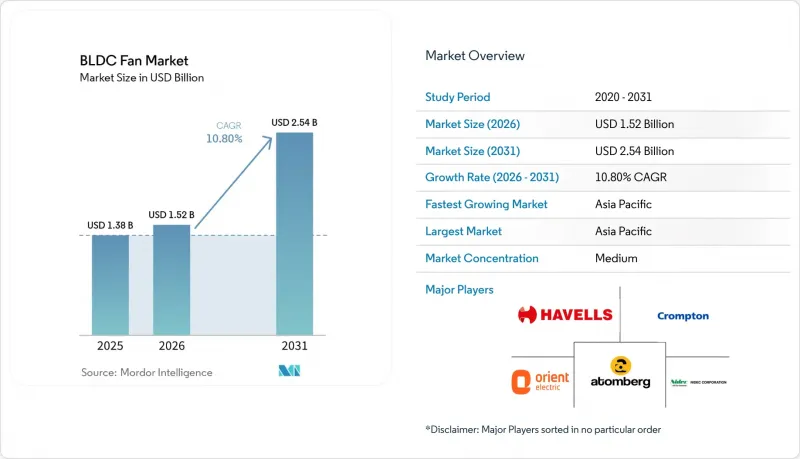

Mordor Intelligence에 의하면, BLDC 팬 시장 규모는 2025년 13억 8,000만 달러로 평가되었고, 2026년 15억 2,000만 달러로 추정되고, 2031년까지 25억 4,000만 달러로 확대될 전망이며, 2026-2031년 연평균 복합 성장률(CAGR)은 10.80%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형별(천장 팬, 스탠드형 팬 등), 모터 구조별(내부 로터 BLDC, 외부 로터 BLDC), 정격 출력별(30W 미만, 30-60W, 기타), 용도별(주택, 상업용 건물, 기타), 판매 채널별(오프라인 매장, 온라인, 기타), 지역별(북미, 남미, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 BLDC 팬 시장 동향 및 분석

소비자를 위한 더욱 엄격한 에너지 효율 기준 및 스타 라벨

미국, 유럽연합(EU) 및 인도의 규제 조화를 통해 시스템 손실을 명확히 보여주는 종합적인 ‘와이어-투-에어’ 지표 및 표시 제도가 도입됨에 따라, 팬의 성능 기준이 재정의되었습니다. 이로 인해 쾌적한 환기 및 공정 환기 모두에서 전자 정류식 모터의 가치가 높아지고 있습니다. 캘리포니아주 타이틀 20에서는 다양한 상업용 및 산업용 팬 유형에 대해 FEI(팬 효율 지수)가 1.00 이상이어야 한다고 규정하고 있으며, 이 기준은 AMCA의 시험 절차 및 인증 과정을 통해 입증되었습니다. MAEDbS에는 이미 다수의 적합 모델이 등록되어 있습니다. 유럽연합 집행위원회의 125W-500kW 팬에 대한 2024년 에코디자인 규정은 2030년까지 연간 31TWh의 전력 절감 효과를 기대하고 있으며, 2026년 6월부터 적용이 시작됩니다. 이에 따라 제조업체들은 고효율 플랫폼을 중심으로 제품 라인업을 간소화하고, 설계자들에게 보다 상세한 성능 데이터를 제공해야 하는 압박을 받고 있습니다. 2025년 환기 팬용 ENERGY STAR Most Efficient 기준에서는 커패시터 시동 유도 시스템 대신 EC 모터와 견고한 제어 시스템을 사용하여 달성해야 할 실용적인 효율 기준치가 상향 조정되었습니다. 캘리포니아주 타이틀 24와 같은 건축 기준에서는 FEI가 필수 요건으로 포함되어 있어, 에너지 성능이 단순한 마케팅상의 선택 사항이 아닌 사양상의 필수 조건이 되었으며, BLDC 팬은 해당 기준을 충족하는 프로젝트에서 기본 선택지로 자리매김하고 있습니다.

투자 회수를 중시한 주거용 AC 유도 팬을 BLDC 천장 팬으로 교체

인도 및 아시아태평양 일부에서는 전기 요금과 하루 평균 긴 가동 시간 덕분에, 일반적인 가격 프리미엄을 고려하더라도 BLDC 천장 팬의 투자 회수 기간이 2년 미만으로 단축됩니다. 이를 통해 보조금 없이도 전환이 매력적으로 느껴져 재구매 의향이 높아집니다. 제조업체의 자료에 따르면, 사용 빈도가 높은 가정의 경우 기존 75W 유도식 천장 팬의 연간 전기 요금이 2,400루피를 초과할 수 있지만, 일반적인 사용 패턴과 요금 체계에서는 28-35W의 BLDC 모델이 해당 비용을 절반 이하로 절감할 수 있으므로, 가계 경제성이라는 관점만 놓고 보더라도, 업그레이드의 타당성이 입증됩니다. 인도에서 천장 팬의 에너지 효율 등급 표시 의무화는 서비스 가치 공개를 의무화함으로써 이러한 전환을 더욱 가속화하고 있습니다. 이를 통해 소비자는 구매 시 와트당 풍량을 비교할 수 있게 되었으며, 제조업체들은 보다 효율적인 BLDC 플랫폼을 중심으로 제품 라인업을 재검토하도록 장려받고 있습니다. 중국의 제품 전략은 에너지 절약보다 커넥티비티 및 스마트 생태계와의 통합에 중점을 두고 있으며, BLDC 모터는 보다 광범위한 홈 오토메이션 및 실내 공기질(IAQ) 솔루션의 일환으로, 조용하고 정밀한 속도 제어를 지원하고 있습니다. 또한, 전력망이 불안정한 신흥 시장에서는 넓은 전압 범위를 지원하는 설계와 컨트롤러의 내구성이 매우 중요하며, 이러한 요소들이 BLDC 팬 시장에서 플랫폼 선택 및 가치 공학의 지침이 되고 있습니다.

희토류 자석과 컨트롤러로 인해 초기 비용이 다소 비싸게 느껴집니다.

가격에 민감한 시장에서는 자본 비용이 여전히 장벽으로 작용하고 있습니다. 특히, 팬이 더 저렴한 구매 가격으로 최소 풍량 요건을 충족하는 기본적인 유도 전동기 제품과 경쟁하는 경우입니다. 조달 전략과 부품 명세서(BOM)의 선택은 고효율 모터, 첨단 컨트롤러, 그리고 현지 관세 수준에서 수용 가능한 투자 회수 기간 사이의 지속적인 균형을 반영합니다. 희토류 가공 및 영구자석 제조 분야공급 집중은 BLDC 모터 부품 구성에 따른 투입 리스크를 높이고 있으며, 이로 인해 장기적으로 높은 비용이 유지되어 대중 시장 부문의 가격 전략을 복잡하게 만들고 있습니다. 이에 대해 제조업체는 플랫폼의 표준화와 제품 라인 전반에 걸친 컨트롤러의 재사용을 통해 규모의 경제를 실현하고, 인증에 드는 비용을 절감하고 있습니다. 예측 기간 동안 대기업들은 투입 비용의 변동을 흡수하는 데 있어 더 유리한 입장에 있으며, 이는 BLDC 팬 시장에서 통합형 공급업체의 상대적 강점을 뒷받침하고 있습니다.

부문별 분석

2025년에는 천장 팬이 52.21%의 점유율을 차지했으며, 판매량 및 매출액 측면에서 가장 큰 제품 카테고리가 되었습니다. 한편, 산업용 HVLS 및 상업용 환기 팬은 2031년까지 연평균 성장률(CAGR) 11.95%로 가장 빠른 성장세를 보이고 있습니다. 이 구성 비율은 BLDC 팬 시장에서 가정용 제품의 교체 주기와 물류, 데이터센터, 산업 시설에서의 신규 수요 증가를 반영한 것입니다. 천장 팬의 설치 대수와 높은 인지도가 그 우위를 유지하고 있으며, 인도 등 일부 국가에서 표시 의무화가 시행되면서 투명성이 높아짐에 따라, 높은 서비스 가치와 저소음 성능을 갖춘 BLDC 모델이 유리한 입지를 점하고 있습니다. 주택 부문의 제품 혁신 사이클에서는 현재 연결성, 디자인, 저소음이 중시되고 있는 반면, 상업용 및 산업용 제품의 경우 제어 기능 통합, 예측 유지보수, HVAC 설계 기준을 준수하는 높은 정압 성능이 중시되고 있습니다. 또한, 유럽 및 북미의 각 벤더들은 네이티브 디지털 프로토콜과 AI 기반 최적화 기능을 갖춘 대구경 EC 축류 팬 및 원심 팬을 시장에 출시하고 있으며, 이를 통해 유도식 솔루션 대비 전체 수명 주기 전반에 걸쳐 성능 면에서 우위를 점하고 있습니다. 이러한 제품 구성으로 인해 천장 팬의 핵심 시장은 견조한 성장세를 유지하는 한편, BLDC 팬 시장 내의 한계 성장분은 HVLS 및 특수 환기 용도로 이동하고 있습니다.

전체 제품 라인에 걸쳐 휴대용 팬, 벽걸이형 팬, 배기 팬은 법규에 따른 환기 및 국소 냉방 분야에서 확고한 역할을 유지하고 있지만, HVLS나 첨단 산업용 시스템에 비하면 그 혁신성은 점진적인 수준에 그치고 있습니다. 데스크형, 타워형, 블레이드리스형 프리미엄 소비자용 제품은 디자인과 저소음 성능으로 경쟁하고 있으며, 앱을 통한 통합 제어 기능과 실내 상황에 맞추어 풍량을 조절하는 센서 피드백 기능을 갖추고 있습니다. 산업용 HVLS 솔루션은 대규모 시설에서 층류 해소 효과와 연중 쾌적성을 중시하며, 가변속 EC 드라이브를 통해 저회전 수에서의 부드러운 제어, 에너지 소비 절감 및 뛰어난 저소음 성능을 실현하고 있습니다. 창고 및 물류 시설에서는 BLDC 팬이 수요 기반 제어와 결합되어 피크 시간대의 실내 공기질(IAQ)과 쾌적성이라는 두 가지 목표를 모두 달성하고 있으며, 제조업체들은 현재 예측 유지보수를 위한 진동 감지 기능이나 BMS(빌딩 관리 시스템)와의 통합 등의 기능을 탑재하고 있습니다. BLDC 팬 시장에서는 양산형 천장 설치 용도와 HVLS 및 첨단 상업용 환기 시스템 분야의 프리미엄화 및 사양 주도형 성장 기회 간의 균형이 계속해서 유지되고 있습니다.

2025년에는 내부 로터 설계가 68.87%의 점유율을 차지했으며, 많은 천장형, 받침대형, 소형 팬에서 여전히 주류 구조로 자리 잡고 있습니다. 한편, HVAC 시스템이 BLDC 팬 시장에서 저속 및 고토크 구성을 선호하는 경향이 있어, 아웃터 로터 EC 설계는 2031년까지 연평균 성장률(CAGR) 9.99%로 가장 빠르게 성장하고 있습니다. 이너 로터 모터는 콤팩트한 설치 면적에서 높은 토크 밀도를 실현하여, 주택이나 소규모 상업시설에서 급격한 속도 변화와 저소음 작동이 중요한 가역식, 회전식 및 스마트 천장 팬에 최적입니다. 이러한 제약은 고연속 전력 작동 시의 열 관리에 있으며, 이로 인해 비용과 무게를 증가시키는 추가적인 열전도 경로나 방열판 없이는 대형 HVAC 팬으로의 확장성이 제한됩니다. 아우터 로터 EC 설계는 저회전 수에서 높은 토크를 구현하기 위해 질량을 외곽부에 분산시켜, 저소음과 베어링 수명 연장을 동시에 달성하면서 더 큰 직경과 높은 풍량에 적합합니다. 공기 처리 용도에서 이 팬들은 넓은 터다운 범위 전반에 걸쳐 효율을 유지할 수 있으며, 이는 상업용 건물의 변동하는 이용자 수에 맞추어 환기 기준을 충족하는 데 있어 매우 중요합니다.

신제품 출시로 인해 이러한 테마가 더욱 강화되었으며, 대구경 EC 플랫폼과 저소음 및 고효율로 축류 팬을 대체할 수 있는 소형 대각선 모듈이 등장하고 있습니다. 유럽 공급업체들은 모듈형 프레임, 넓은 전압 허용 범위, 그리고 디지털 통신 프로토콜을 중시하고 있으며, 이를 통해 시운전을 신속하게 진행하고 시스템 수준의 최적화를 도모함으로써 장기적으로 제공되는 성능이 향상됩니다. 주택용 공급업체들은 연결 기능의 고도화, 앱 제어, 그리고 저속 주행 시의 정숙성에 주력하고 있습니다. 경쟁이 치열한 소매 분야에서 사용자 경험이 차별화의 핵심이 되기 때문입니다. 예측 기간 동안, 출하 대수 기준으로는 내부 로터 방식이 압도적인 점유율을 유지할 것으로 보이지만, 외부 로터 EC 구성은 정압 및 저소음이라는 장점을 바탕으로 HVAC, 클린룸 및 공정 환기 분야에서 점유율을 확대할 것으로 전망됩니다. 이러한 아키텍처의 조합을 통해 BLDC 팬 시장은 소비자의 선호도와 상업적 성능 목표 모두를 지속적으로 충족시킬 수 있게 될 것입니다.

지역별 분석

아시아태평양은 2025년에 45.75%의 점유율을 차지했으며, 2031년까지 연평균 성장률(CAGR) 12.68%로 지역 성장을 주도할 것입니다. 인도에서는 사용 빈도가 높은 가정과 표시 의무화가 BLDC로의 업그레이드를 촉진하고 있으며, 중국에서는 BLDC 팬 시장의 광범위한 전기화 및 실내 공기질(IAQ) 목표에 부합하는 상업 및 산업용도입이 진행되고 있습니다. 인도에서는 와트 수나 송풍량과 관련된 가치 제안이 소비자가 프리미엄 가격과 총 소유 비용을 비교 검토하는 데 도움이 되고 있으며, 한편으로는 커넥티드 기능과 다양한 색상 옵션이 도시 지역에서 시장 점유율 확대에 기여하고 있습니다. 동남아시아에서는 선진적인 그린빌딩 규제의 영향을 받은 싱가포르의 상업 프로젝트에서 BLDC의 높은 보급률부터, 가격에 민감한 대규모 시장의 초기 전환 단계에 이르기까지 도입 현황은 다양합니다. 일본과 호주에서는 가정 및 소규모 상업시설에서 저소음, 청결성, 그리고 커넥티드 기능을 갖춘 환기 시스템에 대한 수요가 높으며, 이것이 프리미엄 EC 제품 라인의 기반이 되고 있습니다. 아시아태평양 전체에서 규격, 표시, 전력 안정성은 BLDC 팬 시장의 플랫폼 설계 및 마케팅 전략 수립에 영향을 미치고 있습니다.

북미에서는 성숙한 교체 수요와 통합 제어, 신뢰성, 그리고 FEI 규격 준수를 요구하는 고부가가치 상업시설 및 데이터센터로의 도입이 균형을 이루고 있습니다. 2025년에 연방 정부가 제안했던 팬 효율 규정을 철회함에 따라, 규제 주도권은 주 및 지방 정부에 남아 있으며, 캘리포니아주의 가전 및 건축 기준이 전국의 에너지 효율 기준을 이끌어가는 기본 성능 기준을 확립하고 있습니다. 에너지 스타(ENERGY STAR) 기준은 여전히 환기 팬의 성능 목표를 규정하고 있으며, 인증을 받은 건물에서 BMS(빌딩 관리 시스템)를 통한 최적화가 에너지 효율(EC) 도입을 촉진하고 있습니다. 데이터센터 생태계에서는 첨단 열 관리 솔루션과 48V 지원 부품이 중요시되고 있으며, 원격 측정 기능과 모듈성을 갖춘 BLDC 팬이 차세대 전원 토폴로지에 최적화되어 통합되어 있습니다. 이러한 요인들로 인해 북미는 BLDC 팬 시장에서 여전히 고부가가치 제품의 주요 도입 지역으로 자리 잡고 있습니다.

유럽 시장 점유율은 아시아태평양과 비교할 때 절대적인 규모는 작지만, 친환경 설계를 뒷받침하는 강력한 정책적 지원, 급등하는 에너지 가격, 그리고 신축 및 리모델링 모두에서 친환경 솔루션을 권장하는 건축 성능 기준의 강화 등을 반영하고 있습니다. 유럽연합 집행위원회의 2024년 팬 관련 개정안(125W-500kW 대상)은 효율 기준을 직접 상향 조정하는 것으로, 2026년 6월부터 적용되며 2030년까지 전력 소비를 대폭 감축한다는 목표가 설정되어 있습니다. 이에 따라 FEI 표준을 준수하는 시스템으로의 제품 포트폴리오 전환이 가속화되고 있습니다. 독일이나 영국 등 시장에서는 상업용 환기 및 청정 환경 분야에서 도입이 활발히 진행되고 있으며, 디지털 제어 기능을 갖춘 대형 EC 원심 팬 및 축류 팬이 현재 표준으로 자리 잡고 있습니다. 영국의 사례 자료에 따르면, BMS 최적화와 고효율 팬의 결합을 통해 에너지 소비와 CO2 배출량을 현저히 줄일 수 있으며, 이러한 투자의 장기적인 경제적 성과가 입증되었습니다. 남유럽 및 동유럽에서는 기후와 비용 요인으로 인해 진전이 더딘 편이지만, 정책, 표시 제도, 인센티브 제도를 통해 그 격차는 계속해서 좁혀지고 있습니다. 예측 기간 동안 유럽의 규제 명확성이 높아지고 설계자들의 EC 플랫폼에 대한 숙련도가 향상됨에 따라, BLDC 팬 시장의 안정성이 유지될 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the bLDC fan market size is projected to expand from USD 1.38 billion in 2025 and USD 1.52 billion in 2026 to USD 2.54 billion by 2031, registering a CAGR of 10.80% between 2026 and 2031.

This report is Segmented by Product Type (Ceiling Fans, Pedestal, and More), Motor Architecture (Inner-Rotor BLDC, Outer-Rotor BLDC), Power Rating (Below30 W, 30-60 W, and More), Application (Residential, Commercial Buildings, and More), Distribution Channel (Offline Retail, Online, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global BLDC Fan Market Trends and Insights

Tighter Energy-Efficiency Standards and Star Labeling for Fans

Converging regulations in the United States, European Union, and India reset the baseline for fan performance by using holistic wire-to-air metrics and labeling schemes that expose system losses, which elevate the value of electronically commutated machines in both comfort and process ventilation. California's Title 20 requires FEI≥ 1.00 across a wide range of commercial and industrial fan types, a standard backed by AMCA test procedures and certification pipelines that already count large numbers of compliant models in MAEDbS. The European Commission's 2024 ecodesign rules for fans from 125W to 500kW project 31 TWh of annual electricity savings by 2030 and begin applying in June 2026, which pushes manufacturers to simplify portfolios around higher-efficiency platforms and provide richer performance data for designers. ENERGY STAR Most Efficient criteria for 2025 ventilating fans raise the most practical efficacy thresholds to achieve with EC motors and robust controls rather than with capacitor-start induction systems. Building codes like California Title 24 integrate FEI into mandatory requirements, which turns energy performance into a specification gate rather than a marketing option and positions BLDC fans as default selections in compliant projects.

Payback-Led Residential Replacement of AC Induction with BLDC Ceiling Fans

In India and across parts of Asia-Pacific, electricity tariffs and long daily runtimes compress payback periods for BLDC ceiling fans to below two years at typical price premiums, which makes the switch compelling even without subsidies and lifts repeat purchase intent. Manufacturer data show a conventional 75W induction ceiling fan can cost over INR 2,400 in annual electricity for high-usage homes, while a 28-35W BLDC model can cut that cost by more than half at common usage patterns and tariffs, reinforcing the upgrade case on household economics alone. India's mandatory star labeling for ceiling fans further amplifies this shift by requiring disclosure on service value, letting consumers compare air delivery per watt at the point of purchase, and pushing manufacturers to redesign portfolios around more efficient BLDC platforms. Product strategies in China center less on energy savings and more on connectivity and integration into smart ecosystems, where BLDC motors support quiet, precise speed control as part of larger home automation and IAQ solutions. Wide-voltage designs and controller robustness are also crucial in emerging markets with grid instability, which guides platform choices and value engineering in the BLDC fan market.

Upfront Cost Premium from Rare-Earth Magnets and Controllers.

Capital cost remains a barrier in price-sensitive markets, particularly where fans compete with basic induction alternatives that meet minimum airflow requirements at lower purchase prices. Procurement strategies and bill-of-material choices reflect an ongoing balance between higher-efficiency motors, controller sophistication, and acceptable payback periods at local tariffs. Supply concentration of rare-earth processing and permanent magnet manufacturing elevates input risk for BLDC bill of materials, which sustains premiums over time and complicates pricing strategies for mass-market segments. Manufacturers respond with platform standardization and controller reuse across product lines to improve scale economics and reduce certification overhead. Over the forecast, larger players are better positioned to absorb input volatility, which supports the relative strength of integrated vendors within the BLDC fan market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid EC Fan Adoption in Commercial HVAC for Variable-Speed Control and IAQ

- Data Center and Electronics Thermal Loads Favoring High-Reliability BLDC Fans

- Rare-Earth Magnet Price Volatility and Supply Concentration Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceiling fans commanded 52.21% share in 2025, making them the largest product category by volume and revenue, while industrial HVLS and commercial ventilation fans deliver the fastest expansion at 11.95% CAGR through 2031, a split that reflects replacement cycles in homes and greenfield growth in logistics, data center, and industrial settings within the BLDC fan market. The installed base and familiarity of ceiling fans sustain their lead, and mandatory labeling in countries like India increases transparency that favors BLDC models with high service value and quiet operation. Product innovation cycles in residential categories now emphasize connectivity, aesthetic options, and lower noise, while commercial and industrial products lean toward controls integration, predictive diagnostics, and high static pressure performance aligned with HVAC design standards. Vendors in Europe and North America have also brought large-diameter EC axial and centrifugal models to market with native digital protocols and AI-supported optimization that build lifetime performance advantages over induction solutions. This mix sustains a strong ceiling fan core while shifting marginal growth to HVLS and specialized ventilation use cases inside the BLDC fan market.

Across product lines, portable, wall, and exhaust fans retain solid roles in code-driven ventilation and spot cooling, but they show more incremental innovation relative to HVLS and advanced commercial systems. Premium consumer products in desk, tower, and bladeless formats compete on design and quietness, with integrated app control and sensor feedback that adapts airflow to room conditions. Industrial HVLS solutions emphasize destratification benefits and year-round comfort in large facilities, where variable-speed EC drives offer smoother control, reduced energy use, and better acoustic performance at low RPM. In warehouses and logistics, BLDC fans combine with demand-based controls to meet both IAQ and comfort targets during peak periods, and manufacturers now include features such as vibration sensing and BMS integration for predictive maintenance. The BLDC fan market continues to balance volume-driven ceiling applications with the growing premium and specification-led opportunity in HVLS and advanced commercial ventilation.

Inner-rotor designs helda 68.87% share in 2025 and remain the architecture of choice for many ceiling, pedestal, and compact fans, while outer-rotor EC designs are the fastest-growing with 9.99% CAGR through 2031 as HVAC systems favor low-speed, high-torque configurations in the BLDC fan market. Inner-rotor motors deliver high torque density in compact footprints and serve reversible, oscillating, and smart ceiling fans well, where rapid speed changes and quiet operation are emphasized in residential and light commercial settings. Their constraints lie in thermal management at higher continuous power, which curbs scalability for large HVAC fans without added conduction paths or heat sinks that raise cost and weight. Outer-rotor EC designs distribute mass around the perimeter for higher torque at low RPM, which suits larger diameters and higher airflows with lower noise and extended bearing life. In air handling applications, these fans can maintain efficiency across wide turndown ranges, which is central to meeting ventilation standards at variable occupancy levels in commercial buildings.

Product launches reinforce these themes with larger-diameter EC platforms and compact diagonal modules that substitute for axial units at lower noise and higher efficiency. European suppliers emphasize modular frames, wide voltage tolerances, and digital communication protocols for faster commissioning and system-level optimization, which improves delivered performance over time. Residential suppliers focus on refinement of connectivity, app control, and silent profiles at low speeds, where user experience drives differentiation in crowded retail categories. Over the forecast period, inner-rotor platforms should retain dominant share by unit volumes, while outer-rotor EC configurations expand share in HVAC, clean room, and process ventilation due to static pressure and low-noise advantages. This architecture mix keeps the BLDC fan market responsive to both consumer preferences and commercial performance targets.

Geography Analysis

Asia-Pacific held 45.75% share in 2025 and leads regional growth at 12.68% CAGR through 2031, with India's high-usage households and mandatory labeling catalyzing BLDC upgrades and China's commercial and industrial deployments aligning with broader electrification and IAQ goals in the BLDC fan market. In India, value communication around wattage and air delivery helps consumers weigh total ownership cost against premiums, while connected features and color choices win share in urban tiers. Southeast Asia presents varied adoption, from high BLDC penetration in Singapore's commercial projects influenced by advanced green building rules to early-stage transitions in large, price-sensitive markets. Japan and Australia show a strong preference for quiet, clean, and connected ventilation in homes and small commercial sites, which underpins premium EC product lines. Across the Asia-Pacific region, standards, labeling, and power stability shape platform designs and marketing narratives in the BLDC fan market.

North America balances mature replacement volumes with high-value commercial and data center deployments that demand integrated controls, reliability, and FEI-aligned specifications. The federal withdrawal of a proposed fan efficiency rule in 2025 kept the regulatory vector at the state and local levels, with California's appliance and building codes establishing baseline performance that guides national portfolios. ENERGY STAR criteria continue to shape ventilating fan performance goals, and BMS-led optimization in certified buildings lifts EC adoption. Data center ecosystems emphasize advanced thermal solutions and 48V-ready components, where BLDC fans with telemetry and modularity integrate best into next-generation power topologies. These factors keep North America a high-value deployment region within the BLDC fan market.

Europe's share reflects smaller absolute volumes compared with Asia-Pacific but strong policy pull from ecodesign, high energy prices, and tightening building performance standards that favor EC solutions in both new builds and retrofits. The European Commission's 2024 update on fans from 125W to 500kW directly raises the efficiency bar, with application in June 2026 and a significant electricity reduction target by 2030, which accelerates portfolio shifts to FEI-aligned systems. Markets like Germany and the UK have seen pronounced adoption in commercial ventilation and clean environments, where large EC centrifugal and axial fans with digital control are now the norm. UK case material demonstrates that BMS optimization combined with efficient fans can drive measurable energy and CO2 reductions, validating longer-run economic outcomes for these investments. Southern and Eastern Europe advance more gradually due to climate and cost factors, but policy, labeling, and incentive structures continue to close gaps. Over the forecast period, Europe's regulatory clarity and designers' familiarity with EC platforms support consistency in the BLDC fan market.

- Atomberg Technologies

- Crompton Greaves Consumer

- Havells India

- Orient Electric

- Usha International

- Polycab India

- Panasonic Life Solutions

- Nidec Corporation

- Delta Electronics

- ebm-papst Group

- Johnson Electric

- Regal Rexnord (Marathon)

- ZIEHL-ABEGG

- Mitsubishi Electric

- Big Ass Fans

- Dyson

- Hunter Fan Company

- Lasko Products

- Haier Smart Home

- Midea Group

- Gree Electric

- MinebeaMitsumi Inc.

- Sanyo Denki

- Allied Motion Technologies

- Jupiter Fan

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tighter energy-efficiency standards and star labeling for fans

- 4.2.2 Payback-led residential replacement of AC induction with BLDC ceiling fans

- 4.2.3 Rapid EC fan adoption in commercial HVAC for variable-speed control and IAQ

- 4.2.4 Data center and electronics thermal loads favoring high-reliability BLDC fans

- 4.2.5 48V DC distribution in racks/buildings enabling direct BLDC fan deployments

- 4.2.6 Utility and green-building incentives bundling smart BLDC fans with BMS/EMS

- 4.3 Market Restraints

- 4.3.1 Upfront cost premium from rare-earth magnets and controllers

- 4.3.2 Rare-earth magnet price volatility and supply concentration risks

- 4.3.3 After-sales electronics service gaps and reliability concerns in harsh environments

- 4.3.4 EMI/acoustic compliance constraints slowing global SKU rollouts

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Ceiling Fans

- 5.1.2 Pedestal & Table Fans

- 5.1.3 Wall & Exhaust Fans

- 5.1.4 Industrial HVLS / Commercial Ventilation Fans

- 5.2 By Motor Architecture

- 5.2.1 Inner-Rotor BLDC

- 5.2.2 Outer-Rotor BLDC (EC)

- 5.3 By Power Rating

- 5.3.1 <30 W

- 5.3.2 30 - 60 W

- 5.3.3 60 - 120 W

- 5.3.4 >120 W

- 5.4 By Application

- 5.4.1 Residential

- 5.4.2 Commercial Buildings

- 5.4.3 Industrial / Warehouse

- 5.4.4 Data-Centre & Electronics Cooling

- 5.4.5 Automotive Cabin & Battery-Thermal

- 5.5 By Distribution Channel

- 5.5.1 Offline Retail (Dealer / MBO)

- 5.5.2 Direct Institutional & OEM

- 5.5.3 Online (E-commerce & D2C)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 Canada

- 5.6.1.2 United States

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Peru

- 5.6.2.3 Chile

- 5.6.2.4 Argentina

- 5.6.2.5 Rest of South America

- 5.6.3 Asia-Pacific

- 5.6.3.1 India

- 5.6.3.2 China

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 South East Asia (SG, MY, TH, ID, VN, PH)

- 5.6.3.7 Rest of Asia-Pacific

- 5.6.4 Europe

- 5.6.4.1 United Kingdom

- 5.6.4.2 Germany

- 5.6.4.3 France

- 5.6.4.4 Spain

- 5.6.4.5 Italy

- 5.6.4.6 BENELUX

- 5.6.4.7 NORDICS

- 5.6.4.8 Rest of Europe

- 5.6.5 Middle East And Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.5.5 Rest of Middle East And Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Atomberg Technologies

- 6.4.2 Crompton Greaves Consumer

- 6.4.3 Havells India

- 6.4.4 Orient Electric

- 6.4.5 Usha International

- 6.4.6 Polycab India

- 6.4.7 Panasonic Life Solutions

- 6.4.8 Nidec Corporation

- 6.4.9 Delta Electronics

- 6.4.10 ebm-papst Group

- 6.4.11 Johnson Electric

- 6.4.12 Regal Rexnord (Marathon)

- 6.4.13 ZIEHL-ABEGG

- 6.4.14 Mitsubishi Electric

- 6.4.15 Big Ass Fans

- 6.4.16 Dyson

- 6.4.17 Hunter Fan Company

- 6.4.18 Lasko Products

- 6.4.19 Haier Smart Home

- 6.4.20 Midea Group

- 6.4.21 Gree Electric

- 6.4.22 MinebeaMitsumi Inc.

- 6.4.23 Sanyo Denki

- 6.4.24 Allied Motion Technologies

- 6.4.25 Jupiter Fan

7 Market Opportunities & Future Outlook

- 7.1 Rapid-cook combi ovens integrating microwave & impingement for QSRs

- 7.2 AI-driven autonomous cooking algorithms for consistency & labour savings