|

시장보고서

상품코드

2062146

복합 창호 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Composite Doors And Windows - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

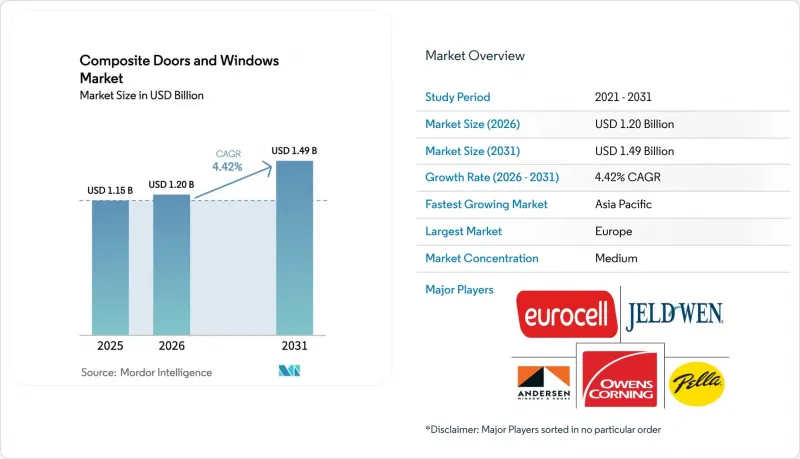

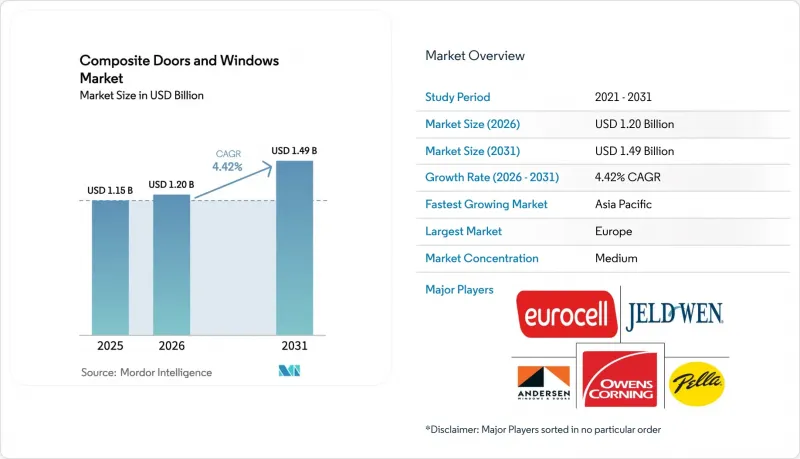

Mordor Intelligence에 의하면, 복합 창호 시장 규모는 2025년 11억 5,000만 달러로 평가되었습니다. 2026년 12억 달러로 확대되어 2026-2031년에 걸쳐 CAGR은 4.42%를 나타내, 2031년에는 14억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 유형(복합 도어 및 복합 창문), 소재 유형(유리섬유 강화 플라스틱, 목질 플라스틱 복합재, 섬유 강화 폴리머, 기타), 용도(주택, 산업·공공시설, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 복합 창호 시장 동향 및 분석

에너지 절약형 건축 외피에 대한 수요 증가

주요 경제권에서 건축 기준이 강화됨에 따라 U값과 일사열 획득률을 낮추는 것이 의무화되어, 복합재 프레임이 선호되는 선택지가 되고 있습니다. 예를 들어, 중국에서는 창문과 벽의 비율을 20-35%로 제한하고, U값의 상한을 1.5-2.0 W/m²·K로 설정하고 있습니다. 호주의 NCC 2022에서는 유리 부분의 U값을 3.8 W/m²·K 이하로 유지해야 하며, 이와 함께 ‘창호 에너지 평가 제도(WERS)’에 따른 표시가 의무화되어 있습니다. EU의 개정된 ‘건축물 에너지 성능 지침’에서는 2030년까지 공공 및 주거용 건축물에 대해 EPC C등급을 의무화하고 있으며, 대규모 개보수 공사를 촉진하고 있습니다. 에어로겔과 진공 단열 패널을 결합한 복합 프로파일은 열전도율이 0.020 W/m·K 이하이며, 상변화에 의한 완충 효과로 HVAC 부하를 저감하여 패시브 하우스의 U값 목표인 0.8 W/m²·K를 충족합니다. 플로리다주의 건축 기준법에 따르면 U값이 0.32 이하이어야 하며, 개발업자에게는 ASHRAE 90.1-2022 및 IECC 기준을 준수하는 GRP 및 FRP 프레임의 채택이 권장되고 있습니다.

복합재의 낮은 유지보수 비용과 뛰어난 내구성

GRP 및 목질 플라스틱 복합재(WPC) 프레임은 부패, 부식, 자외선으로 인한 열화에 강하며, 목재에서 흔히 발생하는 재도장 필요성을 없애고, 알루미늄에서 나타나는 산화를 방지합니다. 재활용 목재 섬유와 비닐 폴리머를 결합한 앤더슨사의 ‘파이버렉스’는 판매량이 1,000만 개를 돌파했으며, 로봇 기술의 업그레이드를 통해 압출 성형 수율을 8% 향상시켰습니다. Rehau는 최대 86%의 재활용 소재를 사용하고 있으며, 이를 통해 연간 7만 톤의 폐기물을 줄이고 10만 톤의 CO2 배출을 억제하고 있습니다. 데쿠닝크(Deceuninck)의 ‘선쉴드(SunShield)’ 안료 기술은 강한 자외선에 노출되는 짙은 색상의 프레임의 색 바램을 최소화합니다. 아마 섬유와 탄소섬유를 결합한 바이오 하이브리드 적층재를 사용한 학술 실험 결과, 순수한 탄소섬유 부품에 비해 24% 더 높은 강성이 확인되어 건축 분야로의 응용 가능성이 시사되고 있습니다.

개발도상 지역에서의 시공업체 인지도 부족

복합재 프레임에는 특수한 고정, 플래싱, 실링 기술이 필요하지만, 북미와 유럽 이외의 지역에서는 인증 교육 기회가 제한적입니다. FGIA의 InstallationMasters 프로그램은 영어와 스페인어로만 제공되며, 사전 현장 경험이 요구되기 때문에 인도, 인도네시아, 사하라 이남 아프리카 등의 지역에서는 보급이 제한되고 있습니다. 적절한 시공 기술이 준수되지 않는 지역에서는 보증 청구 건수가 30-50% 증가하고 있으며, 이는 제조업체의 이익률과 소비자의 신뢰에 영향을 미치고 있습니다. Modulex나 Interarch와 같은 기업들은 자사 공장 내에 시공 팀을 배치하고 있지만, 이러한 접근 방식은 소규모 도급업체들이 분산되어 있는 환경에서는 확장성이 없습니다. 증강현실(AR) 도구는 이해도를 높여주고 있으며, Andersen은 리드 전환율이 25% 증가했다고 보고하고 있지만, 언어 장벽과 스마트폰 접근 환경의 불균형으로 인해 지방 시장에서 그 효과가 제한되고 있습니다.

부문별 분석

2025년 매출에서 복합 도어가 차지하는 비중은 54.11%였으나, 복합 창문 시장 규모는 2031년까지 연평균 성장률(CAGR) 4.81%로 확대되어 도어의 성장률을 상회할 것으로 전망됩니다. 북미에서는 주택 소유자들이 문을 25-30년마다 교체하는 반면, 창문은 15-20년마다 교체하고 있습니다. 또한 독일과 프랑스에서는 주택 1채당 최대 6만 유로, 창문 1개당 100유로의 보조금 제도가 도입되어 있어, 이를 통해 투자 회수 기간이 단축되고 있습니다. U값이 0.22 이하인 ‘ENERGY STAR Most Efficient’ 기준은 여전히 프리미엄 포지셔닝을 뒷받침하고 있습니다.

Rehau의 32mm 창호를 채택한 슬라이드 시스템 ‘SLINOVA X’는 유럽의 발코니 도어용으로 설계되었습니다. 한편, 앤더슨(Andersen)의 확장된 100 시리즈는 판매 대수 1,000만 대를 돌파하며 규모의 경제성을 뚜렷이 보여주고 있습니다. 데쿠닝크(Deceuninck)와 알펜(Alpen)은 U값 0.09라는 낮은 수치를 실현한 삼중 유리 창호 ‘엘레강트(Elegant)’를 출시하여, 일렉트로크로믹(전착 변색) 기술을 활용한 리모델링 수요에 대응하고 있습니다. 보안 및 대피용 용도에서는 여전히 도어가 주류를 이루고 있으며, BS 6853 및 EN 45545의 화재 안전 기준을 충족하는 GRP 재질의 옵션이 제공되고 있습니다.

지역별 분석

유럽은 2025년 매출의 43.24%를 차지했으며, 독일의 BEG EM 보조금(최대 6만 유로)이나 창문 개보수에 대한 20%의 보조금 등, 알찬 개보수 지원 프로그램의 뒷받침을 받고 있습니다. 프랑스의 ‘MaPrimeRenov’는 창문 1개당 40-100유로를 지원하며, 영국의 ‘ECO4’ 제도는 가구 소득에 따라 5,000-1만 5,000파운드를 지급합니다. 이탈리아의 ‘슈퍼 보너스’는 2024년에 70%로 인하된 뒤 단계적으로 폐지될 예정이지만, 누적된 신청 건수가 수요를 지탱하고 있습니다. 앞으로 도입될 ‘디지털 제품 여권’은 재료 데이터의 투명성을 높이고, 내재된 탄소량이 적은 FRP 시스템을 촉진할 가능성이 있습니다. 리모델링 수요의 급증에 따라 공급 체제를 확대하기 위해, 유로셀이 2025년에 알넷 그룹을 인수한 사례에서도 알 수 있듯이, 산업 재편이 가속화되고 있습니다.

북미 시장은 허리케인 위험 완화 대책과 연방 정부의 세제 혜택에 힘입어 성장하고 있습니다. 플로리다주에서는 폭풍 보험료가 10-45% 할인됨에 따라 GRP 창문의 투자 회수 기간이 3년 이하로 단축되었습니다. 또한, ‘에너지 효율이 높은 주택 개보수 세액 공제(Energy Efficient Home Improvement Credit)’를 통해 개구부 1개당 최대 600달러의 환급을 받을 수 있습니다. 앤더슨사가 애리조나주 굿이어에서 진행한 4억 2,000만 달러 규모의 확장 사업으로 인해, Fibrex의 생산 능력은 두 배로 늘어났고, 운송 비용은 15% 절감되었으며, 서부 지역에서의 서비스가 개선되었습니다. 캐나다의 ‘Greener Homes Grant’에서는 개구부 1개당 125-250 캐나다 달러가 지급되며, 멕시코 바히오 회랑 지역의 주택 시장 회복이 복합재 채택을 뒷받침하고 있습니다.

아시아태평양은 오프사이트 제조의 호조에 힘입어 2031년까지 연평균 성장률(CAGR)이 5.21%로 가장 높은 성장세를 보이고 있습니다. 뭄바이 근교에 위치한 Modulex Global의 메가팩토리에서는 연간 최대 30만 제곱미터의 모듈식 파사드를 생산하고 있습니다. 중국의 건축 기준에서는 U값을 1.5-2.0 W/m²·K로 제한하고 있으며, 제14차 5개년 계획에서는 3억 5,000만 m²의 개보수를 목표로 하고 있어, 고성능 프레임에 대한 수요를 견인하고 있습니다. 호주의 NCC 2022 및 향후 예정된 2025년 개정안에서는 단열 기준이 강화되는 반면, 일본의 내진 보강 사업은 1981년 이전에 지어진 건물을 대상으로 하고 있습니다. 주택 시장 회복세가 지속되고 있는 브라질, NEOM과 같은 거대 프로젝트에서 저탄소 복합 커튼월이 지정된 사우디아라비아에서는 아직 초기 단계이긴 하지만, 뚜렷한 진전이 나타나고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the composite doors and windows market size is expected to grow from USD 1.15 billion in 2025 to USD 1.20 billion in 2026 and is forecast to reach USD 1.49 billion by 2031 at 4.42% CAGR over 2026-2031.

This report is Segmented by Product Type (Composite Doors and Composite Windows), Material Type (Glass Reinforced Plastic, Wood-Plastic Composite, Fibre-Reinforced Polymer, and More), Application (Residential, Industrial/Institutional, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Composite Doors And Windows Market Trends and Insights

Growing Demand for Energy-Efficient Building Envelopes

Stricter building codes in major economies are mandating lower U-values and solar heat gain coefficients, making composite frames a preferred choice. For example, China limits window-to-wall ratios to 20-35% and caps U-values at 1.5-2.0 W/m2*K, as per. Australia's NCC 2022 requires glazing U-values as low as 3.8 W/m2*K, along with mandatory Window Energy Rating Scheme labeling. The EU's recast Energy Performance of Buildings Directive mandates EPC C ratings for public and non-residential buildings by 2030, driving deep-retrofit activities. Composite profiles incorporating aerogels and vacuum insulation panels, with thermal conductivities below 0.020 W/m*K, provide phase-change buffering that reduces HVAC loads and meets Passive House U-value targets of 0.8 W/m2*K. In Florida, the Building Code enforces U-factors no greater than 0.32, encouraging developers to adopt GRP and FRP frames that comply with ASHRAE 90.1-2022 and IECC standards.

Low Maintenance and Superior Durability of Composites

GRP and wood-plastic composite (WPC) frames resist rot, corrosion, and ultraviolet degradation, eliminating the need for repainting common with wood and preventing oxidation seen in aluminum. Andersen's Fibrex, which combines reclaimed wood fiber with vinyl polymer, has surpassed 10 million units sold and achieved an 8% extrusion yield improvement through robotics upgrades. Rehau incorporates up to 86% recycled content, diverting 70,000 tons of material annually and saving 100,000 tons of CO2. Deceuninck's SunShield pigment technology minimizes fading in dark frames exposed to high UV levels. Academic trials with flax-carbon bio-hybrid laminates have shown 24% higher stiffness compared to pure carbon parts, indicating potential for architectural applications.

Limited Installer Awareness in Developing Regions

Composite frames require specialized anchoring, flashing, and sealing techniques, but certified training is limited outside North America and Europe. The FGIA InstallationMasters program is only available in English and Spanish and requires prior field experience, restricting adoption in regions like India, Indonesia, and sub-Saharan Africa. Warranty claims are 30-50% higher in areas where proper installation techniques are not followed, impacting manufacturer margins and consumer confidence. While companies like Modulex and Interarch embed installation crews within their factories, this approach is not scalable for fragmented small-contractor ecosystems. Augmented-reality tools have improved comprehension, with Andersen reporting a 25% increase in lead conversion, but language barriers and inconsistent smartphone access limit their effectiveness in rural markets.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Modular Facade Factories in Emerging Asia-Pacific

- Insurance-Premium Discounts for Hurricane-Rated GRP Frames

- PFAS-Free Resin Mandates Raising Formulation Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Composite doors accounted for 54.11% of 2025 revenue, but the composite doors and windows market size for composite windows is projected to grow at a 4.81% CAGR through 2031, surpassing the growth rate of doors. In North America, homeowners replace windows every 15-20 years compared to 25-30 years for doors. Additionally, German and French rebates of up to EUR 60,000 per home and EUR 100 per window are driving faster payback periods. ENERGY STAR Most Efficient criteria with U-factors < 0.22 continue to support premium positioning.

Rehau's SLINOVA X sliding system with a 32 mm sash is designed for balcony doors in Europe, while Andersen's expanded 100 Series line has exceeded 10 million units sold, highlighting scale advantages. Deceuninck and Alpen have introduced Elegant triple-pane windows with U-values as low as 0.09, catering to electrochromic retrofits. Doors remain dominant in security and egress applications, with GRP options meeting BS 6853 and EN 45545 fire safety standards.

Geography Analysis

Europe contributed 43.24% of 2025 revenue, supported by generous retrofit programs such as Germany's BEG EM grants of up to EUR 60,000 and 20% subsidies for window upgrades. France's MaPrimeRenov' offers EUR 40-100 per window, and the United Kingdom's ECO4 scheme provides GBP 5,000-15,000 based on household income. Even as Italy's Superbonus drops to 70% in 2024 and phases out, pent-up applications are sustaining demand. The upcoming Digital Product Passport will promote transparent material data, likely favoring FRP systems with lower embodied carbon. Consolidation is accelerating, as evidenced by Eurocell's 2025 acquisition of Alunet Group to scale delivery amid the retrofit surge.

North America is driven by hurricane risk mitigation and federal tax incentives. Wind-storm insurance discounts of 10-45% in Florida reduce GRP window payback periods to under three years, while the Energy Efficient Home Improvement Credit reimburses up to USD 600 per opening. Andersen's USD 420 million expansion in Goodyear, Arizona, doubled Fibrex capacity and reduced freight costs by 15%, improving service in western states. Canada's Greener Homes Grant provides CAD 125-250 per opening, and Mexico's housing recovery in the Bajio corridor is boosting composite adoption.

Asia-Pacific posts the fastest 5.21% CAGR through 2031, fueled by off-site fabrication. Modulex Global's mega-factory near Mumbai produces up to 300,000 m2 of unitized facades annually. China's codes cap U-values at 1.5-2.0 W/m2*K, and its 14th Five-Year Plan targets 350 million m2 of retrofits, driving demand for high-performance frames. Australia's NCC 2022 and upcoming 2025 revisions tighten thermal thresholds, while Japan's seismic replacement initiatives target pre-1981 structures. Early but notable traction is seen in Brazil, where housing recovery is underway, and Saudi Arabia, where giga-projects such as NEOM specify low-carbon composite curtain walls.

- ANDERSEN CORPORATION

- Apeer

- Deceuninck

- Door-Stop International Limited

- Ecoste

- Emplas

- ETO Doors

- Eurocell Plc

- Fibertec Window and Door

- Hurst

- JELD-WEN, Inc.

- Kommerling

- Marvin

- Oknoplast

- Owens Corning

- Pella Corporation

- Plastpro

- Rehau Group

- Safestyle

- Spitfire Doors

- Visen Industries Limited

- VPI Quality Windows, Inc.

- Window Supply Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for energy-efficient building envelopes

- 4.2.2 Low maintenance and superior durability of composites

- 4.2.3 Surge in modular facade factories in emerging Asia-Pacific

- 4.2.4 Insurance-premium discounts for hurricane-rated GRP frames

- 4.2.5 Smart-glazing-ready Composite Frames

- 4.3 Market Restraints

- 4.3.1 Limited installer awareness in developing regions

- 4.3.2 Ambiguous carbon-footprint labelling for hybrid WPC frames

- 4.3.3 Anticipated PFAS-free resin mandates raising formulation costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Composite Doors

- 5.1.2 Composite Windows

- 5.2 By Material Type

- 5.2.1 Glass Reinforced Plastic (GRP)

- 5.2.2 Wood-Plastic Composite (WPC)

- 5.2.3 Fibre-Reinforced Polymer (FRP)

- 5.2.4 Other Material Types (Carbon, Bio-composite)

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial/Institutional

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 Australia

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ANDERSEN CORPORATION

- 6.4.2 Apeer

- 6.4.3 Deceuninck

- 6.4.4 Door-Stop International Limited

- 6.4.5 Ecoste

- 6.4.6 Emplas

- 6.4.7 ETO Doors

- 6.4.8 Eurocell Plc

- 6.4.9 Fibertec Window and Door

- 6.4.10 Hurst

- 6.4.11 JELD-WEN, Inc.

- 6.4.12 Kommerling

- 6.4.13 Marvin

- 6.4.14 Oknoplast

- 6.4.15 Owens Corning

- 6.4.16 Pella Corporation

- 6.4.17 Plastpro

- 6.4.18 Rehau Group

- 6.4.19 Safestyle

- 6.4.20 Spitfire Doors

- 6.4.21 Visen Industries Limited

- 6.4.22 VPI Quality Windows, Inc.

- 6.4.23 Window Supply Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment