|

시장보고서

상품코드

2062148

플라스틱 압출기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Plastic Extrusion Machine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

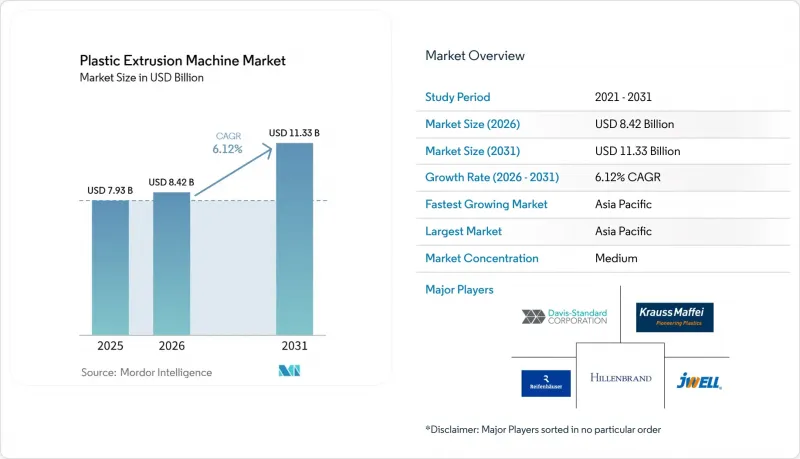

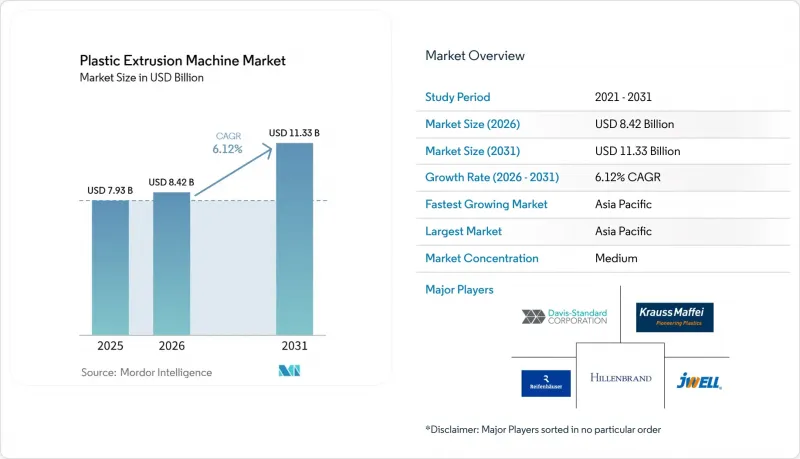

Mordor Intelligence에 의하면, 플라스틱 압출기 시장 규모는 2025년에 79억 3,000만 달러, 2026년에 84억 2,000만 달러가 되어, 2031년까지 113억 3,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 6.12%로 성장할 전망입니다.

본 보고서는 기계 유형(단축 압출, 이축 압출 등), 공정 유형(인플레이션 필름 압출, 시트/필름 압출 등), 자동화 수준(반자동, 기존 수동/릴레이식, 완전 자동 SCADA/IoT 대응), 최종 사용자 산업(포장, 건축 및 건설 등) 및 지역(아시아태평양, 북미 등)에 따라 분류되어 있습니다.

세계 플라스틱 압출기 시장 동향 및 분석

자동화 및 에너지 절약 기계의 발전

Bausano사의 ORQUESTRA 4.0과 같은 중앙 제어 플랫폼은 가동 중인 실시간 데이터를 수집하여 유지보수 작업을 계획합니다. 이러한 접근 방식을 통해 예상치 못한 가동 중단 시간을 줄여, 유럽의 전력 가격 급등 속에서도 컨버터가 수익성을 유지할 수 있도록 지원합니다. 2026년, SML사는 캐스트 필름 라인에 단위 에너지 투입량을 10-15% 절감하고 겔 발생을 20% 줄인 이축 스크류 시스템을 도입했습니다. 이번 개발은 에너지 효율과 품질 향상에 대한 관심이 높아지고 있음을 여실히 보여주고 있습니다. 코페리온(Coperion)의 라이프사이클 관리 제품군 ‘C-Beyond’는 기어박스의 진동을 모니터링하여 중대한 고장을 예방할 수 있는 경고를 제공합니다. 이 기능은 설비의 수명 연장을 지원하며, 숙련 기술자의 은퇴로 인한 과제를 해결합니다. 독일과 미국이 조기 도입을 주도하고 있으며, 총소유비용(TCO) 절감이 구매 결정의 중요한 요인으로 작용하여 자동화를 촉진하고 있습니다.

재활용 폴리머 및 생분해성 폴리머의 압출 성형에 대한 수요 증가

EU의 포장 및 포장 폐기물 규정에 따르면, 2030년부터 2040년까지 재활용 소재 함량을 30-65%로 의무화하고 있어, 분진이 많은 플레이크 스트림을 트윈 스크류 스타드 피딩 방식으로 처리하는 라인으로의 개조가 잇따르고 있습니다. 코펠리온의 STS 35 Mc 11은 맞물리는 스크류가 자체 세척 기능을 수행하고 용융 온도를 제어함으로써, 오염된 재생재의 처리 능력을 27% 향상시킵니다. 2032년까지 모든 포장재를 재활용 가능하거나 퇴비화 가능하도록 하라는 캘리포니아주의 요건에 따라, 바이오 PLA 압출 라인에 대한 관심이 높아지고 있습니다. 각 제조업체는 내마모성 스크류, 더욱 정밀한 체류 시간 제어, 그리고 재생 폴리머의 품질을 보호하는 저전단 용융 구역을 도입하여 이에 대응하고 있으며, 플라스틱 압출기 시장 전체의 가치 제안을 재구축하고 있습니다.

신규 플라스틱 사용에 관한 환경 규제

캐나다의 일회용 플라스틱 금지 조치와 캘리포니아주의 SB 54 법안에 따라, 소매업체와 음식점들은 신규 원료에서 재활용 원료나 퇴비화 가능한 원료로 전환해야 합니다. 이러한 규제에 대응함에 따라 식품용 rPET 수요가 증가하고 있지만, 그 가격은 신재에 비해 25% 더 비쌉니다. 또한, 각 변환기 제조업체들은 촉박한 납기 속에서 새로운 배합 검증에 매진하고 있습니다. 유럽에서는 2030년부터 재활용 의무화가 시행됨에 따라, 층간 박리가 쉽지 않은 다층 라미네이트의 사용이 제한될 것입니다. 생산 라인을 개조할 수 없는 컨버터는 브랜드 소유주들이 추적 가능한 재생 소재를 제공하는 공급업체를 점점 더 선호하게 됨에 따라 계약을 잃을 위험이 있습니다.

부문별 분석

2축 스크류 유닛은 2031년까지 연평균 성장률(CAGR)이 6.21%이 되어, 이는 플라스틱 압출기 시장 전체보다 더 빠르게 성장할 것으로 전망됩니다. 2025년에는 단축 스크류 기계가 플라스틱 압출기 시장 점유율의 53.11%를 차지했으나, 이러한 성장 추세는 다양한 지역에서 관찰되고 있습니다. 플라스틱 압출용 실험용 이축 스크류 시스템 시장 규모는 현재로서는 비교적 작지만, 빠른 속도로 확대되고 있습니다. 이러한 추세는 각지의 컨버터들이 생산 규모를 확대하기 전에 재활용 소재나 바이오 배합재를 사용한 시험 생산을 진행하고 있기 때문입니다.

모듈식 스크류 요소를 통해 작업자는 혼련, 이송, 탈휘발 섹션을 조정할 수 있으며, 이를 통해 0.1%의 첨가량에서도 안료 분산성이 향상되고, 흡습성 폴리머의 열적 열화를 방지하는 데 도움이 됩니다. 설비 투자는 스크류 직경 증가에 따라 늘어나지만, 처리 능력은 그 직경의 제곱에 비례하여 증가하므로, 대량 생산 플랜트에서 kg당 비용은 절감됩니다. 단일 스크류 기계는 유지보수 요건이 비교적 간단하기 때문에 파이프 및 프로파일 분야에서는 여전히 주류를 이루고 있습니다. 그러나 컨버터가 트윈 스크류 기계에서만 안정적으로 처리할 수 있는 고재활용률 배합 레시피를 인증하고 있는 지역에서는 그 시장 점유율이 서서히 감소하고 있습니다.

2025년에는 인플레이션 필름이 매출 점유율의 32.24%를 차지했습니다. 그러나 브랜드 소유주들 사이에서 단일 소재 배리어 구조에 대한 선호도가 높아지고 있는 점을 반영하여, 압출 코팅 및 라미네이션 시장은 연평균 성장률(CAGR) 6.42%로 성장할 것으로 전망됩니다. 플라스틱 압출기 시장, 특히 9-11층 코팅 라인 시장은 식품 브랜드들이 혼합 라미네이트 파우치에서 향후 도입될 A등급 재활용 가능 라벨 기준을 충족하는 전 PE 소재 대체품으로 전환함에 따라 확대되고 있습니다.

에너지 감사에 따르면, 공압출 성형의 에너지 소비량은 1제곱미터당 2.6kWh 미만으로, 이는 용제계 라미네이트 생산의 에너지 사용량의 약 절반 수준입니다. 이를 통해 변환기는 에너지 비용과 용제 배출과 관련된 규정 준수 비용을 절감할 수 있습니다. 인도 및 아세안 지역에서는 파이프, 튜브, 프로파일 생산 라인이 여전히 인프라 수요를 충족시키고 있지만, 투자는 점차 배리어 필름 생산 라인으로 이동하고 있습니다. 이 라인들은 생고기나 즉석식품 등 제품의 유통기한 연장이 필요한 계약에 대응할 수 있도록 설계되었습니다.

지역별 분석

2025년, 아시아태평양은 전 세계 매출의 48.22%를 차지해, 중국, 인도 및 아세안(ASEAN) 국가들의 생산 능력 확대에 힘입어 2031년까지 연평균 성장률(CAGR) 6.88%를 달성할 것으로 전망됩니다. 3,200개의 정유사와 3,460만 톤의 석유화학 생산 능력을 보유한 태국에서는 재활용 분야에서 개선의 여지가 있습니다. 정책 입안자들이 보다 엄격한 순환형 경제 목표를 수립한다면, 성장의 기회가 생길 가능성이 있습니다.

북미에서는 특히 캘리포니아주의 SB 54 법안이나 캐나다의 규제 강화 등으로 인해, 신규 시설 건설보다 기존 시설의 개보수가 우선시되고 있습니다. 그러나 기계적 재활용률이 낮기 때문에 유럽산 인증 rPET 수입에 의존하고 있으며, 이로 인해 이축 스크류식 재생 라인에 대한 투자가 지속적으로 증가하고 있습니다. 멕시코는 특히 전기차용 전선 및 식품 접촉용 필름 분야에서 니어쇼어링 투자를 유치하고 있으며, USMCA 협정에 따라 미국 OEM 업체에 대한 국경을 넘는 공급을 촉진하고 있습니다.

유럽에서는 업계에서 가장 엄격한 규제를 준수하며 사업을 운영하고 있습니다. PPWR이 재생 원료 함유율과 재활용 적합 등급에 중점을 두고 있기 때문에 각 변환업체들은 온라인 품질 분석 기능을 갖춘 첨단 5-11층 공압출기를 도입하도록 권장받고 있습니다. 독일과 이탈리아는 자동화 도입을 주도하고 있는 반면, 동유럽과 북유럽 국가들에서는 고진공 비휘발성 압출기가 필요한 화학적 재활용 원료 조제가 시범적으로 이루어지고 있습니다. 남미와 중동에서는 성장 정도에 차이가 있습니다. 브라질은 환율 변동에도 불구하고 사일리지용 필름 생산 라인에 대한 투자를 지속하고 있으며, 사우디아라비아는 수자원 인프라 수요에 대응하기 위해 HDPE 파이프 생산 능력을 확대되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the plastic extrusion machine market size is projected to be USD 7.93 billion in 2025, USD 8.42 billion in 2026, and reach USD 11.33 billion by 2031, growing at a CAGR of 6.12% from 2026 to 2031.

This report is Segmented by Machine Type (Single Screw Extrusion, Twin Screw Extrusion, and More), Process Type (Blown Film Extrusion, Sheet/Film Extrusion, and More), Automation Level (Semi-Automated, Conventional Manual/Relay-based, and Fully-Automated SCADA/IoT-enabled), End-User Industry (Packaging, Building and Construction, and More), and Geography (Asia-Pacific, North America, and More).

Global Plastic Extrusion Machine Market Trends and Insights

Advancements in Automation and Energy-Efficient Machinery

Centralized control platforms, such as Bausano's ORQUESTRA 4.0, collect live operating data and organize maintenance events. This approach reduces unscheduled downtime, helping converters manage margins amid rising power prices in Europe. In 2026, SML introduced a twin-screw system that achieved a 10-15% reduction in specific energy input and a 20% decrease in gels on cast-film lines. This development highlights the growing focus on energy efficiency and quality improvements. Coperion's C-Beyond lifecycle suite monitors gearbox vibrations and provides alerts to prevent catastrophic failures. This feature supports asset-life extensions, addressing challenges posed by the retirement of skilled technicians. Germany and the U.S. are leading early adoption, with the reduced total cost of ownership driving automation as a critical factor in purchase decisions.

Rising Demand for Recycled and Biodegradable Polymer Extrusion

The EU Packaging and Packaging Waste Regulation mandates 30-65% recycled content between 2030 and 2040, prompting a wave of line retrofits that favor twin-screw starve-feeding of dusty flake streams. Coperion's STS 35 Mc 11 boosts throughput by 27% on contaminated regrind because intermeshing screws self-clean and control melt temperature. California's requirement that all packaging be recyclable or compostable by 2032 lifts interest in bio-based PLA extrusion lines. Manufacturers respond with abrasion-resistant screws, tighter residence-time control, and low-shear melting zones that protect recycled polymer integrity, reshaping value propositions across the plastic extrusion machine market.

Environmental Regulations on Virgin-Plastic Use

Canada's prohibition on single-use plastics, along with California's SB 54, is requiring retailers and restaurants to transition from virgin materials to recycled or compostable options. This regulatory compliance has increased demand for food-grade rPET, which is priced 25% higher than its virgin counterpart. Additionally, converters are working within tight deadlines to validate new formulations. In Europe, a 2030 recyclability mandate will restrict multilayer laminates that cannot be easily delaminated. Converters unable to modify their production lines may lose contracts, as brand owners increasingly prefer suppliers that provide traceable recycled content.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Predictive Process Control for Zero-Defect Output

- On-Site Micro-Extrusion for Personalized Medical Implants

- Scarcity of High-Torque Gearbox Suppliers Lengthening Lead Times

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Twin-screw units are projected to grow faster than the broader plastic extrusion machine market, with a 6.21% CAGR through 2031. This growth is observed across various regions, even though single-screw machines accounted for 53.11% of the plastic extrusion machine market share in 2025. The market size for laboratory twin-screw systems in plastic extrusion remains relatively small today, but it is expanding at a notable rate. This trend is driven by converters in different geographies running trial batches of recycled or bio-based formulations before scaling to production.

Modular screw elements allow operators to adjust kneading, conveying, and devolatilizing sections, which improves pigment dispersion at 0.1% loadings and helps prevent thermal degradation in hygroscopic polymers. Capital investment increases with screw diameter, but throughput grows with the square of that diameter, reducing cost per kilogram for high-volume plants. Single-screw machines continue to dominate the pipe and profile sector due to their simpler maintenance requirements. However, their market share is gradually declining in regions where converters are qualifying high-regrind recipes that only twin-screw machines can process consistently.

In 2025, blown film accounted for 32.24% of the revenue share. However, extrusion coating and lamination are anticipated to grow at a CAGR of 6.42%, reflecting the increasing preference among brand owners for mono-material barrier structures. The plastic extrusion machine market, particularly for nine-to-eleven-layer coating lines, is expanding as food brands transition from mixed laminate pouches to all-PE alternatives that align with upcoming grade-A recyclability labels.

Energy audits indicate that co-extrusion consumes less than 2.6 kWh per square meter, which is approximately half the energy usage of solvent-based laminate production. This allows converters to reduce energy expenses and compliance costs related to solvent emissions. While pipe, tubing, and profile lines continue to meet infrastructure demands in India and ASEAN, investments are gradually shifting toward barrier-film lines. These lines are designed to support contracts requiring extended shelf life for products such as fresh meat and ready-to-eat meals.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 48.22% of global revenue and is projected to achieve a CAGR of 6.88% through 2031, supported by capacity expansions in China, India, and ASEAN nations. Thailand, with its 3,200 converters and 34.6 million tonnes of petrochemical capacity, shows room for improvement in recycling. Growth opportunities may arise if policymakers implement stricter circular-economy targets.

In North America, retrofitting facilities is prioritized over constructing new ones, particularly with regulations such as California's SB 54 and Canadian bans becoming more stringent. However, low mechanical-recycling rates have led to a reliance on importing certified rPET from Europe, which continues to drive investments in twin-screw reclamation lines. Mexico is attracting near-shoring investments, particularly in EV wiring and food-contact films, facilitating cross-border supplies to U.S. OEMs under the USMCA agreement.

Europe operates under some of the most stringent regulations in the industry. The PPWR's focus on recycled content and recyclability grades is encouraging converters to adopt advanced five-to-eleven-layer coextruders equipped with online quality analytics. Germany and Italy are leading in automation adoption, while Eastern Europe and the Nordics are testing chemical-recycling feedstock preparation, which requires high-vacuum devolatilization extruders. In South America and the Middle East, growth remains uneven: Brazil is investing in silage-film lines despite currency fluctuations, and Saudi Arabia is increasing its HDPE pipe capacity to address water infrastructure needs.

- Bausano S.p.A, societa unipersonale

- BREYER Maschinenfabrik GmbH

- Coperion GmbH

- Costruzioni Meccaniche Luigi Bandera SpA

- Cowell (Nanjing) Extrusion Machinery Co., Ltd.

- Davis-Standard, LLC

- Hillenbrand

- JianTai

- JWELL Extrusion Machinery Co., Ltd.

- Kolsite Group (Rajoo Engineers)

- KraussMaffei

- KUNG HSING PLASTIC MACHINERY CO., LTD.

- Leistritz Extrusionstechnik GmbH

- Nanjing KY Chemical Machinery

- Qingdao Shansu Extrusion Equipment Co.,ltd

- Reifenhauser Group

- SML Maschinengesellschaft mbH

- The Japan Steel Works Ltd.

- Windsor Machines Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advancements in automation and energy-efficient machinery

- 4.2.2 Rising demand for recycled and biodegradable polymer extrusion

- 4.2.3 Government incentive schemes for circular-economy equipment

- 4.2.4 AI-enabled predictive process control for zero-defect output

- 4.2.5 On-site micro-extrusion for personalised medical implants

- 4.3 Market Restraints

- 4.3.1 Environmental regulations on virgin-plastic use

- 4.3.2 Scarcity of high-torque gearbox suppliers lengthening lead-times

- 4.3.3 Skilled operator shortage amid demographic shift

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Machine Type

- 5.1.1 Single Screw Extrusion

- 5.1.2 Twin Screw Extrusion

- 5.1.3 Multi-screw and Exotic Configurations

- 5.1.4 Ancillary Down-stream Equipment

- 5.2 By Process Type

- 5.2.1 Blown Film Extrusion

- 5.2.2 Sheet / Film Extrusion

- 5.2.3 Tubing and Profile Extrusion

- 5.2.4 Pipe Extrusion

- 5.2.5 Extrusion Coating and Lamination

- 5.2.6 Other Process Types

- 5.3 By Automation Level

- 5.3.1 Semi-Automated (PLC-integrated)

- 5.3.2 Conventional (Manual / Relay-based)

- 5.3.3 Fully-Automated (SCADA / IoT-enabled)

- 5.4 By End-user Industry

- 5.4.1 Packaging

- 5.4.2 Building and Construction

- 5.4.3 Automotive and Transportation

- 5.4.4 Electrical and Electronics

- 5.4.5 Consumer Goods and Appliances

- 5.4.6 Medical and Healthcare

- 5.4.7 Agriculture

- 5.4.8 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Bausano S.p.A, societa unipersonale

- 6.4.2 BREYER Maschinenfabrik GmbH

- 6.4.3 Coperion GmbH

- 6.4.4 Costruzioni Meccaniche Luigi Bandera SpA

- 6.4.5 Cowell (Nanjing) Extrusion Machinery Co., Ltd.

- 6.4.6 Davis-Standard, LLC

- 6.4.7 Hillenbrand

- 6.4.8 JianTai

- 6.4.9 JWELL Extrusion Machinery Co., Ltd.

- 6.4.10 Kolsite Group (Rajoo Engineers)

- 6.4.11 KraussMaffei

- 6.4.12 KUNG HSING PLASTIC MACHINERY CO., LTD.

- 6.4.13 Leistritz Extrusionstechnik GmbH

- 6.4.14 Nanjing KY Chemical Machinery

- 6.4.15 Qingdao Shansu Extrusion Equipment Co.,ltd

- 6.4.16 Reifenhauser Group

- 6.4.17 SML Maschinengesellschaft mbH

- 6.4.18 The Japan Steel Works Ltd.

- 6.4.19 Windsor Machines Pvt. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment