|

시장보고서

상품코드

2062153

카르보닐 철분말 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Carbonyl Iron Powder - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

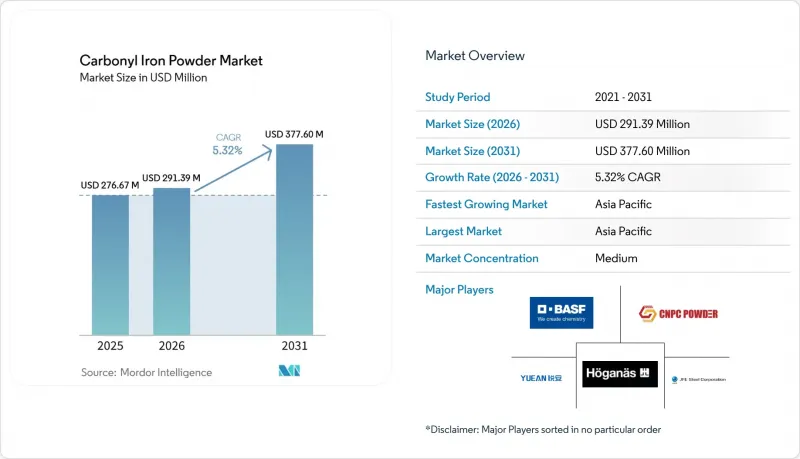

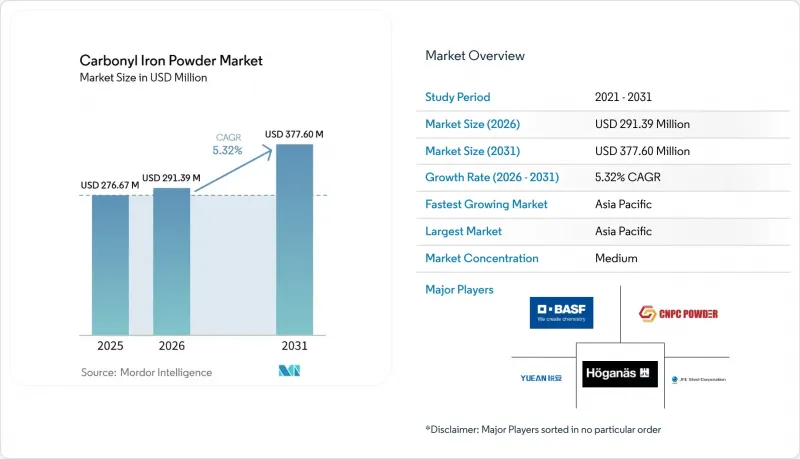

Mordor Intelligence에 의하면, 카르보닐 철분말 시장 규모는 2025년 2억 7,667만 달러로 평가되었습니다. 2026년 2억 9,139만 달러에서 2031년까지 3억 7,760만 달러로 확대되어 2026-2031년까지 연평균 복합 성장률(CAGR)은 5.32%를 나타낼 것으로 예측됩니다.

본 보고서는 유형별(환원 카르보닐 철분말 및 분무 건조 카르보닐 철분말), 순도 등급별(표준 Fe 97% 이상, 기타), 최종 사용자 산업별(전자 및 전기, 자동차, 의료 및 제약, 기타), 지역별(아시아태평양, 북미, 유럽, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 카르보닐 철분말 시장 동향 및 분석

경량 전기차 구동계 부품에 대한 분말 야금 기술의 활용 확대

전기자동차 제조업체들은 기어, 캠, 브래킷 등의 분말 야금 부품의 채택을 확대되고 있습니다. 이러한 부품들은 500 MPa 이상의 피로 강도를 유지하면서 구동계의 질량을 15%에서 20%까지 줄이는 데 도움이 됩니다. 이러한 경량화를 통해 1Kg을 줄일 때마다 15-20km의 항속 거리 연장이 가능해집니다. Porite의 사례 연구에 따르면, 기계 가공된 강재에 비해 20%에서 30%의 비용 절감 효과가 나타났습니다. 마찬가지로, Sterling Sintered Technologies는 카르보닐 철분을 사용한 연자성 복합재료를 통해 코어 손실을 20% 줄이고 모터 크기를 30% 축소할 수 있었다고 보고했습니다. 전기자동차 분야에서 경량이며 고효율인 부품에 대한 수요가 증가함에 따라, 분말 야금 솔루션의 도입이 촉진되고 있습니다. 카르보닐 철분말은 구형 형태와 뛰어난 소결성 덕분에 고성능 용도 분야에서 주목을 받고 있습니다. 1-5 마이크론 범위 내에서 입자 직경을 맞춤 설정하고, 와전류 손실을 최소화하기 위한 사전 절연 등급을 제공할 수 있는 공급업체는 더 높은 가격을 책정할 수 있을 것으로 보입니다. 반면, 이러한 능력을 갖추지 못한 생산자들은 자동차 제조업체들이 구매량을 무기로 삼아 가격 인하를 요구해 오기 때문에 이익률 압박에 직면할 가능성이 있습니다.

소형 의료기기용 금속 사출 성형의 보급

2024년, 의료 및 치과용 금속 사출 성형(MIM)의 매출액은 5억 7,800만 달러에서 18억 8,000만 달러 사이였으며, 연평균 성장률(CAGR)은 약 9%를 기록했습니다. 카르보닐 철분이 선호되는 이유는 그 구형 입자 때문입니다. 이를 통해 60부피%의 고형분 충진이 가능해지며, 소결 후 이론 밀도의 95%를 초과하는 밀도를 달성할 수 있습니다. USP 및 ASTM B883-10 규격을 충족하기 위해 산소 함량은 0.2%로 제한되어 있으며, 이로 인해 체액 환경에서 기공률 감소에 기여하고 있습니다. FDA 21 CFR 820의 문서화 요건이 강화됨에 따라, 이를 준수하지 못하는 공급업체는 수익성이 높은 계약에서 제외될 가능성이 있습니다. 0.05mm 이하의 공차와 1.6 마이크로미터보다 미세한 표면 마감을 실현할 수 있는 금속 사출 성형은 교정용 브라켓이나 이식형 하우징의 제조에 필수적입니다.

직장 내 나노입자 흡입에 관한 법적 책임

규제 당국은 체계적인 검토 결과 질병과의 일관된 연관성이 확인되지 않았음에도 불구하고, 작업장 내 산화철 노출 상한치를 10 mg/m³로 설정했습니다. 현재, 2027년 7월까지 실시간 분진 모니터링 및 건강 모니터링을 의무화하고 있습니다. HEPA 필터 도입, 분기별 감사, 건강 상태 추적 등 규정 준수 조치를 강화함에 따라 생산 라인 1개당 연간 5만-15만 달러의 추가 비용이 발생하고 있습니다. 이러한 비용 상승에 따라 보험사는 보험료를 15%에서 25%까지 인상했습니다. 대형 통합 제조업체들은 이러한 비용을 잘 관리하고 있지만, 중소 가공업체들은 재정적 압박에 직면해 있어 시장에서 철수하게 될 가능성이 있습니다. 이러한 추세에 따라 카보닐 철분말 시장은 점차 통합이 진행되는 방향으로 나아가고 있습니다.

부문별 분석

2025년, 저급 제품, 의약품용 첨가제, 금속 사출 성형 의료 부품(산소 함량 0.2% 이하, 입자 직경 1-10 마이크로미터)은 저급 부문에서 카르보닐 철분말 시장의 67.11%를 차지했습니다. 생산에는 20 MPa 이상에서 120시간을 초과하는 사이클로 가동되는 반응기가 필요하며, 이를 통해 99.5% 이상의 철 순도를 달성하고 있습니다. 이러한 특성 덕분에 충분한 생강도와 이론 기준의 95%를 초과하는 치밀화가 확보되어, 가격 민감도가 비교적 안정적인 헬스케어 및 뉴트라슈티컬 분야의 요구를 충족시키고 있습니다.

8 MPa 반응기에서 60시간에 걸쳐 제조되는 분무 코발트철 분말 시장은 연평균 성장률(CAGR) 5.88%를 나타낼 것으로 전망됩니다. 이러한 성장은 3-8 마이크로미터라는 비교적 좁은 D50 분포에 기인하며, 연자성 복합재료, 특히 50-100 kHz 인버터 코일에서 와전류 손실을 줄이는 데 기여하고 있습니다. 이 부문은 아시아태평양의 자동차 프로그램에서 800V 전기차 플랫폼과 실리콘 카바이드 인버터의 채택 확대에 힘입어 성장하고 있습니다. 사전 절연 처리된 아토마이즈 등급 제품을 공급하는 업체들은 고주파 인덕터 시장에서 입지를 강화하고 있으며, 이 부문에서는 코어 손실이 1% 감소할 때마다 충전 시간이 0.5% 단축됩니다. 또한, 고압 환원법과 중압 분무법 모두를 통해 생산이 가능한 듀얼 라인 생산업체는 카르보닐 철분말 시장의 다양한 수요에 대응하면서도 수익성을 유지할 수 있는 입장에 있습니다.

지역별 분석

2025년, 아시아태평양은 매출의 42.27%를 차지했으며, 2031년까지 연평균 성장률(CAGR)은 6.31%를 나타낼 것으로 전망됩니다. 이러한 성장은 전 세계 생산 능력의 45% 이상을 차지하며, 2023년 수요가 8,000톤을 넘어설 것으로 예상되는 중국이 수행하는 중요한 역할에 힘입어 이루어지고 있습니다. 2025년 1분기, 중국의 한 생산업체는 동남아시아와 북미의 고객 수요에 대응하기 위해 1만 2,000톤 규모의 신규 생산 라인을 가동할 것이라고 발표했습니다. 인도는 운송 비용에 20%-30%의 추가 비용을 부담하고 있으며, 2025년에는 1,200-1,500톤을 수입해, 지역적 유통 허브의 필요성이 제기되었습니다.

북미에서는 항공우주, 방위, 제약 부문이 수요를 주도하고 있으며, ASTM 및 USP의 추적성이 중요시되고 있습니다. 앨라배마주에 위치한 아메리칸 카보닐의 공장은 국내 공급에서 중요한 역할을 하고 있습니다. 또한, 호가나스(Hoganas)사의 바이오차 대체 이니셔티브를 통해 2026년까지 CO₂ 배출 강도를 15% 감축할 것으로 예상되며, 이는 OEM의 스코프 3 목표와 부합합니다. 유럽에서는 BASF의 루트비히스하펜 공장이 2023년에 생산 능력을 800톤 증설했으며, 현재는 서브마이크론급 제품에 대해 더욱 엄격한 분류 기준을 적용하고 있습니다. 그러나 지침 2024/1785에 따라 규정 준수 비용이 증가함에 따라, 중소규모의 변환기 업체들은 사업 통합이나 이전을 검토하고 있습니다.

남미와 중동 및 아프리카는 여전히 수입에 전적으로 의존하고 있으며, 8-12주의 리드타임이라는 과제에 직면해 있습니다. 500-1,000톤 규모의 재고를 갖춘 보세 지역 창고와 기술 서비스 센터를 설립함으로써, 10-15%의 가격 프리미엄을 확보할 수 있을 것으로 보입니다. 다국적 바이어들이 EU 및 미국의 기준에 따라 공급업체 감사를 실시하고 있기 때문에 이러한 접근 방식은 특히 중요합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the carbonyl iron powder market size is projected to expand from USD 276.67 million in 2025 and USD 291.39 million in 2026 to USD 377.60 million by 2031, registering a CAGR of 5.32% between 2026 to 2031.

This report is Segmented by Type (Reduced Carbonyl Iron Powder and Atomized Carbonyl Iron Powder), Purity Grade (Standard More Than or Equal To 97% Fe, and More), End-User Industry (Electronics and Electricals, Automotive, Healthcare and Pharmaceuticals, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Carbonyl Iron Powder Market Trends and Insights

Surge in Powder-Metallurgy Use for Lightweight Electric Vehicle Drivetrain Parts

Electric-vehicle manufacturers are increasingly adopting powder-metallurgy components such as gears, cams, and brackets. These components help reduce drivetrain mass by 15% to 20% while maintaining fatigue strength above 500 MPa. This reduction contributes to an additional range of 15 to 20 km for every kilogram saved. A case study from Porite indicated a 20% to 30% cost reduction compared to machined steel. Similarly, Sterling Sintered Technologies reported that soft magnetic composites made with carbonyl iron powder reduced core losses by 20% and decreased motor sizes by 30%. The growing demand for lightweight and efficient components in electric vehicles is driving the adoption of powder-metallurgy solutions. Carbonyl iron powder is gaining attention in high-performance applications due to its spherical morphology and high sinterability. Suppliers capable of customizing particle sizes within the 1 to 5 micron range and providing pre-insulated grades to minimize eddy-current losses are positioned to achieve higher pricing. On the other hand, producers without these capabilities may face pressure on margins as automakers leverage their purchasing volumes to negotiate lower prices.

Uptake of Metal-Injection Molding for Miniaturized Medical Devices

In 2024, the revenue from medical and dental metal-injection molding (MIM) ranged between USD 578 million and USD 1.88 billion, with a growth rate of nearly 9% CAGR. The preference for carbonyl iron powder is driven by its spherical particles, which enable a 60 vol% solids loading and achieve densities exceeding 95% of theoretical post-sintering. To meet USP and ASTM B883-10 standards, oxygen content is limited to 0.2%, which helps reduce porosity in body-fluid environments. Suppliers that fail to comply may face exclusion from high-margin contracts, as FDA 21 CFR 820 documentation requirements become stricter. Metal-injection molding, capable of achieving tolerances below 0.05 mm and surface finishes finer than 1.6 µm, is essential for manufacturing orthodontic brackets and implantable housings.

Occupational Nanoparticle Inhalation Liabilities

Regulators, despite a systematic review finding no consistent disease link, have capped workplace iron-oxide exposure at 10 mg m-3. They now require real-time dust monitoring and medical surveillance by July 2027. Compliance upgrades, such as HEPA filtration, quarterly audits, and health tracking, increase costs by USD 50,000 to 150,000 annually per line. This rise in costs has prompted insurers to adjust premiums by 15% to 25%. While large integrated producers are managing these costs, smaller converters are experiencing financial pressure, which could lead to their exit from the market. This development is gradually driving the carbonyl iron powder market toward increased consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Iron-Fortified Micro-Encapsulated Nutraceuticals

- Localized Radar-Absorbing Composites for Autonomous-Vehicle Sensors

- Substitution Threat from Cheaper Water-Atomized Iron Powders

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, reduced grades, pharmaceutical supplements and metal-injection-molding medical parts, requiring oxygen levels of <0.2% and particle sizes between 1-10 µm, accounted for 67.11% of the carbonyl iron powder market under the reduced grades segment. Production depends on reactors operating at ≥ 20 MPa for cycles exceeding 120 hours, achieving iron purity levels above 99.5%. These characteristics ensure adequate green strength and densification surpassing 95% of theoretical standards, meeting the needs of healthcare and nutraceutical applications with relatively stable price sensitivity.

Atomized carbonyl iron powder, produced in 8 MPa reactors over a span of 60 hours, is projected to grow at a 5.88% CAGR. This growth is driven by its tighter D50 distributions of 3-8 µm, which help reduce eddy-current losses in soft magnetic composites, particularly for 50-100 kHz inverter coils. The segment is supported by the increasing adoption of 800-V EV platforms and silicon-carbide inverters in Asia-Pacific's vehicle programs. Suppliers offering pre-insulated atomized grades are gaining traction in high-frequency inductors, where a 1% reduction in core loss results in a 0.5% decrease in charging time. Additionally, dual-line producers capable of both high-pressure reduced and mid-pressure atomized outputs are positioned to maintain margins while addressing the varied demands of the carbonyl iron powder market.

Geography Analysis

In 2025, Asia-Pacific represented 42.27% of the revenue, with a projected 6.31% CAGR through 2031. This growth is supported by China's significant role, holding over 45% of global capacity and a demand exceeding 8,000 tons in 2023. In the first quarter of 2025, Chinese producers announced 12,000 tons of new production lines to cater to customers in Southeast Asia and North America. India, dealing with a 20%-30% premium on landed costs, imported between 1,200 and 1,500 tons in 2025, indicating the need for regional distribution hubs.

In North America, the aerospace, defense, and pharmaceutical sectors drive demand, with a focus on ASTM and USP traceability. American Carbonyl's plant in Alabama plays a key role in the domestic supply. Additionally, Hoganas' biochar substitution initiative is expected to reduce CO2 intensity by 15% by 2026, aligning with OEM Scope 3 targets. In Europe, BASF's site in Ludwigshafen increased capacity by 800 tons in 2023 and is now applying stricter classifications for sub-µm grades. However, Directive 2024/1785 is raising compliance costs, prompting smaller converters to consider consolidation or relocation.

South America and the Middle East & Africa remain fully dependent on imports, facing challenges with lead times of 8 to 12 weeks. Establishing bonded regional warehouses with 500 to 1,000 tons of stock and technical-service centers could enable price premiums of 10% to 15%. This approach is particularly relevant as multinational buyers implement supplier audits aligned with EU and U.S. standards.

- Americal Carbonyl

- BASF

- CNPC Powder

- CRS Holdings, LLC.

- Hoganas AB

- JFE Steel Corporation

- Jiangsu Tianyi Ultra-fine Metal Powder

- Jiangxi Yuean Advanced Materials Co Ltd

- KPT

- Micrometals Inc.

- MUBY Chemicals

- Nanorh

- Rio Tinto

- Shanghai Knowhow Powder-Tech Co.,Ltd

- Sintez-CIP Ltd

- Stanford Advanced Materials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand in EMI-Shielding Applications

- 4.2.2 Increasing Use in Powder Metallurgy and Automotive Components

- 4.2.3 Adoption in Metal Injection-Molding (MIM) for Complex Parts

- 4.2.4 Expansion of Pharmaceutical Iron-Supplement Production

- 4.2.5 Emerging 3-D-Printed EM-Absorber Structures

- 4.3 Market Restraints

- 4.3.1 High Production Cost and Volatile Iron-Carbonyl Feedstock Supply

- 4.3.2 Health and Environmental Risks from Nano-Particle Inhalation

- 4.3.3 Substitution Threat from Cheaper Atomized Iron Powders

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Reduced Carbonyl Iron Powder

- 5.1.2 Atomized Carbonyl Iron Powder

- 5.2 By Purity Grade

- 5.2.1 Standard (more than or equal to 97% Fe)

- 5.2.2 High-Purity (more than or equal to 99% Fe)

- 5.2.3 Ultra-High-Purity (more than or equal to 99.9% Fe)

- 5.3 By End-user Industry

- 5.3.1 Electronics and Electricals

- 5.3.2 Automotive

- 5.3.3 Healthcare and Pharmaceuticals

- 5.3.4 Aerospace and Defense

- 5.3.5 Industrial Machinery

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Americal Carbonyl

- 6.4.2 BASF

- 6.4.3 CNPC Powder

- 6.4.4 CRS Holdings, LLC.

- 6.4.5 Hoganas AB

- 6.4.6 JFE Steel Corporation

- 6.4.7 Jiangsu Tianyi Ultra-fine Metal Powder

- 6.4.8 Jiangxi Yuean Advanced Materials Co Ltd

- 6.4.9 KPT

- 6.4.10 Micrometals Inc.

- 6.4.11 MUBY Chemicals

- 6.4.12 Nanorh

- 6.4.13 Rio Tinto

- 6.4.14 Shanghai Knowhow Powder-Tech Co.,Ltd

- 6.4.15 Sintez-CIP Ltd

- 6.4.16 Stanford Advanced Materials

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment