|

시장보고서

상품코드

2062158

선박용 발전기 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Marine Gensets - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

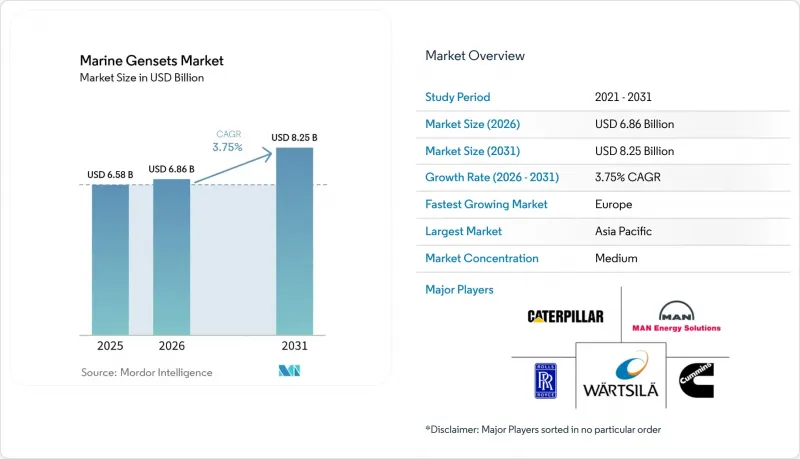

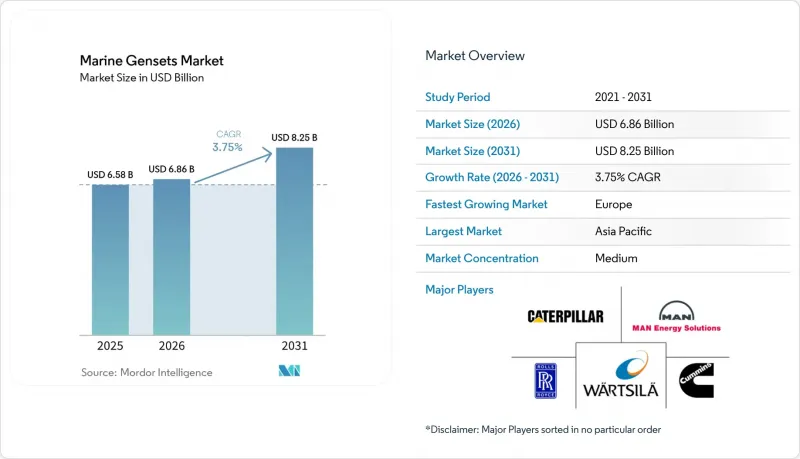

Mordor Intelligence에 의하면, 선박용 발전기 시장 규모는 2025년 65억 8,000만 달러로 평가되었습니다. 2026년에는 68억 6,000만 달러로 확대되어 2026-2031년 CAGR은 3.75%를 나타내, 2031년까지 82억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 정격 출력(500 kW 이하, 501-1,000 kW, 1,000 kW 초과), 연료 유형(디젤, 가스, 디젤·전기 하이브리드, 기타), 용도(주추진, 보조/호텔 부하, 기타), 선박 유형(상업용 화물선, 기타), 지역(북미, 유럽, 아시아·태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 선박용 발전기 시장 동향 및 분석

해운 활동 증가

2024년 전 세계 해상 무역량은 127억 2,000만 톤에 달했으며, 홍해 주변 항로 변경으로 인해 항해 거리가 늘어나 보조 동력에 대한 수요가 증가하고 있습니다. 운항 중인 선단의 약 3분의 1에 해당하는 1,000만 TEU 규모의 컨테이너선 수주 잔고는 최신 보조 기술을 적용하고 있으나, 톤마일 증가세가 둔화될 경우 공급 과잉의 위험이 있습니다. 해체 속도가 둔화됨에 따라 구형 발전기가 계속 가동되고 있어, 배기가스 제어 모듈의 사후 장착 시장을 뒷받침하고 있습니다. 운항사는 항로의 경제성이 변화할 때 재배치가 가능한 모듈식 발전기 뱅크를 선호함으로써 지정학적 불확실성에 대한 헤지를 도모하고 있으며, 이로 인해 플러그 앤 플레이 방식의 보조 패키지를 제공하는 공급업체들이 혜택을 보고 있습니다.

발전기의 설계 및 하이브리드화 분야의 기술 발전

바르칠라사는 2024년에 하이브리드 추진 시스템 31건, 하이브리드 보조 시스템 46건의 도입 실적을 기록하며, 발전기를 최대 효율에 가까운 상태로 가동시키는 배터리 버퍼가 탑재된 아키텍처로의 전환이 확고해졌습니다. 코버스 에너지사는 3,000MWh가 넘는 선박용 배터리를 납품했으며, 이를 통해 페리는 기항 중에 엔진을 정지할 수 있게 되었습니다. 발라드사의 FCwave 연료전지 모듈은 노르웨이의 OSV(해상 지원 선박)에서 해상 시험을 시작했으며, 수소를 보조 전원으로 활용할 수 있는 가능성을 보여주고 있습니다. ABB와 지멘스의 DC 마이크로그리드는 주파수 동기화 제약을 해소하고 고조파 왜곡을 줄이는 동시에, 호텔 부하가 급격하게 변동하는 크루즈선에서 배터리 통합을 간소화합니다.

높은 초기 투자 비용

선택적 촉매 환원(SCR) 장치를 갖춘 2메가와트 듀얼 연료 발전기는 디젤 전용 유닛보다 35%-45% 더 비싸며, 배터리 하이브리드 패키지를 도입할 경우 중형 페리의 보조 동력 시스템에 드는 비용은 800만 달러에 달할 가능성이 있습니다. 자금 조달의 장벽은 여전히 남아 있습니다. 2025년에는 선박 대출 금리가 6%를 넘어섬에 따라, 대출 기관들은 담보 가치 산정 시 하이브리드화 개조 비용을 제외하는 경우가 늘고 있습니다. 캐터필러와 지멘스가 제공하는 가동 시간 기반 리스는 설비 투자(CAPEX)를 운영비(OPEX)로 전환하지만, 도입 사례의 15% 미만을 차지할 뿐이며, 신용 등급이 최고 수준인 선박으로만 제한되어 있습니다.

부문별 분석

2025년 기준으로 1,001-3,000kW 대역은 선박용 발전기 시장의 37.3%를 차지했으며, 파나막스급 컨테이너선 및 아프라막스급 유조선의 보조 동력 수요에 부합합니다. 500kW 이하 시스템 시장 규모는 작지만, 배터리식 페리나 순시선이 모듈식 항속 거리 연장용 발전기를 도입함에 따라 연평균 5.9%의 성장률을 나타낼 것으로 전망됩니다. 롤스로이스가 2025년 바레리아사의 전기 페리를 위해 체결한 2,840kW급 MTU 유닛 8기 계약은 안전상 중요한 설비가 소형화되는 추세를 여실히 보여주고 있습니다. 5메가와트를 초과하는 선박용 발전기 시장 규모는 여전히 틈새 시장에 머물러 있으며, 단일 설비당 10메가와트를 초과하기도 하는 초대형 컨테이너선이나 FPSO에 집중되어 있습니다. 운항사는 5메가와트 발전기 2대 대신 2.5메가와트 발전기 4대를 지정하는 사례가 늘어나고 있으며, 이로 인해 초기 비용은 5-8% 증가하지만, 15년의 사용 수명 동안 예정에 없던 가동 중단 시간을 20% 줄일 수 있습니다.

2025년 매출액 기준 디젤 발전기는 70.1%의 점유율을 유지했으나, 디젤·전기 하이브리드 시스템은 2031년까지 연평균 6.3%의 성장률을 기록하고 있습니다. 배터리 비용은 급격히 하락하고 있으며, 지상 전원 사용 의무화에 따라 발전기가 70%-85%의 부하로 가동되고 배터리가 피크 부하를 관리하는 구성이 우대받고 있습니다. 듀얼 연료(LNG·디젤) 유닛은 이미 가스 설비가 장착된 LNG 운반선이나 크루즈선을 중심으로 큰 시장 점유율을 차지하고 있습니다. Ballard FCwave와 Corvus의 배터리 팩이 양산 단계에 접어들면서, 연료전지 또는 배터리 보조형 발전기는 두 자릿수 성장세를 보이고 있습니다. 기술력 부족으로 인해 도입이 제한되고 있으며, 하이브리드 시스템에는 배터리 및 가스 취급에 관한 전문 지식을 갖춘 엔지니어가 필요하지만, 북유럽이나 미국 걸프 연안 지역에서는 이러한 엔지니어의 급여가 15%-25% 더 높습니다.

지역별 분석

아시아·태평양 지역은 2025년 매출의 45.2%를 차지했으며, 이는 전 세계 조선량에서 중국이 차지하는 63%-70%의 점유율과 LNG 운반선 수주에서 한국이 차지하는 70%의 점유율에 힘입은 것입니다. 2024년 한국의 중국으로의 엔진 수출액은 12억 9,000만 달러를 넘어, 양 지역 간의 긴밀한 협력을 반영하고 있습니다. 츠네이시 조선이 미쓰이 E&S의 조선 자산을 인수하는 것을 포함한 일본의 업계 재편은 더 대규모의 발전기 수주 확보를 목적으로 하고 있습니다. 인도의 ‘Maritime Vision 2030’은 세계 시장 점유율 5%를 목표로 하고 있지만, 여전히 수입된 보조 시스템에 의존하고 있습니다.

유럽은 2031년까지 연평균 성장률(CAGR) 4.6%를 기록하며 가장 빠르게 성장하고 있는 지역으로, 하이브리드화 개조 및 육상 전원 도입을 촉진하는 ‘FuelEU Maritime’의 제재 조항이 이를 뒷받침하고 있습니다. 노르웨이의 NOx 기금은 하이브리드 페리에 보조금을 지급하고 있으며, 스웨덴의 요금 할인은 콜드 아이언 전환을 촉진하고 있습니다. 해군 프로젝트?독일의 53억 유로 규모 F126 호위함 건조 및 영국의 유형 26 프로그램?는 킬, 함부르크, 글래스고의 조선소 주변에서 내충격성 발전기에 대한 수요를 뒷받침하고 있습니다.

북미와 중동은 규모는 작지만, 고사양 제품에 대한 수요가 집중되는 지역입니다. 미 해군의 2026 회계연도 474억 달러 규모의 함정 건조 계획은 비상용 발전기 수주를 뒷받침하고 있지만, 일정 지연으로 인해 국방부는 한국, 일본, 인도의 조선소들과의 유지보수 제휴를 검토해야 하는 상황에 몰리고 있습니다. 캐나다의 400억 캐나다 달러 규모의 ‘국가 조선 전략’에서는 북극권 순찰함 및 지원함을 위해 캐터필러사와 커민스사의 발전기가 채택되었습니다. 사우디아라비아와 모잠비크에서 해양 개발이 확대됨에 따라, 3,000kW 이상의 발전기가 필요한 OSV(해양 지원 선박)의 수주가 증가하고 있습니다. 한편, 브라질의 프레솔트층 프로젝트와 남아프리카공화국의 초계함 구매 사업은 유럽 공급업체들에게 선택적인 수주 기회가 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the marine gensets market size is expected to grow from USD 6.58 billion in 2025 to USD 6.86 billion in 2026 and is forecast to reach USD 8.25 billion by 2031 at 3.75% CAGR over 2026-2031.

This report is Segmented by Power Rating (Up To 500 KW, 501 To 1, 000 KW, and More), Fuel Type (Diesel, Gas, Hybrid Diesel-Electric, Others), Application (Main Propulsion, Auxiliary/Hotel Loads, and More), Vessel Type (Commercial Cargo, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Marine Gensets Market Trends and Insights

Increasing Marine Trade Activities

Global seaborne trade reached 12,720 million tons in 2024, and route diversions around the Red Sea are lengthening voyages and increasing auxiliary-power demand. A 10 million TEU container-ship orderbook, equal to roughly one-third of the active fleet, embeds the newest auxiliary technologies yet risks oversupply if ton-mile growth lags. Older gensets remain in service as scrapping slows, sustaining a retrofit aftermarket for emission-control modules. Operators hedge geopolitical uncertainty by favoring modular genset banks that can be re-sorted as route economics shift, rewarding suppliers of plug-and-play auxiliary packages.

Technological Advancements in Genset Design & Hybridization

Wartsila recorded 31 hybrid-propulsion and 46 hybrid-auxiliary installations in 2024, confirming the pivot to battery-buffered architectures that let gensets run near peak efficiency. Corvus Energy has delivered over 3,000 MWh of maritime batteries, enabling ferries to shut down engines during port stays. Ballard's FCwave fuel-cell module entered sea trials on a Norwegian OSV, hinting at hydrogen's auxiliary potential. DC microgrids from ABB and Siemens eliminate frequency-sync constraints, reduce harmonic distortion, and simplify battery integration on cruise ships whose hotel loads swing drastically.

High Upfront Capital Expenditure

A 2-megawatt dual-fuel genset with selective catalytic reduction costs 35%-45% more than a diesel-only unit, while battery-hybrid packages can lift auxiliary-power spend on a mid-size ferry to USD 8 million. Finance hurdles persist: interest rates on ship mortgages exceeded 6% in 2025, and lenders often exclude hybrid retrofits from collateral value estimates. Operating-hour leasing from Caterpillar and Siemens converts capex to opex but covers less than 15% of placements, restricted to top-tier credits.

Other drivers and restraints analyzed in the detailed report include:

- Stringent IMO Tier III & CII Emission Regulations

- Rising Demand for Offshore Support Vessels (OSVs)

- Volatile Marine Diesel & LNG Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 1,001 to 3,000 kilowatt band held 37.3% marine gensets market share in 2025, matching the auxiliary needs of Panamax container ships and Aframax tankers. Up to 500 kilowatt systems, though smaller in value, are forecast to grow at 5.9% annually as battery-electric ferries and patrol vessels adopt modular range-extender gensets. Rolls-Royce's 2025 contract for eight 2,840-kilowatt MTU units on Balearia electric ferries highlights the shift toward smaller safety-critical sets. The marine gensets market size for units above 5 megawatts remains niche, focused on ultra-large container ships and FPSOs where single gensets can exceed 10 megawatts. Operators increasingly specify four 2.5 megawatt machines instead of two 5 megawatt ones, adding 5%-8% upfront yet cutting unscheduled downtime by 20% over a 15-year life.

Diesel retained 70.1% of 2025 revenue, but hybrid diesel-electric systems are expanding at 6.3% annually to 2031. Battery costs have plunged, and shore-power mandates reward gensets that run at 70%-85% load while batteries manage peaks. Dual-fuel LNG-diesel units held a significant share, centered on LNG carriers and cruise ships where gas is already onboard. Fuel-cell or battery-assisted gensets show double-digit gains as Ballard FCwave and Corvus battery packs reach serial production. Skill gaps limit adoption; hybrid systems need engineers with battery and gas-handling expertise who command 15%-25% wage premiums in Northern Europe and the U.S. Gulf.

Geography Analysis

Asia-Pacific generated 45.2% of 2025 revenue, underpinned by China's 63%-70% share of global shipbuilding volume and South Korea's 70% share of LNG-carrier orders. Korean engine exports to China topped USD 1.29 billion in 2024, reflecting tight regional integration. Japan's consolidation, including Tsuneishi's acquisition of Mitsui E&S shipbuilding assets, aims to secure larger genset contracts. India's Maritime Vision 2030 seeks 5% global share yet relies on imported auxiliary systems.

Europe is the fastest-growing region at a 4.6% CAGR through 2031, propelled by FuelEU Maritime penalties that drive hybrid retrofits and shore-power adoption. Norway's NOx Fund subsidizes hybrid ferries, and Sweden's fee discounts spur cold-ironing upgrades. Naval projects-Germany's EUR 5.3 billion F126 frigate build and the UK Type 26 program-support demand for shock-qualified gensets near Kiel, Hamburg, and Glasgow yards.

North America and the Middle East form smaller yet high-specification pockets. The U.S. Navy's USD 47.4 billion FY 2026 build plan fuels emergency-genset orders, though schedule slippage pushes the Pentagon to explore sustainment tie-ups with Korean, Japanese, and Indian yards. Canada's CAD 40 billion National Shipbuilding Strategy sources Caterpillar and Cummins sets for Arctic patrol and support ships. Offshore expansion in Saudi Arabia and Mozambique lifts OSV orders needing 3,000 kilowatt-plus gensets, while Brazil's pre-salt projects and South Africa's patrol-vessel buys offer selective wins for European suppliers.

- Caterpillar Inc.

- MAN Energy Solutions

- Mitsubishi Heavy Industries Ltd.

- Wartsila Corporation

- Rolls-Royce Holdings plc (Bergen Engines)

- Cummins Inc.

- Volvo Penta

- John Deere Power Systems

- Hyundai Heavy Industries Co. Ltd.

- Yanmar Holdings Co., Ltd.

- Daihatsu Diesel Mfg. Co., Ltd.

- Anglo Belgian Corporation NV

- Weichai Group

- Doosan Infracore Co., Ltd.

- Scania AB

- Isotta Fraschini Motori S.p.A

- Baudouin (Societe Internationale des Moteurs Baudouin)

- Kohler Power Systems

- ABB Ltd (Turbogenerator & Hybrid Systems)

- Aggreko plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing marine trade activities

- 4.2.2 Technological advancements in genset design & hybridization

- 4.2.3 Stringent IMO Tier III & CII emission regulations

- 4.2.4 Rising demand for offshore support vessels (OSVs)

- 4.2.5 Adoption of on-board microgrids / DC power architectures

- 4.2.6 Cold-ironing retrofits driving load-following LNG-ready gensets

- 4.3 Market Restraints

- 4.3.1 High upfront capital expenditure

- 4.3.2 Volatile marine diesel & LNG prices

- 4.3.3 Certification & compliance complexity across flag states

- 4.3.4 Supply-chain bottlenecks for high-pressure fuel-injection components

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Power Rating

- 5.1.1 Up to 500 kW

- 5.1.2 501 to 1,000 kW

- 5.1.3 1,001 to 3,000 kW

- 5.1.4 3,001 to 5,000 kW

- 5.1.5 Above 5,000 kW

- 5.2 By Fuel Type

- 5.2.1 Diesel

- 5.2.2 Gas (NG/LPG)

- 5.2.3 Hybrid Diesel-Electric

- 5.2.4 Dual-Fuel (LNG + Diesel)

- 5.2.5 Fuel-Cell/Battery-Assisted

- 5.3 By Application

- 5.3.1 Main Propulsion

- 5.3.2 Auxiliary/Hotel Loads

- 5.3.3 Emergency/Backup Power

- 5.4 By Vessel Type

- 5.4.1 Commercial Cargo Vessels

- 5.4.2 Tankers and Bulk Carriers

- 5.4.3 Container Ships

- 5.4.4 Offshore Support Vessels

- 5.4.5 Defense/Naval Vessels

- 5.4.6 Leisure and Passenger (Cruise/Ferry/Yacht)

- 5.4.7 Fishing and Workboats

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Spain

- 5.5.2.5 Nordic Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Malaysia

- 5.5.3.6 Thailand

- 5.5.3.7 Indonesia

- 5.5.3.8 Vietnam

- 5.5.3.9 Australia

- 5.5.3.10 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 MAN Energy Solutions

- 6.4.3 Mitsubishi Heavy Industries Ltd.

- 6.4.4 Wartsila Corporation

- 6.4.5 Rolls-Royce Holdings plc (Bergen Engines)

- 6.4.6 Cummins Inc.

- 6.4.7 Volvo Penta

- 6.4.8 John Deere Power Systems

- 6.4.9 Hyundai Heavy Industries Co. Ltd.

- 6.4.10 Yanmar Holdings Co., Ltd.

- 6.4.11 Daihatsu Diesel Mfg. Co., Ltd.

- 6.4.12 Anglo Belgian Corporation NV

- 6.4.13 Weichai Group

- 6.4.14 Doosan Infracore Co., Ltd.

- 6.4.15 Scania AB

- 6.4.16 Isotta Fraschini Motori S.p.A

- 6.4.17 Baudouin (Societe Internationale des Moteurs Baudouin)

- 6.4.18 Kohler Power Systems

- 6.4.19 ABB Ltd (Turbogenerator & Hybrid Systems)

- 6.4.20 Aggreko plc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment