|

시장보고서

상품코드

2062174

왕복동 압축기 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Reciprocating Compressors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

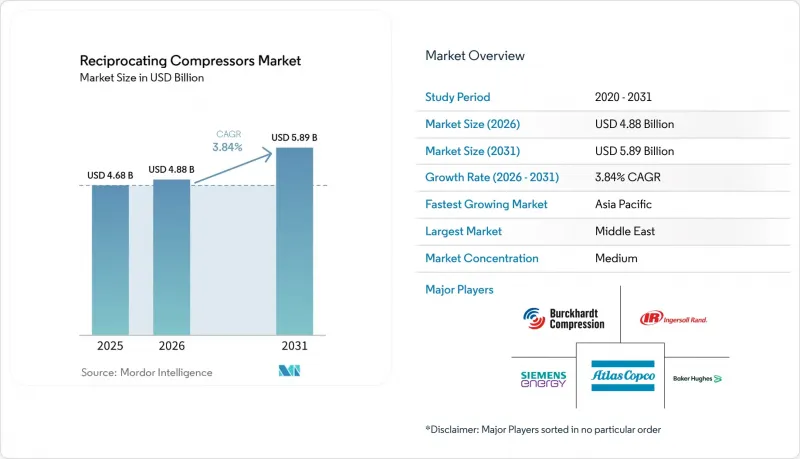

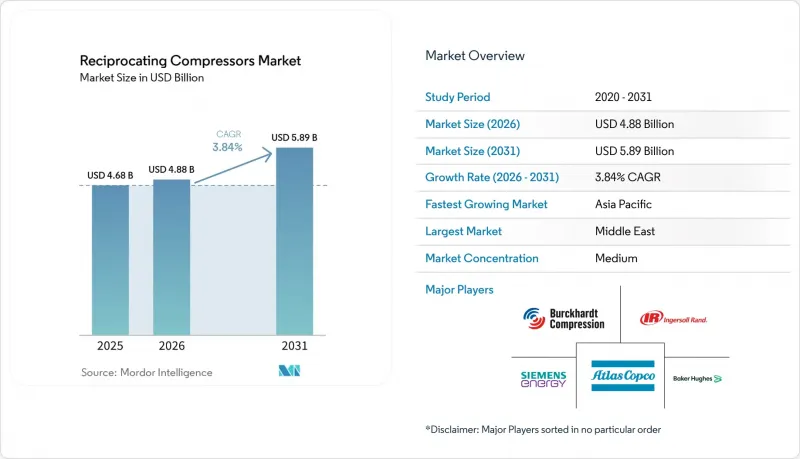

Mordor Intelligence에 의하면, 왕복동 압축기 시장 규모는 2025년 46억 8,000만 달러로 평가되었습니다. 2026년 48억 8,000만 달러에서 2031년까지 58억 9,000만 달러로 확대되어 2026-2031년 CAGR은 3.84%를 나타낼 것으로 예측됩니다.

본 보고서는 압축기의 설계(수평 대향형, 수직 직렬형, V형, 다이어프램형, 복동식), 윤활 방식(오일식, 오일프리식), 단수(단단식, 2단식, 다단식), 최종 사용자 산업(석유 및 가스, 화학제품 및 석유화학제품, 기타) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 왕복동 압축기 시장 동향 및 인사이트

LNG 액화 플랜트의 재건

2025년 이후의 최종 투자 결정에 따라 새로운 LNG 플랜트 건설이 진행되는 가운데, 보일오프 가스의 재액화 및 냉매 용도 분야에서 대형 왕복동 압축기 패키지가 다시 주목받고 있습니다. 2025년 2월 사우디 아람코가 자프라 3단계 프로젝트를 위해 가스 압축 트레인 6기를 발주한 것은 중동에서 오일 프리 고압 기계에 대한 노력을 뒷받침하는 사례입니다. 이에 이어 버크하르트 컴프레션(Burkhardt Compression)도 아부다비의 타지즈 터미널을 대상으로 Laby 4K165-3을 수주하며, 극저온 분야에서 오일프리 제품에 대한 수요가 증가하고 있음을 여실히 보여주었습니다. 카타르의 노스 필드 이스트와 미국 걸프 코스트의 확장 계획에 따라, 향후 몇 년간 대당 1,000마력을 초과하는 수주가 예상됩니다. 제조업체들은 온실가스 감축 목표를 달성하기 위해 전기 모터 구동을 점점 더 많이 채택하고 있으며, 이를 통해 가스 엔진식 1단 압축기에 고유한 메탄 누출을 줄이고 있습니다. 공급망이 긴축되는 가운데, 중요한 크랭크샤프트나 고압 밸브를 재고로 보유한 공급업체들은 가격 결정력을 확보하고 있습니다.

수소 충전 인프라 구축

유럽, 캘리포니아, 일본, 한국에서 의무화된 무공해 트럭 전용 노선에 따라, 수소를 200-500바의 저장 압력에서 350-700바공급 압력까지 승압할 수 있는 다이어프램식 및 다단 왕복동식 기술에 대한 수요가 확대되고 있습니다. 지멘스 에너지가 2026년 1월 함부르크의 ‘그린 수소 허브’를 위해 체결한 계약은 누출이 없고 오일 프리 압축이 필요한 프로젝트의 전형적인 사례입니다. 호비거의 HCP 500 다이어프램 모델은 엘라스토머의 파손을 방지함으로써 유지보수 주기를 8,000시간으로 연장했습니다. 아리엘사는 급유 및 파이프라인 주입용으로 최대 6,000 psig의 수소용 장비를 이미 150대 이상 출하했습니다. 원심식이나 스크류식 기계는 양정이 매우 높을 경우 효율이 떨어지기 때문에 이 틈새 시장에서는 왕복동 프레임이 주류를 이루고 있습니다. 그 결과, 수주 잔고는 2031년까지 왕복동 압축기 시장 전체를 웃도는 속도로 증가할 것으로 전망됩니다.

원유 가격이 배럴당 65달러 미만일 경우 심해 프로젝트에 대한 설비 투자 연기

브렌트 원유 가격이 배럴당 65달러 아래로 떨어지면, 운영사들은 심해 프로젝트에 대한 최종 투자 결정을 보류하고, 가스 리프트, 수출 및 증기 회수 서비스를 위한 압축 패키지 도입을 연기할 것입니다. 국제에너지기구(IEA)의 기록에 따르면, 과거 경기 침체기에는 심해 프로젝트 승인 건수가 사상 최저 수준을 기록했으며, 이는 OEM 업체들의 수주 잔고가 거시경제적 위험에 노출되어 있음을 여실히 보여주고 있습니다. 부유식 생산·저장·하역선(FPSO)은 2-4년의 설계 리드타임이 필요하기 때문에 2026년의 가격 침체는 2020년대 후반의 수주 파이프라인에 연쇄적인 영향을 미치게 될 것입니다. 육상, 석유화학, 수소 관련 사업으로 사업을 전개하고 있는 공급업체는 위험을 분산시킬 수 있습니다.

부문별 분석

수평 대향형 기계는 2025년 매출의 44.19%를 차지하며, 하루 28만 3,000 m³를 초과하는 가스 수거량에 적합한 것으로 나타났습니다. 파이프라인 사업자들은 이러한 프레임이 제공하는 저진동성과 단순화된 기초를 중요하게 여기고 있기 때문에 왕복동 압축기 시장 점유율이 급격히 떨어질 가능성은 낮을 것으로 보입니다. 대조적으로, 다이어프램식 유닛은 2025년 전체 시장 규모에서 차지하는 비중이 극히 미미하지만, 수소 소매 충전소의 보급에 따라 연평균 성장률(CAGR) 4.58%를 나타낼 것으로 전망됩니다. 호비거사의 500바 정격 금속 다이어프램 기술은 엘라스토머 막에 내재된 투과 위험을 제거함으로써, 연료전지차의 주요 분야에서 채택이 확대되고 있습니다. V형 및 인라인 설계는 기계 공장이나 소규모 공정 설비의 콤팩트한 레이아웃에 적합합니다. 3,000 psig를 초과하는 암모니아 및 메탄올 루프에서는 여전히 복동식 실린더가 선택되고 있으며, 이는 왕복동 압축기 시장에서 단일 기술이 모든 용도를 지배하고 있지 않은 이유를 보여줍니다.

제약 및 반도체 업계의 엄격한 순도 규격(ISO 8573-1 Class 0 공기 필수)으로 인해 다이어프램식 압축기의 보급이 촉진되고 있습니다. 2027년에 탭아웃이 예정된 아시아태평양의 팹에서는 스크류식이나 스크롤식 압축기가 150 psig를 초과하면 성능이 저하되기 때문에 오일 프리 금속 다이어프램식 스키드가 선호되고 있습니다. 이에 대해 밸런스형 대향식 압축기 OEM 업체들은 개선된 맥동 댐퍼와 시운전 시간을 30% 단축하는 디지털 트윈 기술로 대응하고 있습니다. 그 결과, 더 빠르게 성장하는 틈새 시장이 주목을 받는 가운데서도, 균형형 대향식 프레임 왕복 압축기 시장 규모는 꾸준히 확대되고 있습니다.

2025년 기준으로, 오일 윤활식 모델은 총 출하량의 63.63%를 차지하며, 미량의 탄화수소가 허용되는 공장용 공기 공급, 중류 가스 집약 및 LNG 냉동 분야를 뒷받침했습니다. 그러나 식품, 음료, 전자기기 제조 공장에서는 클래스 0 기준을 충족하기 위해 프리미엄 가격을 예산에 반영하고 있으며, 이것이 오일 프리 왕복동 압축기의 연평균 성장률(CAGR) 4.23%를 견인하고 있습니다. Burckhardt사의 미로 피스톤 방식 ‘Laby’ 시리즈는 암모니아 재액화 시 교차 오염을 방지합니다. 한편, ELGi사와 CompAir사는 오일 혼입량을 측정 기기의 검출 한계 이하로 억제하는 PTFE 링 키트를 적극 권장하고 있습니다. 소비자용 브랜드는 제품 리콜로 인한 제재를 받게 되므로, 이러한 설비 투자의 높은 비용은 정당화됩니다.

각 제조업체는 제품 수명 주기 전반에 걸친 전력 비용도 고려하고 있습니다. 오일 프리 단계에서는 토출 온도가 높아지기 때문에 많은 설비에서 인터쿨러를 통한 열 회수 시스템을 도입하여 플랜트의 순 에너지 집약도를 낮추고 있습니다. 유럽과 캘리포니아에서 탄소 가격 제도가 도입되고 기존 정유시설의 개보수가 이루어짐에 따라, 왕복동 압축기 시장에서는 이러한 효율 향상이 진행되고 있습니다. 예측 기간 동안에는 유체 윤활식 유닛이 업스트림 및 중류 부문 설비의 주력으로 남아 있을 것으로 보이지만, 제품 로드맵은 분명히 드라이 씰 기술로 향하고 있습니다.

지역별 분석

아시아태평양은 인도의 LNG 터미널 건설 및 중국 연안 지역의 정유시설 개보수 공사로 인해 2025년 매출의 42.59%를 차지했습니다. 이 지역의 각국 정부는 효율화 의무를 강화하고 있으며, 인도의 에너지 효율국은 2026년에 압축기 기준을 강화하여 기준 미달 제품의 교체를 촉진하고 있습니다. 베트남과 인도네시아의 산업 성장이 워크숍용 에어컨 판매를 견인하며, 기초 수요를 뒷받침하고 있습니다. 아시아태평양의 왕복동 압축기 시장 규모는 국내 OEM 업체들이 수입 관세를 피하기 위해 현지에서 생산을 확대함에 따라 계속해서 견조한 추세를 보이고 있습니다.

북미는 셰일가스의 재파쇄 및 수반가스 수거에 힘입어 약 28%의 점유율을 유지했습니다. 크랭크샤프트와 밸브공급망에서 발생하는 병목 현상으로 인해 장비 임대 요율이 상승하고 있으며, 재고를 보유한 기존 기업들이 유리한 입장에 서 있습니다. 또한, 미국에서는 텍사스주에서 캘리포니아주에 이르는 구간에 수소 회랑 시범 사업이 진행 중이며, 700바급 다이어프램 스키드가 조기에 발주되었습니다. 캐나다의 ‘LNG 캐나다 2단계’ 및 ‘우드파이버 LNG’ 프로젝트가 향후 성장 여지를 제공합니다.

유럽은 2025년에 매출의 약 18%를 차지했지만, 음향 출력을 제한하고 저속 설계를 의무화하는 EU 지침 2000/14/EC에 따른 엄격한 소음 규제에 직면해 있습니다. 방음 커버나 가변 속도 구동 장치를 사후 설치하여 기존 설비를 규정에 부합하도록 개조하는 것은 가능하지만, 단위당 비용은 증가합니다. 한편, 연평균 성장률(CAGR)이 4.44%로 예상되는 중동에서는 자프라, 타지즈, 카타르의 노스 필드 이스트와 같은 프로젝트가 가속화되고 있으며, 이들 프로젝트에서는 오일 프리 왕복동 압축기를 블루 암모니아 및 수소 복합 시설에 도입하고 있습니다. 남미에서는 브라질의 프레솔트층 개발과 아르헨티나의 바카 무에르타 셰일층에 연결된 압축 플랜트가 수요 증가를 뒷받침하고 있으며, 아프리카의 성장은 나미비아 및 모잠비크 연안의 심해 유전 발견에 달려 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the reciprocating compressors market size is projected to expand from USD 4.68 billion in 2025 and USD 4.88 billion in 2026 to USD 5.89 billion by 2031, registering a 3.84% CAGR between 2026 to 2031.

This report is Segmented by Compressor Design (Horizontal Balanced-Opposed, Vertical In-Line, V-Type, Diaphragm, and Double-Acting), Lubrication (Oil-Lubricated, Oil-Free), Number of Stages (Single-Stage, Two-Stage, and Multi-Stage), End-User Industry (Oil and Gas, Chemicals and Petrochemicals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Reciprocating Compressors Market Trends and Insights

Renewed LNG Liquefaction Train Build-Out

Large-frame reciprocating packages are returning to favour for boil-off-gas reliquefaction and refrigerant duty as post-2025 final-investment decisions push new LNG trains forward. The February 2025 Saudi Aramco Jafurah Phase 3 award for six gas-compression trains underscores the commitment to oil-free, high-pressure machines in the Middle East. Burckhardt Compression soon followed with Laby 4K165-3 orders for Abu Dhabi's TA'ZIZ terminal, highlighting oil-free demand in cryogenic service. North Field East in Qatar and Gulf Coast expansions in the United States add a multiyear pipeline of orders exceeding 1,000 horsepower per unit. Owners increasingly specify electric-motor drives to meet greenhouse-gas targets, cutting methane slip inherent in gas-engine primaries. As supply chains strain, vendors that stock critical crankshafts and high-pressure valves secure pricing power.

Hydrogen Refuelling Infrastructure Build-Out

Mandated zero-emission truck corridors in Europe, California, Japan, and South Korea are scaling diaphragm and multi-stage reciprocating technology that can raise hydrogen from 200-500 bar storage to 350-700 bar dispensing. Siemens Energy's January 2026 contract for Hamburg's Green Hydrogen Hub typifies projects that need leak-tight, oil-free compression. Hoerbiger's HCP 500 diaphragm model extends service intervals to 8,000 hours by eliminating elastomer failure. Ariel has already shipped more than 150 hydrogen units up to 6,000 psig for refuelling and pipeline injection. Because centrifugal and screw machines lose efficiency at very high heads, reciprocating frames dominate this niche. The resulting order book is on course to outpace the broader reciprocating compressors market through 2031.

Capex Deferments in Deep-Water Projects Below USD 65 per Barrel

When Brent crude slips under USD 65 per barrel, operators freeze deepwater final-investment decisions, postponing compression packages for gas-lift, export, and vapor-recovery service. The International Energy Agency records a historic low in deepwater sanctions during prior downturns, highlighting macro exposure for OEM backlogs. Because floating production, storage, and offloading vessels need two to four years of engineering lead time, price weakness in 2026 would cascade into the late-2020s order funnel. Suppliers with onshore, petrochemical, and hydrogen exposure diversify risk.

Other drivers and restraints analyzed in the detailed report include:

- AI-Enabled Predictive Maintenance Unlocking 3-5 Point Uptime Gains

- Rise in Shale Gas Re-Fracturing Cycles

- Shift from Gas Lift to Electric Submersible Pumps in Mature Fields

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Horizontal balanced-opposed machines commanded 44.19% 2025 revenue, evidencing their suitability for gas gathering volumes above 283,000 m3 per day. The reciprocating compressors market share is unlikely to erode quickly because pipeline operators prize the low vibration and simplified foundation these frames deliver. In contrast, diaphragm units, though just a sliver of 2025 totals, are slated for a 4.58% CAGR as hydrogen retail stations proliferate. Hoerbiger's metal-diaphragm technology, rated 500 bars, removes permeation risks that plague elastomer membranes, expanding acceptance among fuel-cell vehicle corridors. V-type and in-line designs fill compact layouts in machine shops and small process units. Double-acting cylinders, still chosen for ammonia and methanol loops above 3,000 psig, illustrate why no single technology dominates every duty inside the reciprocating compressors market.

Diaphragm expansion is reinforced by stringent purity codes in pharmaceuticals and semiconductors, where ISO 8573-1 Class 0 air is mandatory. Asia-Pacific fabs scheduled for 2027 tape-out favour oil-free metal-diaphragm skids because screw or scroll machines struggle beyond 150 psig. Balanced-opposed OEMs counter with improved pulsation dampers and digital twins that cut commissioning time by 30%. As a result, the reciprocating compressors market size for balanced-opposed frames continues to inch forward even while faster niches steal headlines.

Oil-lubricated variants retained 63.63% volume in 2025, underpinning workshop air, midstream gas gathering, and LNG refrigeration where trace hydrocarbons are tolerated. Yet food, beverage, and electronics plants now budget premium pricing for Class 0 compliance, driving a 4.23% CAGR in oil-free reciprocating compressors. Burckhardt's labyrinth-piston Laby line avoids cross-contamination during ammonia reliquefication, while ELGi and CompAir promote PTFE ring kits that drop oil carryover below instrument-detectable limits. Because consumer-facing brands face product-recall penalties, the capital premium is justified.

Manufacturers also weigh life-cycle electricity costs. Oil-free stages deliver higher discharge temperatures, so many installations integrate intercooler heat recovery that trims net plant energy intensity. The reciprocating compressors market tracks these efficiency gains as brownfield refinery retrofits coincide with carbon-pricing schemes in Europe and California. Although oil-lubricated units will remain the backbone of upstream and midstream fleets for the forecast window, product roadmaps clearly arc toward dry-sealed technologies.

Geography Analysis

Asia-Pacific commanded 42.59% 2025 revenue on LNG terminal builds in India and Chinese coastal refinery upgrades. The region's governments add efficiency mandates India's Bureau of Energy Efficiency tightens compressor standards in 2026 that spur replacement of sub-standard units. Vietnam and Indonesia industrial growth drives workshop air sales, reinforcing baseline demand. The reciprocating compressors market size in Asia-Pacific remains buoyant as domestic OEMs localize production to skirt import duties.

North America held roughly 28% share, underpinned by shale gas re-fracturing and associated gas gathering. Supply-chain pinch points in crankshafts and valves elevate equipment lease rates, advantaging incumbents that carry inventory. The United States also pilot's hydrogen corridors from Texas to California, placing early orders for 700 bar diaphragm skids. Canada's LNG Canada Phase 2 and Woodfibre LNG add future upside.

Europe generated about 18% revenue in 2025 but contends with stringent noise rules under EU Directive 2000/14/EC that cap sound power and force low-speed designs. Retrofitting acoustic wraps and variable-speed drives helps legacy units stay compliant but raises unit cost. Meanwhile, the Middle East, forecast at a 4.44% CAGR, accelerates with Jafurah, TA'ZIZ, and Qatar's North Field East projects that bundle oil-free reciprocating compressors into blue-ammonia and hydrogen complexes. South America's pre-salt developments in Brazil and compression plants linked to Argentina's Vaca Muerta shale underpin incremental demand, while African growth hinges on deepwater discoveries off Namibia and Mozambique.

- Atlas Copco AB

- Ingersoll Rand Inc.

- Burckhardt Compression AG

- Baker Hughes Company

- Siemens Energy AG

- Elliott Group (Ebara Corporation)

- Howden Group Ltd. (Chart Industries)

- Ariel Corporation

- Hitachi Ltd.

- Kobe Steel Ltd.

- Shenyang Blower Works Group Co. Ltd.

- Kirloskar Pneumatic Company Ltd.

- Mitsui E&S Machinery Co. Ltd.

- Sundyne LLC

- Mayekawa Mfg. Co., Ltd.

- Kaeser Kompressoren SE

- Hanwha Power Systems Co. Ltd.

- Shanghai Screw Compressor Co. Ltd.

- Enerflex Ltd.

- MAN Energy Solutions SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Renewed LNG Liquefaction Train Build-Out (Post-2025 FIDs)

- 4.2.2 Hydrogen Refuelling Infrastructure Build-Out

- 4.2.3 Rise in Shale Gas Re-Fracturing Cycles (North America)

- 4.2.4 Mandatory Energy-Efficiency Retrofits in Brown-Field Refineries

- 4.2.5 AI-Enabled Predictive Maintenance Unlocking 3-5 pp Uptime Gains

- 4.2.6 OEM Shift to Modular Skid-Mounted Packages for Offshore FPSOs

- 4.3 Market Restraints

- 4.3.1 Capex Deferments in Deep-Water Projects Below USD 65 bbl

- 4.3.2 Shift from Gas Lift to Electric Submersible Pumps in Mature Fields

- 4.3.3 Industrial Move Toward Oil-Free Screw Units in Food and Pharma

- 4.3.4 Stringent Urban Noise Codes Greater Than 75 dB-A Curbing Inner-City Installations

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Compressor Design

- 5.1.1 Horizontal Balanced-Opposed

- 5.1.2 Vertical In-Line

- 5.1.3 V-Type

- 5.1.4 Diaphragm

- 5.1.5 Double-Acting

- 5.2 By Lubrication

- 5.2.1 Oil-Lubricated

- 5.2.2 Oil-Free

- 5.3 By Number of Stages

- 5.3.1 Single-Stage

- 5.3.2 Two-Stage

- 5.3.3 Multi-Stage

- 5.4 By End-User Industry

- 5.4.1 Oil and Gas

- 5.4.2 Chemicals and Petrochemicals

- 5.4.3 Power Generation

- 5.4.4 Manufacturing and Industrial

- 5.4.5 HVAC and Refrigeration

- 5.4.6 Others End-User Industry (Healthcare, Food and Beverage)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Atlas Copco AB

- 6.4.2 Ingersoll Rand Inc.

- 6.4.3 Burckhardt Compression AG

- 6.4.4 Baker Hughes Company

- 6.4.5 Siemens Energy AG

- 6.4.6 Elliott Group (Ebara Corporation)

- 6.4.7 Howden Group Ltd. (Chart Industries)

- 6.4.8 Ariel Corporation

- 6.4.9 Hitachi Ltd.

- 6.4.10 Kobe Steel Ltd.

- 6.4.11 Shenyang Blower Works Group Co. Ltd.

- 6.4.12 Kirloskar Pneumatic Company Ltd.

- 6.4.13 Mitsui E&S Machinery Co. Ltd.

- 6.4.14 Sundyne LLC

- 6.4.15 Mayekawa Mfg. Co., Ltd.

- 6.4.16 Kaeser Kompressoren SE

- 6.4.17 Hanwha Power Systems Co. Ltd.

- 6.4.18 Shanghai Screw Compressor Co. Ltd.

- 6.4.19 Enerflex Ltd.

- 6.4.20 MAN Energy Solutions SE

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment