|

시장보고서

상품코드

2062176

탄화로 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Carbonization Furnace - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

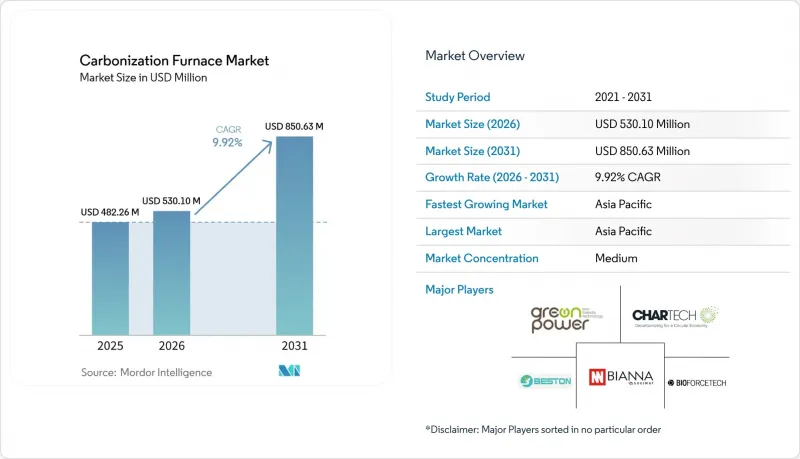

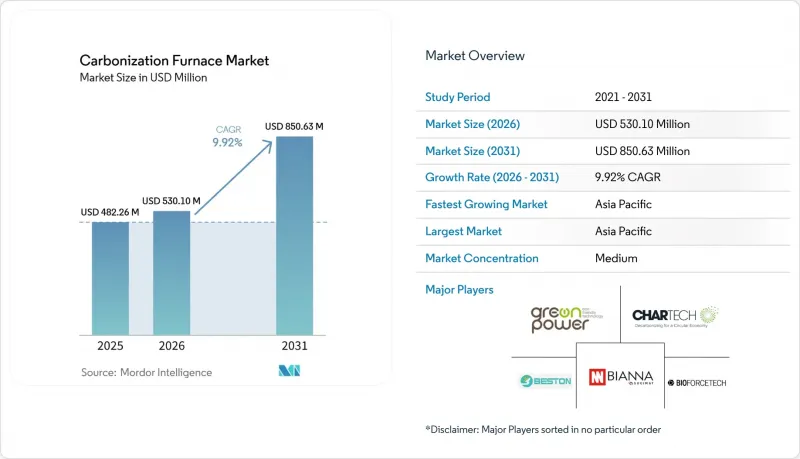

Mordor Intelligence에 의하면, 탄화로 시장 규모는 2025년 4억 8,226만 달러로 평가되었습니다. 2026년에는 5억 3,010만 달러로 확대되어 2026-2031년 CAGR은 9.92%를 나타내, 2031년까지 8억 5,063만 달러에 이를 것으로 예측됩니다.

본 보고서는 로의 유형(연속 탄화로, 배치식 탄화로), 원료(목재, 코코넛 껍질, 톱밥, 벼 껍질, 기타), 용도(공업용, 농업용, 에너지 생산용, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 탄화로 시장 동향 및 인사이트

야금·시멘트 산업에서의 산업용 목탄 사용 증가

2024년, 고로 및 시멘트 가마 운영 사업자들은 약 12억 톤의 석탄을 소비했습니다. 시범 프로그램에서는 이 석탄 투입량의 10%를 바이오 코크스로 대체하는 노력이 시작되어, CO2 배출량을 20% 감축하는 데 성공했습니다. 2025년에는 Carbon Re 등의 인공지능(AI) 제어 플랫폼을 통해 가마의 연료 사용량이 5% 감소했습니다. 이에 따라 연속식 로에서 공급되는 휘발성이 낮고 입자 크기가 균일한 바이오차에 대한 수요가 지속적으로 증가하고 있습니다. 중국이 제시한 바이오매스 혼소 10기가와트(GW) 목표는 연간 목탄 수요를 300만 톤 증가시킬 가능성이 있으며, 이 분야가 연속식 설비에 의존하고 있음을 여실히 보여주고 있습니다.

바이오매스 에너지 프로젝트에 대한 정부의 인센티브

인도의 신·재생에너지부(MNRE)는 바이오매스 프로젝트 자본 비용의 최대 40%를 보조하고 있으며, 이를 통해 중형 보일러의 투자 회수 기간을 5년 미만으로 단축하고 있습니다. 2026년 2월, Varhad Capital사는 이 제도에 따라 연간 3,000톤의 처리 능력을 갖춘 공장을 가동했습니다. 2024년, 중국은 바이오매스 프로젝트에 20억 위안(약 2억 8,000만 달러) 상당의 보조금을 배정했습니다. 미국 농무부(USDA)의 ‘미국 농촌 에너지 프로그램(REAP)’은 2025년에 1억 4,500만 달러를 지출했습니다. 또한, 인증된 바이오숯에 대한 프리미엄 가격 책정은 일본의 J-Credit 및 한국의 비료 기준에 의해 뒷받침되고 있으며, 아시아 전역에서 규제 측면에서 긍정적인 요인으로 작용하고 있습니다.

엄격한 배출 규제 및 허가 요건

미국 환경보호청(EPA)의 40 CFR 63 Subpart M에 따르면, 각 보일러에 연속 배출 모니터링 장치를 설치해야 하며, 그 비용은 5만-15만 달러에 달할 전망입니다. 이 요건은 소규모 배치식 사업자에게 재정적 부담이 될 가능성이 있습니다. 또한, 2026년 1월에 발효되는 국제 해상 위험물 규정(IMDG) 개정안 42-24에 따르면, 바이오숯은 제4.2류 위험물로 분류되어 있습니다. 이러한 분류에 따라 14일간의 풍화 기간이나 불활성 가스를 이용한 퍼지 등의 조치가 도입됨에 따라, 컨테이너 비용이 최대 30% 증가할 가능성이 있습니다.

부문별 분석

2025년에는 연속식 장치가 매출의 60.12%를 차지하며, 연평균 성장률(CAGR) 10.34%로 성장했습니다. 이러한 효율성 덕분에 연간 8,000시간 이상 가동할 수 있으며, 톤당 비용을 최대 40% 절감할 수 있습니다. 이 부문은 2025년 탄화로 시장에 2억 9,000만 달러를 기여했습니다. PyroGreen사의 스크류 컨베이어 설계는 합성가스 재활용을 통해 85-90%의 에너지 자급률을 실현하고 있습니다. 정저우 구천사의 프로그래머블 로직 컨트롤러(PLC) 제어 라인은 생산성을 향상시켜, 단 한 명의 작업자로 5배의 생산량을 달성할 수 있게 해줍니다.

배치식 가마는 원료의 균일성이 떨어지거나 설비 투자 요건이 낮은 시장에서 여전히 중요한 역할을 하고 있습니다. 2만 달러부터 시작하는 이 가격대의 보급형 모델은 Verra의 VM0044 조사 기법에 따라 농산물을 수익화하려는 소규모 생산자들의 관심을 끌고 있습니다. 그러나 미국 각 주에서 이산화탄소(CO) 배출 상한선이 강화됨에 따라, 점화 시 배출량이 급증하는 것을 방지하기 위해 구매자들은 연속식 시스템으로 전환하고 있습니다. 2026년 2분기에 연간 5,000톤(t/y)으로 생산량을 늘린 CHAR Technologies의 Thorold 공장은 이러한 추세를 여실히 보여주고 있습니다. 목재 폐기물 선별 기능을 통합한 연속 오거 리액터를 채택하여, 연속 시스템의 장점을 극대화하는 엔드투엔드 통합의 이점을 부각시키고 있습니다.

지역별 분석

2025년 매출의 46.11%를 차지한 아시아태평양은 2031년까지 연평균 성장률(CAGR) 10.37%를 나타낼 것으로 전망됩니다. 이러한 성장은 인도의 바이오매스 혼소 의무화(7%)와 중국의 10기가와트(GW) 규모 개조 계획에 힘입은 것입니다. 설비 투자 측면에서는 BiocharIND사가 하루 100톤(t/d)의 처리 능력을 갖춘 5기의 설비에 15억 루피(1,000만 달러)를 투자할 계획이며, Varhad Capital사가 마하라슈트라주에서 새로 가동한 연간 3,000톤(t/y) 규모의 플랜트 등이 있습니다. 또한, 일본의 J-Credit 프리미엄과 한국의 비료 기준 역시 해당 지역 전체 수요를 견인하고 있습니다.

북미에서는 산불 대책이 진전되고 있습니다. CharBoss사의 이동식 장비는 시간당 1톤(t/h)의 속도로 벌채 잔재물을 처리하여 탄소 크레딧을 창출하고, 미세먼지(PM)의 기준 초과량을 줄이고 있습니다. CHAR Technologies사는 에스파뇰라에서 연간 5만 톤(t/y) 규모의 프로젝트에 대해 BMI로부터 1,000만 캐나다 달러(716만 달러)의 투자를 확보했습니다. Kanadevia Inova사는 연간 7만 5,000톤의 유기물을 8,000톤의 바이오숯 및 재생 가능 천연가스(RNG)로 전환할 계획이며, 2027년에 가동을 시작할 예정입니다.

유럽에서는 기업의 보고서에 바이오숯을 반영하는 ‘탄소 제거 인증 체계’가 발전하고 있습니다. 이 정책으로 인해 2028년까지 수요가 3배로 증가할 것으로 예측됩니다. Carbonfuture는 2025년에 250만 톤의 탄소 배출권 거래를 중개함으로써, 소규모 소성로에 있어 장기적인 임베디드 계약을 수익원으로 전환했습니다. 북유럽의 지역 난방 시범 사업에서는 합성 가스를 열전병급(CHP) 네트워크에 통합하여 한랭 지역의 경제적 안정성을 높이고 있습니다.

남미에서는 브라질의 사탕수수 바가스에 주력하고 있습니다. 톤당 150달러를 넘는 탄소 크레딧 덕분에 상파울루주와 미나스제라이스주에서는 연간 1만-2만 톤의 처리 능력을 갖춘 바이오숯 플랜트 개발이 진행되고 있습니다. 중동 및 아프리카에서는 아직 초기 단계이지만, 사우디아라비아의 ‘비전 2030’에서는 다각화 계획의 일환으로 바이오매스 에너지가 중시되고 있으며, 남아프리카공화국에서는 황폐화된 옥수수 재배 토양을 개선하기 위한 바이오숯의 활용이 검토되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the carbonization furnace market size is expected to grow from USD 482.26 million in 2025 to USD 530.10 million in 2026 and is forecast to reach USD 850.63 million by 2031 at 9.92% CAGR over 2026-2031.

This report is Segmented by Furnace Type (Continuous Carbonization Furnace, Batch Carbonization Furnace), Feedstock (Wood, Coconut Shell, Sawdust, Rice Husk, Others), Application (Industrial, Agricultural, Energy Production, Others), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Carbonization Furnace Market Trends and Insights

Rising Industrial Charcoal Use in Metallurgy and Cement

In 2024, operators of blast furnaces and cement kilns consumed approximately 1.2 billion tons of coal. Pilot programs have started replacing 10% of this coal charge with bio-coke, achieving a 20% reduction in CO2 emissions. In 2025, artificial intelligence (AI) control platforms such as Carbon Re reduced kiln fuel usage by 5%. This has driven consistent demand for biochar with low volatility and uniform size, supplied by continuous furnaces. China's target of 10 gigawatts (GW) for biomass co-firing could increase annual charcoal demand by 3 million tons, highlighting the sector's reliance on continuous equipment.

Government Incentives for Biomass-to-Energy Projects

India's Ministry of New and Renewable Energy (MNRE) subsidizes up to 40% of capital costs for biomass projects, reducing the payback period for mid-scale furnaces to under five years. In February 2026, Varhad Capital commissioned a unit with a capacity of 3,000 tons per year under this scheme. In 2024, China allocated grants worth CNY 2 billion(approximately USD 280 million) for biomass projects. The United States Department of Agriculture's (USDA) Rural Energy for America Program (REAP) disbursed USD 145 million in 2025. Additionally, premium pricing for certified biochar is supported by Japan's J-Credit and South Korea's fertilizer standards, creating regulatory momentum across Asia.

Stringent Emission-Control and Permitting Requirements

U.S. Environmental Protection Agency's (EPA) 40 CFR 63 Subpart M requires each furnace to be equipped with continuous emissions monitoring hardware, with costs ranging from USD 50,000 to 150,000. This requirement can be financially challenging for smaller batch operators. Additionally, the International Maritime Dangerous Goods (IMDG) Amendment 42-24, effective January 2026, classifies biochar as a Class 4.2 dangerous good. This classification introduces measures such as a 14-day weathering period and inert-gas purging, potentially increasing container costs by up to 30%.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Voluntary Carbon-Credit Markets

- Deployment of Mobile Carbonization Units for Wildfire Mitigation

- Limited Skilled Workforce for AI-Driven Continuous Furnaces

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, continuous units accounted for 60.12% of the revenue and are projected to grow at a 10.34% compound annual growth rate (CAGR). Their efficiency enables operation for over 8,000 hours annually, reducing per-ton costs by up to 40%. This segment contributed USD 290 million to the carbonization furnace market in 2025. PyroGreen's screw-conveyor design achieves 85-90% energy self-sufficiency by recycling syngas. Zhengzhou Jiutian's programmable logic controller (PLC)-controlled line enhances productivity, allowing a single operator to achieve five times the output.

Batch kilns remain significant for heterogeneous feedstocks and markets with lower capital requirements. Entry-level units, priced from USD 20,000, attract small growers monetizing their produce under Verra's VM0044 methodology. However, tighter carbon dioxide (CO) caps in U.S. states are driving buyers toward continuous systems to avoid ignition spikes. CHAR Technologies' Thorold plant, set to scale up to 5,000 tons per year (t/y) in Q2 2026, demonstrates this trend. Using a continuous auger reactor integrated with wood-waste sorting, it highlights the benefits of end-to-end integration in favoring continuous systems.

Geography Analysis

Asia-Pacific, accounting for 46.11% of 2025 revenue, is projected to grow at a 10.37% compound annual growth rate (CAGR) until 2031. This growth is supported by India's 7% biomass co-firing mandate and China's 10 gigawatt (GW) retrofit initiative. Capital investments include BiocharIND's commitment of INR 1.5 billion (USD 0.01 billion) toward five 100 tons per day (t/d) units and Varhad Capital's newly operational 3,000 tons per year (t/y) plant in Maharashtra. Additionally, Japan's J-Credit premium and Korea's fertilizer standards are driving demand across the region.

In North America, wildfire mitigation strategies are advancing. CharBoss's mobile units process slash at a rate of 1 ton per hour (t/h), generating carbon credits and reducing particulate matter (PM) exceedances. CHAR Technologies secured a CAD 10 million (USD 7.16 million) investment from BMI for a 50,000 t/y project in Espanola. Kanadevia Inova plans to convert 75,000 t/y of organic material into 8,000 tons of biochar and renewable natural gas (RNG), with operations starting in 2027.

Europe is progressing with its Carbon Removal Certification Framework, which incorporates biochar into corporate reporting. This policy is expected to triple demand by 2028. Carbonfuture facilitated the brokering of 2.5 million tons of credits in 2025, turning long-term offtakes into revenue streams for smaller furnaces. Nordic district-heating pilots are integrating syngas into combined heat and power (CHP) networks, enhancing economic stability in colder climates.

South America is focusing on Brazil's sugarcane bagasse. Carbon credits exceeding USD 150 per ton are encouraging the development of char plants with capacities of 10,000-20,000 t/y in Sao Paulo and Minas Gerais. The Middle East and Africa are in early stages, with Saudi Arabia's Vision 2030 emphasizing biomass energy in its diversification plans and South Africa evaluating biochar for improving degraded maize soils.

- Beston Group Co., Ltd.

- Bioforcetech Corporation

- CHAR Technologies Ltd.

- Gomine Industrial Technology Co.,Ltd

- Gongyi Lantian Mechanical Plant

- GreenPower

- Gunung Raja Paksi Biochar Furnaces

- Henan Honest Heavy Machinery Co. Ltd.

- Henan Lvkun Environmental Protection Technology Co.,Ltd

- Henan Olten Environmental Sci-Tech Co. Ltd.

- HENAN SINOVO MACHINERY ENGINEERING CO.,LTD

- MaxTon Industrial Co., Ltd.

- NextChar

- Sugimat S.L.

- Zhengzhou Protech Technology Co., Ltd

- Zhengzhou Shuliy Machinery Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising industrial charcoal use in metallurgy and cement

- 4.2.2 Government incentives for biomass-to-energy projects

- 4.2.3 Expansion of voluntary carbon-credit markets

- 4.2.4 Deployment of mobile carbonization units for wildfire mitigation

- 4.2.5 Integration with carbon-negative hydrogen hubs

- 4.3 Market Restraints

- 4.3.1 Stringent emission-control and permitting requirements

- 4.3.2 Limited skilled workforce for AI-driven continuous furnaces

- 4.3.3 Fragmented international shipping rules for biochar classification

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Furnace Type

- 5.1.1 Continuous Carbonization Furnace

- 5.1.2 Batch Carbonization Furnace

- 5.2 By Feedstock

- 5.2.1 Wood

- 5.2.2 Coconut Shell

- 5.2.3 Sawdust

- 5.2.4 Rice Husk

- 5.2.5 Others (Bamboo, Palm Shells)

- 5.3 By Application

- 5.3.1 Industrial (Metallurgy, Cement)

- 5.3.2 Agricultural (Soil Improvement, Biochar)

- 5.3.3 Energy Production

- 5.3.4 Others (Waste Management, Incense)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Beston Group Co., Ltd.

- 6.4.2 Bioforcetech Corporation

- 6.4.3 CHAR Technologies Ltd.

- 6.4.4 Gomine Industrial Technology Co.,Ltd

- 6.4.5 Gongyi Lantian Mechanical Plant

- 6.4.6 GreenPower

- 6.4.7 Gunung Raja Paksi Biochar Furnaces

- 6.4.8 Henan Honest Heavy Machinery Co. Ltd.

- 6.4.9 Henan Lvkun Environmental Protection Technology Co.,Ltd

- 6.4.10 Henan Olten Environmental Sci-Tech Co. Ltd.

- 6.4.11 HENAN SINOVO MACHINERY ENGINEERING CO.,LTD

- 6.4.12 MaxTon Industrial Co., Ltd.

- 6.4.13 NextChar

- 6.4.14 Sugimat S.L.

- 6.4.15 Zhengzhou Protech Technology Co., Ltd

- 6.4.16 Zhengzhou Shuliy Machinery Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment