|

시장보고서

상품코드

2062182

티오글리콜산 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Thioglycolic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

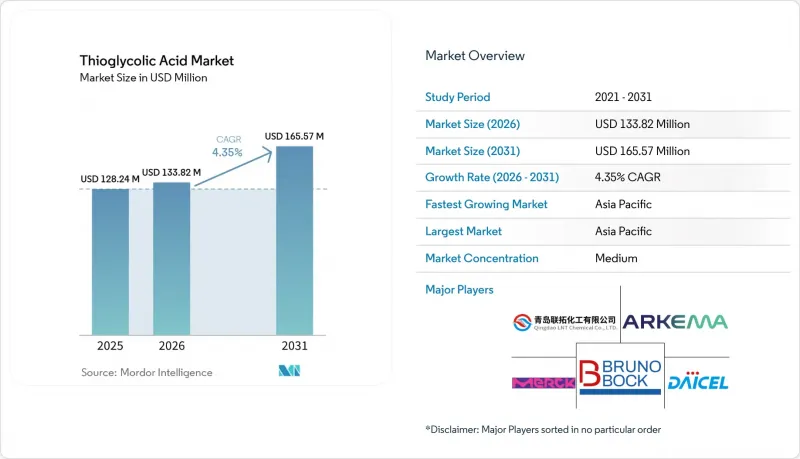

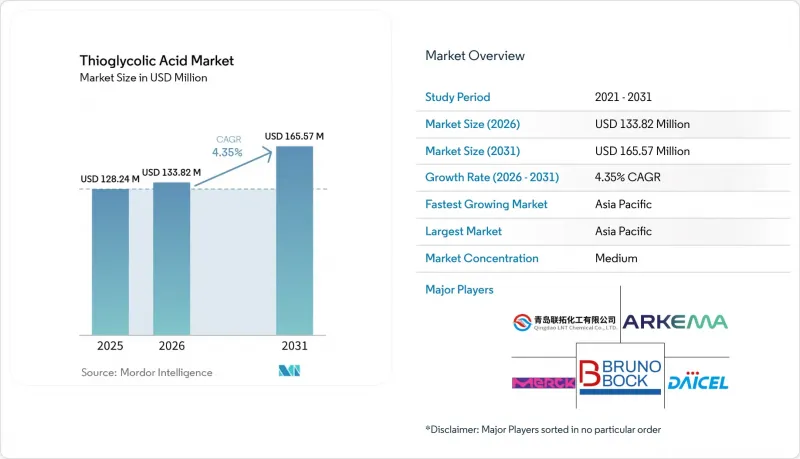

Mordor Intelligence에 의하면, 티오글리콜산 시장 규모는 2025년 1억 2,824만 달러에서 2026년에는 1억 3,382만 달러로 확대되어 2031년까지 1억 6,557만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 4.35%로 성장할 전망입니다.

본 보고서는 등급(기술 등급 및 고순도 등급), 용도(헤어케어·화장품, 석유 및 가스 산업, 가죽 가공, 섬유 산업, 화학 중간체, 기타) 및 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 티오글리콜산 시장 동향 및 분석

석유 및 가스 우물 산 처리에서 부식 방지제로서의 사용 확대

티오글리콜산(TGA)은 환원제 및 킬레이트 배위체라는 이중 역할을 수행합니다. 특히, 탄산염 저류층의 매트릭스 산 처리 시 철의 제어에 효과적입니다. 이러한 저류층에서는 수산화철의 침전으로 인해 유정 주변의 투수성이 저하되어, 자극 처리의 효과가 떨어질 가능성이 있습니다. TGA는 저농도에서도 효율적으로 작용하여 Fe³?를 보다 안정된 킬레이트화된 Fe²? 형태로 변환합니다. 구연산, EDTA, NTA와 같은 기존의 킬레이트제나 에리소르빈산, 아스코르브산과 같은 환원제와는 달리, TGA는 고온이나 산성 pH 조건에서도 안정성을 유지합니다. 또한, TGA의 티올기는 고온에서 연강 표면에 보호막 역할을 하는 Fe-S 막을 형성합니다. 이 막은 고농도 염수나 고농도 H₂S 환경에서 발생하는 부식을 억제합니다. 이러한 조건들은 심해나 비전통 유정에서 흔히 접하게 되는 조건입니다. TGA를 포함한 작은 황 함유 분자는 Fe-S 결합을 통해 결합합니다. 텅스텐산염이나 티오우레아 등의 강화제와 조합함으로써 부식 속도를 대폭 낮출 수 있습니다. 업계가 초고온 유정(150℃ 이상) 및 셰일층의 장거리 수평 시추로 전환됨에 따라, 열적으로 안정적이고 저용량의 부식 억제제에 대한 수요가 증가하고 있습니다. 이러한 억제제는 지층에 미치는 손상을 최소화할 뿐만 아니라, 화학 약품의 물류 비용도 절감합니다.

PVC 열안정제 및 기타 중간체로서의 소비 확대

유기 주석 티오글리콜산 에스테르는 특히 식품 접촉용 포장재나 음용수 배관용 PVC 배합에서 열안정제로 사용되고 있습니다. 낮은 독성과 이온 이동량의 최소화를 중시하는 엄격한 규제 기준을 바탕으로, 이러한 에스테르는 PVC 수돗물 배관, 펌프 및 식품 가공 장비에 사용이 승인되어 투명성과 열안정성을 모두 향상시키고 있습니다. 규제 강화로 인해 전 세계적으로 납 및 카드뮴계 안정제에서 벗어나는 추세가 가속화되면서, 칼슘·아연계 및 유기주석계 대체재 시장이 확대되고 있습니다. 그러나 주로 비용이나 통합의 장벽으로 인해 여전히 과제가 남아 있습니다. 칼슘계 PVC 안정제의 생산 능력 확대는 액체형에서 고체형 안정제 시스템으로의 전환을 촉진하는 규제 동향을 여실히 보여주고 있습니다. PVC 외에도, TGA는 아크릴산 및 아크릴레이트 계열의 에멀션 중합에서 사슬 전이제로 활용되고 있습니다. 이러한 완벽한 수분 산화성과 친핵성 덕분에 수성 환경에서 분자량을 정밀하게 조절할 수 있습니다. TGA는 폴리머 첨가제 시장에서 틈새 시장이지만 중요한 위치를 차지하고 있으며, 하류 PVC 및 아크릴 수지 제조업체와 지리적으로 인접해 있다는 이점 덕분에 아시아태평양이 생산 능력 면에서 주도적인 입지를 차지하고 있습니다.

TGA 농도에 대한 엄격한 소비자 안전 기준

유럽연합(EU)의 화장품 규정에 대한 최근 개정으로 인해, 화장품 내 TGA 및 그 염류에 대해 엄격한 제한이 부과되고 있습니다. 해당 규정에서는 헤어 펌 및 스트레이트 펌용 제품에 대해, 제품의 pH 값에 따라 일반 소비자용과 전문가용의 최대 농도를 달리 정하고 있습니다. 제모제나 씻어내는 유형의 헤어 케어 제품에 대해서도 명확한 농도 상한선이 설정되어 있습니다. 또한, 눈에 자극을 줄 우려가 있어 속눈썹 펌용 제품은 전문가 전용으로 제한되어 있으며, 일반 소비자는 구입할 수 없습니다. “눈에 들어가지 않도록 주의해 주십시오. 만약 눈에 들어간 경우에는 즉시 씻어내십시오. 적절한 장갑을 착용해 주십시오. 티오글리콜산이 함유되어 있습니다. 사용 설명서를 따르십시오. “어린이의 손이 닿지 않는 곳에 보관하십시오”와 같은 표시 경고 등의 규정 준수 요건은 비용을 증가시킬 뿐만 아니라 처방 유연성도 제한합니다. 아세안(ASEAN) 회원국들도 이러한 규제를 반영하고 있어, 주요 소비 시장 전반에 걸쳐 엄격한 규제 환경이 조성되어 있습니다. 일반용 헤어 펌 제품의 경우, TGA와 티올락트산의 합계 농도 상한선이 제제 개발자의 배합 능력을 제한하고 있습니다. 이로 인해 단위당 수익성이 저하되고, 이익률이 높은 전문용 제제가 라이선싱된 유통 경로로 밀려나면서 시장이 세분화되고 있습니다.

부문별 분석

2025년, 테크니컬 그레이드는 매출의 54.11%를 차지하며, PVC 안정제, 유전용 화학제품 및 가죽 제모 처리 분야에서 뛰어난 가격 경쟁력을 보이고 있습니다. 한편, 색상이나 미량 금속이 매우 중요한 의약품 중간체 및 광전자 분야에서 수요에 힘입어, 고순도 등급은 2026년부터 2031년까지의 예측 기간 동안 4.66%라는 견실한 연평균 성장률(CAGR)을 기록했습니다. 인라인 GC/FTIR 기술 및 MCA의 용융 결정화와 같은 혁신적인 기술을 통해 디클로로아세트산염 불순물을 효과적으로 최소화함으로써, 결함이 없는 고순도 제품을 확보하고 있습니다.

수요 동향에서는 양극화 현상이 나타나고 있습니다. 산업용 구매자들은 소량의 디티오글리콜산 잔류물을 용인하는 경향이 있지만, 양자점 제조업체나 비오틴 생산업체들은 수분 함량을 엄격히 0.1% 미만으로, 금속 함량을 1ppm 이하로 억제하기 위해 더 높은 가격을 지불할 의향이 있습니다. ESG(환경·사회·지배구조)를 바탕으로 한 용융결정화 장치의 업그레이드와 ISCC+ 질량균형 인증을 획득한 원료의 도입을 통해, 각 생산사는 티오글리콜산 시장 내 특수 제품의 수익성을 극대화하고 있습니다.

지역별 분석

2025년, 아시아태평양은 매출의 47.79%라는 압도적인 점유율을 차지하고 있으며, 2026년부터 2031년까지의 예측 기간 동안 연평균 성장률(CAGR) 5.07%로 성장할 것으로 전망됩니다. 이 지역의 MCA 공급을 주도하는 중국은 2028년 다야완에서 크래커와 고성능 설비의 가동을 시작함으로써 그 입지를 공고히 하고 있습니다. 이 전략적 움직임은 PVC 안정제 및 양자점 소재에 대한 급증하는 하류 수요를 겨냥하고 있습니다. 동시에, 인도의 피마자유 공급은 바이오 제품을 뒷받침할 뿐만 아니라 티오글리콜산 시장의 경쟁을 심화시키고 있습니다. 일본과 한국의 연구 거점은 TGA로 캡 처리된 CdTe 양자점의 상용화에 성공했으며, 차세대 디스플레이 시장을 목표로 하고 있습니다.

북미에서는 셰일가스 사업자들이 시추공 부식 방지제로 EDTA 대신 TGA를 선택하는 경향이 강해지고 있어, 그 중요성을 보여주고 있습니다. 이러한 변화는 저취성 합성을 권장하는 OSHA의 노출 규정에 크게 기인합니다. 유럽에서는 공급량 증가세가 둔화되고 있지만, 특히 제약 및 전문 미용 분야에서 고순도 등급 제품에 대한 수요가 급증하고 있습니다. REACH 규제로 인해 업계는 용융 결정화 MCA 및 폐쇄형 황 처리 방식으로 전환되고 있으며, 유럽의 플랜트들은 저배출 기술의 최전선에 서 있습니다.

남미, 중동 및 아프리카는 여전히 틈새 시장이지만, 잠재력을 보여주기 시작하고 있습니다. 브라질과 아르헨티나의 광산에서는 비시안화물 침출법 시험이 진행되고 있으며, 사우디아라비아의 고염분 저류층은 TGA를 기반으로 한 산 처리 혼합물의 도입을 위한 길을 열어주고 있습니다. 이 지역들의 향후 성장 전망은 비용 측면에서의 타당성 확인과, 기존의 시안화물 및 티오황산염 공법을 대체할 TGA 공법에 대한 규제 당국의 승인 여부에 달려 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the thioglycolic acid market size is expected to increase from USD 128.24 million in 2025 to USD 133.82 million in 2026 and reach USD 165.57 million by 2031, growing at a CAGR of 4.35% over 2026-2031.

This report is Segmented by Grade (Technical Grade and High Purity Grade), Application (Hair Care and Cosmetic Products, Oil and Gas Industry, Leather Processing, Textile Industry, Chemical Intermediates, and Others), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Thioglycolic Acid Market Trends and Insights

Rising Use as Corrosion Inhibitor in Oil and Gas Well Acidizing

Thioglycolic acid (TGA) serves a dual purpose: as a reducing agent and a chelating ligand. It is particularly effective in controlling iron during the matrix acidizing of carbonate reservoirs. In these reservoirs, ferric hydroxide precipitation can hinder near-wellbore permeability, reducing stimulation effectiveness. TGA operates efficiently at low concentrations, converting Fe3+ to the more stable chelated Fe2+ form. Unlike traditional chelants, such as citric acid, EDTA, and NTA, or reducers like erythorbic and ascorbic acids, TGA remains stable even at high temperatures and acidic pH levels. Additionally, TGA's thiol group forms a protective Fe-S film on mild steel at elevated temperatures. This film inhibits corrosion in concentrated salt solutions and high-H2S environments, conditions often encountered in deepwater and unconventional wells. Small sulfur-containing molecules, including TGA, bond through Fe-S connections. When paired with intensifiers like tungstate or thiourea, they can drastically cut corrosion rates. As the industry pivots to ultra-high-temperature wells (over 150 degrees Celsius) and extended-reach horizontal laterals in shale plays, there is a rising demand for thermally stable, low-dosage inhibitors. These inhibitors not only minimize formation damage but also reduce chemical logistics costs.

Growing Consumption as PVC Heat Stabilizer and Other Intermediates

Organotin thioglycolates are being adopted as thermal stabilizers in PVC formulations, especially for food-contact packaging and potable-water piping. Given the stringent regulatory standards emphasizing low toxicity and minimal migration, these esters have gained approval for use in PVC water pipes, pumps, and food-processing equipment, boosting both transparency and thermal stability. The global move away from lead and cadmium-based stabilizers, due to regulatory crackdowns, has expanded the market for calcium-zinc and organotin alternatives. Yet, challenges persist, primarily due to cost and integration hurdles. The ramp-up of calcium-based PVC stabilizer capacity highlights the regulatory push steering a transition from liquid to solid stabilizer systems. Beyond PVC, TGA finds application as a chain-transfer agent in the emulsion polymerization of acrylic acid and acrylates. Its complete water miscibility and nucleophilic reactivity allow for precise molecular-weight control in aqueous environments. While TGA holds a niche yet crucial position in polymer additives, the Asia-Pacific region leads in production capacity, thanks to its closeness to downstream PVC and acrylic resin manufacturers.

Strict Consumer-Safety Limits on TGA Concentration

Recent amendments to the European Union's Cosmetic Products Regulation impose stringent limits on TGA and its salts in cosmetic products. The regulation sets maximum concentrations for hair-waving or straightening products, varying for general consumers and professionals based on the product's pH. Depilatories and rinse-off hair-care items also face defined concentration caps. Due to potential eye irritation risks, products for eyelash waving are restricted to professional use, making them unavailable to general consumers. Compliance mandates, such as labeling warnings like "Avoid eye contact; rinse immediately if contact occurs; wear suitable gloves; contains thioglycolate; follow instructions; keep out of reach of children," not only increase costs but also limit formulation flexibility. ASEAN member states have mirrored these restrictions, establishing a stringent regulatory landscape across major consumer markets. In general-use hair-waving products, the cap on the combined concentration of TGA and thiolactic acid limits formulators' blending capabilities, reducing revenue potential per unit and pushing higher-margin professional formulations into licensed channels, fragmenting the market.

Other drivers and restraints analyzed in the detailed report include:

- Adoption in Quantum-Dot Passivation for Opto-Electronics

- Emerging Non-Cyanide Gold-Leaching Chemistries Using TGA Ligands

- Feedstock Volatility (Monochloroacetic Acid, H2S)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, the Technical Grade accounted for 54.11% of the revenue, highlighting its pricing edge in PVC stabilizers, oilfield chemicals, and leather dehairing. Meanwhile, the High Purity Grade, driven by demand in pharmaceutical intermediates and optoelectronics, where color and trace metals are critical, experienced a robust CAGR of 4.66% during the forecast period of 2026-2031. Innovations such as Inline GC/FTIR techniques and the melt crystallization of MCA have effectively minimized dichloroacetate impurities, ensuring a flawless high-purity output.

Demand dynamics reveal a split. Industrial buyers may tolerate minor dithioglycolic acid residues, but quantum-dot manufacturers and biotin producers are willing to pay a premium for water content strictly below 0.1% and metals limited to 1 ppm. With ESG-driven upgrades in melt crystallizers and the integration of ISCC+ mass-balance feedstocks, producers are capitalizing on specialty margins in the thioglycolic acid market.

Geography Analysis

In 2025, the Asia-Pacific region commanded a dominant 47.79% share of the revenue and is set to expand at a CAGR of 5.07% through the forecast period of 2026-2031. China, a key player in the region's MCA supply, is solidifying its stance with the 2028 commissioning of a cracker and a high-performance unit at Daya Bay. This strategic move targets the burgeoning downstream demand for PVC stabilizers and quantum-dot materials. Concurrently, India's castor supply not only supports bio-based products but also intensifies competition in the thioglycolic acid market. Research hubs in Japan and South Korea are successfully commercializing TGA-capped CdTe QDs, setting their sights on the next-generation display market.

North America asserts its significance, with shale operators increasingly opting for TGA corrosion inhibitors over EDTA for their wells. This shift is largely driven by OSHA's exposure regulations advocating for low-odor synthesis. Europe, despite experiencing slower volume growth, is witnessing a surge in demand for High Purity Grade products, particularly in the pharmaceutical and professional beauty sectors. The REACH initiative is guiding the industry towards melt-crystallized MCA and a closed-loop sulfur handling approach, elevating European plants to the forefront of low-emission technologies.

While South America, the Middle-East and Africa remain niche players, they are beginning to show potential. Mines in Brazil and Argentina are trialing non-cyanide leaching methods, and Saudi Arabia's high-salinity reservoirs are paving the way for TGA-based acidizing blends. The future growth trajectory in these regions hinges on cost validations and the regulatory acceptance of TGA over conventional cyanide or thiosulfate methods.

- Anoky Co.,Ltd. No

- Arkema

- Biosynthetic Technologies

- BRUNO BOCK

- Daicel Corporation

- Discovery Fine Chemicals

- Hunan ke sheng new materials co., LTD

- Jinan Qinmu Fine Chemical

- Merck KGaA

- Nouryon

- Osaka Sasaki Chemical Co. Ltd

- Qingdao LNT Chemical Co., Ltd

- Quingdao Ruchang Mining Industry Co., LTD

- SASAKICHEMICAL CO.,LTD

- Shandong Xinhua Pharma

- Tokyo Chemical Industry (India) Pvt. Ltd.

- Wuhan Grand Hoyo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising use as corrosion inhibitor in oil and gas well acidizing

- 4.2.2 Growing consumption as PVC heat-stabilizer and other intermediates

- 4.2.3 Adoption in quantum-dot passivation for opto-electronics

- 4.2.4 Emerging non-cyanide gold-leaching chemistries using TGA ligands

- 4.2.5 Low-odor, low-H2S syntheses boosting EHS compliance and plant uptime

- 4.3 Market Restraints

- 4.3.1 Strict Consumer-Safety Limits on TGA Concentration

- 4.3.2 Feedstock Volatility (Monochloroacetic Acid, H2S)

- 4.3.3 Bio-Based Reductants Replacing TGA in Premium Cosmetics

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Technical Grade

- 5.1.2 High Purity Grade

- 5.2 By Application

- 5.2.1 Hair Care and Cosmetic Products

- 5.2.2 Oil and Gas Industry

- 5.2.3 Leather Processing

- 5.2.4 Textile Industry

- 5.2.5 Chemical Intermediates

- 5.2.6 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Anoky Co.,Ltd. No

- 6.4.2 Arkema

- 6.4.3 Biosynthetic Technologies

- 6.4.4 BRUNO BOCK

- 6.4.5 Daicel Corporation

- 6.4.6 Discovery Fine Chemicals

- 6.4.7 Hunan ke sheng new materials co., LTD

- 6.4.8 Jinan Qinmu Fine Chemical

- 6.4.9 Merck KGaA

- 6.4.10 Nouryon

- 6.4.11 Osaka Sasaki Chemical Co. Ltd

- 6.4.12 Qingdao LNT Chemical Co., Ltd

- 6.4.13 Quingdao Ruchang Mining Industry Co., LTD

- 6.4.14 SASAKICHEMICAL CO.,LTD

- 6.4.15 Shandong Xinhua Pharma

- 6.4.16 Tokyo Chemical Industry (India) Pvt. Ltd.

- 6.4.17 Wuhan Grand Hoyo

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment