|

시장보고서

상품코드

2062199

케이블 어셈블리 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Cable Assembly - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

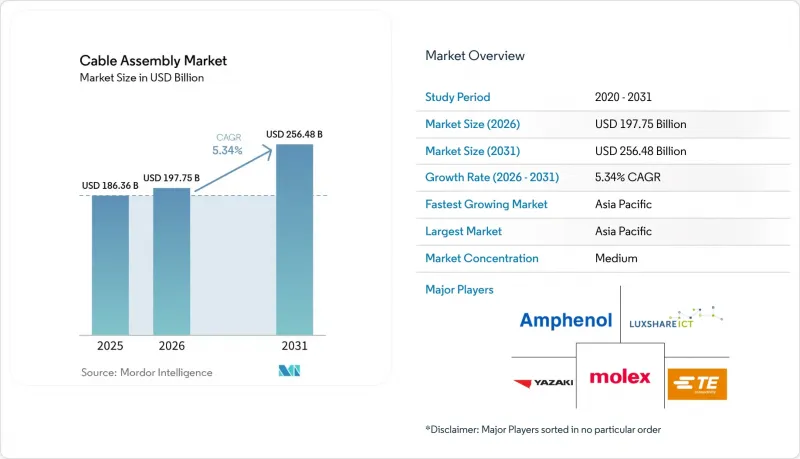

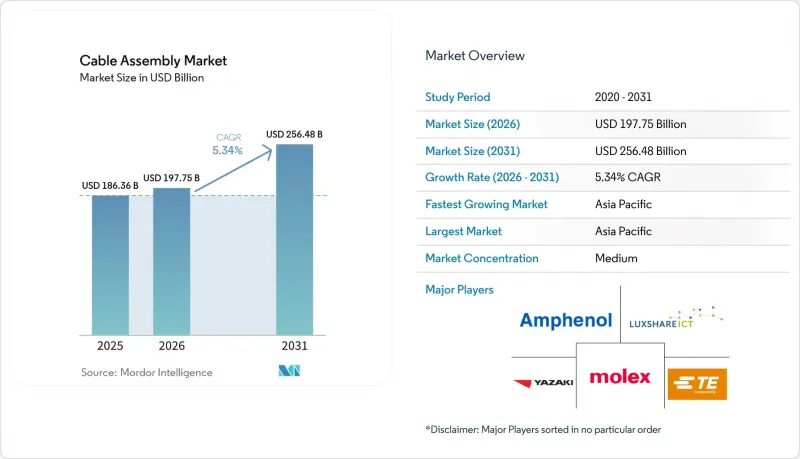

Mordor Intelligence에 의하면, 케이블 어셈블리 시장 규모는 2025년에 1,863억 6,000만 달러로 평가되었습니다. 2026년에 1,977억 5,000만 달러에서 2031년까지 2,564억 8,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 5.34%를 나타낼 전망입니다.

본 보고서는 제품 유형(맞춤형 케이블 어셈블리, 표준/기성품 어셈블리, 오버몰드 케이블 어셈블리, 광섬유 어셈블리 등), 케이블 유형(동축 케이블 등), 최종 이용 산업(자동차 및 운송, 전기통신 등), 용도(데이터 전송·통신 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 케이블 어셈블리 시장 동향 및 인사이트

고속 데이터센터 상호 연결 수요 급증

하이퍼스케일 사업자들은 400 Gbps에서 800 Gbps 및 1.6 Tbps 광 모듈로 전환하고 있으며, 이에 따라 교체 주기가 약 2년으로 단축되면서 다년 공급 계약에 따른 광섬유 구매량이 증가하고 있습니다. 액티브 광케이블은 직접 어태치 구리 케이블보다 포트 전력 소비량이 약 절반 수준입니다. 이러한 차이로 인해, 서버 1대당 10kW를 소비하는 고밀도 GPU 랙에서 광케이블이 유리합니다. 1교대당 1만 개 이상의 단자를 인증할 수 있는 자동 연마 라인은 여전히 부족하여, 이로 인해 대규모 사업자들은 실행 면에서 우위를 점하고 있습니다. 2026년 초 IEEE 802.3가 1.6 Tbps 이더넷을 승인함에 따라, 이미 도입된 200G 및 400G 장비의 교체가 가속화되어 예측 기간 동안 광섬유 어셈블리의 두 자릿수 성장이 지속될 전망입니다.

5G 및 FTTH(Fiber-To-The-Home) 구축 확대

2025년, 미국의 FTTH(Fiber-To-The-Home) 구축 규모는 1,180만 가구 이상 증가했으며, 설치 업체들이 융착 접속 방식에서 푸시온 커넥터 방식으로 전환함에 따라 가구당 1.2-1.5개의 드롭 케이블 어셈블리가 소비되었습니다. 사전 조립형 하네스는 1개당 최대 35% 더 비싸지만, 현장 작업량을 약 3분의 1로 줄일 수 있으므로, 현장 작업비가 시간당 75달러를 초과하는 시장에서는 매력적인 절충안이 됩니다. 5G 미드밴드의 밀도 향상이 병행되면서, 원격 무선 헤드(RRH)용 직류 전원을 통합한 하이브리드 구리·광섬유 피더 케이블에 대한 수요가 증가하고 있습니다. 한편, 농촌 지역의 고정 무선망 구축에서는 굴착이 어려운 지형에서 NEMA 4X 규격을 준수하는 백홀 어셈블리가 선호되고 있습니다.

구리 및 특수 금속 가격 변동

런던 금속 거래소(LME)의 구리 선물 가격은 2025년 초부터 2026년 중반까지 63% 상승하여, 조립 제조업체의 원자재 비용을 약 5분의 1 가량 끌어올렸습니다. 자동차 업계의 계약에는 지수 연동형 조정 조항이 포함되어 있지만, 60-90일의 시차로 인해 가격이 급등할 경우 매출총이익률이 최대 400베이시스포인트까지 축소되는 상황이 발생하고 있습니다. 린청동이나 베릴륨동과 관련해 헤지나 수량 할인 제도를 갖추지 못한 중소 지역 조립업체들은 할증 요금을 부과하거나, Kg당 60-70%의 원가 절감이 기대되는 알루미늄 도체로 전환하고 있으며, 이로 인해 전도율은 40% 저하됩니다. 평균 80-100kg의 구리를 사용하는 전기차용 배선 하네스의 경우, 구리 가격이 톤당 1만 달러로 안정될 때 배선 비용이 최대 1,000달러 증가하게 되며, 자동차 제조업체가 이를 전액 부담하기에는 어려운 상황입니다.

부문별 분석

광섬유 어셈블리는 2025년 매출의 36.54%를 차지했으며, 하이퍼스케일 캠퍼스가 800Gbps 광통신으로 전환됨에 따라 기존 구리 제품을 능가하는 연평균 성장률(CAGR) 6.06%로 확대될 것으로 전망됩니다. 광섬유 제품의 케이블 어셈블리 시장 규모는 메타(Meta)가 코닝(Corning)사와 체결한 수십억 달러 규모의 계약 덕분에 성장하고 있습니다. 이 계약은 생산 능력을 사전에 확보하기 위한 것으로, 장기적인 수요에 대한 확신을 보여줍니다. 매출의 약 28-30%를 차지하는 맞춤형 케이블 어셈블리는 자동차, 항공우주, 의료 분야의 프로젝트를 뒷받침하고 있으며, 적시 공급 방식의 키트화를 통해 OEM 제조업체의 현장 재고가 감소하고 있습니다.

일반적인 기성품 조립품은 여전히 가격에 민감한 편이며, 중국의 하청업체들이 기본형 USB-C 케이블을 개당 2달러 미만으로 생산하고 있기 때문에 소매 브랜드의 틈새 시장을 제외하면 이익률이 압박받고 있습니다. 오버몰드 설계 및 고주파 조립은 방진·방수 성능과 삽입 손실을 저렴한 비용으로 보장하기 어렵기 때문에 매출총이익률을 30% 수준으로 유지하고 있습니다. 리본 케이블이나 플랫 케이블은 초슬림형 소비자 가전제품에 널리 사용되고 있지만, 신호층과 전원층을 적층한 플렉서블 인쇄회로기판으로 부분적으로 대체되는 추세가 확산되고 있습니다.

광섬유 케이블은 2025년 매출의 37.72%를 차지했으며, 삽입 손실이 0.3dB 미만인 단일 모드 사양이 스파인-리프 아키텍처에서 표준화됨에 따라 연평균 성장률(CAGR) 6.11%로 시장을 계속 주도할 전망입니다. 케이블 어셈블리 시장 규모의 약 5분의 1을 차지하는 동축 케이블은 5G 설치 업체들이 저손실 파형 케이블을 선호함에 따라 성장 속도가 둔화되고 있지만, 100미터를 초과하는 안테나 피더에는 여전히 필수적입니다.

전력 케이블은 800V 차량 아키텍처를 배경으로 성장세가 가속화되고 있으며, 절연 정격 및 전류 허용치의 상승에 따라 케이블 어셈블리 시장 내 점유율을 한 자릿수 중반까지 끌어올리고 있습니다. RF 및 마이크로파 케이블 시장은 전자전 시스템의 업그레이드에 힘입어, 고주파 레이더에 중점을 둔 국방 예산 덕분에 한 자릿수 중반대의 성장세를 유지하고 있습니다. Cat6A 및 Cat7 트위스트 페어 케이블은 기업 캠퍼스 내의 교체 수요를 주도하고 있지만, 상품화 현상으로 인해 성장률은 한 자릿수 초반으로 둔화되고 있습니다.

지역별 분석

아시아태평양은 2025년 전 세계 매출의 42.12%를 차지했으며, TE Connectivity, Hirose Electric, Luxshare가 필리핀, 인도, 중국 본토에 새로운 자본을 투자함에 따라 연평균 성장률(CAGR) 5.78%를 나타낼 전망입니다. 일본과 한국은 국내 클라우드 시장 확대에 대응하기 위해 광섬유 용량에 대한 투자를 추진하고 있는 반면, 베트남은 각 브랜드가 중국 이외의 조달처를 다각화하는 가운데, 소비자용 전자기기 수주 계약을 따내고 있습니다.

북미 시장 점유율은 약 29%이며, 넥산즈의 일렉트로 케이블즈 인수와 주요 인프라 공급망을 대상으로 한 여러 주의 우대 조치에 힘입어 리쇼어링 추세가 가속화되고 있습니다. 멕시코는 미국 조립 공장에 공급하는 하네스의 니어쇼어링 거점으로 부상하며, 미국의 높은 인건비를 상쇄하고 있습니다.

유럽은 매출의 약 5분의 1을 차지하고 있습니다. RoHS 및 REACH 규정에 따른 준수 부담이 중소 제조업체들에게 무겁게 짓누르고 있지만, AI 데이터센터용 광섬유나 800V 차량용 하네스와 같은 프리미엄 틈새 시장은 호황을 누리고 있습니다. 중동 및 아프리카 및 남미의 비중은 합쳐서 10% 미만에 그치고 있지만, 해저 케이블, 교통수단의 전기화, 지역 데이터센터 확장을 위한 수주는 견조한 추세를 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the cable assembly market size is projected to be USD 186.36 billion in 2025, USD 197.75 billion in 2026, and reach USD 256.48 billion by 2031, growing at a CAGR of 5.34% from 2026 to 2031.

This report is Segmented by Product Type (Custom Cable Assemblies, Standard/Off-the-Shelf Assemblies, Overmolded Cable Assemblies, Fiber-Optic Assemblies, and More), Cable Type (Coaxial, and More), End-Use Industry (Automotive and Transportation, Telecommunications, and More), Application (Data Transfer and Communication, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cable Assembly Market Trends and Insights

Surge In High-Speed Data-Center Interconnect Demand

Hyperscale operators are migrating from 400 Gbps to 800 Gbps and 1.6 Tbps optics, compressing refresh cycles to roughly two years and lifting fiber purchases under multi-year supply agreements. Active optical cables dissipate roughly half the port power of direct-attach copper, a difference that favors them in dense GPU racks where a single server can draw 10 kilowatts. Automated polishing lines that certify more than 10,000 termini per shift remain scarce, giving scale players an execution edge. IEEE 802.3's ratification of 1.6 Tbps Ethernet in early 2026 will accelerate replacement of installed 200 G and 400 G inventories, sustaining double-digit fiber-assembly growth well into the forecast window.

Expansion Of 5 G And Fiber-To-The-Home Deployments

United States FTTH construction passed 11.8 million additional premises during 2025, absorbing 1.2-1.5 drop-cable assemblies per home as installers pivot from fusion splicing to push-on connectors. Pre-terminated harnesses cost up to 35% more per unit yet cut truck-roll labor by around one-third, an attractive trade-off in markets where field labor exceeds USD 75 per hour. Parallel 5 G mid-band densification boosts demand for hybrid copper-fiber feeder cables that integrate DC power for remote radio heads, while rural fixed-wireless rollouts favor NEMA 4X-rated backhaul assemblies in difficult trench terrain.

Volatility In Copper and Specialty Metal Prices

London Metal Exchange copper futures climbed 63% from early 2025 to mid-2026, inflating the raw-material cost of goods by roughly one-fifth for assembly houses. Automotive contracts offer indexed adjustments, yet 60-90-day lags compress gross margin by as much as 400 basis points during rapid spikes. Smaller regional assemblers, lacking hedging or volume rebates on phosphor bronze and beryllium copper, apply surcharges or shift toward aluminum conductors that save 60-70% per kilogram but sacrifice 40% conductivity. Electric-vehicle harnesses averaging 80-100 kg of copper would incur up to USD 1,000 in extra wiring cost at a steady USD 10,000 per metric-ton price, a figure automakers struggle to absorb in full.

Other drivers and restraints analyzed in the detailed report include:

- Electrification And ADAS-Driven Automotive Wiring Complexity

- Industrial Automation and Smart-Factory Rollouts

- Stringent RoHS/REACH And Halogen-Free Material Mandates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fiber-optic assemblies held 36.54% of 2025 revenue and are projected to expand at a 6.06% CAGR, outpacing legacy copper offerings as hyperscale campuses migrate to 800 Gbps optics. The cable assembly market size for fiber products benefits from Meta's multibillion-dollar Corning agreement, which pre-books capacity and signals confidence in long-term demand. Custom cable assemblies, about 28-30% of sales, underpin automotive, aerospace, and medical projects where just-in-time kitting shrinks' inventory on original equipment manufacturers' floors.

Standard off-the-shelf assemblies remain price sensitive, with Chinese contractors routing basic USB-C cables at sub-USD 2-unit costs, compressing margins outside retail-branded niches. Overmolded designs and high-frequency assemblies sustain gross margins near 30% because ingress-protection and insertion-loss guarantees are hard to replicate cheaply. Ribbon and flat-cable formats serve ultrathin consumer devices but face partial substitution from flexible printed circuits that co-laminate signal and power layers.

Fiber-optic cables accounted for 37.72% of 2025 revenue and will continue to lead at a 6.11% CAGR as single-mode specifications with sub-0.3 dB insertion loss become standard in spine-leaf architectures. Coaxial lines, roughly one-fifth of the cable assembly market size, grow more slowly as 5 G installers prefer lower-loss corrugated designs, yet they stay critical for antenna feeders that exceed 100 meters.

Power cables are gaining momentum from 800-volt vehicle architectures, lifting their share of the cable assembly market by mid-single digits as insulation ratings and current thresholds rise. RF and microwave cables, buoyed by electronic-warfare upgrades, sustain mid-single-digit growth on defense budgets that favour higher-frequency radar. Cat6A and Cat7 twisted-pair lines refresh enterprise campuses, but commoditization tempers growth to the low-single-digit range.

Geography Analysis

Asia-Pacific contributed 42.12% of global 2025 revenue and is set to rise at a 5.78% CAGR as TE Connectivity, Hirose Electric, and Luxshare commit fresh capital to the Philippines, India, and mainland China. Japan and South Korea invest in optical-fiber capacity to serve domestic cloud expansion, whereas Vietnam picks up consumer-electronics programs as brands diversify sourcing beyond China.

North America sits near 29% share, with reshoring activity accelerating after Nexans' Electro Cables acquisition and multiple state incentives targeting critical infrastructure supply chains. Mexico advances as a nearshoring hub for harnesses feeding U.S. assembly plants, balancing higher U.S. labor costs.

Europe holds roughly one-fifth of revenue; compliance burdens from RoHS and REACH weigh on smaller shops, yet premium niches such as AI-datacenter fiber and 800-volt vehicle harnesses thrive. Middle East and Africa and South America collectively remain below 10% but log steady orders for submarine links, transit electrification, and regional data-center buildouts.

- TE Connectivity Ltd.

- Amphenol Corporation

- Molex LLC

- Luxshare Precision Industry Co., Ltd.

- Yazaki Corporation

- Aptiv PLC

- Sumitomo Electric Industries, Ltd.

- Rosenberger Hochfrequenztechnik GmbH & Co. KG

- Carlisle Interconnect Technologies (Carlisle Companies Inc.)

- Samtec, Inc.

- HARTING Technology Group

- JAE Electronics, Inc. (Japan Aviation Electronics Industry, Ltd.)

- LEMO SA

- Hirose Electric Co., Ltd.

- Radiall SA

- Belden Inc.

- BizLink Holding Inc.

- Nexans SA

- W. L. Gore & Associates, Inc.

- 3M Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in High-Speed Data-Center Interconnect Demand

- 4.2.2 Expansion of 5G and Fiber-to-the-Home Deployments

- 4.2.3 Electrification and ADAS-Driven Automotive Wiring Complexity

- 4.2.4 Industrial Automation and Smart-Factory Roll-outs

- 4.2.5 Quantum-Computing Cryogenic Cabling Requirements

- 4.2.6 eVTOL and Urban-Air-Mobility Modular Power Harnesses

- 4.3 Market Restraints

- 4.3.1 Volatility in Copper and Specialty Metal Prices

- 4.3.2 Stringent RoHS/REACH and Halogen-Free Material Mandates

- 4.3.3 Tight Supply of High-Performance Fluoropolymer Dielectrics

- 4.3.4 Signal-Integrity Challenges in Ultra-Miniature High-Freq Connectors

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Custom Cable Assemblies

- 5.1.2 Standard / Off-the-Shelf Assemblies

- 5.1.3 Overmolded Cable Assemblies

- 5.1.4 Fiber-Optic Assemblies

- 5.1.5 Ribbon / Flat-Cable Assemblies

- 5.1.6 High-Speed and High-Freq Assemblies

- 5.2 By Cable Type

- 5.2.1 Coaxial

- 5.2.2 Fiber-Optic

- 5.2.3 Ribbon / Flat

- 5.2.4 Twisted-Pair / Networking

- 5.2.5 RF and Microwave

- 5.2.6 Power

- 5.3 By End-Use Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Telecommunications

- 5.3.3 Consumer Electronics

- 5.3.4 Industrial Automation and Robotics

- 5.3.5 Healthcare and Medical Devices

- 5.3.6 Aerospace and Defense

- 5.3.7 IT and Data Centers

- 5.3.8 Energy and Power

- 5.3.9 Rail and Mass Transit

- 5.4 By Application

- 5.4.1 Data Transfer and Communication

- 5.4.2 Power Transmission

- 5.4.3 RF / Microwave Signal

- 5.4.4 High-Performance Computing

- 5.4.5 Sensor and Control

- 5.4.6 Charging and Battery Management

- 5.4.7 Lighting and Display

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TE Connectivity Ltd.

- 6.4.2 Amphenol Corporation

- 6.4.3 Molex LLC

- 6.4.4 Luxshare Precision Industry Co., Ltd.

- 6.4.5 Yazaki Corporation

- 6.4.6 Aptiv PLC

- 6.4.7 Sumitomo Electric Industries, Ltd.

- 6.4.8 Rosenberger Hochfrequenztechnik GmbH & Co. KG

- 6.4.9 Carlisle Interconnect Technologies (Carlisle Companies Inc.)

- 6.4.10 Samtec, Inc.

- 6.4.11 HARTING Technology Group

- 6.4.12 JAE Electronics, Inc. (Japan Aviation Electronics Industry, Ltd.)

- 6.4.13 LEMO SA

- 6.4.14 Hirose Electric Co., Ltd.

- 6.4.15 Radiall SA

- 6.4.16 Belden Inc.

- 6.4.17 BizLink Holding Inc.

- 6.4.18 Nexans SA

- 6.4.19 W. L. Gore & Associates, Inc.

- 6.4.20 3M Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment