|

시장보고서

상품코드

2062206

모놀리식 세라믹 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Monolithic Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

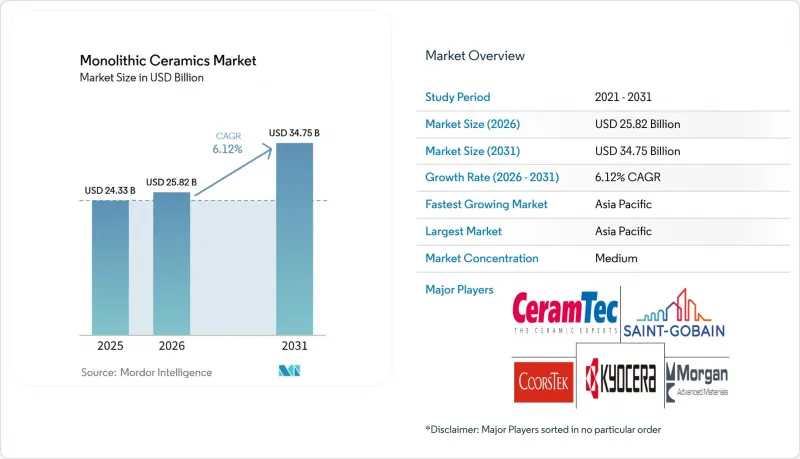

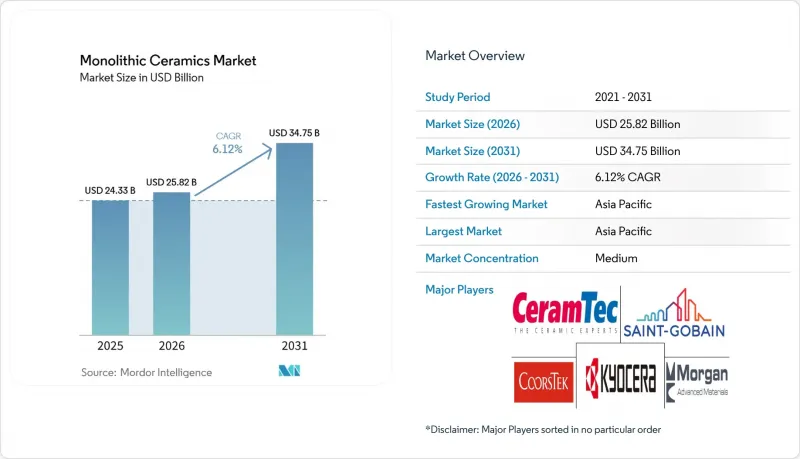

Mordor Intelligence에 의하면, 모놀리식 세라믹 시장 규모는 2025년 243억 3,000만 달러로 평가되었습니다. 2026년에는 258억 2,000만 달러로 확대되어 2031년까지 347억 5,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 6.12%를 나타낼 전망입니다.

본 보고서는 재료의 유형(알루미나, 지르코니아, 실리콘 질화물 등), 구조(투명, 불투명, 다공질), 최종 사용자 산업(일렉트로믹스 및 반도체, 자동차 및 운송 장비 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 모놀리식 세라믹 시장 동향 및 인사이트

EV 파워트레인의 열 관리

와이드 밴드갭 실리콘 카바이드(SiC) 인버터는 현재 99% 이상의 효율을 달성하고 있으며, 실리콘 IGBT에 비해 열 부하를 절반으로 줄이고, 1회 충전당 차량 주행 거리를 약 7% 연장하고 있습니다. ROHM-Schaeffler, STMicroelectronics 및 Infineon의 200mm 웨이퍼 양산으로 인해 다이 비용이 낮아지면서 세라믹 기판 수요 증가가 촉진되고 있습니다. 이러한 열 손실을 방출하기 위해서는 알루미나 및 알루미늄 질화물(AIN)의 직접 본딩 구리 기판이 필수적이지만, 인버터 개발자에게 있어 박리 위험을 줄이기 위한 ISO 26262 준수는 여전히 매우 중요합니다. 모놀리식 세라믹 시장은 800V e-모빌리티 플랫폼의 성장과 밀접하게 연동되어 있습니다. 후공정 공급업체로부터 이미 AIN 시트에 대해 9개월의 리드타임이 보고되어, 가격 결정력의 지속성이 부각되고 있습니다.

반도체 에칭 및 CMP 지그에 대한 수요

TSMC의 2026년 560억 달러 규모의 설비 투자 계획과 인텔의 18A 공정 양산화에 따라, 팹 1곳당 수천 개의 알루미나 웨이퍼 캐리어, 이트리아 코팅 챔버 라이너 및 실리콘 카바이드 서셉터에 대한 수요가 증가할 것으로 예측됩니다. CHIPS법의 지원금을 통해 2025년 말까지 미국의 첨단 로직 생산 점유율이 15% 가까이 확대되었으며, 이에 따라 반도체 고정 장치에 대한 국내 수요가 증가할 것으로 보입니다. NGK 인슐레이터스는 2030년까지 매출 200억 엔을 달성하기 위해 HICERAM의 생산 능력을 3배로 확대하고 있으며, 부품 제조와 반도체 팹의 통합을 중시하고 있습니다. 그러나 인력 부족으로 인해 장비 설치가 지연되면서 특수 캐리어의 미처리 주문량이 증가하고 있습니다. 모놀리식 세라믹 시장은 여전히 반도체 설비 투자 주기와 밀접한 관련이 있으며, 2028년까지의 생산량 전망이 확보되어 있습니다.

고유한 취성 및 설계상의 제약

세라믹의 파단 인성은 3-6 MPa√m 범위이며, 금속에 비해 현저히 낮기 때문에 인장이나 충격이 수반되는 용도에서의 사용이 제한되고 있습니다. 예를 들어, 실리콘 질화물로 제작된 EV 모터용 베어링에는 표면 거칠기 14 nm 이하가 요구되며, 이에 따라 강재에 비해 가공 비용이 4배로 급증합니다. 응력에 대처하기 위해 치수 여유를 확보하면 무게가 증가하는 반면, 적층 조형은 기하학적 유연성을 제공하는 동시에 이방성 결함을 초래합니다. ASTM C1161 및 C1239와 같은 규격은 굽힘 시험 및 와이블 시험에 관한 지침을 제공하고 있지만, 안전성이 극히 중요한 적층 가공 부품에 대한 통일된 인증 절차는 존재하지 않습니다. 이러한 과제들이 세라믹의 보급을 저해하고 있으며, 설계 기준이 발전하기 전까지는 대상 시장이 좁아질 수밖에 없습니다.

부문별 분석

2025년에는 알루미나의 매출 비중이 47.12%를 차지했으나, 실리콘 카바이드는 2031년까지 연평균 성장률(CAGR) 6.58%를 달성할 것으로 예측되어, 소재 부문에서 가장 빠른 성장세를 보일 것으로 전망됩니다. 이는 EV 인버터 및 재생에너지용 컨버터에서 광대역 갭 소자로의 전환에 기인한 것입니다. 알루미나의 경우 비용 면에서의 우위 덕분에 CMP 링이나 임플란트 어버트먼트에 계속 사용되는 반면, 지르코니아의 변태 강화 특성 덕분에 고체 산화물 전해조의 전해질로의 응용이 확대되고 있습니다. 인피니온이 200mm 실리콘 카바이드 웨이퍼로 전환함에 따라 에피택시 비용이 30% 절감되어, 가격 경쟁력 확보를 위한 노력이 탄력을 받고 있습니다.

ST-Sanan사의 48만 장 규모 생산 라인이 2028년에 본격 가동되면, 실리콘 카바이드 기판용 모놀리식 세라믹 시장 규모는 대폭 확대될 것으로 예측됩니다. 한편, 지그용 모놀리식 세라믹 시장에서는 알루미나(알루미나)가 여전히 지배적인 위치를 차지하고 있습니다. 실리콘 질화물이나 틈새 시장용 산화물 소재는 규모는 작지만, 베어링이나 장갑 등의 용도에서 전략적으로 중요합니다. 교세라의 ‘BIOCERAM AZUL’ 하이브리드 블렌드는 굽힘 강도가 1,400 MPa에 달하며, 기존 주요 소재를 뛰어넘는 단계적인 소재 혁신을 상징합니다.

지역별 분석

아시아태평양은 2025년에 매출의 44.22%를 차지했으며, 중국의 첨단 세라믹 생산에 힘입어 2031년까지 연평균 성장률(CAGR) 6.88%를 나타낼 것으로 전망됩니다. 지보(Zibo)와 포산(Foshan) 산업 클러스터의 총 매출액은 1,000억 위안 이상인 반면, 일본 제조업체들은 2024년부터 2026년에 걸쳐 생산 능력과 연구 개발에 550억 엔을 투자하고 있습니다. 또한, 중국 연안 지역의 인건비가 상승하는 가운데, 아세안(ASEAN)의 조립 거점도 부상하고 있습니다.

북미는 CHIPS법의 우대 조치의 혜택을 받고 있습니다. 방위 분야를 중심으로 한 우주용 세라믹에 대한 수요도 성장에 기여하고 있습니다. 2027년에 가동을 시작할 예정인 NGK의 5,800만 달러 규모의 애리조나 공장은 웨이퍼 캐리어 공급을 현지화하게 될 것입니다. 캐나다와 멕시코는 여전히 틈새 시장으로 남아 있으며, 각각 유전용 센서와 기존 타일에 주력하고 있습니다.

유럽에서는 세라믹와 수소 목표가 서로 밀접하게 연관되어 있습니다. 9,400만 유로의 자금 지원을 받은 Topsoe의 덴마크산 전해 장치 공장을 통해 스칸디나비아는 그린 수소 분야의 선도적 위치를 확고히 하고 있습니다. 독일의 기계 부문과 영국의 Morgan Advanced Materials는 항공우주용 복합재료의 주요 공급업체입니다. 그러나 CBAM(탄소국경조정조치) 비용의 상승으로 인해 남유럽 전역에서 가마의 전기화가 추진되고 있습니다. 러시아의 고품질 분말 수출에 대한 제재로 인해, CIS(독립국가연합) 지역 내 수요는 국내 제분 공장으로 이동하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the monolithic ceramics market size is expected to increase from USD 24.33 billion in 2025 to USD 25.82 billion in 2026 and reach USD 34.75 billion by 2031, growing at a CAGR of 6.12% over 2026-2031.

This report is Segmented by Material Type (Alumina, Zirconia, Silicon Nitride, and More), Structure (Transparent, Opaque, and Porous), End-User Industry (Electronics and Semiconductor, Automotive and Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Monolithic Ceramics Market Trends and Insights

EV Power-Train Thermal Management

Wide-bandgap silicon-carbide inverters now achieve over 99% efficiency, reducing heat loads by half compared to silicon IGBTs and increasing vehicle range by approximately 7% per charge. Mass production by ROHM-Schaeffler, STMicroelectronics, and Infineon on 200 mm wafers is lowering die costs and driving higher ceramic substrate volumes. Alumina and aluminum-nitride direct-bonded copper substrates are essential for dissipating these heat losses, while ISO 26262 compliance remains critical to mitigate delamination risks for inverter developers. The Monolithic ceramics market is well-aligned with the growth of 800-V e-mobility platforms. Back-end suppliers are already reporting nine-month lead times for AIN sheets, highlighting sustained pricing power.

Demand for Semiconductor Etch and CMP Fixtures

TSMC's USD 56 billion capital expenditure plan for 2026 and Intel's 18A ramp are expected to add thousands of alumina wafer carriers, yttria-coated chamber liners, and silicon-carbide susceptors per fab. CHIPS Act grants are projected to increase the U.S. share of advanced logic production to nearly 15% by the end of 2025, boosting local demand for semiconductor fixtures. NGK Insulators is tripling its HICERAM capacity to achieve JPY 20 billion in sales by 2030, emphasizing the integration of component manufacturing with semiconductor fabs. However, labor shortages are delaying tool installations, extending order backlogs for specialty carriers. The monolithic ceramics market remains closely tied to semiconductor capital expenditure cycles, ensuring volume visibility through 2028.

Intrinsic Brittleness and Design Limits

The fracture toughness of ceramics, ranging from 3-6 MPa√m, is significantly lower than that of metals, limiting their use in tensile or impact applications. For example, silicon-nitride EV motor bearings require surface roughness of ≤14 nm, increasing machining costs by four times compared to steel. Over-dimensioning to handle stress adds weight, while additive manufacturing introduces anisotropic flaws despite offering geometric flexibility. Standards such as ASTM C1161 and C1239 provide guidelines for flexural and Weibull testing, but no unified certification pathway exists for safety-critical additive-manufactured parts. These challenges constrain the broader adoption of ceramics, narrowing the addressable market until design standards evolve.

Other drivers and restraints analyzed in the detailed report include:

- Medical and Dental Implant Adoption Boom

- Green-Hydrogen Solid-Oxide Electrolyzer Stacks

- Carbon-Neutral Furnace Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alumina held 47.12% of revenue dominance in 2025, but silicon carbide is anticipated to achieve a 6.58% CAGR through 2031, marking the fastest growth among materials. This is attributed to the shift towards wide-bandgap devices in EV inverters and renewable energy converters. Alumina's affordability ensures its continued use in CMP rings and implant abutments, while zirconia's transformation toughening enhances its application in solid-oxide electrolyzer electrolytes. Infineon's transition to 200 mm silicon carbide wafers has reduced epitaxy costs by 30%, supporting efforts to achieve price parity.

The monolithic ceramics market size for silicon carbide substrates is expected to grow significantly once ST-Sanan's 480,000-wafer production line reaches full capacity in 2028. Alumina, however, continues to dominate the monolithic ceramics market for fixtures. Silicon nitride and niche oxides, though smaller in scale, are strategically important for applications such as bearings and armor. Kyocera's BIOCERAM AZUL hybrid blend, with a flexural strength of 1,400 MPa, highlights incremental material innovations beyond the primary materials.

Geography Analysis

Asia-Pacific captured 44.22% of revenue in 2025 and is projected to grow at a 6.88% CAGR through 2031, driven by China's advanced ceramics production. Industrial clusters in Zibo and Foshan have a combined turnover exceeding CNY 100 billion, while Japanese manufacturers are investing JPY 55 billion in capacity and R&D between 2024 and 2026. ASEAN assembly hubs are also emerging as labor costs rise along China's coastal regions.

North America benefits from CHIPS Act incentives. Defense-driven demand for space ceramics is also contributing to growth. NGK's USD 58 million Arizona plant, set to become operational in 2027, will localize wafer-carrier supply. Canada and Mexico remain niche players, focusing on oil-field sensors and traditional tiles, respectively.

Europe interlinks ceramics with hydrogen goals. Topsoe's Danish electrolyzer plant, supported by EUR 94 million in funding, positions Scandinavia as a leader in green hydrogen. Germany's machinery sector and the U.K.'s Morgan Advanced Materials are key suppliers of aerospace composites. However, rising CBAM costs are prompting kiln electrification across southern Europe. Sanctions on Russia's advanced powder exports are redirecting demand within the CIS to domestic mills.

- 3M

- CeramTec GmbH

- CoorsTek Inc.

- Elan Technology

- H.C. Starck Tungsten GmbH

- Hitachi Chemical Co., Ltd.

- Kyocera Corporation

- Materion Corporation

- Morgan Advanced Materials

- Murata Manufacturing Co., Ltd.

- NGK INSULATORS, LTD.

- Rauschert Heinersdorf-Pressig GmbH

- Saint-Gobain

- SGL Carbon

- Sumitomo Electric Industries, Ltd.

- TOSOH CERAMICS CO., LTD.

- Vesuvius

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV power-train thermal management

- 4.2.2 Demand for semiconductor etch and CMP fixtures

- 4.2.3 Medical and dental implant adoption boom

- 4.2.4 Green-hydrogen solid-oxide electrolyzer stacks

- 4.2.5 Space economy (re-usable launchers, hypersonics)

- 4.3 Market Restraints

- 4.3.1 Intrinsic brittleness and design limits

- 4.3.2 Dopant-grade alumina and yttria supply squeeze

- 4.3.3 Carbon-neutral furnace regulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Alumina

- 5.1.2 Zirconia

- 5.1.3 Silicon Nitride

- 5.1.4 Silicon Carbide

- 5.1.5 Other Material Types (Magnesia, Mullite, Boron Carbide, etc.)

- 5.2 By Structure

- 5.2.1 Transparent

- 5.2.2 Opaque

- 5.2.3 Porous

- 5.3 By End-user Industry

- 5.3.1 Electronics and Semiconductor

- 5.3.2 Automotive and Transportation

- 5.3.3 Medical and Dental

- 5.3.4 Energy and Power

- 5.3.5 Other End-user Industries (Industrial Equipment, Chemical, Metallurgy, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 CeramTec GmbH

- 6.4.3 CoorsTek Inc.

- 6.4.4 Elan Technology

- 6.4.5 H.C. Starck Tungsten GmbH

- 6.4.6 Hitachi Chemical Co., Ltd.

- 6.4.7 Kyocera Corporation

- 6.4.8 Materion Corporation

- 6.4.9 Morgan Advanced Materials

- 6.4.10 Murata Manufacturing Co., Ltd.

- 6.4.11 NGK INSULATORS, LTD.

- 6.4.12 Rauschert Heinersdorf-Pressig GmbH

- 6.4.13 Saint-Gobain

- 6.4.14 SGL Carbon

- 6.4.15 Sumitomo Electric Industries, Ltd.

- 6.4.16 TOSOH CERAMICS CO., LTD.

- 6.4.17 Vesuvius

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment