|

시장보고서

상품코드

2062230

환형 올레핀 공중합체 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cyclic Olefin Copolymer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

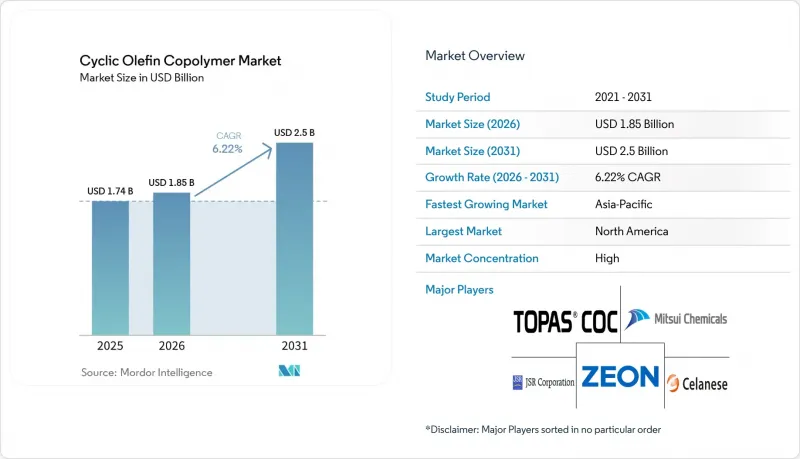

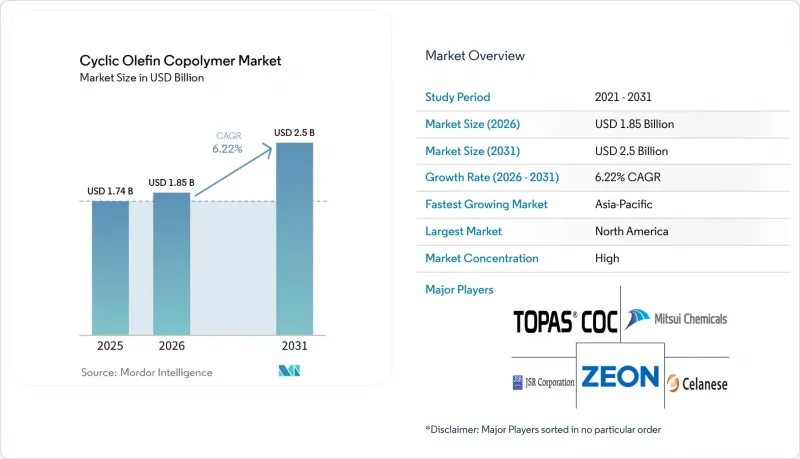

Mordor Intelligence에 의하면, 환형 올레핀 공중합체 시장 규모는 2025년 17억 4,000만 달러로 평가되었습니다. 2026년 18억 5,000만 달러로 확대되어 2031년까지 25억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 6.22%를 나타낼 것으로 전망됩니다.

본 보고서는 유형별(비정질 COC 및 반결정질 COC), 등급별(사출 성형용 등급, 블로우 성형용 등급, 필름 및 시트용 등급, 기타), 최종 사용자 산업별(헬스케어 및 의료, 전자·광전자, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 환형 올레핀 공중합체 시장 동향 및 분석

의약품용 블리스터 팩, 프리필드 주사기, 바이알에 대한 수요 증가

유리 표면은 바이오의약품을 열화시키는 단백질의 흡착을 촉진하지만, COC의 26 mN/m에 달하는 표면 에너지는 이러한 결합을 억제하여 약물의 효능을 유지합니다. ZEONEX의 의료용 주사기는 -194°C에서도 충격 강도를 유지하므로, 초저온 유통망을 통한 mRNA 및 세포 치료제의 운송을 가능하게 합니다. 단일 소재로 제작된 COC 블리스터는 수증기 투과율이 0.1 g/m²/일 이하에 달하여 포일 라미네이트에 필적하는 성능을 발휘할 뿐만 아니라, EU의 재활용 가능성 관련 규정도 준수하고 있습니다. 제온의 수직 통합형 C5 체인은 잔류 불포화도를 0.02 wt% 이하로 억제하고 있으며, 이는 FDA의 의약품 마스터 파일(DMF) 승인을 위한 전제조건입니다. 그러나 다이셀은 2026년 수주량이 4% 감소함에 따라 독일에서의 가동 시작을 2027년 1분기로 연기했습니다. 이로 인해 소수의 제약 기업에 대한 의존도가 드러났습니다.

마이크로플루이딕스 및 현장 진단용 랩온칩 장치에의 적용

폴리디메틸실록산은 소수성 시약을 흡수하지만, 시중에 유통되는 환상 올레핀 공중합체(COC) 용액에서는 저분자 물질의 분배가 거의 관찰되지 않기 때문에 분석의 정확도가 향상됩니다. 프라운호퍼 연구소의 테스트 결과, 엘라스토머 재질의 COC 칩으로 1만 회의 공압 밸브 사이클을 달성하여, 경질 열가소성 플라스틱에 비해 장치의 수명을 연장했습니다. COVID-19 형광 검사에서 폴리스티렌 기판에서 COC 기판으로 변경한 결과, 자가형광 노이즈가 신호의 5% 이하로 감소했습니다. 하이브리드 COC-PLGA 마이크로채널은 약물 전달 저장소를 내장한 웨어러블 인슐린 펌프의 구현을 가능하게 합니다. EU와 미국의 ISO 10993 검사 요건 차이는 북미의 수탁 성형 업체에 유리한 규제 상의 차익 거래를 낳고 있습니다.

폴리올레핀 범용 플라스틱에 비해 높은 수지 비용

환형 올레핀 공중합체 시장 가격은 직쇄형 LDPE(LLPE)의 2.5-3.5배 수준에서 거래되고 있습니다. 이는 노르볼렌의 합성 및 메타세시스 중합에 막대한 설비 투자가 필요한 C5 크래커와 다단계 수소화 공정이 요구되기 때문입니다. 신흥 지역의 일반적인 블리스터 포장 용도에서는 하루 1-2 g/m²의 수분 함량 목표를 절반의 비용으로 충족시키는 폴리프로필렌이 계속해서 사용되고 있습니다. 중국 공급업체의 가격은 일본 기준 가격보다 15-20% 저렴하지만, 펠릿 건조 공정의 미비로 인해 가수분해로 인한 결함이 발생하여 의약품 및 반도체 공급망에서 배제되고 있습니다. 2025년 1분기, 아시아의 크래커가 예기치 않게 가동을 중단함에 따라 시클로펜타디엔 원료 가격이 18% 급등했고, 고정 가격 의약품 계약에 묶여 있던 컨버터의 이익률이 압박을 받았습니다. 고객들의 신중한 태도로 인해 다이셀은 독일 공장의 가동을 연기할 수밖에 없게 되었으며, 가격 변동이 장기 공급 계약을 얼마나 억제하는지가 여실히 드러났습니다.

부문별 분석

2025년, 비정질 COC는 유리에 필적하는 투명성을 갖추고 있으며, 바이알 및 마이크로플루이딕스 장치용의 공차가 엄격한 사출 성형이 가능하다는 점 덕분에 사이클로올레핀 공중합체 시장 점유율의 58.27%를 차지했습니다. 이 등급들은 101-154°C의 유리 전이 온도와 2,900 MPa에 가까운 탄성 계수를 실현하여, 정렬 공차가 5 마이크로미터 이내로 유지되는 스마트폰 렌즈를 뒷받침하고 있습니다. 반결정질 등급은 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 6.58%를 나타낼 것으로 전망됩니다. 이는 자동차용 헤드업 디스플레이나 ADAS(첨단 운전자 보조 시스템) 카메라의 경우, 김서림 현상 없이 120°C를 초과하는 높은 열변형 온도가 요구되기 때문입니다.

새로운 공중합체 사슬로 강화된 반결정성 수지는 성장률을 4%에서 245%까지 확대하여, 1만 회의 굽힘 사이클을 견딜 수 있는 폴더블 디스플레이의 백플레인을 구현합니다. ZEONEX 360R의 초저 복굴절률은 색차로 인한 지연이 5 nm 이하로 억제되므로, 증강현실(AR)용 광학 시스템을 지원합니다. 스미토모 화학의 광경화성 COC는 열가소성 수지의 가공성과 열경화성 수지의 치수 안정성을 결합하여, 반도체 리소그래피 분야에서 용제 내성 포토레지스트에 대한 수요를 충족시키고 있습니다. 엄격한 ISO 9001 규격에 따른 관리를 통해 굴절률 편차를 ±0.001 이내로 억제하고 있으며, 이는 스마트폰 카메라 OEM 업체가 요구하는 기준치입니다.

지역별 분석

2025년 매출액 중 북미가 31.16%를 차지했습니다. 미국의 약물 전달 기업들은 -194°C의 운송 환경에서도 균열이 발생하지 않는 COC 재질의 주사기를 높이 평가했습니다. 제온의 국내 창고 덕분에 리드타임이 1주일로 단축되어, 유럽에서의 해상 운송에 비해 뚜렷한 우위를 보이고 있습니다. 캐나다의 마이크로플루이딕스 스타트업은 염료 흡수율이 낮다는 점을 고려해 폴리디메틸실록산(PDMS)에서 COC로 소재를 전환하고 있는 반면, 멕시코의 렌즈 성형 제조업체는 120°C에서 작동하는 ADAS 카메라용으로 APEL을 채택하고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 7.02%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 제온이 700억 엔(4억 7,000만 달러)을 투자해 건설하는 ‘토쿠야마 이스트’ 복합 시설 덕분에, 2028년까지 일본의 생산량은 30% 증가한 연간 54킬로톤에 달할 전망이며, 이에 따라 한국의 디스플레이 공장에 대한 수지 공급난이 완화될 것으로 보입니다. 인장 성장률을 5배로 높인 한국의 연구 결과, 해당 지역공급업체들은 롤형 OLED 기판 부문의 선두에 서 있습니다. 중국은 2024년에 연간 1만 톤의 저비용 사출 성형용 수지를 생산했으나, 펠릿의 수분 함량이 규격을 초과함에 따라 의약품 사업에서 시장 점유율은 여전히 극히 낮은 수준에 머물러 있습니다. 인도는 고습도 API용 COC 블리스터 웹을 검토하고 있으나, 여전히 가격에 민감한 상황입니다.

유럽에서는 2025년 VerpackG 요금 인상에 따라 블리스터 형태의 유효성 검증이 가속화되고 있습니다. 그럼에도 불구하고, 폴리플라스틱스는 초기 단계의 PPWR(폴리프로필렌 수지)에 대한 투자가 부진한 상황을 감안하여 로이나 공장의 가동을 2027년으로 연기했습니다. 북유럽에서 실시된 인슐린 바이알에 대한 시범 검사 결과, COC의 흡습률이 0.1 g/m²/일 이하임이 입증되어 24개월의 보관 기간이 확보되었습니다. 남미와 중동 및 아프리카는 이미 고가의 수지에 운송비와 수입 관세가 10-15% 추가되기 때문에 사용이 최상위급 바이오의약품으로만 제한되어 뒤처지고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the cyclic olefin copolymer market size is expected to increase from USD 1.74 billion in 2025 to USD 1.85 billion in 2026 and reach USD 2.5 billion by 2031, growing at a CAGR of 6.22% over 2026-2031.

This report is Segmented by Type (Amorphous COC and Semi-Crystalline COC), Grade (Injection-Molding Grade, Blow-Molding Grade, Film and Sheet Grade, and More), End-User Industry (Healthcare and Medical, Electronics and Optoelectronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Cyclic Olefin Copolymer Market Trends and Insights

Rising Demand for Pharmaceutical Blister Packs, Pre-filled Syringes and Vials

Glass surfaces promote protein adsorption that degrades biologics, whereas COC's 26 mN/m surface energy curbs binding and maintains drug potency. ZEONEX medical-grade syringes retain impact strength at -194°C, enabling mRNA and cell-therapy distribution in ultra-cold chains. Monomaterial COC blisters reach moisture-vapor transmission rates below 0.1 g/m2/day, rivaling foil laminates and aligning with EU recyclability rules. Zeon's vertically integrated C5 chain secures residual-unsaturation levels under 0.02 wt%, a prerequisite for FDA Drug Master File acceptance. Yet Daicel shifted its German start-up to Q1 2027 after 2026 order volumes fell 4%, exposing reliance on a few pharmaceutical accounts.

Adoption in Microfluidics and Point-of-Care Lab-on-Chip Devices

Polydimethylsiloxane absorbs hydrophobic reagents, whereas cyclic olefin copolymer market solutions show negligible small-molecule partitioning, sharpening assay accuracy. Fraunhofer trials achieved 10,000 pneumatic-valve cycles in elastomeric COC chips, extending device lifetimes versus rigid thermoplastics. COVID-19 fluorescence tests lowered autofluorescence noise to under 5% of signal when switching from polystyrene to COC substrates. Hybrid COC-PLGA microchannels are enabling wearable insulin pumps with integrated drug-delivery reservoirs. Divergent ISO 10993 test regimes between the EU and the USA create regulatory arbitrage that favors North American contract molders.

High Resin Cost Versus Polyolefin Commodity Plastics

Cyclic olefin copolymer market resin sells at 2.5-3.5 times linear low-density polyethylene because norbornene synthesis and metathesis polymerization require capital-heavy C5 crackers and multi-stage hydrogenation. Generic blister applications in emerging regions stay with polypropylene that meets 1-2 g/m2/day moisture targets at half the cost. Chinese suppliers undercut Japanese benchmarks by 15-20%, but pellet-drying lapses yield hydrolysis defects that rule them out of pharma and semiconductor supply chains. Cyclopentadiene feedstock prices spiked 18% in Q1 2025 after Asian crackers shut unexpectedly, squeezing converter margins locked into fixed drug-contract pricing. Customer reticence forced Daicel to delay its German plant commissioning, highlighting how price volatility suppresses long-term offtake deals.

Other drivers and restraints analyzed in the detailed report include:

- Growth of High-Resolution Display and LED Optical Films

- EU PPWR Push for Monomaterial Recyclable Pharma Blister Formats

- Limited Large-Scale Mechanical Recycling Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Amorphous COC controlled 58.27% cyclic olefin copolymer market share in 2025, owing to glass-like clarity and tight-tolerance injection molding for vials and microfluidics. These grades deliver glass-transition points of 101-154°C and modulus near 2,900 MPa, sustaining smartphone lenses where alignment tolerances stay within 5 µm. Semi-crystalline variants are pacing a 6.58% CAGR for the forecast period (2026-2031) as automotive head-up displays and ADAS (Advanced Driver Assistance Systems) cameras need higher heat-deflection ceilings above 120°C without haze growth.

Semi-crystalline resins, strengthened through novel copolymer chains, extend elongation from 4% to 245%, permitting foldable display backplanes that endure 10,000 flex cycles. ZEONEX 360R's ultralow birefringence supports augmented-reality optics because color shift remains under 5 nm retardation. Sumitomo's photocurable COC hybridizes thermoplastic processing with thermoset dimensional stability, responding to semiconductor lithography's need for solvent-resistant photoresists. Tight ISO 9001 controls cap refractive-index variance at +-0.001, a threshold demanded by phone-camera OEMs.

Geography Analysis

North America accounted for 31.16% of 2025 sales. U.S. drug-delivery firms value COC syringes that survive -194°C transport without cracks. Zeon's domestic depots shorten lead times to one week, a clear edge over ocean freight from Europe. Canadian microfluidic start-ups pivot from Polydimethylsiloxane (PDMS) to COC for low dye absorption, while Mexican lens molders adopt APEL for ADAS cameras that function at 120°C.

Asia-Pacific is the fastest-growing geography with a 7.02% CAGR to 2031. Zeon's JPY 70 billion (USD 470 million) Tokuyama East complex will lift Japanese output 30% to 54 kilotons/year by 2028, easing resin allocations for South Korean display fabs. Korean research that multiplies tensile elongation fivefold positions regional suppliers at the forefront of rollable OLED substrates. China added 10 kilotons/year of low-cost injection resin in 2024, yet still captures a very low share of the pharmaceutical business because pellets exceed moisture specs. India explores COC blister webs for high-humidity APIs but remains price sensitive.

Europe accelerates blister-format validation following the 2025 VerpackG fee hike. Still, Polyplastics deferred its Leuna start-up to 2027 amid weak early-stage PPWR spending. Nordic insulin-vial pilots showcase COC's less than 0.1 g/m2/day moisture rate, protecting 24-month shelf lives. South America and MEA lag because freight costs and import duties add 10-15% to already premium resin, restricting use to top-tier biologics.

- Asahi Kasei Corporation

- Avantor Inc.

- BOREALIS GMBH.

- Celanese Corporation

- Daikyo Seiko Ltd.

- ExxonMobil Corp.

- JSR Corporation

- Mitsui Chemicals, Inc.

- Polysciences

- RTP Company

- SABIC

- Sumitomo Chemical Co., Ltd.

- TOPAS Advanced Polymers / Polyplastics

- ZEON CORPORATION

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for pharmaceutical blister packs, pre-filled syringes and vials

- 4.2.2 Adoption in micro-fluidics and point-of-care lab-on-chip devices

- 4.2.3 Growth of high-resolution display and LED optical films

- 4.2.4 EU-PPWR push for monomaterial recyclable pharma blister based on COC

- 4.2.5 COC backplane substrates enabling ultra-thin foldable micro-LED panels

- 4.3 Market Restraints

- 4.3.1 High resin cost versus polyolefin commodity plastics

- 4.3.2 Limited large-scale mechanical recycling infrastructure

- 4.3.3 Supply-chain concentration with lesser global resin producers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Amorphous COC

- 5.1.2 Semi-crystalline COC

- 5.2 By Grade

- 5.2.1 Injection-Molding Grade

- 5.2.2 Blow-Molding Grade

- 5.2.3 Film and Sheet Grade

- 5.2.4 Medical and Pharmaceutical Grade

- 5.3 By End-user Industry

- 5.3.1 Healthcare and Medical

- 5.3.2 Electronics and Optoelectronics

- 5.3.3 Packaging

- 5.3.4 Automotive and Transportation

- 5.3.5 Other End-user Industries (Consumer Goods, and More)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Asahi Kasei Corporation

- 6.4.2 Avantor Inc.

- 6.4.3 BOREALIS GMBH.

- 6.4.4 Celanese Corporation

- 6.4.5 Daikyo Seiko Ltd.

- 6.4.6 ExxonMobil Corp.

- 6.4.7 JSR Corporation

- 6.4.8 Mitsui Chemicals, Inc.

- 6.4.9 Polysciences

- 6.4.10 RTP Company

- 6.4.11 SABIC

- 6.4.12 Sumitomo Chemical Co., Ltd.

- 6.4.13 TOPAS Advanced Polymers / Polyplastics

- 6.4.14 ZEON CORPORATION

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment