|

시장보고서

상품코드

2062232

그라비어 인쇄용 잉크 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Rotogravure Printing Inks - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

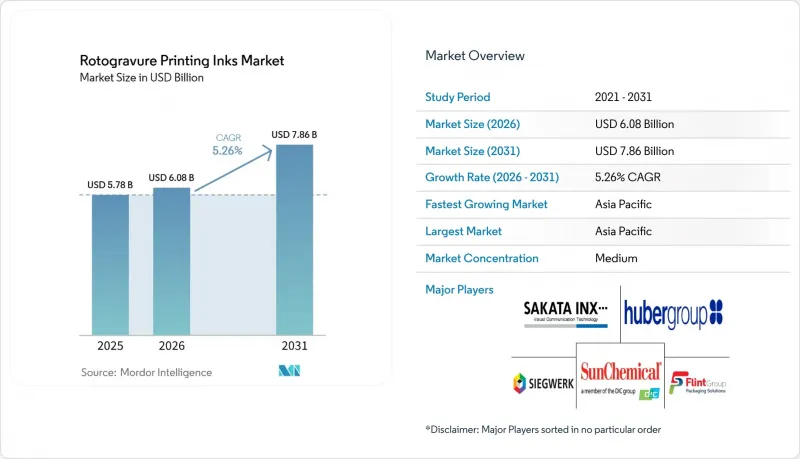

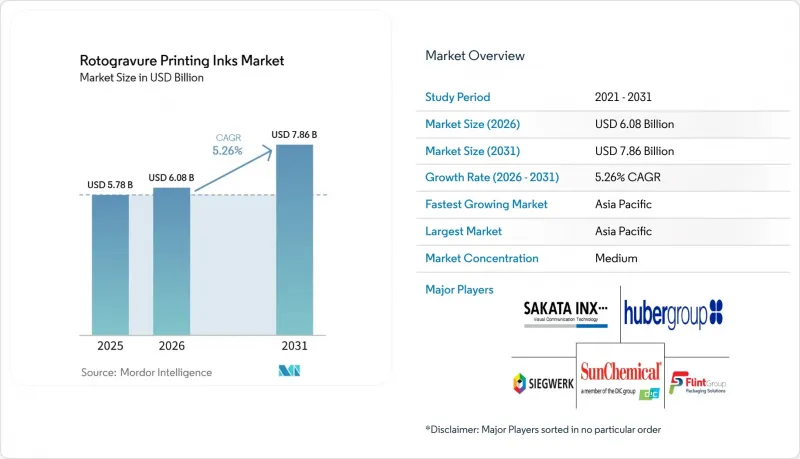

Mordor Intelligence에 의하면, 그라비어 인쇄용 잉크 시장 규모는 2025년에 57억 8,000만 달러로 평가되었습니다. 2026년 60억 8,000만 달러에서 2031년까지 78억 6,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 5.26%를 나타낼 전망입니다.

본 보고서는 수지 유형(니트로셀룰로오스, 폴리아미드 등), 기술(용제형, 수성, EB/UV 경화형), 용도(연질 포장, 라벨·포장지 등), 최종 사용자 산업(식품 및 음료, 퍼스널케어 및 화장품 등), 지역(아시아태평양, 북미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 그라비어 인쇄용 잉크 시장 동향 및 분석

연질 포장 분야에서 고속 인쇄에 대한 수요 증가

현재, 연질 포장 변환 업체들은 중앙 인장식 그라비어 인쇄기를 분당 400m의 지속 속도로 가동하고 있으며, 이는 2020년 대비 25% 증가한 수치입니다. 이로 인해 소비재(FMCG) 분야의 리드타임이 2주에서 72시간으로 단축되었습니다. 이러한 고속 인쇄에 필요한 점도 안정성 덕분에, 인쇄 중 용매 손실에 대한 내성이 있는 폴리우레탄 및 아크릴 개질 바인더에 대한 선호도가 높아지고 있습니다. 아시아태평양의 연포장 시장 규모는 2026년에 901억 2,000만 달러에 달할 것으로 보이며, 인도, 인도네시아, 베트남의 도시화 진전을 배경으로 2035년까지 1,247억 7,000만 달러로 확대될 것으로 전망됩니다. 도요 잉크가 2025년 11월에 발표한 구자라트주의 액체 잉크 공장을 1.5배로 확장하겠다는 계획은 해당 지역에서 고처리량 그라비어 인쇄의 중요성이 앞으로도 지속될 것이라는 공급업체의 확신을 반영하고 있습니다.

신흥 시장의 FMCG 및 식품 및 음료 포장 시장의 성장

2025년, 식품 및 음료 분야는 전 세계 잉크 사용량의 48.02%를 차지했으며, 인도와 동남아시아의 1인당 포장 식품 소비량 증가에 따라 이와 유사한 점유율을 유지할 것으로 예측됩니다. 인도에서만 해도 2025년에 슈퍼마켓 체인이 1만 2,000개 매장을 신규로 개설되었으며, 각 매장에서는 위조 방지 기능과 고해상도 그래픽이 요구되고 있습니다. 그라비어 인쇄는 10만 부를 초과하는 생산 물량에서 플렉소 인쇄에 비해 비용 면에서 우위를 차지합니다. 2025년 9월 지크베르크사가 단행한 35억 루피 규모의 투자는 프리미엄 과자 부문에서 15-20%의 가격 프리미엄이 기대되는 메탈릭 효과 바니시에 초점을 맞춘 것입니다.

VOC 및 유해 용제 규제 강화

EU의 산업 배출 지침에서는 신규 그라비어 인쇄 라인에 대해 50 mg/m³의 상한치가 설정되어 있으며, REACH 부속서 XVII에서는 완제품 내 벤조페논 함유량을 0.6 mg/kg 미만으로 제한하고 있습니다. 미국의 EPA 지침에 따른 유사한 규제로 인해, 각 변환기 제조업체들은 산화 장치에 50만-200만 달러를 투자하지 않는 한, 수성 또는 전자선(EB) 경화형 화학 약품으로 전환해야 하는 상황에 처해 있습니다. Flint Group의 EcoVadis 골드 인증을 획득한 니트로셀룰로오스 무함유 제품군은 RecyClass의 사전 승인을 받아 2025년 입찰에 참여했습니다. 이를 통해 해당 회사는 브랜드 소유자가 제출한 제안 요청서(RFP)에 대해, 지역 내 경쟁사들이 12주가 소요되는 데 비해 불과 4주 만에 대응할 수 있게 되었습니다.

부문별 분석

니트로셀룰로오스는 2025년 매출의 36.13%를 차지했습니다. 바이오 원료로 생산된 폴리우레탄 시장은 2031년까지 연평균 성장률(CAGR) 5.89%를 기록하며 성장할 것으로 전망됩니다. 폴리아미드는 고속 출판 인쇄 분야에서 여전히 선호되고 있습니다. 다만, 이 분야의 성장세는 여전히 완만합니다. 아크릴 개질 시스템은 자외선 저항성 덕분에 장식용 라미네이트 분야에서 틈새 수요를 유지하고 있습니다. 한편, 에폭시 바인더는 항균 기능층에 있어 필수적입니다.

탄소 가격이 톤당 80유로를 넘으면, 2029년까지 피마자유 유래 폴리올과 석유화학계 대체품 간의 비용 차이는 해소될 것으로 예측됩니다. 도요 잉크의 톨루엔 무함유 니므라나 공장은 코로나 처리 필름에 대한 밀착성을 확보하면서도 용제 노출을 줄이려는 공급업체의 노력을 상징합니다.

2025년에는 용제형 그라비어 잉크가 수요의 68.92%를 차지했습니다. 이는 PE 및 PP 기판 위에서 분당 400미터의 인쇄 속도를 지원할 수 있기 때문입니다. 수성 잉크는 60°C에서 실시된 RecyClass 세척 시험을 통과한 DIC의 RePOS 탈잉크 가능 제품 라인을 바탕으로 그 기세를 더해가고 있습니다. EB/UV 경화형 그라비어 잉크는 의약품 일련번호 부여 요건을 배경으로, 2031년까지 연평균 성장률(CAGR) 6.04%를 기록하며 성장할 것으로 전망됩니다.

하이브리드 워크플로가 점차 보편화됨에 따라, 각 변환기 제조업체들은 불투명한 백색 잉크에 고고형분 용제형 잉크를 사용하고, CMYK 오버레이에는 광개시제 함량을 40% 줄인 ‘SunCure Advance ECO’ 등의 LED-UV 잉크를 채택하고 있습니다. 그러나 높은 설비 투자 비용이 EB 기술의 보급에 걸림돌이 되고 있어, 그 사용은 블리스터 팩이나 화장품 등 수익성이 높은 용도로만 제한되고 있습니다.

지역별 분석

아시아태평양은 2025년 수요의 46.83%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 6.37%를 나타낼 것으로 전망됩니다. 2026년 3월 지크베르크사가 하이테크 잉크스를 인수함에 따라, 인도 내 해당 회사 시장 점유율은 20%를 넘어섰으며, 저이온화 기술에 대한 전문 지식과 현지 용제 생산 체계를 결합하게 되었습니다. 중국의 성장세는 둔화되고 있지만, DIC의 RePOS 잉크를 사용한 초콜릿, 커피, 화장품용 프리미엄 포장 시장으로 전환되고 있습니다. 일본과 한국은 완만한 성장에 그치고 있지만, 블리스터 팩용 EB 기술의 도입을 계속하고 있습니다. 아세안 국가들에서는 2025년에 1만 8,000개의 슈퍼마켓이 늘어났으며, 이는 소포장 및 파우치 제품에 대한 수요를 견인할 것으로 보입니다.

북미에서는 미국의 변환업체들이 관세 개혁으로 인한 MEK 가격 급등에 직면해 있지만, EC 시장용 내마모성 요건으로 인해 용제형 그라비어 잉크 수요는 유지되고 있습니다. 캐나다와 멕시코는 니어쇼어링 추세의 혜택을 누리고 있으며, 국경을 넘나드는 적시 공급망이 자동차용 와이어 하네스 생산을 뒷받침하고 있습니다.

유럽에서는 엄격한 IED 규제로 인해 수성 및 EB 기술의 도입이 가속화되고 있습니다. 독일, 프랑스, 영국에서는 주로 의약품 블리스터 포장이나 고급 식품 포장 분야에서 RecyClass 인증이 요구되고 있습니다. 러시아 시장은 공급 제약으로 인해 위축되는 추세이지만, 폴란드와 체코는 출판 및 인쇄 분야의 제2 거점으로 부상하고 있습니다.

남미 수요는 브라질의 커피, 제과류 및 개인 위생용품 포장 시장이 주도하고 있습니다. 중동 및 아프리카는 여전히 개발도상 시장이지만, WHO가 지원하는 항말라리아제 시리얼화 시범 사업을 통해 INVENTRA사가 제조하는 RFID 지원 그라비어 슬리브에 대한 수요가 발생하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the rotogravure printing inks market size was valued at USD 5.78 billion in 2025 and is estimated to grow from USD 6.08 billion in 2026 to reach USD 7.86 billion by 2031, at a CAGR of 5.26% during the forecast period (2026-2031).

This report is Segmented by Resin Type (Nitrocellulose, Polyamide, and More), Technology (Solvent-Based, Water-Based, and EB/UV-curable), Application (Flexible Packaging, Labels and Wrappers, and More), End-User Industry (Food and Beverage, Personal Care and Cosmetics, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Rotogravure Printing Inks Market Trends and Insights

Rising Demand for High-Speed Printing in Flexible Packaging

Flexible packaging converters now operate central-impression gravure presses at sustained speeds of 400 m/min, a 25% increase compared to 2020, reducing lead times from two weeks to seventy-two hours in fast-moving consumer goods segments. The viscosity stability required for such speeds has shifted preferences toward polyurethane and acrylic-modified binders that resist solvent loss during printing. Asia-Pacific's flexible packaging expenditure reached USD 90.12 billion in 2026 and is projected to grow to USD 124.77 billion by 2035, driven by urbanizing populations in India, Indonesia, and Vietnam. Toyo Ink's November 2025 plan to expand its Gujarat liquid-ink plant by 1.5 times reflects supplier confidence in the continued importance of high-throughput gravure printing in the region.

FMCG and Food-Beverage Packaging Growth in Emerging Markets

Food and beverage applications accounted for 48.02% of global ink volume in 2025 and are expected to maintain a similar share as per-capita packaged food consumption increases in India and Southeast Asia. In India alone, supermarket chains added 12,000 outlets in 2025, each requiring tamper-evident, high-definition graphics. Gravure printing offers cost advantages over flexography for production runs exceeding 100,000 impressions. Siegwerk's INR 350 crore investment in September 2025 focuses on metallic-effect varnishes, which command a 15-20% price premium in the premium confectionery segment.

Tightening VOC and Hazardous-Solvent Regulations

The EU Industrial Emissions Directive has set a 50 mg/m3 ceiling for new gravure lines, while REACH Annex XVII restricts benzophenone levels to below 0.6 mg/kg in finished articles. Similar regulations in the United States under EPA guidelines are pushing converters toward water-based or electron-beam (EB) curable chemistries unless they invest USD 0.5-2 million in oxidizers. Flint Group's EcoVadis Gold-certified nitrocellulose-free product suite entered 2025 tenders with RecyClass pre-clearance, enabling the company to respond to brand-owner requests for proposals (RFPs) in four weeks, compared to twelve weeks for regional competitors.

Other drivers and restraints analyzed in the detailed report include:

- Brand-Owner Push for Premium Graphics on Recyclable Mono-Material Films

- Expansion of E-Commerce Requiring Long-Run Durable Prints

- Photoinitiator Toxicology Scrutiny in UV/EB Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nitrocellulose retained 36.13% of 2025 revenue. Polyurethane, supported by bio-based grades, is projected to grow at a CAGR of 5.89% through 2031. Polyamide continues to be preferred for high-speed publication printing, although growth in this application remains slow. Acrylic-modified systems maintain niche demand in decorative laminates due to their UV resistance, while epoxy binders are critical for antimicrobial functional layers.

Carbon pricing exceeding EUR 80 per ton is expected to eliminate the cost difference between castor-oil polyols and petrochemical alternatives by 2029. Toyo Ink's toluene-free Neemrana plant highlights supplier efforts to reduce solvent exposure while ensuring adhesion on corona-treated films.

Solvent-based gravure inks accounted for 68.92% of demand in 2025, driven by their compatibility with 400 m/min press speeds on PE and PP substrates. Water-based inks are gaining traction, supported by DIC's RePOS de-inkable line, which passed RecyClass wash tests at 60°C. EB/UV-curable gravure inks are anticipated to grow at a CAGR of 6.04% through 2031, driven by drug serialization requirements.

Hybrid workflows are becoming more common, with converters using high-solids solvent inks for opaque whites and overlaying CMYK with LED-UV inks, such as SunCure Advance ECO, which reduces photoinitiator mass by 40%. However, high capital costs remain a barrier to broader adoption of EB technology, limiting its use to high-margin applications like blister packs and cosmetics.

Geography Analysis

Asia-Pacific absorbed 46.83% of 2025 demand and is projected to grow at a CAGR of 6.37% through 2031. Siegwerk's acquisition of Hi-Tech Inks in March 2026 increased its market share in India to over 20%, combining expertise in low-migration technology with local solvent production. While China's growth moderates, it is shifting toward premium packaging for chocolate, coffee, and cosmetics using DIC's RePOS inks. Japan and South Korea show slow growth but continue adopting EB technology for blister packs. ASEAN nations are expected to add 18,000 supermarkets in 2025, driving demand for sachets and pouches.

In North America, U.S. converters face rising MEK prices due to tariff reforms, but e-commerce abrasion requirements sustain demand for solvent-based gravure inks. Canada and Mexico benefit from near-shoring trends, with cross-border just-in-time supply chains supporting automotive harness production.

In Europe, stringent IED regulations are accelerating the adoption of water-based and EB technologies. In Germany, France, and the United Kingdom, primarily in pharmaceutical blister packs and premium food wraps requires RecyClass certification. Russia's market is contracting due to supply constraints, while Poland and the Czech Republic are emerging as secondary hubs for publication printing.

South America's demand is driven by Brazilian coffee, confectionery, and personal care packaging. The Middle-East and Africa remain nascent markets, but WHO-backed serialization pilots for antimalarials are creating demand for RFID-enabled gravure sleeves produced by INVENTRA.

- Artience Co., Ltd.

- DIC Corporation

- Doneck Euroflex

- Flint Group

- hubergroup Deutschland GmbH

- Nazdar Ink Technologies

- Royal Ink & Resin

- SAKATA INX CORPORATION

- Siegwerk Druckfarben AG & Co. KGaA

- Sun Chemical

- Superior Printing Inks Co.

- Toyo Ink SC Holdings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for high-speed printing in flexible packaging

- 4.2.2 FMCG and food-beverage packaging growth in emerging markets

- 4.2.3 Brand-owner push for premium graphics on recyclable mono-material films

- 4.2.4 Expansion of e-commerce requiring long-run durable prints

- 4.2.5 Bio-based polyurethane dispersions enabling less than 5% VOC gravure inks

- 4.2.6 Embedded RFID/printed-electronics gravure inks for supply-chain traceability

- 4.3 Market Restraints

- 4.3.1 Tightening VOC and hazardous-solvent regulations

- 4.3.2 Feedstock-price volatility (resins, pigments, solvents)

- 4.3.3 Rapid migration to digital inkjet for short runs

- 4.3.4 Photoinitiator toxicology scrutiny in UV/EB systems

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Nitrocellulose

- 5.1.2 Polyamide

- 5.1.3 Polyurethane

- 5.1.4 Acrylic-modified Resins

- 5.1.5 Epoxy and Other Resin Types

- 5.2 By Technology

- 5.2.1 Solvent-based Gravure Inks

- 5.2.2 Water-based Gravure Inks

- 5.2.3 EB/UV-curable Gravure Inks

- 5.3 By Application

- 5.3.1 Flexible Packaging

- 5.3.2 Labels and Wrappers

- 5.3.3 Publication Printing

- 5.3.4 Gift Wrap and Decorative Films

- 5.3.5 Decorative Laminates and Wallpapers

- 5.4 By End-user Industry

- 5.4.1 Food and Beverage

- 5.4.2 Personal Care and Cosmetics

- 5.4.3 Pharmaceuticals and Healthcare

- 5.4.4 Home and Industrial Cleaning

- 5.4.5 Consumer Electronics and Appliances

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Artience Co., Ltd.

- 6.4.2 DIC Corporation

- 6.4.3 Doneck Euroflex

- 6.4.4 Flint Group

- 6.4.5 hubergroup Deutschland GmbH

- 6.4.6 Nazdar Ink Technologies

- 6.4.7 Royal Ink & Resin

- 6.4.8 SAKATA INX CORPORATION

- 6.4.9 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.10 Sun Chemical

- 6.4.11 Superior Printing Inks Co.

- 6.4.12 Toyo Ink SC Holdings

7 Market Opportunities and Future Outlook

- 7.1 Eco-friendly and low-VOC gravure ink chemistries

- 7.2 White-space and Unmet-Need Assessment