|

시장보고서

상품코드

2062233

라이오셀 섬유 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Lyocell Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

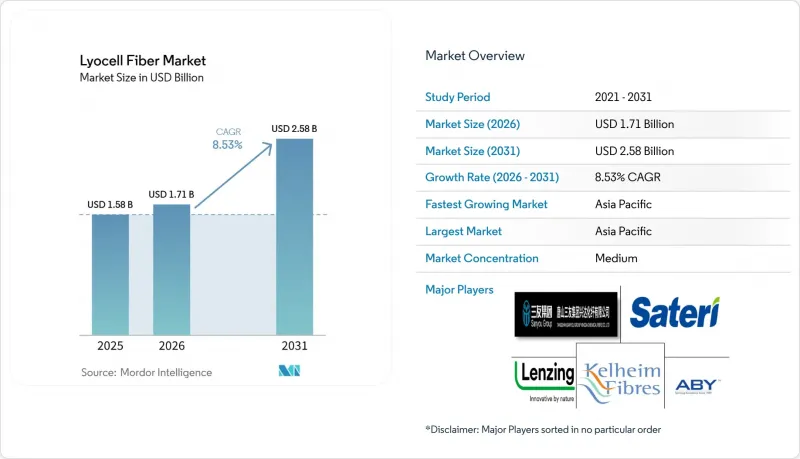

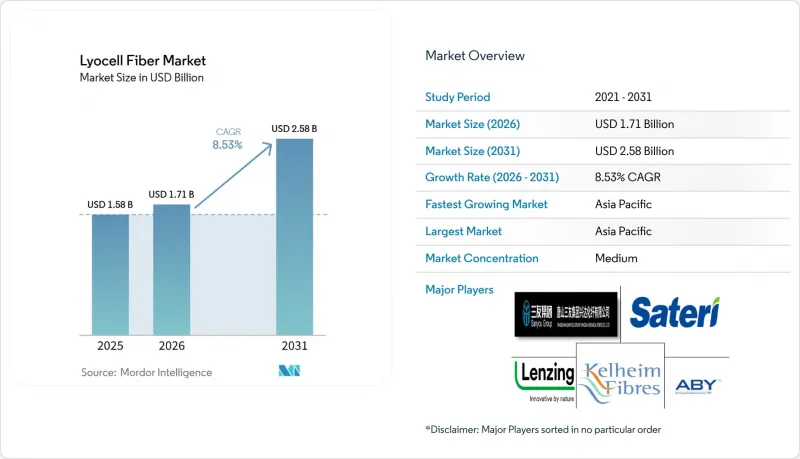

Mordor Intelligence에 의하면, 라이오셀 섬유 시장 규모는 2025년 15억 8,000만 달러에서 2026년에는 17억 1,000만 달러로 확대되어 2031년까지 25억 8,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 8.53%로 성장할 전망입니다.

본 보고서는 섬유 유형(스테이플 섬유 및 필라멘트 섬유), 제조 공정(기존 라이오셀 및 클로즈드 루프/차세대 라이오셀), 용도(의류, 홈 텍스타일 등), 최종 사용자 산업(섬유·패션, 헬스케어·위생용품 등), 지역(아시아태평양, 북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 라이오셀 섬유 시장 동향과 분석

지속 가능하고 생분해성 섬유에 대한 수요 증가

각 브랜드는 비용 문제에 대한 우려보다 생분해성이나 탄소 발자국 감소를 우선시하며, 폴리에스터의 대체 소재로서 라이오셀의 활용을 확대되고 있습니다. 전 세계 소매업체들은 2030년까지 100% 지속 가능한 원단으로의 전환을 약속했으며, 순환 경제 목표를 달성하기 위해 2025년부터 2026년까지 기계적으로 회수된 면 섬유와 버진 라이오셀을 결합한 자체 컬렉션을 출시할 예정입니다. 2025년에 발표된 독립 연구소의 연구에 따르면, 100% 라이오셀 부직포는 호기성 토양 조건에서 35일 이내에 83%가 분해되었으며, 55일 만에 완전한 생분해를 달성했습니다. 이는 셀룰로오스 아세테이트나 재생 폴리에스테르보다 훨씬 빠른 속도입니다. 유럽연합(EU)의 ‘일회용 플라스틱 지침’에 따라, 플라스틱을 사용하지 않은 물티슈에 대한 수요가 꾸준히 증가하고 있습니다. 또한, 수명 주기 분석에 따르면, 기존의 스펀레이스 제조 방식과 비교하여 제조 단계까지의 이산화탄소 배출량이 최대 42% 감소하는 것으로 나타났습니다. 이러한 동향으로 인해 안정적인 수요 기반이 확립되어, 의류 시장의 변동에 따른 판매량에 미치는 영향을 완화하고 있습니다.

의류 및 홈 텍스타일 분야에서의 사용 확대

의류 및 침구류는 여전히 라이오셀의 최대 소비 분야이지만, 수요는 고급 리넨에서 대중적인 데님 및 캐주얼 베이직 제품으로 이동하고 있습니다. 2025년에 도입된 슬래브 효과가 있는 라이오셀 원사를 통해 데님 제조업체들은 뛰어난 흡습·발산성을 유지하면서도 면 특유의 불규칙한 질감을 재현할 수 있게 되었습니다. 바이오 엘라스탄 공급업체와 라이오셀 생산업체간의 제휴를 통해, 2025년 하반기 주요 무역 박람회에서 액티브 스트레치 컬렉션이 공개되었으며, 이는 애슬레저 분야에서의 더 광범위한 채택 가능성을 시사했습니다. 이 호텔 체인은 투숙객의 편안함을 높이기 위해 라이오셀 소재를 많이 사용한 침구를 지정하고 있으며, 내부 감사 결과 침구 업그레이드 후 객실 점유율이 향상된 것으로 보고되었습니다. 편안함, 미적 매력, 그리고 입증된 지속가능성의 조화를 통해 라이오셀은 가격에 민감한 중산층 시장에 성공적으로 진출할 수 있게 되었습니다.

면이나 폴리에스테르에 비해 높은 생산 비용

새로운 라이오셀 생산 시설을 건설하려면 약 3억 달러의 투자가 필요하며, 이는 톤당 비용으로 계산할 때 비스코스의 2배, 폴리에스터의 4배에 해당합니다. 용매 회수 시스템과 고순도 N-메틸모르폴린 N-옥사이드(NMMO)에 대한 수요가 운영 비용을 상승시키고 있습니다. 게다가 유럽의 에너지 가격 급등이 이익률을 압박하여, 2024년에는 특수 섬유 제조업체 한 곳이 파산에 몰렸습니다. 환경에 미치는 외부성을 고려한 탄소 가격 제도가 없는 한, 라이오셀은 가격에 민감한 부문에서 폴리에스터를 대체하는 데 어려움을 겪을 것이며, 단기적인 시장 침투는 제한적일 것입니다.

부문별 분석

2025년 기준으로 스테이플 섬유는 라이오셀 섬유 시장 점유율의 64.84%를 차지했습니다. 이는 주로 면 방적 시스템과의 호환성이 뛰어나며, 의류, 침구, 물티슈 등 다양한 분야에서 폭넓게 사용되기 때문입니다. 필라멘트 섬유는 보풀 방지 성능과 광택이 높이 평가되어 스포츠웨어 및 기능성 섬유 분야에서 수요가 증가하고 있는 만큼, 2031년까지 연평균 성장률(CAGR) 9.02%를 기록하며 스테이플 섬유를 앞지를 것으로 전망됩니다.

스테이플 섬유는 방적 공장이 새로운 설비를 도입하지 않고도 면이나 재생 폴리에스터와 혼방할 수 있기 때문에 매출 1위 자리를 유지할 것으로 예측됩니다. 그러나 연속 필라멘트 라이오셀은 고급 의류 및 자동차 내장재 시장에서 고가 제품군을 차지하고 있으며, 생산량 증가세는 완만하지만 가치의 변화가 예상되고 있습니다. 두 가지 형태 모두를 공급할 수 있는 생산자는 수익성을 극대화하고, 주요 원자재의 상품화 과정에서 발생하는 위험을 줄일 수 있습니다.

2025년에는 기존 라이오셀이 매출 점유율의 78.78%를 차지했으나, 폐쇄형 또는 차세대 라이오셀은 2031년까지 연평균 성장률(CAGR) 9.30%로 성장할 것으로 전망됩니다. 용제 회수율이 99.8% 이상의 시설은 운영 비용을 약 10% 절감하고 검증된 저탄소 실적을 제공하기 때문에 주요 의류 브랜드들로부터 선호받고 있습니다.

현재 화학 재활용 공정에서는 신규 라이오셀 생산 라인에 30%의 재활용 펄프가 포함되어 있으며, 이를 통해 목재 수요가 감소하는 동시에 유럽에서 제안된 재활용 소재 함유율 할당 기준도 충족하고 있습니다. 이러한 기술에 대한 투자를 미루는 생산자들은 구매자들이 추적 가능한 공급망을 갖춘 재활용 소재 제품을 제공하는 공장을 점점 더 선호하게 됨에 따라, 이익률 압박 위험에 직면하게 될 것입니다.

지역별 분석

아시아태평양은 2025년에 45.59%의 점유율을 차지하며 주도적인 위치를 차지하고 있으며, 2031년까지 연평균 성장률(CAGR) 9.67%로 성장할 것으로 전망됩니다. 중국은 연간 60만 톤의 생산 능력을 갖춘 공장을 신설하고 있으며, 이에 따라 중국의 수출은 더욱 증가할 전망입니다. 2024년 국내 가동률은 약 85%로 건실한 가동 상황을 보여주고 있으며, 2025년 1월부터 11월까지의 수출이 48.7% 증가한 것은 유럽의 제사 공장과 비교했을 때의 비용 경쟁력을 여실히 보여주고 있습니다.

유럽에서는 엄격한 에코디자인 규제로 인해 고품질 라이오셀이 소비되고 있지만, 독일의 특수 섬유 제조업체가 2026년 3월까지 문을 닫겠다고 발표함에 따라 생산 능력이 감소하고 있습니다. 이러한 격차로 인해 아시아 공급업체들은 CBAM 감사 요건을 충족하는 저탄소 발자국을 입증할 수 있다면, 수익성이 높은 유럽 시장을 공략할 기회를 얻게 됩니다.

북미는 전 세계 소비량의 약 4분의 1을 차지하지만, 여전히 수입에 대한 의존도가 높은 상황입니다. 2026년 7월에 시행될 캘리포니아주의 생산자 책임법 및 주 차원의 화학물질 규제로 인해 소매업체들은 생분해성 섬유로의 전환을 촉진하고 있으며, 국내 공급이 제한적임에도 불구하고 안정적인 수요 증가를 뒷받침하고 있습니다.

남미, 중동 및 아프리카는 여전히 규모는 작지만 두 자릿수 성장 가능성을 지니고 있습니다. 브라질의 유칼립투스 원료라는 강점은 향후 하류 부문 투자를 유치할 가능성이 있는 반면, 튀르키예의 제사 공장은 유럽의 지속가능성 요건을 충족하기 위해 수출용 의류 제품에 라이오셀을 도입하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the lyocell fiber market size is expected to increase from USD 1.58 billion in 2025 to USD 1.71 billion in 2026 and reach USD 2.58 billion by 2031, growing at a CAGR of 8.53% over 2026-2031.

This report is Segmented by Fiber Type (Staple Fibers and Filament Fibers), Process Type (Conventional Lyocell and Closed-loop/Next-gen Lyocell), Application (Apparel, Home Textiles, and More), End-User Industry (Textile and Fashion, Healthcare and Hygiene, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Lyocell Fiber Market Trends and Insights

Growing Demand for Sustainable and Biodegradable Fibers

Brands are increasingly promoting lyocell as a substitute for polyester, prioritizing its biodegradability and lower carbon footprint over cost concerns. Global retailers have pledged to transition to 100% preferred fibers by 2030, with in-house collections launched in 2025-2026, incorporating mechanically recovered cotton waste with virgin lyocell to meet circularity objectives. Independent laboratory studies published in 2025 revealed that 100% lyocell nonwovens disintegrated 83% within 35 days under aerobic soil conditions, achieving complete biodegradation in 55 days, significantly faster than cellulose acetate and recycled polyester. The European Union's Single-Use Plastics Directive is driving consistent demand for plastic-free wipes, while life-cycle analyses show up to 42% lower cradle-to-gate CO2 emissions compared to traditional spunlace formulations. These developments establish a stable demand base, protecting volumes from fluctuations in the apparel market.

Increasing Usage in Apparel and Home Textiles

Apparel and bedding remain the largest consumers of lyocell, but demand is shifting from premium linens to mass-market denim and casual basics. A slub-effect lyocell yarn, introduced in 2025, enables denim manufacturers to replicate the irregular textures associated with cotton while maintaining superior moisture management. Collaborations between bio-based elastane suppliers and lyocell producers resulted in active-stretch collections showcased at major trade shows in late 2025, signaling broader adoption in athleisure. Hospitality chains are specifying lyocell-rich sheets to enhance guest comfort, with internal audits reporting improved occupancy rates following bedding upgrades. The combination of comfort, aesthetics, and verified sustainability is enabling lyocell to penetrate price-sensitive mid-tier categories.

Higher Production Costs vs. Cotton and Polyester

Establishing a greenfield lyocell facility requires an investment of approximately USD 300 million, which is double the cost of viscose and four times that of polyester on a per-ton basis. The need for solvent recovery systems and high-purity N-methylmorpholine N-oxide (NMMO) increases operational expenses. Additionally, energy price spikes in Europe eroded margins, leading to the insolvency of a specialty fiber mill in 2024. Without carbon pricing to account for environmental externalities, lyocell faces challenges in displacing polyester in price-sensitive segments, limiting its short-term market penetration.

Other drivers and restraints analyzed in the detailed report include:

- High Moisture-Absorption and Strength Enabling Performance Wear

- Carbon-Border Taxes Accelerating Low-Impact Fibers

- Complex Chemical Recovery and Manufacturing Process

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Staple fibers accounted for 64.84% of the lyocell fiber market share in 2025, primarily due to their compatibility with cotton-spinning systems and widespread application in apparel, bed linens, and wipes. Filament fibers are projected to grow at a 9.02% CAGR through 2031, surpassing staple fibers in growth rate, as they are valued in sportswear and technical textiles for their pilling resistance and sheen.

Staple fibers are expected to maintain revenue leadership as mills can blend them with cotton or recycled polyester without requiring new equipment. However, continuous filament lyocell commands higher prices in luxury apparel and automotive interiors, indicating a shift in value even as tonnage growth remains slower. Producers capable of supplying both formats can maximize profitability and mitigate risks associated with commoditization in staple grades.

Conventional lyocell held a 78.78% revenue share in 2025, while closed-loop or next-generation lyocell is anticipated to grow at a 9.30% CAGR through 2031. Facilities recovering over 99.8% of solvents reduce operating costs by approximately 10% and provide verified low-carbon credentials, making them preferred by leading apparel brands.

Chemical recycling now integrates 30% recycled pulp into new lyocell production lines, reducing wood demand and aligning with proposed recycled-content quotas in Europe. Producers delaying investment in these technologies risk margin pressures as buyers increasingly prefer mills offering recycled-content products with traceable supply chains.

Geography Analysis

Asia-Pacific dominated with 45.59% share in 2025 and is forecast to rise at a 9.67% CAGR through 2031. China is adding a 600,000 tpa plant, which will further boost its exports. Domestic operating rates of approximately 85% in 2024 indicate healthy utilization, while export growth of 48.7% between January and November 2025 highlights cost competitiveness compared to European mills.

Europe consumes premium lyocell because of strict eco-design rules, but is losing production capacity after a German specialty mill announced closure by March 2026. The gap invites Asian suppliers to capture higher-margin European demand, provided they document low carbon footprints to satisfy CBAM audits.

North America represents roughly one-quarter of global consumption yet relies heavily on imports. California's producer-responsibility law, effective July 2026, and state-level chemical restrictions are encouraging retailers to shift toward biodegradable fibers, supporting stable demand growth despite limited domestic supply.

South America and the Middle-East and Africa remain small but show double-digit growth potential. Brazil's eucalyptus feedstock advantage could attract future downstream investments, while Turkish mills are incorporating lyocell into export-oriented apparel to meet European sustainability requirements.

- Acelon Chemicals & Fiber Corp.

- Aditya Birla Yarn

- Baoding Swan Fiber Co., Ltd.

- China Populus Textile Ltd. (CPT)

- Guangxi Sun Paper Co., Ltd.

- Kelheim Fibres GmbH

- Lenzing AG

- Sappi Ltd.

- Sateri

- SMARTFIBER AG

- Tangshan Sanyou Xingda Chemical Fiber Co., Ltd.

- Xinxiang Chemical Fiber Co., Ltd.

- Yibin Grace Group Co., Ltd.

- Zhejiang Fulida Fibre Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for sustainable and biodegradable fibers

- 4.2.2 Increasing usage in apparel and home textiles

- 4.2.3 Expansion of eco-friendly collections by fashion brands

- 4.2.4 High moisture-absorption and strength enabling performance wear

- 4.2.5 Carbon-border taxes accelerating low-impact fibers

- 4.2.6 Textile-to-textile chemical recycling streams favoring lyocell

- 4.3 Market Restraints

- 4.3.1 Higher production costs vs. cotton and polyester

- 4.3.2 Complex chemical recovery and manufacturing process

- 4.3.3 Competition from other regenerated cellulose fibers

- 4.3.4 Volatile dissolving-pulp supply due to biorefinery demand

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Fiber Type

- 5.1.1 Staple Fibers

- 5.1.2 Filament Fibers

- 5.2 By Process Type

- 5.2.1 Conventional Lyocell

- 5.2.2 Closed-loop/Next-gen Lyocell

- 5.3 By Application

- 5.3.1 Apparel

- 5.3.2 Home Textiles

- 5.3.3 Medical and Hygiene Products

- 5.3.4 Industrial

- 5.3.5 Other Applications (Packaging, Personal Care)

- 5.4 By End-user Industry

- 5.4.1 Textile and Fashion

- 5.4.2 Healthcare and Hygiene

- 5.4.3 Automotive and Transportation

- 5.4.4 Home Furnishing

- 5.4.5 Industrial and Technical Textiles

- 5.4.6 Other End-user Industries (Retail, E-commerce)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Acelon Chemicals & Fiber Corp.

- 6.4.2 Aditya Birla Yarn

- 6.4.3 Baoding Swan Fiber Co., Ltd.

- 6.4.4 China Populus Textile Ltd. (CPT)

- 6.4.5 Guangxi Sun Paper Co., Ltd.

- 6.4.6 Kelheim Fibres GmbH

- 6.4.7 Lenzing AG

- 6.4.8 Sappi Ltd.

- 6.4.9 Sateri

- 6.4.10 SMARTFIBER AG

- 6.4.11 Tangshan Sanyou Xingda Chemical Fiber Co., Ltd.

- 6.4.12 Xinxiang Chemical Fiber Co., Ltd.

- 6.4.13 Yibin Grace Group Co., Ltd.

- 6.4.14 Zhejiang Fulida Fibre Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Sustainable hygiene and personal-care products growth

- 7.3 Development of lyocell-blended technical and smart fabrics