|

시장보고서

상품코드

2062237

프레임 그래버 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Frame Grabber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

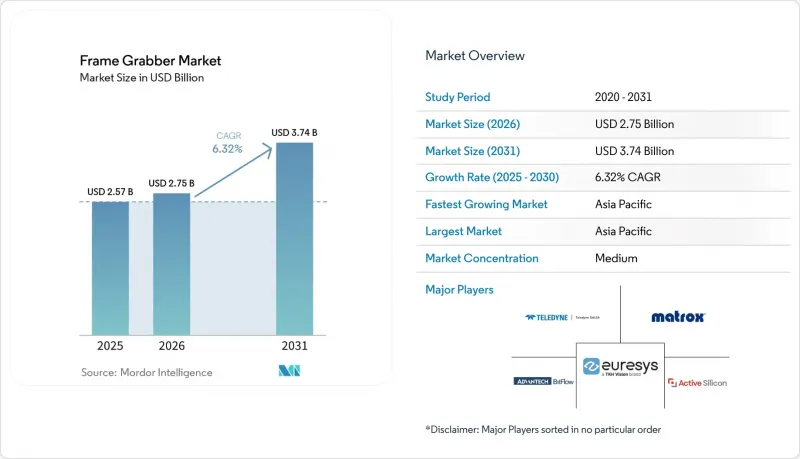

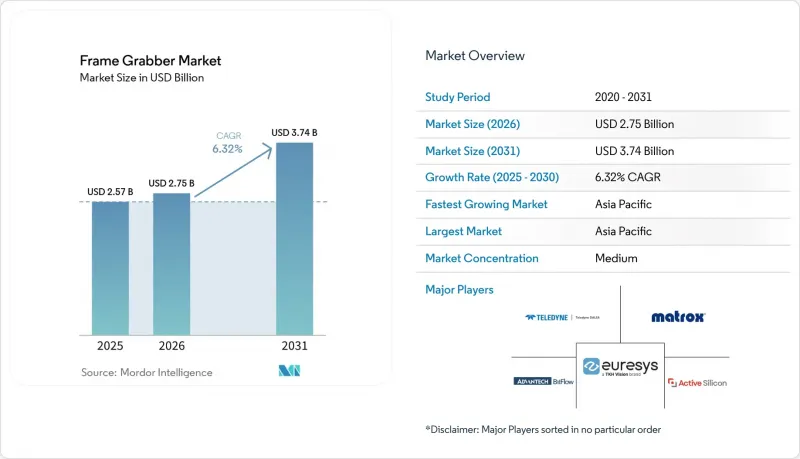

Mordor Intelligence에 의하면, 프레임 그래버 시장 규모는 2025년 25억 7,000만 달러에서 2026년에는 27억 5,000만 달러로 확대되어 2031년까지 37억 4,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 6.32%로 성장할 전망입니다.

본 보고서는 인터페이스 유형(Camera Link, Coaxpress, Gigavision 등), 호스트 버스 및 폼 팩터(PCIe 및 PCI 카드, USB 외부 캡처 장치 등), 프레임 레이트 지원 능력(최대 60 FPS, 60-120 FPS 등), 응용 산업(산업 및 제조, 일렉트로믹스 및 반도체 검사 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 프레임 그래버 시장 동향 및 분석

생산 라인에서 5,000만 화소 이상의 이미지 센서 채택 확대

캐논의 4억 1,000만 화소 CMOS 센서나 소니의 IMX927(1억 500만 화소) 센서가 초당 100프레임으로 작동하는 사례는 해상도 향상을 상징하며, 이에 따라 생산 라인 통합 업체들은 기존의 Camera Link Base나 GigE Vision 인터페이스를 CoaXPress 2.0이나 Camera Link HS로 교체해야 할 필요에 직면해 있습니다. 100fps로 촬영된 1억 500만 화소 이미지는 초당 약 10.5기가바이트의 원시 베이어 데이터를 생성하며, 이는 표준 GigE Vision의 초당 1기가비트라는 상한선을 훨씬 뛰어넘는 수치입니다. 이러한 대역폭 불일치로 인해 제조업체들은 총 처리량이 초당 10기가바이트를 초과하는 프레임 그래버를 도입할 수밖에 없게 되었으며, 이는 PCIe Gen4 카드 및 CoaXPress 멀티링크 구성에 대한 수요를 견인하고 있습니다. STMicroelectronics의 500만 화소 하이브리드 세계 롤링 셔터 센서는 처리 도중 세계 셔터 모드와 롤링 셔터 모드를 전환할 수 있는 유연한 프레임 그래버 아키텍처가 필요한, 특정 용도 맞춤형 이미징으로의 추세를 더욱 여실히 보여주고 있습니다. 5,000만 화소를 넘는 센서로 전환되는 추세는 반도체 웨이퍼 검사, 플랫 패널 디스플레이 결함 감지, 자동차 바디-인-화이트 측정 분야에서 가장 두드러지며, 이러한 분야에서는 서브미크론 해상도가 수율 향상 및 보증 비용 절감과 직결됩니다.

실시간 이미지 처리가 필요한 인더스트리 4.0의 확산

인더스트리 4.0 아키텍처에서는 이미지 획득부터 액추에이터의 응답까지의 지연 시간을 10밀리초 미만으로 억제하는 폐루프 제어가 필수적이며, 이러한 요구 사항으로 인해 범용 CPU에서 실행되는 소프트웨어 기반 파이프라인보다 FPGA 기반의 전처리 기능을 갖춘 프레임 그래버가 더 유리합니다. Gidel사의 Proc1C10N 프레임 그래버는 초당 143테라오퍼레이션의 INT8 추론 성능을 캡처 카드에 직접 통합하여, 픽셀 데이터를 호스트 GPU로 왕복 전송할 필요 없이 실시간 결함 분류를 가능하게 합니다. 이러한 온보드 인텔리전스를 통해 멀티 카메라 셀 내의 네트워크 혼잡이 완화되어, 다른 워크로드가 호스트 리소스를 경쟁하고 있는 경우에도 결정적인 지연 시간이 보장됩니다. 2023년 11월 Basler가 Siemens와 체결한 파트너십을 통해 pylon SDK가 Siemens의 Industrial Edge 디바이스에 통합되었습니다. 이를 통해 공장 운영자는 생산 라인 전체에 걸쳐 수평적으로 확장 가능한 컨테이너화된 마이크로서비스 형태로 비전 용도를 배포할 수 있게 되었습니다. 시간 의존형 네트워크 프로토콜, 머신 간 통신을 위한 OPC UA, 그리고 결정론적 프레임 그래버의 융합을 통해 이미징은 단순한 사후 검사 단계가 아닌, 산업용 IoT 스택의 핵심 구성 요소로서의 입지를 확고히 하고 있습니다.

디스크리트형 프레임 그래버를 대체하는 스마트 카메라

Allied Vision의 스마트 카메라 ‘Alecs’는 초당 100테라오퍼레이션의 AI 성능을 갖춘 NVIDIA Jetson Orin NX 모듈을 탑재하여, 별도의 프레임 그래버나 호스트 PC 없이도 결함 분류, 광학 문자 인식, 치수 측정을 위한 온디바이스 추론을 가능하게 합니다. 마찬가지로, Teledyne사의 BOA3 AI 카메라도 에지 측에서 이미지를 처리하는 신경망 가속기를 내장하고 있어, GigE 또는 USB3를 통해 메타데이터와 경보 신호만 전송함으로써 네트워크 대역폭을 두 자릿수 수준으로 줄여줍니다. 이러한 아키텍처 전환은 카메라 한 대만으로도 충분하고, 설치 공간이 제한적이며, 전용 프레임 그래버나 호스트 PC의 비용을 감당하기 어려운 용도에 적합합니다. 그러나 스마트 카메라는 다중 카메라 동기화 시나리오, 수술용 로봇과 같이 결정론적 지연 시간이 요구되는 용도, 그리고 추적성을 위해 비압축 픽셀 데이터를 보관해야 하는 고처리량 검사 셀에서는 어려움을 겪고 있습니다. 한편, 프레임 그래버 생태계는 수십 대의 카메라에 걸쳐 서브 마이크로초 수준의 지터를 갖는 하드웨어 트리거를 통한 캡처, OS 스케줄링 지연을 회피하는 FPGA 기반 실시간 처리, 그리고 추론 파이프라인을 가속화하기 위한 GPU 메모리에 대한 직접 액세스를 제공함으로써, 이러한 틈새 시장에서 여전히 우위를 점하고 있습니다.

부문별 분석

인터페이스형 솔루션 분야의 프레임 그래버 시장 규모를 살펴보면, 2025년에는 CoaXPress가 매출 점유율의 38.19%를 차지해, 연평균 성장률(CAGR) 6.97%는 Camera Link나 GigE와 같은 대체 솔루션을 상회하고 있어, 2031년까지 점유율이 꾸준히 상승할 것으로 전망됩니다. CoaXPress는 링크당 12.5Gbps의 전송 속도와 전원 공급 기능을 결합하여, 이를 통해 케이블 하네스를 간소화하고 전송 거리를 연장할 수 있습니다. 이는 반도체 웨이퍼 검사나 자동차 도장 부스에서 매우 중요한 특성입니다. Camera Link는 항공우주 분야와 의료용 X선 분야에서 확고한 입지를 다져왔기 때문에 기존 설비의 개조 프로젝트에서는 여전히 유용하지만, 신규 도입의 경우 CoaXPress 2.0이나 Camera Link HS가 지닌 미래 대응 능력과 확장성이 더 선호되고 있습니다. GigE Vision은 비용 면에서 우수하지만, 패킷 손실이나 CPU 오버헤드가 정확한 검사를 방해하기 때문에 분산형 또는 비용 효율성을 중시하는 작업으로 그 용도가 제한됩니다.

미래를 내다본 수요는 링크당 25Gbps를 목표로 하는 CoaXPress 3.0 규격 초안에 집중되어 있으며, 이를 통해 플랫 패널 디스플레이 측정 분야에서 단일 케이블을 통한 2억 화소 카메라 구현의 길이 열리게 됩니다. Camera Link HS는 방사선 내성 부품이 요구되는 분야에서 여전히 특정 사용자층을 유지하고 있지만, 엔지니어링 분야에서의 관심은 CoaXPress로 옮겨가고 있습니다. USB3 Vision은 그 보급률과 플러그 앤 플레이의 편의성 덕분에 휴대용 스캐너나 실험실용 장비 분야에서 확고한 입지를 유지하고 있지만, 5Gbps라는 전송 속도 한계로 인해 적절한 프레임 속도를 유지하려면 20MP 미만의 해상도로 제한됩니다. 그 결과, CoaXPress는 프레임 그래버 시장의 선두주자로 자리매김하며, 성능에 대한 기대와 경쟁사들의 로드맵을 모두 정의하게 될 것입니다.

PCIe 및 PCI 카드는 2025년 매출의 46.52%를 차지하고 있으며, 이는 기존 비전 아키텍처에서 타워형 및 랙 마운트형 워크스테이션이 주류를 이루었음을 보여줍니다. 소형 엣지 어플라이언스의 부상으로 M.2 및 Thunderbolt 모듈이 주목받고 있으며, 2031년까지 연평균 성장률(CAGR) 7.03%를 나타낼 것으로 전망됩니다. M.2 모듈은 신용카드보다 작은 크기로 PCIe 레인에 직접 연결되며, 로봇 팔의 뒷면이나 패널 PC 내부에 장착할 수 있는 팬리스 설계를 구현합니다. Thunderbolt 4는 40Gbps의 총 대역폭, 데이지 체인 연결 및 핫 플러그 기능을 제공하며, 이러한 기능들은 휴대용 검사 장비의 설치 비용을 절감합니다.

PC/104 및 CompactPCI 규격의 임베디드 보드는 충격 및 진동에 대한 요구 사항이 일반 상용 PC의 허용 범위를 초과하는 항공우주 및 방위 분야에서 여전히 사용되고 있습니다. USB 외부 캡처 장치는 카메라 1대로도 충분한 경우의 초급 사용자 요구 사항을 충족하지만, 호스트 USB 컨트롤러에 의존하기 때문에 지연 시간이 변동될 수 있어 정밀한 검사에는 적합하지 않습니다. 고밀도 라인에서는 여전히 4개 이상의 카메라 링크에 걸쳐 FPGA 리소스를 통합하는 풀 하이트 PCIe 카드에 의존하고 있으며, 이는 프레임 그래버 시장 내 수요 곡선의 양극화를 여실히 보여주고 있습니다. 그 결과, 엣지 AI 도입의 확대에 힘입어 폼 팩터의 전환은 급격한 것이 아니라 점진적으로 이루어지고 있습니다.

지역별 분석

아시아태평양은 2025년 전 세계 프레임 그래버 시장 매출의 32.43%를 차지해, 2031년까지 연평균 성장률(CAGR) 7.88%를 나타낼 것으로 전망됩니다. 중국의 반도체 국산화 정책, 한국의 메모리 패키징 분야에서의 리더십, 그리고 인도의 전자기기 생산 연계형 인센티브가 맞물려 이 지역의 성장세를 뒷받침하고 있습니다. 바슬러(Basler)가 알파 테크시스 오토메이션 인디아(Alpha TechSys Automation India)의 지분 76%를 인수한 사례에서 볼 수 있듯이, 유럽과 미국공급업체들은 민첩한 현지 경쟁사들에 뒤처지지 않기 위해 현지 사업 기반을 강화하고 있습니다. 또한, 일본의 노동력 고령화와 자동화의 필요성은 정확한 이미지 처리가 필요한 공장 개조 시 자동화 시스템 도입을 마찬가지로 촉진하고 있습니다.

북미와 유럽은 성숙한 산업 기반, 엄격한 자동차 품질 기준, 그리고 항공우주 및 방위 분야의 견조한 수요에 힘입어 2025년 매출의 약 절반을 차지했습니다. 미국에서는 MIL-STD 인증 프로그램을 위해 견고한 캡처 카드의 도입이 계속해서 요구되고 있는 반면, 독일의 자동차 1차 공급업체들은 CoaXPress 2.0 링크로 연결된 멀티 카메라 검사 셀을 선호하고 있습니다. FDA와 IEC 기준이 통합됨에 따라 의료 영상 분야 공급업체들의 규정 준수 대응은 효율화되고 있지만, 현재 진행 중인 IEC 60601-1 제4판 개정으로 인해 사이버 보안 및 소프트웨어 수명 주기 기준이 강화됨에 따라, 확립된 품질 관리 시스템(QMS) 인프라를 갖춘 기존 기업들에게 유리하게 작용할 것입니다.

남미, 중동 및 아프리카의 합계는 2025년 매출의 15% 미만에 그쳤습니다. 브라질의 자동차 산업 거점이 가장 큰 점유율을 차지하고 있지만, 환율 변동과 설비 투자 제약으로 인해 첨단 프레임 그래버의 주문 추세가 주춤하고 있습니다. 중동의 석유 및 가스 복합 시설에서는 파이프라인 점검 및 부품 검사에 머신 비전이 도입되고 있지만, 그 도입 규모는 아시아태평양의 반도체 공장과 비교하면 여전히 소규모입니다. 아프리카의 광산 사업에서는 즉각적인 투자 수익률(ROI)을 기대할 수 있는 비전 기반 광석 선별 기술이 도입되고 있지만, 인프라와 기술력의 부족으로 인해 광범위한 확산은 더딘 상황입니다. 이러한 지역 전반에 걸쳐 잠재적 수요를 발굴하기 위해서는 공급업체의 자금 조달 모델과 긴밀한 통합 파트너십이 필요합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the frame grabber market size is expected to increase from USD 2.57 billion in 2025 to USD 2.75 billion in 2026 and reach USD 3.74 billion by 2031, growing at a CAGR of 6.32% over 2026-2031.

This report is Segmented by Interface Type (Camera Link, Coaxpress, Gige Vision, and More), Host-Bus and Form Factor (PCIe and PCI Cards, USB External Capture Units, and More), Frame-Rate Capability (Up To 60 FPS, 60-120 FPS, and More), Application Industry (Industrial and Manufacturing, Electronics and Semiconductor Inspection, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Frame Grabber Market Trends and Insights

Rising Adoption of >50 MP Image Sensors on Production Lines

Canon's 410-megapixel CMOS sensor and Sony's IMX927 105-megapixel sensor running at 100 frames per second exemplify the resolution escalation that forces production-line integrators to replace legacy Camera Link Base or GigE Vision interfaces with CoaXPress 2.0 or Camera Link HS. A single 105-megapixel frame at 100 frames per second generates approximately 10.5 gigabytes per second of raw Bayer data, exceeding the 1 gigabit per second ceiling of standard GigE Vision by an order of magnitude. This bandwidth mismatch compels manufacturers to deploy frame grabbers with aggregate throughput beyond 10 gigabytes per second, driving demand for PCIe Gen4 cards and CoaXPress multi-link configurations. STMicroelectronics' 5-megapixel hybrid global-rolling-shutter sensor further illustrates the trend toward application-specific imaging that requires flexible frame-grabber architectures capable of switching between global-shutter and rolling-shutter modes midstream. The shift to >50-megapixel sensors is most pronounced in semiconductor wafer inspection, flat-panel-display defect detection, and automotive body-in-white measurement, where sub-micron resolution directly correlates with yield improvement and warranty-cost reduction.

Industry 4.0 Roll-Outs Requiring Real-Time Imaging

Industry 4.0 architectures mandate closed-loop control with sub-10-millisecond latency between image acquisition and actuator response, a requirement that favors frame grabbers with FPGA-based pre-processing over software-only pipelines running on general-purpose CPUs. Gidel's Proc1C10N frame grabber integrates 143 tera-operations per second of INT8 inference capacity directly on the capture card, enabling real-time defect classification without round-tripping pixel data to a host GPU. This on-board intelligence reduces network congestion in multi-camera cells and ensures deterministic latency even when other workloads contest host resources. Basler's November 2023 partnership with Siemens embedded the pylon SDK into Siemens Industrial Edge devices, allowing factory operators to deploy vision applications as containerized microservices that scale horizontally across production lines. The convergence of time-sensitive networking protocols, OPC UA for machine-to-machine communication, and deterministic frame grabbers positions imaging as a first-class citizen in the industrial Internet of Things stack, rather than a bolt-on inspection step.

Smart Cameras Replacing Discrete Frame Grabbers

Allied Vision's Alecs smart camera integrates an NVIDIA Jetson Orin NX module with 100 tera-operations per second of AI performance, enabling on-device inference for defect classification, optical character recognition, and dimensional measurement without a separate frame grabber or host PC. Teledyne's BOA3 AI camera similarly embeds a neural network accelerator that processes images at the edge, transmitting only metadata or alarm signals over GigE or USB3, thereby reducing network bandwidth by two orders of magnitude. This architectural shift appeals to applications where a single camera suffices, installation space is constrained, and the cost of a dedicated frame grabber and host PC cannot be justified. However, smart cameras struggle in multi-camera synchronization scenarios, deterministic-latency applications such as surgical robotics, and high-throughput inspection cells where uncompressed pixel data must be archived for traceability. The frame-grabber ecosystem retains an advantage in these niches by offering hardware-triggered acquisition across dozens of cameras with sub-microsecond jitter, FPGA-based real-time processing that bypasses operating-system scheduling latency, and direct GPU memory access for accelerated inference pipelines.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of CoaXPress 2.0 and PCIe 4.0 Bandwidth

- Growth of Automated Optical Inspection in Electronics

- High Up-Front Cost of CoaXPress Cards for SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The frame grabber market size for interface-type solutions shows CoaXPress occupying 38.19% revenue share in 2025, a share projected to climb steadily through 2031 as its 6.97% CAGR outpaces that of Camera Link and GigE alternatives. CoaXPress fusion of 12.5 Gbps per link and power delivery translates into simplified cable harnesses and extended reach, attributes crucial in semiconductor wafer inspection and automotive paint booths. Camera Link's entrenched base in aerospace and medical X-ray keeps it relevant for retrofit projects, yet new installations prefer the headroom and future-proofing of CoaXPress 2.0 and Camera Link HS. GigE Vision, while cost-friendly, suffers from packet loss and CPU overhead that undermine deterministic inspection, relegating it to distributed or cost-sensitive tasks.

Forward-looking demand centers on the draft CoaXPress 3.0 standard, which targets 25 Gbps per link, clearing the way for single-cable 200-MP cameras in flat-panel display metrology. Camera Link HS retains a specialized following where radiation-hard components are required, but engineering mindshare is pivoting toward CoaXPress. USB3 Vision maintains a foothold in handheld scanners and laboratory instruments thanks to its ubiquity and plug-and-play elegance, yet its 5 Gbps ceiling limits it to resolutions under 20 MP at moderate frame rates. Consequently, CoaXPress will remain the flagship of the frame grabber market, defining both performance expectations and competitive roadmaps.

PCIe and PCI cards supplied 46.52% of 2025 revenue, a testament to the dominance of tower and rackmount workstations in legacy vision architectures. The rise of compact edge appliances now lifts M.2 and Thunderbolt modules, forecast to log a 7.03% CAGR through 2031. M.2 modules mate directly to PCIe lanes in a footprint smaller than a credit card, enabling fanless designs that mount behind robot arms or inside panel PCs. Thunderbolt 4 provides 40 Gbps aggregate bandwidth, daisy-chaining, and hot-plug convenience, features that improve installation economics for portable inspection rigs.

Embedded boards in PC/104 and CompactPCI formats persist in aerospace and defense, where shock and vibration requirements exceed commercial PC tolerances. USB external capture units meet entry-level needs when a single camera suffices, but their reliance on host USB controllers introduces latency variability, disqualifying them for deterministic inspection. High-density lines still lean on full-height PCIe cards that pool FPGA resources across four or more camera links, underscoring a bifurcated demand curve inside the frame grabber market. The outcome is a gradual, not abrupt, form-factor transition driven by the rise of edge AI deployments.

Geography Analysis

Asia-Pacific accounted for 32.43% of the global frame grabber market revenue in 2025 and is projected to register a 7.88% CAGR through 2031. China's semiconductor localization mandates, South Korea's leadership in memory packaging, and India's production-linked incentives for electronics combine to anchor regional momentum. Western vendors, as illustrated by Basler's 76% purchase of Alpha TechSys Automation India, are deepening local footprints to keep pace with agile domestic competitors. Japan's aging workforce and the imperative of automation likewise propel adoption in factory retrofits that demand deterministic imaging.

North America and Europe jointly contributed roughly half of 2025 revenue, supported by mature industrial bases, stringent automotive quality standards, and robust demand in aerospace and defense. The United States continues to specify ruggedized capture cards for MIL-STD-qualified programs, while Germany's automotive tier-ones favor multi-camera inspection cells wired through CoaXPress 2.0 links. Harmonized FDA and IEC pathways streamline vendor compliance in medical imaging, yet the pending IEC 60601-1 Edition 4 upgrade will raise cybersecurity and software lifecycle bars, tilting the advantage toward incumbents with established QMS infrastructures.

South America, the Middle East, and Africa together generated less than 15% of 2025 revenue. Brazil's automotive hubs offer the largest parcel, but currency swings and capex constraints temper ordering patterns for advanced frame grabbers. Middle Eastern oil and gas complexes deploy machine vision for pipeline inspection and component verification, yet volumes remain modest compared to those in Asia-Pacific fabs. African mining operations adopt vision-based ore sorting where ROI is immediate, though infrastructure and skills gaps slow pervasive rollout. Collectively, these regions require vendor financing models and close integration partnerships to unlock latent demand.

- Teledyne DALSA Inc.

- Matrox Electronic Systems Ltd.

- BitFlow, Inc.

- Euresys SA

- Active Silicon Ltd.

- KAYA Instruments Ltd.

- Pleora Technologies Inc.

- Advantech Co., Ltd.

- Gidel Ltd.

- Sensoray Company, Inc.

- Epix, Inc.

- Silicon Software GmbH

- Basler AG

- National Instruments Corporation

- Axiomtek Co., Ltd.

- dPict Imaging, Inc.

- Imperx, Inc.

- Raptor Photonics Ltd.

- ADLINK Technology Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of >50 MP Image Sensors on Production Lines

- 4.2.2 Industry 4.0 Roll-Outs Requiring Real-Time Imaging

- 4.2.3 Expansion of CoaXPress 2.0 and PCIe 4.0 Bandwidth

- 4.2.4 Growth of Automated Optical Inspection in Electronics

- 4.2.5 On-Board AI Pre-Processing Reducing Host CPU Load

- 4.2.6 Emerging Demand for Deterministic Video in Surgical Robots

- 4.3 Market Restraints

- 4.3.1 Smart Cameras Replacing Discrete Frame Grabbers

- 4.3.2 High Up-Front Cost of CoaXPress Cards for SMEs

- 4.3.3 Thermal-Management Issues Beyond 25 Gbps per Channel (Under-the-Radar)

- 4.3.4 FPGA Supply-Chain Tightness Delaying Product Launches (Under-the-Radar)

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Interface Type

- 5.1.1 Camera Link

- 5.1.2 CoaXPress

- 5.1.3 GigE Vision

- 5.1.4 USB3 Vision

- 5.1.5 LVDS and Parallel Digital

- 5.2 By Host-Bus / Form Factor

- 5.2.1 PCIe / PCI Cards

- 5.2.2 USB External Capture Units

- 5.2.3 Embedded Boards (PC/104, cPCI)

- 5.2.4 M.2 / Thunderbolt Modules

- 5.3 By Frame-Rate Capability

- 5.3.1 Up to 60 FPS

- 5.3.2 60 - 120 FPS

- 5.3.3 Above 120 FPS

- 5.4 By Application Industry

- 5.4.1 Industrial and Manufacturing

- 5.4.2 Electronics and Semiconductor Inspection

- 5.4.3 Medical and Life Sciences

- 5.4.4 Security and Surveillance

- 5.4.5 Aerospace and Defense

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Russia

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Teledyne DALSA Inc.

- 6.4.2 Matrox Electronic Systems Ltd.

- 6.4.3 BitFlow, Inc.

- 6.4.4 Euresys SA

- 6.4.5 Active Silicon Ltd.

- 6.4.6 KAYA Instruments Ltd.

- 6.4.7 Pleora Technologies Inc.

- 6.4.8 Advantech Co., Ltd.

- 6.4.9 Gidel Ltd.

- 6.4.10 Sensoray Company, Inc.

- 6.4.11 Epix, Inc.

- 6.4.12 Silicon Software GmbH

- 6.4.13 Basler AG

- 6.4.14 National Instruments Corporation

- 6.4.15 Axiomtek Co., Ltd.

- 6.4.16 dPict Imaging, Inc.

- 6.4.17 Imperx, Inc.

- 6.4.18 Raptor Photonics Ltd.

- 6.4.19 ADLINK Technology Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment