|

시장보고서

상품코드

2062252

폴리카복실산 에테르 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Polycarboxylate Ether - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

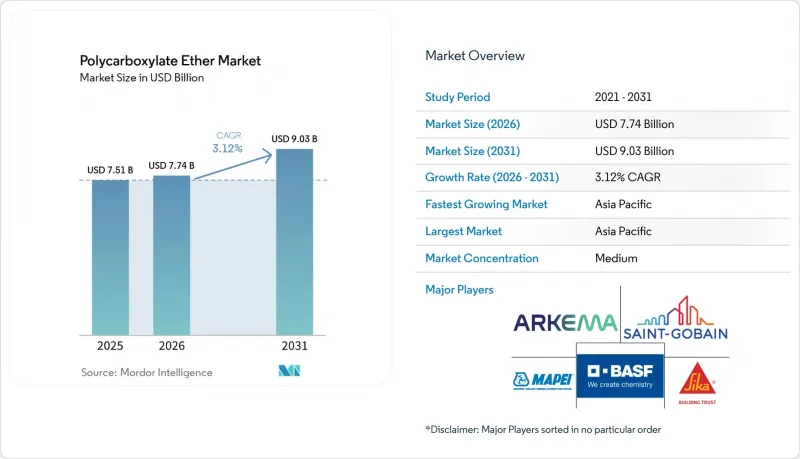

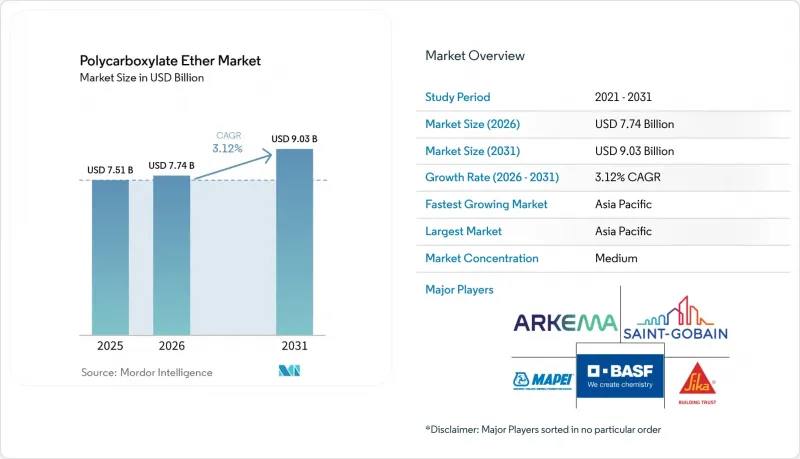

Mordor Intelligence에 의하면, 폴리카복실산 에테르 시장 규모는 2025년 75억 1,000만 달러로 평가되었습니다. 2026년 77억 4,000만 달러에서 2031년까지 90억 3,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR은 3.12%를 나타낼 것으로 예측됩니다.

본 보고서는 유형별(MPEG 계열, TPEG 계열, 기타), 형태별(액체, 분말), 용도별(레디믹스트 콘크리트, 고성능 콘크리트, 기타), 최종 사용자 산업별(주택 건설, 상업용 건설, 기타), 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 폴리카복실산 에테르 시장 동향 및 분석

아시아·태평양 및 아프리카의 급속한 인프라 투자

남아시아, 동남아시아, 아프리카는 2026년부터 2028년까지 예정된 교통 회랑, 전력망, 수자원 프로젝트에 총 2,500억 달러 이상을 배정했습니다. 아시아개발은행만 해도 그 기간 동안 986억 달러를 배정했습니다. 자금은 교량, 고속도로, 지하철 시스템에 사용되는 콘크리트에 투입되고 있으며, 장거리 펌프 운송 시 120분 동안 슬럼프를 유지할 수 있기 때문에 TPEG 기반 화학제품이 선호되고 있습니다. 아프리카의 연간 약 1,700억 달러에 달하는 인프라 격차는 수송량을 70% 줄여주는 분말형 혼합제에 대한 수요를 촉진하고 있으며, 이는 내륙 운송 경로에서 결정적인 비용 우위를 가져다줍니다. 이러한 자본 투자 프로그램은 2031년까지 폴리카복실산 에테르 시장을 추정 연평균 성장률(CAGR) 기준으로 1.2포인트 끌어올릴 것으로 전망됩니다.

친환경 건축 기준에 따른 물-시멘트 비율 규제 강화

캘리포니아주 버클리시의 조례에 따르면, 5,000제곱피트를 초과하는 프로젝트의 경우 물-시멘트 비율을 0.40 이하로 제한하고 있으며, 시공성을 유지하기 위해서는 폴리카복실산 에테르 제품 등의 광범위 감수제 사용이 사실상 의무화되어 있습니다. EU의 환경제품선언(EPD) 제도에서는 시멘트의 15-20%를 보충 재료로 대체한 혼합물에 대해 수명 주기 탄소 크레딧이 부여되지만, 이 목표는 고성능 감수제 없이는 달성하기 어렵습니다. LEED v5와 BREEAM 2024에서는 물-시멘트 비율이 0.40 이하인 슬래브에 추가 점수가 부여되도록 되어, 2031년까지 구조적 수요의 견인력이 강화되고 있습니다.

생분해되지 않는 폴리머 잔류물에 대한 환경적 검토

유럽연합(EU)의 미세플라스틱 규정 2023/2055에 따라, 혼합제 제조업체는 폴리에틸렌옥사이드 측쇄의 분해 경로를 문서화해야 할 의무가 있습니다. 2028년 재검토에 따라, 현재 건설 부문에 적용되고 있는 예외 조항이 철회될 가능성이 있습니다. 마찬가지로, 미국 환경보호청(EPA)이 개정된 유해물질 규제법(TSCA)의 목록에 따르면, 제조업체는 분자량 분포를 공개해야 할 의무가 있으며, 각 배합마다 5만-10만 달러의 규정 준수 비용이 추가로 발생합니다. 이러한 압력으로 인해 28-32%의 감수 효과를 가져오지만, 비용이 20-25% 더 드는 리그닌계 대체재에 대한 조사가 가속화되고 있습니다.

부문별 분석

MPEG는 TPEG보다 비용이 20-25% 저렴하기 때문에 2025년에 폴리카복실산 에테르 시장의 41.14% 점유율을 차지했습니다. 그러나 TPEG는 원격지의 인프라 구간에서 필수적인 35-45℃ 조건에서의 타설 시 120분 동안 슬럼프 유지성을 갖추고 있어, 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 3.26%를 나타낼 것으로 전망됩니다. 현재의 사양이 유지된다면, TPEG 기반 폴리카복실산 에테르 시장 규모는 2031년까지 확대될 가능성이 있지만, APEG는 프리캐스트 부문에서 틈새 시장으로 남을 것으로 보입니다. BASF가 2025년 5월에 Pluriol A2400I의 생산 능력을 확대한 것은 TPEG 수요가 가속화되고 있음을 뒷받침합니다.

지역에 따라 경향은 다릅니다. 중동의 메가 프로젝트에서는 압도적으로 TPEG가 지정되고 있지만, 중국의 2선급 건설업체들은 입찰을 따내기 위해 MPEG를 대안으로 채택하고 있으며, 유럽에서는 인프라 사양에 따라 운송 기간이 길어짐에 따라 점차 TPEG로 전환되고 있습니다. 신흥 리그닌계 및 포스폰산 개질 유형은 원료 및 공정의 병목 현상으로 인해 2031년 시점 시장 점유율은 극히 미미할 것으로 예상되지만, 바이오 또는 점토 내성이 필수적인 부문에서는 프리미엄 가격에 판매될 것으로 전망됩니다.

2025년, 폴리카복실산 에테르 시장 규모 중 74.56%를 액상 제품이 차지했습니다. 이는 플러그 앤 플레이 방식의 배치 처리가 가능하기 때문입니다. 한편, 분말 형태는 예측 기간(2026-2031년) 동안 연평균 성장률(CAGR) 3.78%를 기록하며 성장할 것으로 보이며, 장거리 해상 및 육상 운송 시 운임이 40% 이상 절감되는 아프리카, 중동, 중앙아시아에서 시장 점유율을 확대할 것으로 예측됩니다. 분말로의 전환이 단 5%만 증가하더라도, 2031년까지 그 수익 기여도는 크게 상승할 가능성이 있습니다.

분무 건조 기술의 발전으로 용해 시간이 3분 이하로 단축되어, 처리 용량이 큰 플랜트에서 주요 운영상의 장애 요인이 해소되었습니다. 유럽과 북미에서는 드라이믹스 모르타르 및 셀프레벨링 컴파운드에서 분말 등급의 채택이 적시 생산 방식의 프리팹 전략을 뒷받침하고 있으며, 액상 제품에 비해 10-15% 높은 가격에 판매되는 프리미엄 하위 시장을 공고히 하고 있습니다.

지역별 분석

아시아태평양은 2025년에 폴리카복실산 에테르 시장 점유율의 45.25%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 3.79%를 유지할 것으로 전망됩니다. 인도의 폴리카복실산 에테르 시장은 레디믹스 콘크리트 시장의 확대에 힘입어 성장하고 있으며, 나그푸르, 란치, 라이푸르, 간디나가르에 신설된 배치 플랜트가 수요를 주도하고 있습니다. 한편, 중국에서는 주택 시장이 45% 위축되면서 주요 대도시권의 폴리머 수요가 억제되었으나, 1조 위안 규모의 인프라 부양책 덕분에 2024년 콘크리트 생산량은 24억 m³를 유지했습니다. 아세안(ASEAN) 연결성 마스터플랜의 회랑 계획을 시행하고 있는 동남아시아 국가들에서는 2026년까지 레디믹스 콘크리트 시장에서 폴리카복실산 에테르의 보급률이 약 60%를 나타낼 것으로 전망됩니다.

2025년 북미 시장 점유율은 5,500억 달러 규모의 ‘인프라 투자 및 고용법’에 힘입어 확대되었습니다. 이 법은 고성능 콘크리트가 필요한 교량 및 광대역 인프라에 자금을 지원하고 있습니다. 해당 지역의 하이퍼스케일 데이터센터가 급증하고 있는 것도 시장 성장을 가속화하는 요인이 되고 있습니다. 2025년 한 해에만 40곳 이상의 건설 공사가 착공되었으며, 각 프로젝트에서 초저수축 콘크리트가 지정되었습니다. 2025년 12월 플로리다주에 문을 연 시카의 자동화 공장은 미국 남동부 지역 수요에 대응하기 위한 현지 생산 능력 확충을 보여주는 사례입니다.

유럽 시장 점유율은 2023년부터 2024년에 걸친 부진에서 회복된 모습을 반영하고 있습니다. 독일과 프랑스에서는 주춤했던 도시 교통 프로젝트가 재개되었으며, 동유럽에서는 EU의 결속 기금을 활용하여 교통 인프라 개선이 진행되고 있습니다. BASF의 Pluriol A2400I 생산 확대는 EPD(환경 제품 선언) 규제가 강화되는 가운데, TPEG 기반 등급에 대한 지역별 원료의 안정적인 공급을 확보하기 위한 조치입니다. 중동 및 아프리카와 남미에서는 평균을 상회하는 성장이 나타나고 있습니다. 사우디아라비아와 아랍에미리트에서는 현장 온도가 45°C에 달하는 메가 프로젝트에 TPEG 폴리머가 지정된 반면, 남아프리카공화국의 1조 랜드(594억 달러) 규모 인프라 계획에서는 장거리 액체 운송 비용을 절감하기 위해 분말 등급이 채택되었습니다. 브라질 시장은 시카사가 광업 및 레디믹스 콘크리트(RMC) 고객을 위해 혼화제 생산을 확대함에 따라 회복세를 보이고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the polycarboxylate ether market size is projected to expand from USD 7.51 billion in 2025 and USD 7.74 billion in 2026 to USD 9.03 billion by 2031, registering a CAGR of 3.12% between 2026 and 2031.

This report is Segmented by Type (MPEG-Based, TPEG-Based, and More), Form (Liquid and Powder), Application (Ready-Mix Concrete, High-Performance Concrete, and More), End-User Industry (Residential Construction, Commercial Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Polycarboxylate Ether Market Trends and Insights

Rapid Infrastructure Investment Across Asia-Pacific and Africa

South Asia, Southeast Asia, and Africa together earmarked more than USD 250 billion for transport corridors, power grids, and water projects slated for 2026-2028; the Asian Development Bank alone allocated USD 98.6 billion for that window. Funds are channeling toward concrete used in bridges, highways, and metro systems, where long-haul pumping favors TPEG-based chemistries thanks to 120-minute slump retention. Africa's annual infrastructure gap of roughly USD 170 billion is stimulating demand for powder-grade admixtures that cut freight volumes by 70%, a decisive cost advantage on landlocked routes. These capital programs collectively lift the Polycarboxylate Ether market by an estimated 1.2 percentage-point CAGR contribution through 2031.

Tightening Water-Cement-Ratio Rules in Green Building Codes

Municipal ordinances in Berkeley, California, cap water-cement ratios below 0.40 for projects above 5,000 ft2, effectively mandating high-range water reducers such as Polycarboxylate Ether products to maintain workability. The EU's Environmental Product Declaration scheme grants life-cycle-carbon credits for mixes that substitute 15-20% cement with supplementary materials, a target difficult to reach without advanced superplasticizers. LEED v5 and BREEAM 2024 now award extra points to slabs achieving the same sub-0.40 ratio, reinforcing a structural pull through 2031.

Environmental Scrutiny of Non-Biodegradable Polymer Residues

The European Union (EU) microplastics restriction 2023/2055 forces admixture producers to document degradation paths for polyethylene-oxide side chains; a 2028 review could rescind current construction exemptions. The U.S. EPA's updated Toxic Substances Control Act inventory likewise obliges manufacturers to disclose molecular-weight distributions, adding USD 50,000-100,000 compliance cost per formulation. These pressures accelerate research into lignin-based alternatives that deliver 28-32 % water reduction yet command 20-25 % higher cost.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of RMC Batching Plants in Tier-2 Cities

- 3D-Printed Concrete Needs Rheology-Tuned Super-Plasticizers

- Patent Thickets Around Comb-Polymer Architectures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MPEG held 41.14% Polycarboxylate Ether market share in 2025 because its cost sits 20-25% below TPEG. TPEG, however, is forecast for a 3.26% CAGR during the forecast period (2026-2031) owing to 120-minute slump retention in 35-45°C pours, essential for remote infrastructure segments. The Polycarboxylate Ether market size for TPEG-based grades could rise by 2031 if current specifications persist, while APEG remains niche for precast. BASF's May 2025 boost in Pluriol A2400I capacity confirms accelerating TPEG demand.

Regional preferences diverge: Middle East megaprojects overwhelmingly specify TPEG, China's tier-2 builders substitute MPEG to win bids, and Europe is slowly pivoting toward TPEG as infrastructure specs lengthen transport windows. Emerging lignin-based and phosphonate-modified types are expected to have a minimal share by 2031, owing to feedstock and process bottlenecks, but may command premium pricing where bio-based or clay-tolerant credentials are mandated.

Liquid products dominated 74.56% of the Polycarboxylate Ether market size in 2025 due to plug-and-play batching. Powder forms, though, are anticipated to grow at 3.78% CAGR during the forecast period (2026-2031), taking share in Africa, the Middle East, and Central Asia, where freight savings exceed 40% on long ocean-plus-road voyages. A shift of even five percentage points toward powder could lift its revenue contribution substantially by 2031.

Dissolution times have shrunk below three minutes through spray-drying advances, removing the chief operational barrier for high-throughput plants. In Europe and North America, powder-grade uptake in dry-mix mortars and self-leveling compounds supports just-in-time prefabrication strategies, solidifying a premium sub-segment that sells at 10-15% price lifts over liquid equivalents.

Geography Analysis

Asia-Pacific commanded 45.25% of the Polycarboxylate Ether market share in 2025 and should sustain a 3.79% CAGR to 2031. India's Polycarboxylate Ether market is buoyed by a ready-mix expansion, with new batching plants in Nagpur, Ranchi, Raipur, and Gandhinagar driving uptake. Conversely, China's 45% residential downturn curtailed polymer demand in top-tier metros, though a CNY 1 trillion infrastructure stimulus preserved concrete production at 2.4 billion m3 in 2024. Southeast Asian nations executing the ASEAN Connectivity master-plan corridors increased Polycarboxylate Ether market penetration in ready-mix to roughly 60% by 2026.

North America's share in 2025 was strengthened by the USD 550 billion Infrastructure Investment and Jobs Act, which is channeling funds to bridges and broadband foundations requiring high-performance concrete. The region's hyperscale data-center boom is another accelerant: more than 40 sites broke ground in 2025 alone, each specifying ultra-low-shrinkage mixes. Sika's December 2025 automated plant in Florida demonstrates local capacity buildup to meet Southeastern U.S. demand.

Europe's market share reflects recovery from the 2023-2024 slump; Germany and France resumed stalled urban-mobility projects, while Eastern Europe leverages EU Cohesion Funds for transport upgrades. BASF's Pluriol A2400I expansion provides regional feedstock security for TPEG-based grades amid stricter EPD rules. The Middle East & Africa and South America exhibit above-average growth. Saudi Arabia and the UAE specify TPEG polymers for mega-projects facing 45°C site temperatures, whereas South Africa's ZAR 1 trillion (USD 59.4 billion) infrastructure pipeline uses powder grades to sidestep long-haul liquid shipping costs. Brazil's market is rebounding as Sika extends admixture output to serve mining and ready-mix clients.

- Arkema

- BASF

- Chembond Chemicals Limited

- CICO Group

- Dow

- Enaspol a.s.

- Fosroc, Inc.

- Ha-Be Betonchemie GmbH

- Kao Chemicals Europe, S.L.U.

- LOTTE Fine Chemical CO,.Ltd.

- MAPEI S.p.A.

- MUHU (China) Construction Materials Co., Ltd.

- Saint-Gobain

- Sika AG

- Sobute New Materials Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid infrastructure investment across Asia-Pacific and Africa

- 4.2.2 Tightening water-cement-ratio rules in green building codes

- 4.2.3 Expansion of RMC batching plants in tier-2 cities

- 4.2.4 3D-printed concrete needs rheology-tuned super-plasticizers

- 4.2.5 Liquid-cooled data-center slabs demand ultra-low-shrinkage mixes

- 4.3 Market Restraints

- 4.3.1 Environmental scrutiny of non-biodegradable polymer residues

- 4.3.2 Patent thickets around comb-polymer architectures

- 4.3.3 Rise of LC3 and geopolymer concrete reducing PCE dosage

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 MPEG-Based

- 5.1.2 APEG-Based

- 5.1.3 TPEG-Based

- 5.1.4 Others

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Powder

- 5.3 By Application

- 5.3.1 Ready-Mix Concrete (RMC)

- 5.3.2 Precast Concrete

- 5.3.3 High-Performance Concrete

- 5.3.4 Self-Compacting Concrete

- 5.3.5 Others

- 5.4 By End-user Industry

- 5.4.1 Residential Construction

- 5.4.2 Commercial Construction

- 5.4.3 Infrastructure Projects

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 NORDIC Countries

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Arkema

- 6.4.2 BASF

- 6.4.3 Chembond Chemicals Limited

- 6.4.4 CICO Group

- 6.4.5 Dow

- 6.4.6 Enaspol a.s.

- 6.4.7 Fosroc, Inc.

- 6.4.8 Ha-Be Betonchemie GmbH

- 6.4.9 Kao Chemicals Europe, S.L.U.

- 6.4.10 LOTTE Fine Chemical CO,.Ltd.

- 6.4.11 MAPEI S.p.A.

- 6.4.12 MUHU (China) Construction Materials Co., Ltd.

- 6.4.13 Saint-Gobain

- 6.4.14 Sika AG

- 6.4.15 Sobute New Materials Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment