|

시장보고서

상품코드

2062257

실험용 유리 기구 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Laboratory Glassware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

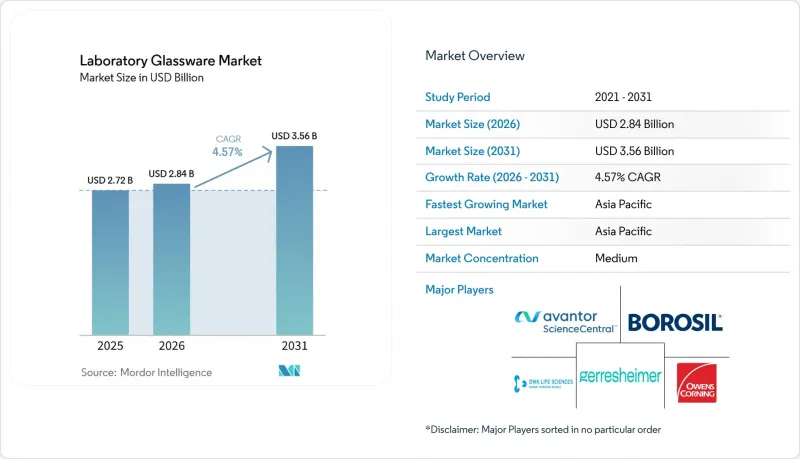

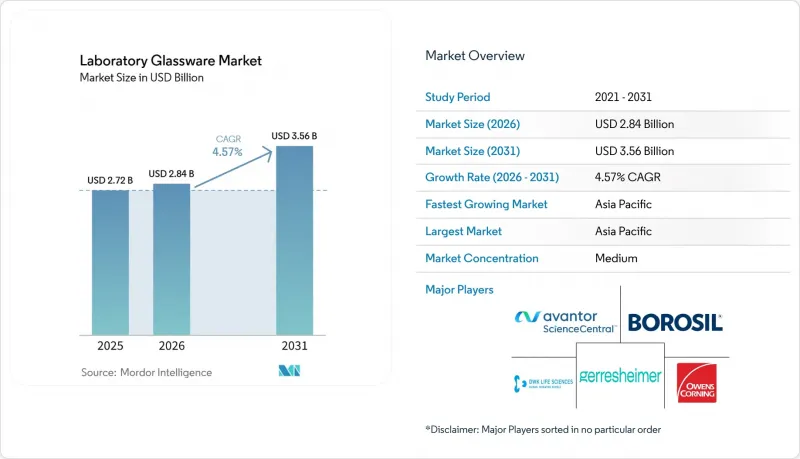

Mordor Intelligence에 의하면, 실험용 유리 기구 시장 규모는 2025년에 27억 2,000만 달러로 평가되었고 2026년 28억 4,000만 달러에서 2031년까지 35억 6,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.57%를 나타낼 전망입니다.

본 보고서는 제품 유형(비커, 시험관 및 배양관 등), 재질(붕규산 유리, 석영 유리 등), 최종 사용자 산업(제약·바이오기술, 학술·연구 기관 등), 그리고 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 실험용 유리 기구 시장 동향 및 분석

학술 및 정부 산하 연구기관의 확대

공공 부문의 과학 연구 자금 지원은 멀티오믹스, 포토닉스, 양자 센싱 연구에 필수적인 소모품으로 점점 더 집중되고 있습니다. 아일랜드는 포토닉스 연구소에 1억 유로(1억 1,538만 달러)를 배정하며, 초저형광 석영 큐벳을 중점적으로 지원하고 있습니다. 동시에, 미국 국립과학재단(NSF)은 바이오 제조 혁신 엔진에 1억 6,000만 달러를 배정하며, 미국 국립표준기술연구소(NIST)의 기준에 부합하는 일련번호가 부여된 메스 플라스크의 필요성을 강조했습니다. 중국은 3조 9,000억 위안(5,600억 달러) 규모의 연구 예산에서 각 성의 조달 담당자들에게 국내 붕규산 유리 공급업체를 우선적으로 선정할 것을 요청하고 있으며, 이에 따라 장쑤성과 저장성에서 생산 능력 확대가 촉진되고 있습니다. 인도 생명공학부는 12개의 생명공학 클러스터를 설립하여, 통합 입찰을 통해 붕규산 유리 제품 및 석영 제품의 대량 조달을 일원화하고 있습니다. 이러한 노력은 필수 장비의 수명을 연장하는 동시에, 미국약전(USP) 1058 규격에 부합하도록 교정된 고품질 유리 기구에 대한 안정적인 수요를 확보합니다.

진단·분석 연구소 증가

인도 및 동남아시아 전역에서 새로운 기준 검사 기관이 설립됨에 따라, 200회의 멸균 주기를 견딜 수 있는 오토클레이브용 붕규산 시험관 수요가 크게 증가하고 있습니다. 2024년 식품·사료 신속경보시스템(RASFF)을 통해 발령된 4,563건의 식품 안전 경보에 따라, 유럽연합 회원국들은 농약 분석 역량을 강화하고 있으며, 그 결과 붕규산제 에를렌마이어 플라스크와 분리 깔때기의 주문이 증가하고 있습니다. 인도 식품안전기준청(FSSAI)은 국제표준화기구/국제전기기술위원회(ISO/IEC) 17025 규격에 따라 2027년까지 인도의 공인 검사 기관 네트워크를 400곳으로 확대할 계획이며, 이에 따라 용량 측정 기기에 대한 수요가 더욱 증가하고 있습니다. 인도의 임상시험에서 2024년 신규 프로토콜 수가 1만 8,000건에 달하며, 배양관과 피펫의 소비량이 크게 증가하여 그 사용량은 표준 진단 검사에 비해 3배에 달하고 있습니다.

임상 현장에서 재사용 가능한 유리 기구에 대한 규제상 제한

재사용 가능한 유리 기구는 지속가능성이라는 장점에도 불구하고, 미국 산업안전보건청(OSHA)의 ‘혈액 유래 병원체 기준’ 및 미국 질병통제예방센터(CDC)의 지침에 따라 병원 검사실에서 점차 퇴출되고 있습니다. 이 지침에서는 일회용 용기의 사용을 권장하고 있습니다. BD사의 Barricor 튜브는 기존의 유리제 혈청 분리 튜브를 대체하는 제품으로, 원심 분리 시간을 단축하고 유리 입자로 인한 오염 위험을 제거합니다. 현재 혈액학용 튜브에는 사이클로올레핀 폴리머 하이브리드 소재가 널리 사용되고 있지만, 에펜도르프(Eppendorf)사의 연구에 따르면 재활용 플라스틱의 배합 비율이 20%를 초과하면 미국약전(USP) 661 시험을 통과하지 못하는 것으로 나타났습니다. 그 결과, 연구소에서는 여전히 붕규산 유리가 사용되고 있는 반면, 임상 현장에서는 검증된 플라스틱 솔루션의 도입이 확대되고 있습니다.

부문별 분석

뷰렛과 피펫은 2025년 실험용 유리 기구 시장 점유율의 26.22%를 차지하고 있으며, 2031년까지 연평균 성장률(CAGR) 5.36%를 기록하며 다른 제품들을 앞지르는 성장이 예상됩니다. 주문형 교정 기능을 갖춘 전자 피펫팅 시스템의 보급으로 인해, 붕규산 팁에 대한 수요가 증가하고 있습니다. 제약 품질 관리(QC) 시설에서는 플라스크를 주로 사용합니다. 특히, 부속서 1의 오염 관리 조항에서 소다석회 유리보다 멸균 처리된 유리가 우선적으로 사용되기 때문입니다. 한편, 시험관은 미생물학 및 연구·교육용 실험실에서는 꾸준히 사용되고 있지만, 병원에서의 도입은 일회용 대체품의 사용 증가로 인해 제한되고 있습니다. 식품 안전 및 환경 시험에 대한 규제가 강화됨에 따라, 측정 실린더, 커패시터 및 특수 솝슬레이 장치를 이용한 시료 전처리 처리 능력이 증가하고 있습니다. 이러한 카테고리 전반에 걸쳐 QR 코드로 변환된 일련번호나 레이저 각인된 눈금의 사용이 표준화되고 있어, 저비용 경쟁사들에게는 과제가 되고 있습니다.

예측 기간이 지남에 따라, 뷰렛과 피펫은 주도적인 위치를 더욱 공고히 하고 있습니다. 이러한 변화는 미국약전(USP)에 부합하는 라이프사이클 기록이 기존의 스프레드시트에서 실험실 정보 관리 시스템(LIMS)의 애플리케이션 프로그래밍 인터페이스(API)로 전환되고 있는 데서 비롯됩니다. 각 벤더사는 이러한 추세를 활용하여, 시리얼 번호가 부여된 뷰렛에 전자 피펫 서비스 계약을 묶음 판매함으로써 지속적인 수익원을 확보하고, 교체 비용을 높이고 있습니다. 비커, 워치글라스, 페트리 접시 등의 표준 품목은 일반적으로 정해진 교체 주기를 따릅니다. 그러나 반도체 및 세포 이미징 분야의 워크플로우를 고려할 때, 정전기 방지 및 저자가형광 제품에 대한 수요가 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 48.11%를 차지하고 있으며, 2031년까지 연평균 성장률(CAGR) 5.67%로 성장할 것으로 전망됩니다. 중국에서는 막대한 연구 투자와 현지 조달 의무가 맞물려, 붕규산 유리 제품의 국내 밸류체인이 강화되고 있습니다. 인도에서는 임상시험 증가와 진단 네트워크의 확장이 메스 실린더와 피펫 수요를 견인하고 있습니다. 일본과 한국은 프리미엄 시장에 주력하고 있으며, 포토닉스 및 반도체 연구소를 위해 설계된 고정밀 석영 큐벳과 마이크로 리액터를 수출하고 있습니다. 한편, 동남아시아에서는 유럽연합(EU)의 식품 수출 기준 충족을 위한 노력이 진행되고 있어, 삭슬리 추출기나 분리 깔때기에 대한 수요가 증가하고 있습니다.

북미에서는 시리얼화된 유리 기구를 중시하는 미국약전(USP) 및 미국 식품의약국(FDA)의 엄격한 규제를 활용하고 있습니다. 미국에서는 주로 캘리포니아주, 노스캐롤라이나주, 버지니아주의 바이오 제조 거점과 관련하여 수백만 개의 메스 플라스크가 도입될 전망입니다. 캐나다에서는 청정기술 세제 혜택에 힘입어 대학들이 석영제 광화학 반응기에 대한 투자를 확대되고 있습니다. 동시에 멕시코는 미국공급망에 대응하는 분석 시험 센터의 니어쇼어링 혜택을 누리고 있습니다.

유럽의 전망은 유럽연합 우수제조기준(EU GMP) 부속서 1의 시행과 기후 변화 관련 보고 의무의 강화로 인해 영향을 받고 있습니다. 독일, 프랑스, 영국은 ‘호라이즌 유럽’의 자금을 양자 센싱 및 세포 치료 연구에 배정하고 있으며, 이 두 분야 모두 초고순도 유리가 필요합니다. 북유럽 국가들은 ‘수질 프레임워크 지침’에 따라 환경 모니터링용으로 석영제 여과 장치를 채택하고 있습니다. 한편, 동유럽에서는 품질 관리 시스템의 단계적 강화가 진행되고 있어, 국제표준화기구(ISO) 규격을 준수하는 붕규산 유리 제품에 대한 잠재적 수요가 부각되고 있습니다.

남미에서는 브라질이 의약품 충전 및 포장 능력을 확대하고 있어 한 자릿수 중반대의 성장이 예상됩니다. 동시에 칠레는 리튬 배터리 연구시설에 투자하고 있으며, 특히 전해액 시험용 붕규산 유리 커패시터가 필요합니다. 중동 및 아프리카에서는 사우디아라비아의 ‘비전 2030’ 과학 공원이나 남아프리카공화국의 수질 모니터링 이니셔티브에 힘입어 신규 수주가 늘고 있지만, 유통망이 분산되어 있어 그 잠재력을 충분히 발휘하지 못하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the laboratory glassware market size was valued at USD 2.72 billion in 2025 and is estimated to grow from USD 2.84 billion in 2026 to reach USD 3.56 billion by 2031, at a CAGR of 4.57% during the forecast period (2026-2031).

This report is Segmented by Product Type (Beakers, Test Tubes and Culture Tubes, and More), Material Type (Borosilicate Glass, Quartz Glass, and More), End-User Industry (Pharmaceutical and Biotechnology, Academic and Research Institutions, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Laboratory Glassware Market Trends and Insights

Expansion of Academic and Government Research Institutes

Public-sector science funding is increasingly directed toward consumables essential for multi-omics, photonics, and quantum-sensing research. Ireland allocated EUR 100 million (USD 115.38 million) for photonics laboratories, emphasizing ultra-low-fluorescence quartz cuvettes. Concurrently, the United States National Science Foundation (NSF) set aside USD 160 million for biomanufacturing innovation engines, highlighting the need for serialized volumetric flasks compliant with National Institute of Standards and Technology (NIST) standards. China's CNY 3.9 trillion (USD 0.56 trillion) research budget requires provincial buyers to prioritize domestic borosilicate suppliers, driving capacity expansions in Jiangsu and Zhejiang. India's Department of Biotechnology is establishing 12 biotechnology clusters, centralizing bulk procurement of borosilicate and quartzware through unified tenders. These initiatives collectively extend the lifecycle of essential equipment and ensure consistent demand for premium glassware calibrated to meet United States Pharmacopeia (USP) 1058 standards.

Rising Number of Diagnostic and Analytical Laboratories

New reference laboratories across India and Southeast Asia are significantly increasing the demand for autoclavable borosilicate test tubes, capable of enduring 200 sterilization cycles. In response to 4,563 food-safety alerts from the Rapid Alert System for Food and Feed (RASFF) in 2024, European member states are enhancing their pesticide-analysis capabilities, leading to increased orders for borosilicate Erlenmeyer flasks and separatory funnels. The Food Safety and Standards Authority of India (FSSAI) plans to expand India's accredited laboratory network to 400 sites by 2027 under International Organization for Standardization/International Electrotechnical Commission (ISO/IEC) 17025 standards, further amplifying the demand for volumetric ware. With clinical trials in India reaching 18,000 new protocols in 2024, there has been a significant increase in the consumption of culture tubes and pipettes, tripling their usage compared to standard diagnostics.

Regulatory Limits on Reusable Glassware in Clinical Settings

Reusable glassware, despite its sustainability benefits, is being phased out in hospital laboratories due to the Occupational Safety and Health Administration's (OSHA) Bloodborne Pathogens Standard and the Centers for Disease Control and Prevention (CDC) guidelines, which recommend single-use containers. BD's Barricor tubes, an alternative to traditional glass serum-separator formats, reduce centrifugation times and eliminate the risk of glass-particle contamination. Cyclic-olefin-polymer hybrids are now widely used in hematology tubes, although research by Eppendorf indicates that recycled-plastic blends exceeding 20% fail United States Pharmacopeia (USP) 661 tests. Consequently, research laboratories continue to use borosilicate glass, while clinical settings increasingly adopt validated plastic solutions.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Precision-Measurement, Contamination-Free Labware

- Stringent Traceability Rules Spurring Serialized Glassware Demand

- Substitution Threat from Disposable/Autoclavable Plasticware

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Burettes and pipettes, commanding 26.22% of the 2025 laboratory glassware market share, are set to outpace their peers with a projected 5.36% CAGR through 2031. The rising demand for borosilicate tips is driven by electronic pipetting systems that feature on-demand calibration. In pharmaceutical quality control (QC) suites, flasks are preferred, especially with Annex 1's contamination-control clauses prioritizing ready-to-sterilize glass over soda-lime. While test tubes see steady use in microbiology and research teaching labs, their adoption in hospitals is limited by the increasing use of single-use alternatives. Mandates in food safety and environmental testing are increasing the throughput of sample preparation for graduated cylinders, condensers, and specialized Soxhlet apparatus. Across these categories, the adoption of QR-coded serial numbers and laser-etched volume marks is becoming standard, creating challenges for low-cost competitors.

As the forecast period progresses, burettes and pipettes are strengthening their leadership. This shift is supported by the transition of United States Pharmacopeia (USP)-compliant lifecycle records from traditional spreadsheets to laboratory information management system (LIMS) application programming interfaces (APIs). Vendors are leveraging this trend by bundling electronic pipette service contracts with serialized burettes to secure recurring revenue streams and increase switching costs. Standard items like beakers, watch glasses, and petri dishes typically follow a mature replacement cycle. However, there is demand for antistatic or low-autofluorescence variants, driven by workflows in semiconductors and cell imaging.

Geography Analysis

Asia-Pacific, accounting for 48.11% of 2025 revenue, is projected to grow at a 5.67% compound annual growth rate (CAGR) through 2031. China's substantial research investments, combined with local sourcing mandates, are strengthening the domestic value chain for borosilicate ware. In India, growth in clinical trials and an expanding diagnostics network are driving demand for graduated cylinders and pipettes. Japan and South Korea are focusing on the premium market, exporting high-precision quartz cuvettes and microreactors designed for photonics and semiconductor laboratories. Meanwhile, Southeast Asia's efforts to comply with European Union (EU) food-export standards are increasing the demand for Soxhlet extractors and separatory funnels.

North America is leveraging stringent United States Pharmacopeia (USP) and Food and Drug Administration (FDA) regulations that emphasize serialized glassware. The United States is expected to introduce millions of volumetric flasks, primarily linked to biomanufacturing hubs in California, North Carolina, and Virginia. In Canada, clean-tech tax incentives are encouraging universities to invest in quartz photochemical reactors. Simultaneously, Mexico is benefiting from the near-shoring of analytical-testing centers catering to United States supply chains.

Europe's outlook is influenced by the enforcement of European Union Good Manufacturing Practice (EU GMP) Annex 1 and emerging climate-ledger reporting mandates. Germany, France, and the United Kingdom are allocating Horizon Europe funds into quantum-sensing and cell-therapy research, both of which require ultra-pure glass. Nordic countries, under the Water Framework Directive, are adopting quartz filtration assemblies for environmental monitoring. Meanwhile, Eastern Europe is gradually upgrading its quality systems, revealing a latent demand for International Organization for Standardization (ISO)-compliant borosilicate ware.

In South America, mid-single-digit growth is evident as Brazil expands its pharmaceutical fill-finish capabilities. Concurrently, Chile is investing in lithium battery research labs, specifically requiring borosilicate condensers for electrolyte testing. The Middle East and Africa are witnessing new orders driven by Saudi Arabia's Vision 2030 science parks and South Africa's water-quality monitoring initiatives, although a fragmented distribution network limits their full potential.

- ATS Life Sciences Wilmad

- Avantor, Inc.

- Borosil Scientific Limited

- Calibre Scientific

- Corning Incorporated

- DWK Life Sciences

- Gerresheimer AG

- Glassco Laboratory Equipment Pvt. Ltd.

- Heathrow Scientific

- Kavalierglass, a.s.

- Sartorius AG

- Technosklo Ltd.

- TECHNOSKLO s.r.o.

- Thomas Scientific

- United Scientific Supplies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of academic and government research institutes

- 4.2.2 Rising number of diagnostic and analytical laboratories

- 4.2.3 Shift toward precision-measurement, contamination-free labware

- 4.2.4 Stringent traceability rules (USP (1058), EU GMP Annex 1) spurring serialized glassware demand

- 4.2.5 Microfluidics start-ups requiring ultra-thin custom glass chips

- 4.3 Market Restraints

- 4.3.1 Regulatory limits on reusable glassware in clinical settings

- 4.3.2 Substitution threat from disposable/autoclavable plasticware

- 4.3.3 Rising insurance premiums linked to glass breakage losses

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Beakers

- 5.1.2 Flasks (Erlenmeyer, Volumetric, Filtering)

- 5.1.3 Test Tubes and Culture Tubes

- 5.1.4 Burettes and Pipettes

- 5.1.5 Graduated Cylinders

- 5.1.6 Petri Dishes and Watch Glasses

- 5.1.7 Condensers and Funnels

- 5.1.8 Desiccators and Stirrers

- 5.1.9 Other Specialised Glassware (Separatory Funnels, Soxhlet Extractors)

- 5.2 By Material Type

- 5.2.1 Borosilicate Glass

- 5.2.2 Quartz Glass

- 5.2.3 Soda-Lime Glass

- 5.2.4 Other Speciality Glass Types

- 5.3 By End-user Industry

- 5.3.1 Pharmaceutical and Biotechnology

- 5.3.2 Academic and Research Institutions

- 5.3.3 Food and Beverage Testing Laboratories

- 5.3.4 Environmental and Water Testing

- 5.3.5 Healthcare and Clinical Diagnostics

- 5.3.6 Chemical and Petrochemical Industries

- 5.3.7 Other End-user Industries (Forensics, Agriculture, Material Science)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ATS Life Sciences Wilmad

- 6.4.2 Avantor, Inc.

- 6.4.3 Borosil Scientific Limited

- 6.4.4 Calibre Scientific

- 6.4.5 Corning Incorporated

- 6.4.6 DWK Life Sciences

- 6.4.7 Gerresheimer AG

- 6.4.8 Glassco Laboratory Equipment Pvt. Ltd.

- 6.4.9 Heathrow Scientific

- 6.4.10 Kavalierglass, a.s.

- 6.4.11 Sartorius AG

- 6.4.12 Technosklo Ltd.

- 6.4.13 TECHNOSKLO s.r.o.

- 6.4.14 Thomas Scientific

- 6.4.15 United Scientific Supplies, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment