|

시장보고서

상품코드

2062260

시각적 분석 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Visual Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

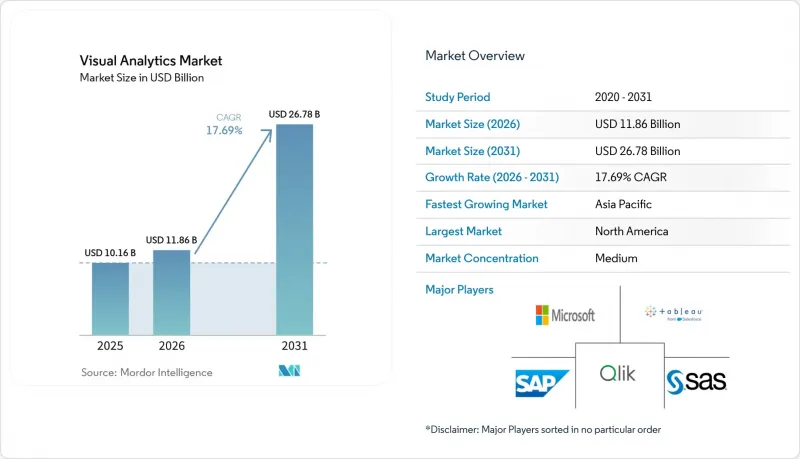

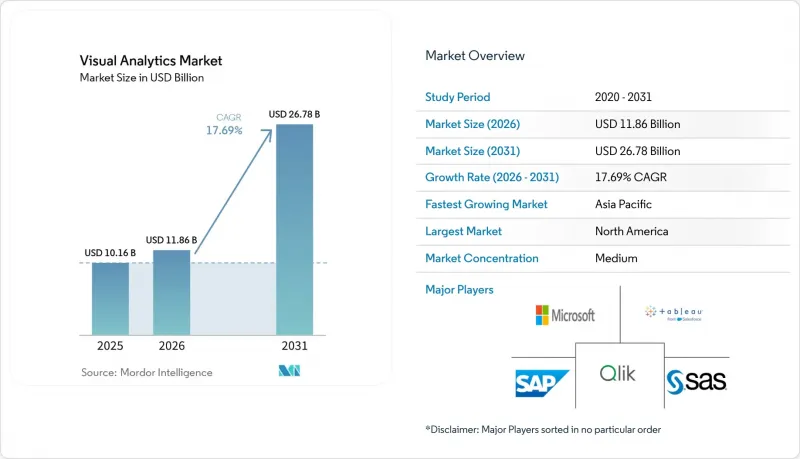

Mordor Intelligence에 의하면, 시각적 분석 시장 규모는 2025년 101억 6,000만 달러, 2026년 118억 6,000만 달러에서 2031년까지 267억 8,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 17.69%를 나타낼 것으로 예측됩니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 형태(On-Premise 및 클라우드), 조직 규모(대기업 및 중소기업), 업종(은행, 금융서비스 및 보험(BFSI), IT 및 통신, 소매 및 소비재 등), 용도(영업·마케팅, 재무·업무 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 시각적 분석 시장 동향과 인사이트

클라우드 기반 데이터 생성 확대

기업의 데이터 자산은 급속히 증가하고 있으며, 2026년 초까지 그 중 약 90%가 비정형 데이터 사일로에 저장될 것으로 예측됩니다. 제로 피크 쿼리 패턴을 통해 사용자는 데이터를 즉시 분석할 수 있게 되며, 추출·변환·로드(ETL)의 오버헤드를 줄이고 하이퍼스케일러에 대한 종속성을 피할 수 있습니다. GPU 가속 엔진은 비정형 분석의 속도를 높여주며, 통합된 시맨틱 레이어는 정형 및 비정형 메타데이터를 통합함으로써 프로젝트를 시범 단계에서 운영 환경으로 전환합니다. 데이터 상주 규정, 지연 시간 요구 사항, 그리고 가격과 성능 간의 상충 관계로 인해 단일 클라우드 전략은 위험 부담이 크기 때문에 하이브리드 아키텍처가 계속해서 자리 잡고 있습니다.

셀프 서비스 BI 플랫폼에 대한 수요 증가

사용자 경험, 거버넌스, 경영진의 지원을 중시하는 조직에서는 6개월 이내에 일반 사용자의 채용률이 15-25%에서 40-60%로 향상됩니다. 중견 기업 대상 도입 시 5년간의 총 소유 비용(TCO)은 종량제 요금제와 자동화된 데이터 리니지 도입으로 인해 2025년에는 100만-140만 달러로 감소했습니다. 그러나 문화적 변화, 데이터 품질 문제, 그리고 교육 부족이 도구 도입의 효과를 상쇄하고 있어, 여전히 프로젝트의 70%가 정체 상태에 머물러 있습니다. 연방형이자 제로 카피 설계는 로컬 환경의 민첩성과 중앙 집중식 관리를 결합하는 한편, 시맨틱 레이어는 행 단위의 보안과 일관된 지표를 철저히 보장합니다.

중소기업의 높은 총 소유 비용

중견 기업을 대상으로 한 분석 프로젝트는 5년 동안 100만-150만 달러의 비용이 소요되지만, 서비스 비용이나 인프라 비용이 라이선스 비용을 크게 웃도는 경우가 적지 않습니다. 도입 후 이용률이 낮은 경우, 사용자당 비용이 1,000달러에서 3만 달러까지 치솟아 도입을 가로막는 요인이 되고 있습니다. 숨겨진 클라우드 비용은월1,000달러에서 5만 달러 이상에 달하며, 지속적인 유지 관리에는 도입 예산의 10-15%가 소요됩니다. 사용량 기반 Spark 과금 방식을 통해 버스트형 워크로드의 비용을 40% 절감할 수 있지만, 중소기업은 과도한 요금을 피하기 위해 사용 현황을 세밀하게 모니터링해야 합니다.

부문별 분석

소프트웨어 부문은 클라우드 네이티브 BI 제품군, 시맨틱 모델링 엔진 및 임베디드 분석 솔루션의 라이선스 매출을 통해 2025년 전체 매출의 71.73%를 차지했습니다. 이러한 도구는 의사결정 과정을 합리화하고 업무 효율을 높이는 것을 목표로 하는 조직에 있어 필수적인 요소가 되었습니다. 그러나 기업들이 도입 청사진, 관리형 운영, 데이터 리터러시 프로그램을 점점 더 많이 요구함에 따라 서비스 부문은 연평균 성장률(CAGR) 19.49%로 성장하고 있습니다. 이러한 서비스는 재무, 공급망, 수익 사이클 분야의 주요 역량 격차를 해소하고, 6개월 이내에 사용자 도입률을 두 배로 늘리도록 설계되었습니다. 전문 서비스는 중견 기업 대상 프로젝트의 경우 일반적으로 25만-75만 달러의 비용이 소요되지만, 성과 기반 계약에서는 순회수율 2-4% 포인트 개선과 같은 측정 가능한 KPI 향상에 보수를 연동함으로써, 고객에게 명확한 투자 수익률(ROI)을 보장합니다.

시각적 분석 서비스 시장은 AI를 활용한 데이터 준비 지원 도구와 사전 예방적 모니터링 에이전트의 통합을 원동력으로 삼아, 소프트웨어 시장보다 더 빠른 성장이 예상됩니다. 이러한 혁신을 통해 수작업이 대폭 줄어들게 되어, 조직은 전략적 과제에 집중할 수 있게 됩니다. Tableau Einstein Alliance 및 Qlik과의 서비스 제휴와 같은 파트너십을 통해, 현재는 마이그레이션 자동화, 시맨틱 레이어 설계, 종합적인 교육 모듈을 포함한 번들 솔루션이 제공되고 있습니다. 이러한 번들 제품은 파트너와의 유대 관계를 강화하고, 도입 과정을 효율화하며, 인사이트 확보까지 걸리는 시간을 단축함으로써, 분석 역량을 강화하고자 하는 기업들에게 매우 매력적인 선택지가 되고 있습니다.

클라우드 워크로드는 2025년 지출의 63.43%를 차지해, Delta Lake, Parquet, Apache Iceberg의 표준화로 인해 벤더 종속성이 완화됨에 따라 2031년까지 연평균 성장률(CAGR) 18.49%로 확대될 것으로 전망됩니다. 이러한 성장은 확장성, 유연성, 비용 효율성을 제공하는 클라우드 네이티브 기술의 도입 확대에 힘입어 이루어지고 있습니다. Microsoft Fabric의 Direct Lake와 SAP의 라이브 Snowflake 커넥터는 전체적인 복제를 수행하지 않으면서도 거버넌스와 지연 시간 요구 사항을 모두 충족하는 제로 카피 쿼리 경로로 전환하는 것을 보여줍니다. 이러한 발전 덕분에 조직은 데이터 거버넌스 정책을 준수하면서도 데이터 처리 및 분석의 효율성을 높일 수 있습니다. Spark 워크로드의 자동 확장 과금을 통해 총 소유 비용(TCO)이 절감되며, 특히 신속한 데이터 인사이트가 요구되는 업계에서 버스트형 분석이나 실험에 클라우드를 활용하는 것이 현실적으로 가능해집니다.

On-Premise 환경은 데이터 보관 요건이나 에어갭 환경에서의 운영이 여전히 필수로 요구되는 규제 산업 분야와 주권 AI 도입 분야에서 여전히 유지되고 있습니다. 의료, 금융, 정부 등 이러한 업계에서는 데이터 보안과 규정 준수가 최우선 과제이며, On-Premise 솔루션이 요구됩니다. 따라서 클라우드의 확장성과 On-Premise 시스템의 제어성을 결합한 하이브리드 방식이 아키텍처 로드맵에서 주류를 이루고 있습니다. 다양한 환경을 아우르는 정책 조정이 가능한 벤더는 마이그레이션 위험과 규정 준수 위험을 줄일 수 있어 시장 점유율을 확대되고 있습니다. 이 하이브리드 모델을 통해 조직은 특정 규제 및 운영 요건을 충족하면서 IT 인프라를 최적화할 수 있습니다.

지역별 분석

북미는 2025년 매출의 38.23%를 차지하고 있으며, 이는 3,570억 달러에 달하는 미국 정부의 기술 예산과 3,611건에 달하는 연방 정부의 AI 활용 사례에 힘입은 결과입니다. 이 지역은 클라우드 인프라, AI 기반 솔루션, 그리고 다양한 산업 분야에 걸친 디지털 전환(DX) 이니셔티브에 대한 적극적인 투자의 혜택을 누리고 있습니다. 정부 기관들은 클라우드 인프라, 통합 데이터 패브릭, 모델 검증 도구의 도입을 가속화하고 있으며, 출처 추적성, 감사 가능성 및 미국 내 호스팅 지역을 제공하는 공급업체를 우선적으로 선정하고 있습니다. 또한, 레거시 시스템의 현대화 필요성, ‘바이 아메리칸(Buy American)’ 규정, 그리고 소프트웨어 부품 명세서(BOM)의 투명성으로 인해, 검증 가능한 조달과 설명 가능한 결과를 제공하는 플랫폼에 대한 수요가 증가하고 있습니다. 주요 기술 공급업체들의 존재와 견고한 규제 체계가 이 지역 시장에서의 입지를 더욱 공고히 하고 있습니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 2031년까지 연평균 성장률(CAGR)은 18.69%를 나타낼 것으로 예측됩니다. 주권 AI에 대한 규제, 온디바이스 추론 요건, 그리고 제조업 클러스터에서의 로우코드 플랫폼 도입 확대가 해당 지역의 성장을 주도하고 있습니다. 이러한 요인들에 더해, OPC-UA 및 MQTT 표준의 도입으로 공장 전체를 아우르는 예측 모델 구축이 가능해졌으며, 업무 효율이 향상되고 있습니다. 엣지 배포는 네트워크 비용과 지연 시간을 줄여준다는 점에서 주목받고 있으며, 일본어, 한국어, 중국어 등으로 현지화된 인터페이스를 통해 사용자 기반이 확대되고 있습니다. 이 지역의 다양한 산업 기반과 디지털화를 추진하는 정부의 이니셔티브이 맞물려, 이 지역은 시장의 주요 성장 거점으로서의 입지를 확고히 하고 있습니다.

유럽에서는 하이브리드 아키텍처를 정착시키는 GDPR(EU 개인정보보호규정) 및 데이터 주권 관련 법률 덕분에 꾸준한 성장세가 이어지고 있습니다. 해당 지역에서 데이터 개인정보 보호 및 규정 준수에 대한 관심이 높아짐에 따라, 엄격한 규제 요건을 충족하는 솔루션의 도입이 촉진되고 있습니다. 데이터 보안과 운영의 유연성을 확보하기 위해, On-Premise와 클라우드 기반 시스템을 결합한 하이브리드 아키텍처가 점점 더 선호되고 있습니다. 남미, 중동 및 아프리카는 뒤처져 있지만, 기술 격차를 해소하기 위한 종량제 요금제나 기존 시맨틱 모델에 대한 관심이 높아지고 있습니다. 그러나 연결성 문제와 예산 부족으로 인해, 이러한 지역에서의 도입은 여전히 제한되고 있습니다. 이러한 과제가 존재하기는 하지만, AI 기반 솔루션의 장점에 대한 인식이 높아지고 디지털 인프라에 대한 투자가 확대됨에 따라, 해당 지역 시장 성장이 점차 가속화될 것으로 예측됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the visual analytics market size is projected to expand from USD 10.16 billion in 2025 and USD 11.86 billion in 2026 to USD 26.78 billion by 2031, registering a CAGR of 17.69% between 2026 and 2031.

This report is Segmented by Component (Software, and Services), Deployment Mode (On-Premises, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (BFSI, IT and Telecom, Retail and Consumer Goods, and More), Application (Sales and Marketing, Finance and Operations, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Visual Analytics Market Trends and Insights

Growing Cloud-Based Data Generation

Enterprise data estates are expanding rapidly, with about 90% residing in unstructured silos by early 2026. Zero-copy query patterns now let users analyze that data in place, cutting extract-transform-load overhead and avoiding hyperscaler lock-in. GPU-accelerated engines accelerate unstructured analytics, while unified semantic layers merge structured and unstructured metadata, enabling projects to move from pilot to production. Hybrid architectures remain entrenched because data residency rules, latency needs, and price-performance trade-offs make single-cloud strategies risky.

Rising Demand for Self-Service BI Platforms

Organizations that emphasize user experience, governance, and executive sponsorship lift casual-user adoption from 15-25% to 40-60% within six months. Five-year total cost of ownership for mid-market deployments fell to USD 1.0-1.4 million in 2025, aided by consumption pricing and automated lineage. Yet 70% of projects still stall because cultural change, data quality, and training gaps outpace tooling. Federated, zero-copy designs blend local agility with centralized control, while semantic layers enforce row-level security and consistent metrics.

High Total Cost of Ownership for SMEs

Mid-market analytics projects cost USD 1.0-1.5 million over five years, with service fees and infrastructure often dwarfing license spend. Under-utilized deployments push per-user expense from USD 1,000 to USD 30,000, deterring adoption. Hidden cloud costs range from USD 1,000 to more than USD 50,000 per month, while ongoing maintenance consumes 10-15% of implementation budgets. Consumption-based Spark billing can trim 40% for bursty workloads, but SMEs still need granular usage monitoring to prevent bill shocks

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of IoT Devices Driving Real-Time Analytics

- Increasing Regulatory Reporting Requirements

- Data Quality and Silos Limiting Insights

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured 71.73% of 2025 revenue by monetizing licenses for cloud-native BI suites, semantic modeling engines, and embedded analytics. These tools have become essential for organizations aiming to streamline decision-making processes and enhance operational efficiency. However, services are expanding at a 19.49% CAGR as enterprises increasingly demand implementation blueprints, managed operations, and data-literacy programs. These services are designed to double user adoption within six months, addressing critical skills gaps across finance, supply chain, and revenue cycle functions. Professional services typically consume USD 250,000-750,000 in mid-market projects, while outcome-based contracts tie fees to measurable KPI gains, such as 2-4-point net-collection improvements, ensuring a clear return on investment for clients.

The visual analytics services market is projected to grow faster than the software market, driven by the integration of AI-powered data-prep assistants and proactive monitoring agents. These innovations significantly reduce manual effort, enabling organizations to focus on strategic initiatives. Partnerships like Tableau Einstein Alliance and Qlik service collaborations now offer bundled solutions, including migration automation, semantic-layer design, and comprehensive training modules. These bundled offerings enhance partner stickiness, streamline deployment processes, and reduce time-to-insight, making them highly attractive to enterprises looking to accelerate their analytics capabilities.

Cloud workloads accounted for 63.43% of 2025 spending and are forecast to compound at 18.49% through 2031 as Delta Lake, Parquet, and Apache Iceberg standardization curbs vendor lock-in. This growth is driven by the increasing adoption of cloud-native technologies that offer scalability, flexibility, and cost efficiency. Microsoft Fabric's Direct Lake and SAP's live Snowflake connectors illustrate a shift toward zero-copy query paths that align governance and latency needs without wholesale replication. These advancements enable organizations to streamline data processing and analytics while maintaining compliance with data governance policies. Autoscale billing for Spark workloads lowers total cost of ownership, making cloud viable for bursty analytics and experimentation, particularly in industries requiring rapid data insights.

On-premise instances persist in regulated industries and sovereign-AI deployments where data residency and air-gapped operations remain mandatory. These industries, such as healthcare, finance, and government, prioritize data security and compliance, which require on-premises solutions. Hybrid approaches hence dominate architecture roadmaps, combining the benefits of cloud scalability with the control of on-premise systems. Vendors that enable policy coordination across environments gain share because they reduce migration risk and compliance exposure. This hybrid model allows organizations to optimize their IT infrastructure while addressing specific regulatory and operational requirements.

Geography Analysis

North America held 38.23% of 2025 revenue, supported by USD 357 billion in U.S. government technology budgets and 3,611 documented federal AI use cases. The region benefits from strong investments in cloud infrastructure, AI-driven solutions, and digital transformation initiatives across various industries. Agencies are accelerating the adoption of cloud foundations, unified data fabrics, and model-assurance tooling, favoring vendors that deliver provenance, auditability, and U.S.-hosted regions. Additionally, legacy modernization needs, Buy American stipulations, and transparency in software bill of materials amplify demand for platforms that offer verifiable sourcing and explainable outputs. The presence of major technology providers and a robust regulatory framework further strengthens the region's position in the market.

Asia-Pacific is the fastest-growing region, with a 18.69% CAGR through 2031. TSovereign AI rules, on-device inference requirements, and the increasing adoption of low-code platforms in manufacturing clusters are driving the region's growth. These factors, combined with the implementation of OPC-UA and MQTT standards, enable factory-wide predictive models and enhance operational efficiency. Edge deployments are gaining traction as they reduce network costs and latency, while localized interfaces broaden user bases in languages such as Japanese, Korean, and Mandarin. The region's diverse industrial base, coupled with government initiatives to promote digitalization, positions it as a key growth area for the market.

Europe maintains steady momentum due to GDPR and data-sovereignty laws that cement hybrid architectures. The region's focus on data privacy and compliance drives the adoption of solutions that align with stringent regulatory requirements. Hybrid architectures, which combine on-premises and cloud-based systems, are increasingly preferred to ensure data security and operational flexibility. South America, the Middle East, and Africa are trailing but show rising interest in consumption pricing and pre-built semantic models to offset skills gaps. However, connectivity constraints and budget pressures still temper uptake in these regions. Despite these challenges, growing awareness of the benefits of AI-driven solutions and increasing investments in digital infrastructure are expected to support gradual market growth in these areas.

- Tableau Software LLC

- QlikTech International AB

- TIBCO Software Inc.

- SAS Institute Inc.

- Microsoft Corporation

- International Business Machines Corporation

- Oracle Corporation

- SAP SE

- MicroStrategy Incorporated

- Sisense Inc.

- Alteryx Inc.

- Domo Inc.

- Dundas Data Visualization Inc.

- Looker Data Sciences LLC

- Zoho Corporation Pvt. Ltd.

- Infor, Inc.

- Information Builders, Inc.

- Yellowfin International Pty Ltd

- Board International SA

- ThoughtSpot Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Cloud-based Data Generation

- 4.2.2 Rising Demand for Self-Service BI Platforms

- 4.2.3 Proliferation of IoT Devices Driving Real-Time Analytics

- 4.2.4 Increasing Regulatory Reporting Requirements

- 4.2.5 Emergence of Low-Code Visual Analytics Tools

- 4.2.6 Edge Analytics Adoption in Industrial Settings

- 4.3 Market Restraints

- 4.3.1 High Total Cost of Ownership for SMEs

- 4.3.2 Data Quality and Silos Limiting Insights

- 4.3.3 Shortage of Skilled Data Visualization Professionals

- 4.3.4 Vendor Lock-in Concerns with Proprietary Platforms

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Application

- 5.3.1 Sales and Marketing

- 5.3.2 Finance and Accounting

- 5.3.3 Operations

- 5.3.4 Supply Chain and Logistics

- 5.3.5 Human Resources

- 5.3.6 Customer Service and Support

- 5.3.7 Other Applications

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-User Industry

- 5.5.1 Banking, Financial Services and Insurance (BFSI)

- 5.5.2 Retail and eCommerce

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Manufacturing

- 5.5.5 Information Technology and Telecommunications

- 5.5.6 Government and Public Sector

- 5.5.7 Media and Entertainment

- 5.5.8 Energy and Utilities

- 5.5.9 Transportation and Logistics

- 5.5.10 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Tableau Software LLC

- 6.4.2 QlikTech International AB

- 6.4.3 TIBCO Software Inc.

- 6.4.4 SAS Institute Inc.

- 6.4.5 Microsoft Corporation

- 6.4.6 International Business Machines Corporation

- 6.4.7 Oracle Corporation

- 6.4.8 SAP SE

- 6.4.9 MicroStrategy Incorporated

- 6.4.10 Sisense Inc.

- 6.4.11 Alteryx Inc.

- 6.4.12 Domo Inc.

- 6.4.13 Dundas Data Visualization Inc.

- 6.4.14 Looker Data Sciences LLC

- 6.4.15 Zoho Corporation Pvt. Ltd.

- 6.4.16 Infor, Inc.

- 6.4.17 Information Builders, Inc.

- 6.4.18 Yellowfin International Pty Ltd

- 6.4.19 Board International SA

- 6.4.20 ThoughtSpot Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment