|

시장보고서

상품코드

2062266

건설용 실리콘 실란트 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Construction Silicone Sealant - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

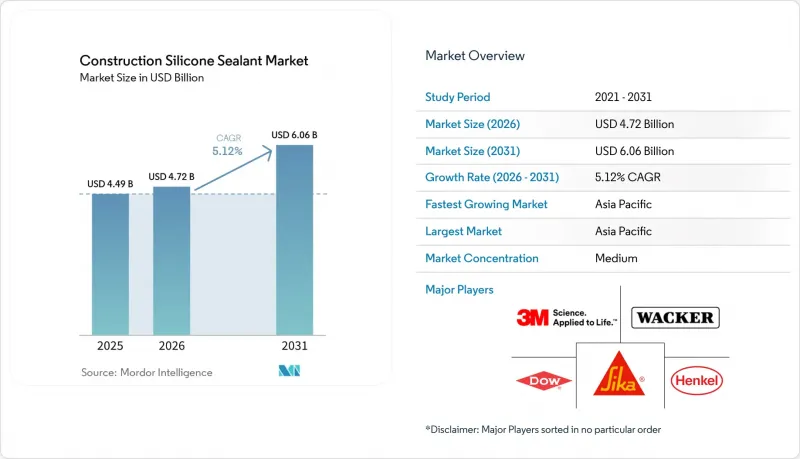

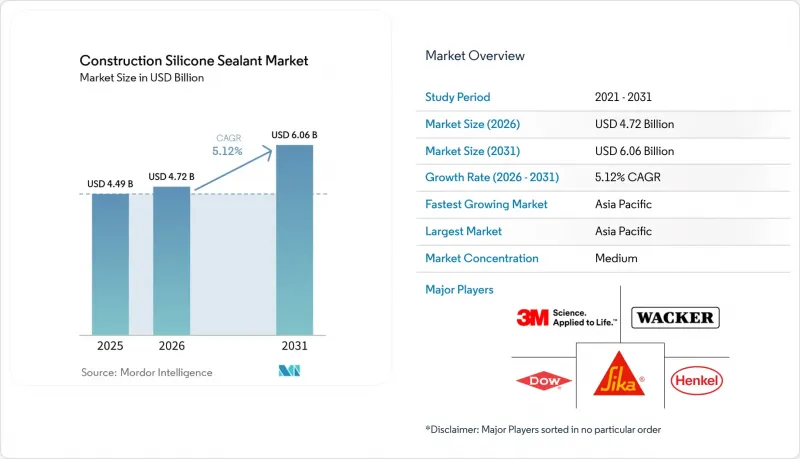

Mordor Intelligence에 의하면, 건설용 실리콘 실란트 시장 규모는 2025년 44억 9,000만 달러에서 2026년에는 47억 2,000만 달러로 확대되어 2031년까지 60억 6,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 5.12%로 성장할 전망입니다.

본 보고서는 제품 유형(중성 경화형 실리콘 실란트, 아세톡시 경화형 실리콘 실란트 등), 용도(이음매 충전, 유리 시공 및 방수 등), 최종 사용자(주택 건설 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 건설용 실리콘 실란트 시장 동향 및 분석

주택 및 상업 건축 분야 수요 증가

2026년, 미국의 신규 사무실 인테리어 공사비는 평방피트당 149달러에 달하고, 2025년 대비 5.5% 증가했습니다. 이러한 추세에 따라, 개발사들은 유지보수 빈도를 줄이기 위해 내구성이 뛰어난 실란트를 채택하고 있습니다. 중국에서는 조립식 건축의 의무화로 인해 변형이 심한 이음매 시공이 공장 환경으로 전환되고 있으며, 이곳에서는 주로 중성 경화형 실리콘이 사용되고 있습니다. 아시아의 주요 도시 주택 소유자들은 저렴한 아크릴계 제품에서는 일반적으로 찾아볼 수 없는 바탕면의 변색을 방지하는 저취성 제품을 선택하고 있습니다. 노동 시장이 핍박하는 가운데, 프로젝트 매니저는 자재 가격뿐만 아니라 총 설치 비용에 중점을 두고 있습니다. 이러한 요인들이 복합적으로 작용하여, 고급 주거용 타워와 A급 상업 공간에서 실리콘의 위상을 높이고 있습니다.

신흥국의 인프라 붐

인도 노이다 국제공항과 델리 메트로 5단계(A) 공사는 총 27억 달러가 넘는 토목 비용을 수반하며, ±25%의 변형에 대응하고 더 높은 내화 성능을 갖춘 인증 실란트가 필요합니다. 마찬가지로, 사우디아라비아의 킹 살만 국제공항과 두바이의 알 막툼 공항 확장 공사(총 640억 달러 이상)에서는 가혹한 사막 환경을 견디기 위해 자외선 안정성이 뛰어나고 모래에 강한 실리콘 실란트가 요구되고 있습니다. 이러한 대규모 프로젝트는 로트 간 일관성을 확보하고 현장에서 기술 지원을 제공할 수 있는 공급업체에게 수년까지 비즈니스 기회를 제공합니다. 또한, 설계 리드타임의 장기화는 수직 통합이나 장기적인 금속 실리콘 계약을 통해 원자재 가격 변동 위험을 완화하고 있는 제조업체에게 유리하게 작용합니다.

실리콘 및 첨가제의 원자재 가격 변동

2026년 1분기, 중국의 염소-알칼리 공장 가동 중단과 금속 실리콘에 대한 관세 인상을 배경으로, 디메틸디클로로실란 가격은 전년 동기 대비 28% 상승했습니다. 이러한 가격 상승은 현물 시장에서의 구매에 의존하고 있는 배합 제조업체에 영향을 미쳤습니다. 또한, 2025년 하반기에는 휴메드 실리카공급 부족으로 인해 리드타임이 4주에서 12주로 연장되었습니다. 이러한 상황은 수직 통합형 기업에게는 유리하게 작용한 반면, 소량 수탁 업체에게는 과제가 되었습니다. 이러한 시장 환경에 대응하여, 와커사는 2026년 4월에 5% 전후의 가격 인상을 발표했습니다. 동시에, 다우사는 경쟁력을 유지하기 위해 실록산 생산을 비용이 높은 유럽에서 다른 지역으로 이전했습니다. 이러한 시장 역학은 프로젝트 예산 수립에 불확실성을 초래하며, 프로젝트 사양이 허용하는 한도 내에서 비용 효율성이 더 높은 화학 물질로의 전환으로 이어질 수 있습니다.

부문별 분석

2025년, 중성 경화형 제품은 양극 산화 알루미늄, 코팅 유리, 천연석과의 호환성을 바탕으로 건설용 실리콘 실란트 시장의 44.11%를 차지했습니다. 한편, 아세톡시 경화형 제품 시장은 2031년까지 연평균 성장률(CAGR) 5.66%로 성장할 것으로 전망됩니다. 이는 신속한 습기 경화 및 30-40% 저렴한 단가를 선호하는 동남아시아 및 라틴아메리카의 주택 건설업체들에 의해 주도되고 있습니다. 옥심계 및 알콕시계는 식수 시스템이나 자동차용 엘라스토머 접착과 같은 특수한 요구 사항을 충족하는 보다 틈새 시장을 차지하고 있습니다. 모멘티브(Momentive)가 2025년 출시 예정인 바이오 유래 상온 가황(RTV) 제품군을 대표로 하는 프리미엄 부문은 제품에 내재된 탄소(엔보디드 카본)에 대한 공개 요구에 부응하기 위해 지속적으로 발전하고 있습니다. 검증된 지속가능성을 지향하는 이 경쟁은 주류 유리 시공 분야에서 아세톡시계 제품의 성장에 대응하는 것을 목표로 합니다.

이러한 제품 구성의 변화는 직접적인 대체라기보다는 가격에 따른 계층화를 여실히 보여주고 있습니다. 널리 사용되는 아세톡시계 제품인 다우(Dow)사의 ‘DOWSIL 791’은 동남아시아 창호 시공의 절반 이상을 차지하고 있으며, 이는 대규모 주택 건설에서 비용 효율성을 중시하는 의사결정을 반영하고 있습니다. 한편, 와커(Wacker)사의 알콕시 경화형 ‘ELASTOSIL A07’은 미국 식품의약국(FDA)의 연방규정집(CFR) 제21편 제177.2600조의 위생 기준을 준수하고 있어, 식품 가공용 클린룸에서 수요를 확보하고 있습니다. 또한, 옥심 경화형 제품은 로봇 압출 성형으로 제작된 다공성 기판에 대한 뛰어난 접착력 덕분에 3D 프린팅 콘크리트 파사드 분야에서 주목받고 있습니다. 건축 기준이 구체적인 이용 사례에 따라 다양화되는 가운데, 단일 화학 기술이 모든 틈새 시장을 독점하지는 못할 것으로 예상되며, 다품목 포트폴리오의 중요성이 부각되고 있습니다.

지역별 분석

2025년, 아시아태평양은 전 세계 매출의 46.78%를 차지해, 2031년까지 연평균 성장률(CAGR) 6.11%로 성장하여 건설용 실리콘 실란트 시장에서 주도적인 위치를 유지할 것으로 전망됩니다. 중국의 조립식 건축에 대한 집중과 인도의 항공 산업 확대는 안정적인 수요를 보여주고 있으며, 해안 지역 성에서는 국내 실란트 소비량의 40% 이상을 차지하고 있습니다. 현지에 혼합 공장을 보유한 지역 제조업체들은 리드타임 단축 및 국가 프로젝트에서의 우선적 지위라는 이점을 누리고 있어, 수입에 의존하는 경쟁사들에게는 과제가 되고 있습니다.

북미에서는 사무실 공간이 주거용으로 전환되는 추세가 나타나면서 도시 경관이 변화하고 있습니다. 2025년에는 공실률이 개선되고, 인테리어 공사비 상승으로 인해 빈번한 재시공의 필요성을 줄일 수 있는 고품질이면서 내구성이 뛰어난 자재에 대한 수요가 증가하고 있습니다. 또한, 정부 건물에 대한 연방 정부의 에너지 성능 규제로 인해 리모델링 투자가 고성능 실리콘 실란트로 집중되면서, 신축 착공 건수가 정체된 상황에서도 안정적인 수요가 확보되고 있습니다.

유럽에서는 신규 건설보다 규제 체계가 더 중요한 역할을 하고 있습니다. ‘기업 지속가능성 보고 지침(CSRD)’ 및 ‘건축물 에너지 성능 지침(EPBD)’에 따라 저휘발성 유기화합물(VOC) 제품이자 탄소 인증을 받은 제품에 대한 조달이 촉진되고 있으며, 추적 가능한 공급망을 갖춘 공급업체는 가격 면에서 우위를 점하고 있습니다. 거시경제의 성장세는 여전히 둔화되고 있지만, 노후화된 공영주택의 개보수 공사로 인해 외장재 및 단열재의 이음재에 대한 수요가 증가하고 있습니다. 남미 및 중동 및 아프리카는 시장 규모는 작지만 급속한 성장을 보이고 있습니다. 두바이의 알 막툼 공항이나 리야드의 킹 살만 공항 등에서는 건조한 기후에 맞추어 설계된 자외선 안정성 실런트가 수백만 미터 규모로 사용될 전망입니다. NEOM의 거울 같은 외관은 주변 온도 45℃에서의 내사침식성 및 광학적 투명도 등 새로운 기술적 요건을 제시하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the construction silicone sealant market size is expected to increase from USD 4.49 billion in 2025 to USD 4.72 billion in 2026 and reach USD 6.06 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

This report is Segmented by Product Type (Neutral-Cure Silicone Sealants, Acetoxy-Cure Silicone Sealants, and More), Application (Joint Sealing, Glazing and Weatherproofing, and More), End-User (Residential Construction and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Construction Silicone Sealant Market Trends and Insights

Rising Demand from Residential and Commercial Construction

In 2026, new office fit-out costs in the United States reached USD 149 per square foot, reflecting a 5.5% increase from 2025. This rise is driving developers to adopt longer-life sealants to reduce maintenance schedules. In China, prefabrication mandates are directing high-movement joints into factory environments, where neutral-cure silicones are predominantly used. Homeowners in tier-1 Asian cities are selecting low-odor products that resist substrate staining, a feature not commonly found in lower-cost acrylics. As labor markets tighten, project managers are focusing on total installed costs rather than just material prices. These factors collectively enhance silicone's positioning in premium residential towers and Grade-A commercial spaces.

Infrastructure Boom in Emerging Economies

India's Noida International Airport and Delhi Metro Phase V(A) represent a combined civil expenditure exceeding USD 2.7 billion, requiring sealants certified for +-25% movement and higher fire ratings. Similarly, expansions at Saudi Arabia's King Salman International and Dubai's Al Maktoum airports, with a combined value exceeding USD 64 billion, demand UV-stable, sand-resistant silicone joints to withstand extreme desert conditions. These large-scale projects provide multi-year opportunities for suppliers capable of ensuring batch consistency and offering on-site technical support. Additionally, extended design lead times benefit manufacturers that mitigate raw-material price volatility through backward integration or long-term silicon-metal contracts.

Volatility in Silicone and Additive Raw-Material Prices

In Q1 2026, prices for Dimethyldichlorosilane increased by 28% year-on-year, driven by outages at Chinese chlor-alkali units and higher tariffs on silicon metal. This price rise has impacted formulators reliant on spot market purchases. Additionally, shortages in fumed silica extended lead times from four to twelve weeks in late 2025. This situation benefited vertically integrated companies while creating challenges for small-batch contractors. In response to these market conditions, Wacker announced a mid-single-digit price increase in April 2026. Concurrently, Dow shifted its siloxane production from high-cost Europe to other regions to maintain competitiveness. These market dynamics introduce uncertainties in project budgeting and may lead to a shift toward more cost-effective chemistries when project specifications allow.

Other drivers and restraints analyzed in the detailed report include:

- Growing Use in Green Buildings and Sustainable Architecture

- Surge in Unitized Curtain-Wall Adoption (High-Movement Joints)

- Competition from Acrylic, Polyurethane, and Polysulfide Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, neutral-cure products accounted for 44.11% of the construction silicone sealant market, supported by their compatibility with anodized aluminum, coated glass, and natural stone. Meanwhile, the market for acetoxy-cure grades is projected to grow at a 5.66% compound annual growth rate (CAGR) through 2031, driven by residential builders in Southeast Asia and Latin America who prefer the rapid moisture cure and a 30-40% lower unit cost. Oxime- and alkoxy-cure chemistries occupy smaller niches, catering to specialized needs like potable-water systems and automotive elastomer bonding. Premium tiers, exemplified by Momentive's 2025 bio-attributed room-temperature vulcanizing (RTV) range, are evolving to meet embodied-carbon disclosure demands. This competitive shift towards verified sustainability aims to address acetoxy-cure's growth in mainstream glazing applications.

The evolving product mix highlights a pricing hierarchy rather than a direct substitution. Dow's DOWSIL 791, a widely used acetoxy product, dominates over half of Southeast Asia's window-perimeter installations, reflecting cost-driven decisions in mass housing. On the other hand, Wacker's alkoxy-cure ELASTOSIL A07, compliant with Food and Drug Administration (FDA) 21 Code of Federal Regulations (CFR) 177.2600 sanitization standards, secures demand from food-processing cleanrooms. Additionally, oxime-cure products are gaining traction in 3D-printed concrete facades due to their superior adhesion on porous substrates crafted through robotic extrusion. As building codes diversify based on specific use cases, no single chemistry is expected to dominate all niches, ensuring the relevance of multigrade portfolios.

Geography Analysis

In 2025, the Asia-Pacific region accounted for 46.78% of global revenue and is projected to grow at a 6.11% compound annual growth rate (CAGR) through 2031, maintaining its leadership in the construction silicone sealant market. China's focus on prefabrication and India's expanding aviation sector indicate consistent demand, with coastal provinces consuming over 40% of the nation's sealants. Regional producers with local mixing plants benefit from shorter lead times and preferred status in state projects, creating challenges for import-dependent competitors.

North America is experiencing a shift as office spaces convert to residential use, altering urban landscapes. Vacancy rates improved in 2025, and rising fit-out costs have driven demand for premium, durable materials, reducing the need for frequent resealing. Additionally, federal energy performance mandates for government buildings are directing retrofit investments into high-performance silicone joints, ensuring stable demand even as new construction levels off.

In Europe, regulatory frameworks play a more significant role than new construction. The Corporate Sustainability Reporting Directive (CSRD) and the Energy Performance of Buildings Directive (EPBD) are driving procurement toward low-volatile organic compound (VOC), carbon-verified products, while suppliers with traceable supply chains gain pricing advantages. Although macroeconomic growth remains slow, retrofitting aging social housing is increasing demand for cladding and insulation joints. South America and the Middle East-Africa, while smaller markets, are showing rapid growth. Airports such as Dubai's Al Maktoum and Riyadh's King Salman are expected to utilize millions of linear meters of UV-stable sealants designed for arid climates. NEOM's mirrored facades are setting new technical requirements, including sand-erosion resistance and optical clarity at ambient temperatures of 45 °C.

- 3M

- Arkema

- Beijing Zhongtian

- CHEMENCE

- Dow

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- Mapei

- Momentive

- Pecora Corporation

- Pidilite Industries Ltd.

- RPM International, Inc.

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Tremco

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand From Residential and Commercial Construction

- 4.2.2 Growing Use in Green Buildings and Sustainable Architecture

- 4.2.3 Infrastructure Boom in Emerging Economies

- 4.2.4 Excellent Weatherability and Durability of Silicone Sealants

- 4.2.5 Adoption of High-movement Sealants for 3-D-printed Building Facades

- 4.3 Market Restraints

- 4.3.1 Volatility in Silicone and Additive Raw-material Prices

- 4.3.2 Availability of Acrylic, Polysulfide, and Polyurethane Substitutes

- 4.3.3 Regulatory Pressure on VOC and Tin-catalyst Formulations

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Neutral-cure silicone sealants

- 5.1.2 Acetoxy-cure silicone sealants

- 5.1.3 Oxime-cure silicone sealants

- 5.1.4 Alkoxy-cure silicone sealants

- 5.2 By Application

- 5.2.1 Joint sealing (expansion and movement joints)

- 5.2.2 Glazing and weatherproofing

- 5.2.3 Insulation and cladding

- 5.2.4 Kitchen and sanitary

- 5.2.5 Fire-resistant applications

- 5.2.6 Other Applications (sound-proofing, electrical, etc.)

- 5.3 By End-user

- 5.3.1 Residential construction

- 5.3.2 Commercial construction

- 5.3.3 Industrial construction

- 5.3.4 Infrastructure (bridges, roads, airports)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Beijing Zhongtian

- 6.4.4 CHEMENCE

- 6.4.5 Dow

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG and Co. KGaA

- 6.4.8 Mapei

- 6.4.9 Momentive

- 6.4.10 Pecora Corporation

- 6.4.11 Pidilite Industries Ltd.

- 6.4.12 RPM International, Inc.

- 6.4.13 Shin-Etsu Chemical Co., Ltd.

- 6.4.14 Sika AG

- 6.4.15 Soudal Group

- 6.4.16 Tremco

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Growth Potential in Prefabricated and Modular Construction