|

시장보고서

상품코드

2062267

냉간 압연 코일강 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cold-Rolled Steel Coil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

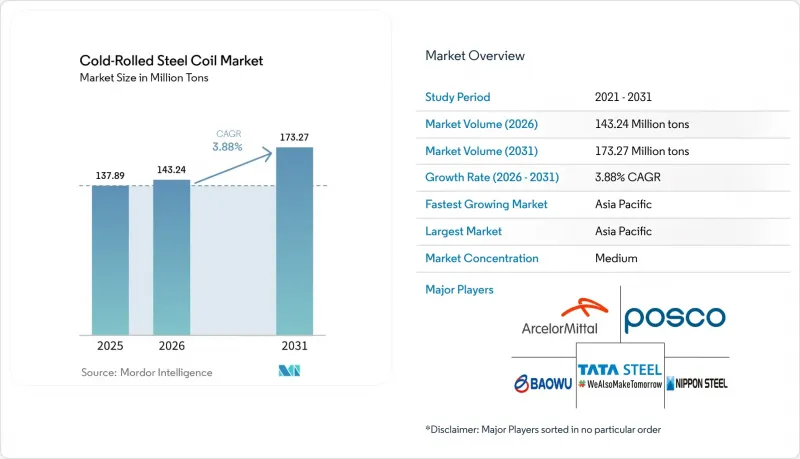

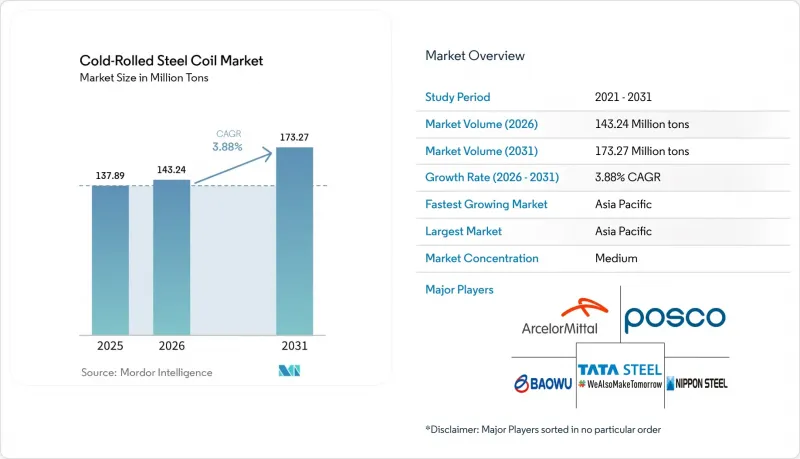

냉간 압연 코일강 시장 규모는 2025년 1억 3,789만 톤으로 평가되었습니다. 2026년에는 1억 4,324만 톤으로 확대되어 2031년까지 1억 7,327만 톤에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 3.88%를 나타낼 전망입니다.

본 보고서는 등급(저탄소강, 고탄소강, 고강도 저합금(HSLA)강 등), 용도(자동차 차체 및 구조 부품, 가정용 가전제품, 산업용 기계·설비 등), 그리고 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 수량(톤) 기준으로 제시되어 있습니다.

세계의 냉간 압연 코일강 시장 동향 및 분석

자동차 및 가전 업계 수요 증가

2025년에는 배터리식 전기차의 생산 대수가 1,400만 대에 달했으며, 각 플랫폼에서는 배터리의 무게를 상쇄하고 충돌 안전 기준을 충족하기 위해 기존 내연기관 차량에 비해 15%-20% 더 많은 AHSS가 사용되게 되었습니다. SSAB는 2025년, 인장 강도가 1,500 MPa를 초과하는 전기차용 최적화 AHSS를 출시함으로써, 자동차 제조업체들이 구조적 무결성을 유지하면서 판 두께를 10%-15% 줄일 수 있게 되었습니다. 중국과 인도의 냉장고 및 세탁기 제조업체들은 기존의 0.6-0.7mm 두께에서 0.4-0.5mm 두께의 도장 코일로 전환함으로써, 자재 비용을 최대 12% 절감하는 동시에 에너지 라벨에 따른 불이익을 줄였습니다. 이 두 가지 수요가 성숙한 경제권에서 자동차 조립량이 정체된 상황에서도 냉연강판 코일 시장을 지탱하고 있습니다. 엄격한 공차 기준에 따른 압연 및 첨단 코팅 기술을 보유한 제철소는 이익률 확대에 있어 가장 유리한 입장에 있는 반면, 범용 철강 제조업체들은 수입 경쟁의 심화에 직면해 있습니다.

건설 및 인프라 프로젝트에서의 활용 확대

북미의 건축 기준에 따르면, 2024년부터 2025년에 걸쳐 다층 건물 및 내진 용도로 냉간 성형 강철 프레임이 채택되면서, 해당 수요가 단독주택의 범위를 넘어 확대되었습니다. 버지니아주, 텍사스주, 아일랜드에서 진행된 데이터센터 건설만으로도 2025년에는 골조, 공조 덕트, 케이블 트레이 용도로 약 120만 톤의 코일이 소비되었습니다. GCC 국가들에서는 2025년에 철강 수요 증가세가 가속화되었으며, 냉연 제품이 태양광 발전소의 지붕 자재나 해수 담수화 플랜트의 외장재로 활용되었습니다. 유럽 및 북미의 모듈식 건축은 연간 30만-40만 톤 수요 증가를 가져오고 있지만, 가격에 민감한 경향이 지속되고 있어, 철강 프리미엄이 골조 비용의 20%를 초과할 경우 공급업체는 대체재 사용의 위험에 직면하게 됩니다. 규제 조화와 노동력 부족은 계속해서 냉간 성형 솔루션을 뒷받침하고 있으며, 자동차 이외의 분야에서 냉연강 코일 시장의 성장세를 지탱하고 있습니다.

원자재 가격 변동

2025년, 철광석은 톤당 90-130달러에 거래된 반면, 미국의 고철 가격은 톤당 300-450달러 범위에서 형성되어, 자체 자원을 보유하지 않은 생산자들의 이익률을 200-300베이시스포인트 압박했습니다. 타타 스틸이나 클리블랜드 클리프스와 같은 일체형 제철소는 내부 이전 가격을 통해 가격 변동의 영향을 완화했지만, 무역사 계열 제철소는 현물 시장의 영향에 노출되었습니다. 전기용광로(EAF) 제조업체들은 고철 가격이 최저치를 기록했을 때는 혜택을 보았으나, 고철 가격이 선철 가격보다 100달러 높아지자 비용 면에서의 우위를 잃게 되었습니다. 이러한 불균형은 2027년까지 지속되어 냉간 압연 코일강 시장의 가격 협상을 복잡하게 만들 것입니다.

부문별 분석

2025년 냉연강판 코일 시장에서 저탄소강은 출하량의 46.61%를 차지했으나, 자동차 제조업체들이 차량 평균 배기가스 목표를 달성하기 위해 기존 강종에서 전환함에 따라, 고강도 강판(AHSS)은 2031년까지 연평균 4.55%의 성장률을 보일 것으로 전망됩니다.

스테인리스 냉연 코일은 여전히 틈새 시장이지만 수익성이 높은 부문이며, 특히 식품 장비 및 화학 처리 분야에서 아웃컴프(Outcomp)와 SSAB가 EU의 에코디자인 기준을 충족하는 저탄소 강종을 공급함으로써 40%-60%의 이익률 향상을 실현하고 있습니다. 고탄소강 및 HSLA강은 전동화로 인해 구동계에서 사용되는 강재량이 감소함에 따라 전반적인 성장세에서 뒤처지고 있습니다. 제철소는 AHSS나 특수 스테인리스 스틸을 생산할 수 없기 때문에 냉연강 코일 시장 내에서 이익률이 압박받을 위험에 직면해 있습니다.

지역별 분석

아시아태평양은 2025년 생산량의 59.94%를 차지했으며, 인도 및 동남아시아의 생산 능력 확대와 중국의 가전제품 수출을 배경으로 2031년까지 연평균 4.36%의 성장률을 보일 것으로 전망됩니다. 인도에서만 2024년부터 2025년에 걸쳐 타타 스틸, JSW 스틸, AM/NS 인디아, 샴 메탈릭스에서 국내 수요와 EU 수출을 충족하기 위해 350만 톤 규모의 신규 생산 설비가 가동되었습니다. 베트남은 2025년에 800만 톤의 생산 능력에 도달할 전망이며, 그 납품 비용은 동북아시아의 제철소보다 10%-15% 저렴합니다.

북미 냉연강판 시장의 성장은 뉴코어(Newcore)사의 웨스트버지니아주 공장(연산 300만 톤)과 2026년 3월에 발표된 현대제철의 58억 달러 규모 미국 그린필드 전기로(EAF) 프로젝트 등의 투자를 통해 주도되고 있습니다. 멕시코의 페스케리아 복합 시설(연산 150만 톤)은 USMCA(미국·멕시코·캐나다 협정)의 규정에 따라 멕시코를 지역 허브로 자리매김하고 있습니다.

유럽에서는 자동차 생산의 정체와 높은 에너지 비용으로 인해 성장이 둔화되고 있지만, CBAM(탄소국경조정메커니즘)의 인센티브 덕분에 폴란드, 스페인, 이탈리아로의 생산 능력 회귀가 진행되고 있습니다. 남미의 성장은 브라질과 아르헨티나의 자동차 산업 회복이 주도하고 있으며, 중동 및 아프리카에서는 GCC(걸프협력회의) 국가들의 공조 및 건설 수요를 겨냥한 EMSTEEL의 6억 2,500만 디르함 규모의 확장 계획을 비롯해, 사우디아라비아와 UAE의 인프라 프로젝트를 통해 성장이 예상됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the cold-Rolled steel coil market size is expected to increase from 137.89 Million tons in 2025 to 143.24 Million tons in 2026 and reach 173.27 Million tons by 2031, growing at a CAGR of 3.88% over 2026-2031.

This report is Segmented by Grade (Low-Carbon Steel, High-Carbon Steel, High-Strength Low-Alloy (HSLA) Steel, and More), Application (Automotive Body and Structural Parts, Consumer Appliances, Industrial Machinery and Equipment, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Cold-Rolled Steel Coil Market Trends and Insights

Growing Demand From Automotive And Appliance Industries

Battery-electric-vehicle output reached 14 million units in 2025, each platform consuming 15%-20% more AHSS than its internal-combustion predecessor to offset battery mass and meet crash requirements. SSAB launched EV-optimized AHSS in 2025 with tensile strengths beyond 1,500 MPa, allowing automakers to trim gauge thickness 10%-15% while holding structural integrity. Refrigerator and washing-machine makers in China and India shifted to 0.4-0.5 mm pre-painted coil from traditional 0.6-0.7 mm, reducing material costs up to 12% and cutting energy-label penalties. These twin pulls sustain the cold-rolled steel coil market even where vehicle assembly flattens in mature economies. Mills with tight-tolerance rolling and advanced coating are best placed to capture expanding margins, whereas commodity producers face intensified import competition.

Increasing Use In Construction And Infrastructure Projects

North American building codes adopted cold-formed steel framing for multi-story and seismic applications in 2024-2025, widening addressable demand beyond single-family housing. Data-center construction in Virginia, Texas, and Ireland alone consumed roughly 1.2 million tons of coil in 2025 for framing, HVAC ducting, and cable trays. GCC countries registered an increase in steel-demand growth in 2025, channeling cold-rolled products into solar-farm roofing and desalination cladding. Modular building in Europe and North America adds 300,000-400,000 tons annually but stays price sensitive, exposing suppliers to substitution if steel premiums exceed 20% of framing cost. Regulatory alignment and labor shortages continue to favor cold-formed solutions, supporting the cold-rolled steel coil market trajectory in non-automotive sectors.

Volatile Raw-Material Prices

Iron ore traded between USD 90 and USD 130 per ton in 2025, while U.S. scrap ranged from USD 300 to USD 450 per ton, squeezing margins by 200-300 basis points for producers lacking captive resources. Integrated mills such as Tata Steel or Cleveland-Cliffs cushioned swings through internal transfer pricing, whereas merchant mills faced spot-market exposure. EAF operators benefited during scrap troughs but lost cost edge when scrap rose USD 100 above pig-iron parity. This asymmetry will persist into 2027, complicating price negotiations in the cold-rolled steel coil market.

Other drivers and restraints analyzed in the detailed report include:

- High-Strength And Surface-Finish Advantages Over Hot-Rolled Steel

- Manufacturing Expansion In Emerging Economies

- Energy-Intensive Processing And Carbon Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Low-carbon steel controlled 46.61% of 2025 volume in the cold-rolled steel coil market, yet Advanced High-Strength Steel (AHSS) is forecast to grow at 4.55% to 2031 as OEMs replace conventional grades to meet fleet-average emission targets.

Stainless cold-rolled coil remains a niche but lucrative slice, especially for food equipment and chemical processing, where Outokumpu and SSAB supply low-carbon variants meeting EU ecodesign norms at 40%-60% margin uplifts. High-carbon and HSLA steels trail overall growth as electrification reduces drivetrain steel content. Mills are unable to produce AHSS or specialty stainless risk margin compression within the cold-rolled steel coil market.

Geography Analysis

Asia-Pacific commanded 59.94% of 2025 volume, expanding at 4.36% through 2031 on the back of Indian and Southeast Asian capacity additions and Chinese appliance exports. India alone commissioned 3.5 million tons of new capacity across Tata Steel, JSW Steel, AM/NS India, and Shyam Metalics during 2024-2025 to satisfy domestic demand and EU-bound exports. Vietnam reached 8 million tons capacity in 2025 with delivered costs 10%-15% under Northeast Asian mills.

North America's cold-rolled steel coil market's growth is propelled by EAF investments such as Nucor's 3-million-ton West Virginia mill and Hyundai Steel's USD 5.8 billion U.S. greenfield EAF announced in March 2026. Mexico's 1.5 million-ton Pesqueria complex positions the country as a regional hub under USMCA rules.

Europe faces slower growth given stagnant auto output and high energy costs, yet CBAM incentives are triggering capacity reshoring to Poland, Spain, and Italy. South America's growth is led by Brazilian and Argentine automotive recovery, while the Middle East and Africa will advance on Saudi and UAE infrastructure pipelines, including EMSTEEL's AED 625 million expansion targeting GCC HVAC and construction buyers.

- ArcelorMittal

- China Baowu Steel Group Corporation Limited

- Cleaveland-Cliffs Inc.

- CRS Holdings, LLC.

- Hyundai Steel

- JFE Steel Corporation

- JSW Steel

- Nippon Steel Corporation

- Nucor Corporation

- Outokumpu

- POSCO

- Salzgitter Flachstahl GmbH

- SSAB AB

- Tata Steel

- Thyssenkrupp Steel Europe

- United States Steel Corporation.

- Voestalpine Stahl GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand from Automotive and Appliance Industries

- 4.2.2 Increasing Use in Construction and Infrastructure Projects

- 4.2.3 High-Strength and Surface-Finish Advantages over Hot-Rolled Steel

- 4.2.4 Manufacturing Expansion in Emerging Economies

- 4.2.5 Cold-Formed Steel Framing in Modular and Data-Center Builds

- 4.3 Market Restraints

- 4.3.1 Volatile Raw-Material (Iron-Ore And Scrap) Prices

- 4.3.2 Energy-Intensive Processing and Carbon Dioxide Regulations

- 4.3.3 Aluminium and Composites Substitution in Lightweighting

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 Low-Carbon Steel

- 5.1.2 High-Carbon Steel

- 5.1.3 High-Strength Low-Alloy (HSLA) Steel

- 5.1.4 Advanced High-Strength Steel (AHSS)

- 5.1.5 Stainless Steel

- 5.2 By Application

- 5.2.1 Automotive Body and Structural Parts

- 5.2.2 Consumer Appliances

- 5.2.3 Construction (Roofing, Wall Panels, Framing)

- 5.2.4 Industrial Machinery and Equipment

- 5.2.5 Furniture And Storage Systems

- 5.2.6 Packaging (Drums, Barrels, Containers)

- 5.2.7 Electrical And HVAC

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 ArcelorMittal

- 6.4.2 China Baowu Steel Group Corporation Limited

- 6.4.3 Cleaveland-Cliffs Inc.

- 6.4.4 CRS Holdings, LLC.

- 6.4.5 Hyundai Steel

- 6.4.6 JFE Steel Corporation

- 6.4.7 JSW Steel

- 6.4.8 Nippon Steel Corporation

- 6.4.9 Nucor Corporation

- 6.4.10 Outokumpu

- 6.4.11 POSCO

- 6.4.12 Salzgitter Flachstahl GmbH

- 6.4.13 SSAB AB

- 6.4.14 Tata Steel

- 6.4.15 Thyssenkrupp Steel Europe

- 6.4.16 United States Steel Corporation.

- 6.4.17 Voestalpine Stahl GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment