|

시장보고서

상품코드

2062268

임의 파형 발생기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Arbitrary Waveform Generator - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

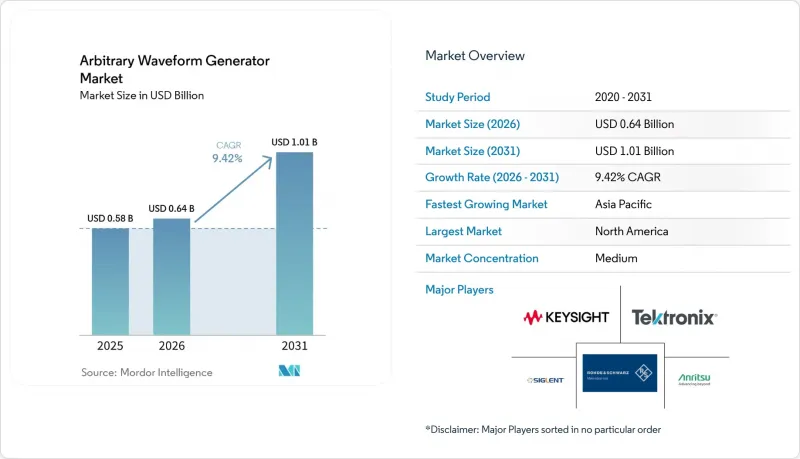

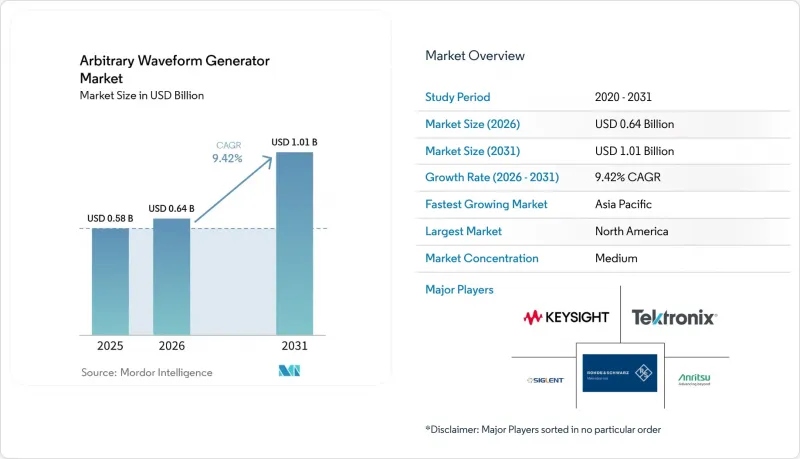

임의 파형 발생기 시장 규모는 2025년 5억 8,000만 달러로 평가되었습니다. 2026년 6억 4,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 9.42%를 나타내, 2031년까지 10억 1,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 기술별(직접 디지털 합성(DDS) AWG, 가변 클럭 AWG 및 복합형 AWG), 제품별(싱글 채널 및 듀얼 채널), 주파수 범위별(1GHz 이하, 1GHz-5GHz 및 5GHz 이상), 최종 사용자 산업(IT 및 통신, 항공우주 및 방위, 기타) 및 지역(북미, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 임의 파형 발생기 시장 동향 및 인사이트

5G 및 6G RF 신호 테스트의 복잡성 증가

6G 조사용 프로토타입은 300GHz에 육박하며, 센싱과 통신을 통합하고 있기 때문에 시험실에서는 서브피코초 수준의 타이밍 정밀도로 테라헤르츠 규모의 파형을 생성할 수 있어야 합니다. 한국과 일본에서 실시한 현장 시험을 통해, 100GHz 대역에서 0.5도 미만의 빔 스티어링 오차가 발생하면 링크 거리가 절반으로 줄어든다는 사실이 확인되었기 때문에 엔지니어들은 현재 외부 소프트웨어가 아닌 임의파형 발생기 내부에서 멀티패스 페이징, 안테나 어레이 결함, 도플러 이동을 재현하고 있습니다. 2024년에 승인된 IEEE 802.11be Wi-Fi 7 개정안 역시 320 MHz 채널과 4096-QAM을 추가했으며, 인접 채널 누설로 인한 마스킹을 방지하기 위해 80 dB의 스퓨리어스 프리 동적 범위를 요구하고 있습니다. 이에 대응하여 각 벤더사는 사용자가 위상 노이즈나 I-Q 불균형을 즉시 조정할 수 있는 FPGA(필드 프로그래머블 게이트 어레이) 기반의 임피어먼트 엔진을 탑재함으로써, 재로딩 시간을 몇 분에서 몇 초로 단축했습니다. 활동은 6G 주파수 대역 할당을 주도하는 지역에 집중되어 있지만, 그 결과로 이루어진 사양의 개선은 모든 주요 무선 연구소에 점차 확산되고 있습니다.

반도체 신속 시제품 제작 및 자동 테스트 장비의 성장

각 파운드리 업체들이 3nm 및 2nm 노드 인증을 서두르는 가운데, 64GT/s 및 80 Gb/s 속도로 PCIe 6.0 및 USB4 버전 2.0 레인을 에뮬레이트하는 파형 발생기가 필요해지면서 자동 테스트에 대한 지출이 급증했습니다. 대만과 한국에 거점을 둔 팹에서는 다이 간 치플릿 링크를 검증하기 위해, 8개 또는 16개의 출력에 걸쳐 펨토초 수준의 코히어런스를 지원하는 멀티채널 플랫폼을 도입했습니다. 납기 지연은 수십억 달러 규모의 제품 출시를 지연시키기 때문에 하이엔드 기기의 리드타임은 6개월 이상으로 늘어났습니다. 북미 및 유럽의 설계 회사들도 테이프아웃을 결정하기 전에 단기간의 시제품이 필요하기 때문에 수요는 0-2년 기간에 집중되어 있으며, 이것이 단기적인 성장 전망을 뒷받침하고 있습니다.

중견 디바이스 OEM 제조업체의 설비 투자 동결

부품 가격 급등과 소비자 수요 부진으로 인해 많은 중견 제조업체의 이익률이 압박을 받으면서, 조사 대상 기업의 38%가 2026년에 예정되어 있던 파형 발생기 업그레이드를 연기했습니다. 이 고객사들은 펌웨어 패치나 타사 보정을 통해 구형 기기의 수명을 연장한 결과, 고가 제품의 미출하 물량이 늘어나는 반면 중가 제품의 출하 대수는 감소했습니다. 현재 각 벤더사는 임대나 종량제 방식의 실험실 이용 서비스를 제공하고 있지만, 데이터 주권 및 지연에 대한 우려로 인해 이러한 서비스의 이용은 중요도가 낮은 작업으로만 제한되고 있습니다. 거시경제 전망이 개선되면, 이러한 영향은 2년 이내에 완화될 것으로 보입니다.

부문별 분석

직접 디지털 신시시스(DDS)는 2025년에 매출 점유율의 55.22%를 차지했습니다. 이는 코히런트 광 변조 및 양자 비트 조작에 필수적인 특성인 결정론적 위상 제어와 80 dBc를 초과하는 스퓨리어스 프리 동적 범위의 이점을 반영한 것입니다. 이러한 우위를 바탕으로, 해당 부문은 임의 파형 발생기 시장에서 규모 면에서의 선도적 위치를 공고히 했으나, 단일 섀시 내에서 가변 클럭의 민첩성과 RF 정밀도를 결합하기 위해 복합 아키텍처 시장은 연평균 성장률(CAGR) 9.10%로 확대될 것으로 전망됩니다.

가변 클럭 모델은 샘플링 속도의 유연성이 위상 일관성보다 우선시되는 상황, 예를 들어 불규칙한 센서 출력을 모방하거나 전력 전자 장치용 펄스 폭 변조(PWM) 신호를 생성하는 경우 등에 여전히 유용합니다. IEEE 1658 개정판에서는 동적 선형성 지표와 관련하여 직접 디지털 합성을 권장하고 있지만, Zurich Instruments의 하이브리드 플랫폼은 연구실이 여러 공급업체의 장비를 구매해야 하는 부담을 덜어주면서도 다양한 이용 사례를 아우를 수 있음을 입증함으로써, 혼합 신호 환경 전반에 걸친 채택을 촉진하고 있습니다.

듀얼 채널 유닛은 2025년에 60.22%의 시장 점유율을 차지하며, 연평균 성장률(CAGR) 10.20%를 나타냈습니다. I-Q 변조기나 듀얼 편파 포토닉스 트랜시버를 구동할 수 있는 능력이 그 우위를 확고히 하고 있으며, 비용 프리미엄이 감소함에 따라 비용에 민감한 연구실에서도 두 개의 출력을 채택하는 추세입니다. 키사이트의 플래그십 모델인 65GS-s는 코히런트 광통신 연구 분야의 벤치마크가 되었으며, 단일 모듈로 400 Gb/s 링크용 4개의 베이스밴드 채널을 생성할 수 있음을 입증했습니다. 이로 인해 고성능 부문에서 임의파형 발생기 시장 점유율 집중도가 높아지고 있습니다.

싱글 채널 장비는 클럭 지터 주입이나 대학 교육용 실험실 등의 용도로 여전히 활용되고 있지만, Liquid Instruments사의 4출력 디바이스 등 통합 플랫폼이 2만 달러 미만의 가격대에 진입함에 따라 그 존재감은 점차 희미해지고 있습니다. 이러한 보급으로 인해 채택 범위는 확대될 뿐만 아니라, 동시에 듀얼 채널이 주류를 이루는 RF 및 포토닉스 검증 분야에서 사실상 표준으로 자리 잡게 될 것입니다.

지역별 분석

2025년, 북미는 매출의 36.82%를 차지했습니다. 이는 확고히 자리 잡은 양자 컴퓨팅 거점, 활발한 항공우주 분야의 조달 활동, 그리고 주요 반도체 설계 기업의 존재에 힘입은 결과입니다. 이러한 요인들이 복합적으로 작용하여, 해당 지역은 임의 파형 발생기 시장에서 지배적인 입지를 공고히 하며 그 선도적 위치를 유지하고 있습니다. 해당 지역의 선진적인 기술 인프라와 강력한 연구개발(R&D) 역량 또한 시장에서의 경쟁력에 한층 더 기여하고 있습니다.

한편, 아시아태평양은 중국, 한국, 일본 등 국가들의 막대한 투자에 힘입어 연평균 성장률(CAGR) 10.67%라는 놀라운 성장이 예상됩니다. 이들 국가는 국내 반도체 제조 시설(팹) 개발과 6G 연구 클러스터 구축에 주력하고 있으며, 이는 해당 지역의 상당한 성장을 이끌 것으로 예측됩니다. 혁신과 인프라 개발에 대한 이러한 전략적 초점은 판매량 성장의 중심을 서서히 동쪽으로 이동시키고 있습니다.

유럽은 독일의 자동차용 레이더 기술에 대한 전문 지식과 유럽연합(EU)의 포토닉스 프로젝트 자금 지원에 힘입어 시장에서 탄탄한 입지를 유지하고 있습니다. 이러한 노력은 해당 지역이 기술 발전에 주력하고 있으며, 경쟁 우위를 유지할 수 있는 능력을 갖추고 있음을 보여줍니다. 한편, 남미와 중동은 시장 개발의 초기 단계에 있거나 전략적으로 중요한 지역으로 부상하고 있습니다. 이 지역들은 향후 몇 년 동안 보급이 확대될 것으로 예상되는 스마트 시티 프로젝트나 위성 백홀 시스템 등 미래의 응용 분야에서 중요한 역할을 수행할 준비가 되어 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the arbitrary waveform generator market size is expected to grow from USD 0.58 billion in 2025 to USD 0.64 billion in 2026 and is forecast to reach USD 1.01 billion by 2031 at a 9.42% CAGR over 2026-2031.

This report is Segmented by Technology (Direct Digital Synthesis AWG, Variable-Clock AWG, and Combined AWG), Product (Single-Channel, and Dual-Channel), Frequency Range (Up To 1 GHz, 1 GHz To 5 GHz, and Above 5 GHz), End-User Industry (IT and Telecommunications, Aerospace and Defense, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Arbitrary Waveform Generator Market Trends and Insights

Rising Complexity of 5G and 6G RF Signal Testing

6G research prototypes reach carriers near 300 GHz and integrate sensing with communications, forcing test labs to generate terahertz-scale waveforms with sub-picosecond timing accuracy. Field trials in South Korea and Japan confirmed that beam-steering errors under 0.5 degrees at 100 GHz halve link range, so engineers now replicate multipath fading, antenna-array defects, and Doppler shifts inside the arbitrary waveform generator itself rather than external software. The IEEE 802.11be Wi-Fi 7 amendment, ratified in 2024, likewise added 320 MHz channels and 4096-QAM, demanding 80 dB spurious-free dynamic range to avoid masking adjacent-channel leakage. Vendors responded by embedding field-programmable-gate-array impairment engines that let users adjust phase noise or I-Q imbalance on the fly, cutting reload times from minutes to seconds. Activity is concentrated in regions leading 6G spectrum allocation, yet the resulting specification uplift is permeating every major wireless laboratory.

Semiconductor Rapid Prototyping and Automated Test-Equipment Growth

Automated-test spending surged as foundries raced to qualify 3 nm and 2 nm nodes, requiring waveform generators that emulate PCIe 6.0 and USB4 Version 2.0 lanes at 64 GT-s and 80 Gb-s. Taiwan- and South Korea-based fabs installed multi-channel platforms supporting femtosecond-level coherence across 8 or 16 outputs to validate die-to-die chiplet links. Because any delay in delivery stalls billion-dollar product launches, lead times for high-end units stretched beyond six months. North American and European design houses also need short-lived prototypes before committing to tape-out, so demand concentrates in the 0-to-2-year window, underpinning the short-term growth outlook.

Capital Spending Freezes at Mid-Tier Device OEMs

Component inflation and soft consumer demand narrowed margins at many mid-tier manufacturers, prompting 38% of surveyed firms to postpone waveform-generator upgrades planned for 2026. These customers extended legacy-instrument life through firmware patches and third-party calibration, depressing mid-range unit shipments even as high-end backlogs swelled. Vendors now offer leasing and pay-per-use lab access, but data-sovereignty and latency concerns confine uptake to non-critical tasks. The impact should ease within two years once macro visibility improves.

Other drivers and restraints analyzed in the detailed report include:

- Quantum-Computing Demand for Ultra-Channel Pulse Control

- Automotive Radar Systems Migrating Beyond 77 GHz

- Lack of Skilled Operators for Ultra-Fast Gear

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Direct digital synthesis held 55.22% revenue share in 2025, benefiting from deterministic phase control and spurious-free dynamic range beyond 80 dBc, attributes vital for coherent-optical modulation and qubit manipulation. This dominance reinforced the arbitrary waveform generator market size leadership of the segment, yet combined architectures are projected to expand at a 9.10% CAGR because they merge variable-clock agility with RF precision in a single chassis.

Variable-clock models remain relevant where sample-rate flexibility outweighs phase coherence, for example when mimicking irregular sensor outputs or generating pulse-width-modulation signals for power electronics. IEEE 1658 revisions favor direct digital synthesis on dynamic-linearity metrics, but Zurich Instruments' hybrid platform illustrates how vendors can bridge use cases without forcing labs to purchase multiple boxes, protecting adoption across mixed-signal environments.

Dual-channel units captured 60.22% share in 2025 and are forecast to grow at a 10.20% CAGR. Their ability to drive I-Q modulators or dual-polarization photonics transceivers cements their lead, and falling cost premiums encourage even cost-sensitive labs to adopt two outputs. Keysight's flagship 65 GS-s model became the benchmark reference for coherent-optical research, illustrating how a single module can generate four baseband channels for 400 Gb-s links, thereby raising the arbitrary waveform generator market share concentration within high-performance tiers.

Single-channel instruments still serve applications such as clock-jitter injection or university teaching labs, but their relevance erodes as integrated platforms like Liquid Instruments' 4-output device enter the sub-USD 20,000 price band. This democratization broadens adoption yet simultaneously cements dual-channel as the de facto baseline for mainstream RF and photonics validation.

Geography Analysis

In 2025, North America accounted for 36.82% of the revenue, driven by its well-established quantum-computing hubs, robust aerospace procurement activities, and the presence of leading semiconductor design houses. These factors collectively reinforce the region's dominant position in the arbitrary waveform generator market, ensuring its continued leadership. The region's advanced technological infrastructure and strong R&D capabilities further contribute to its market strength.

Meanwhile, the Asia-Pacific region is projected to grow at a notable 10.67% CAGR, fueled by significant investments from countries such as China, South Korea, and Japan. These nations are focusing on developing domestic semiconductor fabrication facilities (fabs) and establishing 6G research clusters, which are expected to drive substantial growth in the region. This strategic focus on innovation and infrastructure development is gradually shifting the center of volume growth toward the east.

Europe maintains a solid foundation in the market, supported by Germany's expertise in automotive radar technologies and the European Union's funding for photonics projects. These initiatives underscore the region's commitment to technological advancement and its ability to sustain a competitive edge. On the other hand, South America and the Middle East, while still in the early stages of market development, are emerging as strategically important regions. They are poised to play a critical role in future applications such as smart-city projects and satellite backhaul systems, which are expected to gain traction in the coming years.

- Keysight Technologies

- Tektronix Inc.

- Rohde & Schwarz GmbH & Co KG

- Tabor Electronics Ltd.

- Active Technologies Srl

- Berkeley Nucleonics Corporation

- Zurich Instruments AG

- National Instruments Corporation

- Siglent Technologies

- B&K Precision Corporation

- Teledyne LeCroy Inc.

- Anritsu Corporation

- Rigol Technologies Co., Ltd.

- Liquid Instruments Pty. Ltd.

- Pico Technology Ltd.

- GW Instek (Good Will Instrument Co., Ltd.)

- Spectrum Instrumentation GmbH

- GaGe (DynamicSignals LLC)

- Yokogawa Electric Corporation

- Stanford Research Systems Inc.

- OPAL-RT Technologies Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Complexity of 5G/6G RF Signal Testing

- 4.2.2 High-Resolution DACs Becoming Industry Standard

- 4.2.3 Automotive Radar Systems Shifting Beyond 77 GHz

- 4.2.4 Semiconductor Rapid Prototyping and ATE Growth

- 4.2.5 Quantum Computing Demands Ultra-Channel Pulse Control

- 4.2.6 Adoption of Photonic-Integrated AWGs for Optical I/O

- 4.3 Market Restraints

- 4.3.1 Capital Spending Freezes at Mid-Tier Device OEMs

- 4.3.2 Lack of Skilled Operators for Ultra-Fast Gear

- 4.3.3 Rising Competition from Vector Signal Generators

- 4.3.4 Uncertainty Around Cryogenic IC Development

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value / Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Direct Digital Synthesis AWG

- 5.1.2 Variable-Clock AWG

- 5.1.3 Combined AWG

- 5.2 By Product

- 5.2.1 Single-Channel

- 5.2.2 Dual-Channel

- 5.3 By Frequency Range

- 5.3.1 Up to 1 GHz

- 5.3.2 Above 1 GHz to 5 GHz

- 5.3.3 Above 5 GHz

- 5.4 By End-User Industry

- 5.4.1 IT and Telecommunications

- 5.4.2 Aerospace and Defense

- 5.4.3 Electronics and Semiconductor

- 5.4.4 Automotive

- 5.4.5 Healthcare

- 5.4.6 Education and Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Russia

- 5.5.2.6 Rest of Europe

- 5.5.3 South America

- 5.5.3.1 Brazil

- 5.5.3.2 Argentina

- 5.5.3.3 Rest of South America

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Kuwait

- 5.5.5.4 Bahrain

- 5.5.5.5 Turkey

- 5.5.5.6 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Keysight Technologies

- 6.4.2 Tektronix Inc.

- 6.4.3 Rohde & Schwarz GmbH & Co KG

- 6.4.4 Tabor Electronics Ltd.

- 6.4.5 Active Technologies Srl

- 6.4.6 Berkeley Nucleonics Corporation

- 6.4.7 Zurich Instruments AG

- 6.4.8 National Instruments Corporation

- 6.4.9 Siglent Technologies

- 6.4.10 B&K Precision Corporation

- 6.4.11 Teledyne LeCroy Inc.

- 6.4.12 Anritsu Corporation

- 6.4.13 Rigol Technologies Co., Ltd.

- 6.4.14 Liquid Instruments Pty. Ltd.

- 6.4.15 Pico Technology Ltd.

- 6.4.16 GW Instek (Good Will Instrument Co., Ltd.)

- 6.4.17 Spectrum Instrumentation GmbH

- 6.4.18 GaGe (DynamicSignals LLC)

- 6.4.19 Yokogawa Electric Corporation

- 6.4.20 Stanford Research Systems Inc.

- 6.4.21 OPAL-RT Technologies Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment