|

시장보고서

상품코드

2062271

자가 검사 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2025-2031년)Self-testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2031) |

||||||

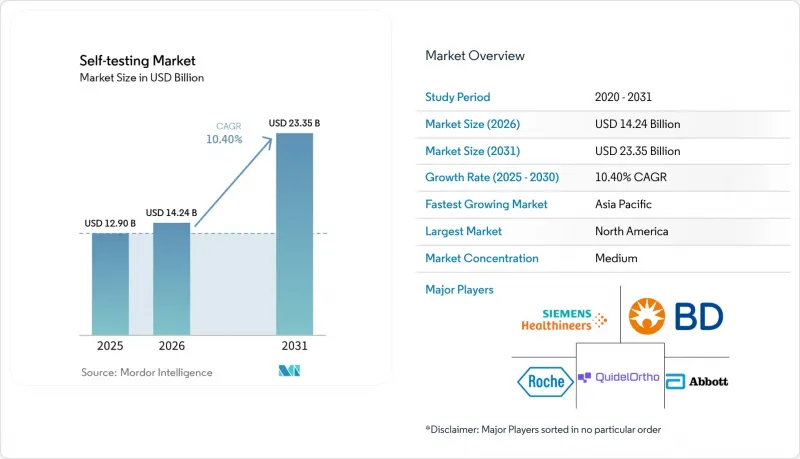

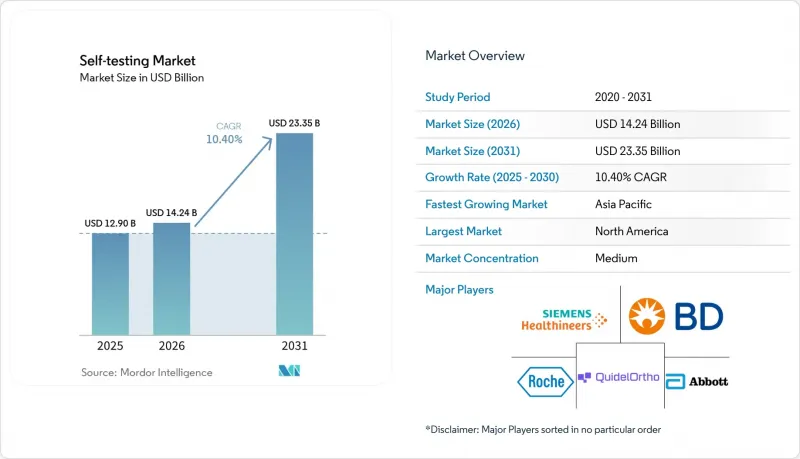

Mordor Intelligence에 의하면, 자가 검사 시장 규모는 2025년 129억 달러로 평가되었고, 2026년에는 142억 4,000만 달러로 추정되고, 2026-2031년 CAGR 10.40%로 성장을 지속할 전망이며, 2031년까지 233억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 검사 유형별(혈당 검사, 임신 및 불임 검사 등), 검체 유형별(혈액, 소변, 타액 등), 판매 채널별(소매 약국 및 드럭스토어, 온라인 약국 및 DTC 웹사이트, 슈퍼마켓 및 하이퍼마켓 등) 및 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 자가 검사 시장 동향 및 인사이트

포스트 코로나 시대에 재택 진단에 대한 소비자의 수용이 급격히 확대되고 있습니다.

팬데믹으로 인한 봉쇄 조치 이후의 행동 변화가 지속되고 있어, 일상적인 건강 관련 의문에 대한 첫 번째 선택지로 자가 검사가 선호되고 있습니다. 시판되는 항원 검사 키트를 통해 가정에서의 검체 채취가 보편화되었고, 재택치료 프로그램에 대한 만족도도 여전히 높은 만큼, 의료 시스템은 원격 의료를 우선으로 하는 진료 경로의 확대를 추진하고 있습니다. 연결된 래터럴 플로우 방식 리더기는 타임스탬프가 포함된 검사 결과를 임상의에게 전송하여, 대면 진료 없이도 처방 업무 흐름을 지원합니다. 원격 모니터링용 메디케어 청구 코드가 의사들의 도입을 촉진하고 있으며, 대형 약국 체인점에서는 여러 질환에 대응하는 자가 검사 키트 전용 매대를 마련하고 있습니다. 이러한 변화로 인해 대사, 감염증, 호르몬 관련 검사 패널에 대한 지속적인 수요가 자리 잡고 있습니다.

당뇨병 및 만성 질환의 부담이 커짐에 따라, 잦은 자가 모니터링이 권장되고 있습니다.

세계적으로 2형 당뇨병 환자가 증가함에 따라, 손가락 채혈용 혈당 측정 스트립과 새롭게 등장한 연속 혈당 모니터링(CGM) 기기에 대한 지속적인 수요가 발생하고 있습니다. 애보트의 ‘Lingo’ 센서는 인슐린 조절보다는 생활 습관 지도를 원하는 점점 늘어나는 당뇨병 전단계 환자층을 대상으로 하고 있습니다. 혈당 측정 외에도, 가정용 지질, 신장 기능, 응고 검사 키트가 심혈관 질환 및 신장 질환의 적극적인 관리를 뒷받침하고 있습니다. 인구 고령화에 따라 다중 질환을 동시에 앓는 환자가 증가하고 있으며, 진료 지침에서도 내원 기간 사이에 환자 주도로 검사를 실시하는 것이 점점 더 권장됨에 따라, 판매량은 장기적으로 꾸준히 증가하고 있습니다.

정확도와 위음성 결과에 대한 우려로 인해 임상 도입이 제한되고 있습니다.

가정용 항원 검사 키트와 집중 관리형 PCR 검사 간의 민감도 차이로 인해, 임상의는 확인 검사를 의뢰하게 되어 진단 과정이 장기화되고, 완전한 대체가 어려워지고 있습니다. 시료량 부족 등 분석 전 단계의 오류가 불일치의 대부분을 차지하고 있지만, 사용자를 위한 교육 자료는 여전히 일관성이 부족합니다. 규제 당국의 시판 후 조사에서는 중대한 이상반응이 확인되고 있지만, 실제 임상 현장에서 발생하는 사소한 오류가 의사의 신뢰를 지속적으로 훼손하고 있으며, 특히 복잡한 다항목 검사 패널에서 이러한 현상이 두드러집니다.

부문별 분석

혈당 측정 키트는 2025년 매출의 41.8%를 차지했으며, 자가 검사 시장 규모에서 가장 큰 기여 요인으로 작용하고 있습니다. 강력한 보험 적용, 내장된 치료 지침, 그리고 마이크로 샘플링 스트립부터 공장 보정된 CGM에 이르기까지의 지속적인 혁신이 이러한 우위를 확고히 하고 있습니다. 디지털 플랫폼은 현재 행동 변화를 유도하는 ‘너지’ 기능을 제공하며, 가치의 중심을 소모품에서 데이터 서비스로 전환하고 있습니다.

조상 및 건강 특성에 대한 지식에 대한 소비자의 관심이 높아지면서 유전자 자가 검사가 연평균 성장률(CAGR) 11.8%를 기록하며 성장하고 있으며, 이는 전체 검사 패널 중 가장 빠른 성장 속도입니다. 시퀀싱 비용의 감소로 다유전자 검사 보고서가 가능해졌으며, 타액 채취를 통해 물류 과정이 간소화되었습니다. 종양학 네트워크와의 업계 제휴를 통해 유전성 암 선별 검사 키트가 약국의 일반 진열대에 진열될 수 있는 체계가 마련됨에 따라, 자가 검사 시장 내 점유율이 더욱 확대될 것으로 전망됩니다. 안정적인 임신 검사 키트의 매출, RSV 및 인플루엔자를 대상으로 한 호흡기 검사 패널의 재출시, 그리고 스마트폰의 비색 측정 기술을 활용한 콜레스테롤 검사 키트가 제품 라인업을 더욱 풍성하게 하고 있습니다. 각 부문은 소매 브랜드의 다양화로 인해 혜택을 보고 있지만, 현재 매출 규모 면에서 혈당 검사에 필적할 만한 부문은 아직 없습니다.

지역별 분석

북미의 매출 점유율 49.7%는 만성 질환용 의료용품에 대한 보험 급여의 일관성, 원격 의료 청구 시스템의 조기 도입, 그리고 커넥티드 진단을 촉진하는 높은 스마트폰 보급률에 기인합니다. OTC(일반의약품) 매독 검사 키트 및 인플루엔자/코로나19 복합 검사 키트에 대한 FDA 승인은 규제 유연성을 보여주고 있으며, 원격 생리학적 모니터링 코드에 대한 지불 기관 측의 정책적 지지는 해당 서비스의 지속적인 이용을 뒷받침하고 있습니다.

아시아태평양의 자가 검사 시장은 2031년까지 연평균 성장률(CAGR) 12.8%로 확대될 것으로 예상되며, 이는 모든 지역을 웃도는 성장 속도입니다. 도시 지역의 중산층이 성장함에 따라, 의사 부족 문제를 해결하기 위해 원격 진료를 장려하는 각국의 e-헬스 구상과 맞물려 발전하고 있습니다. 일본, 한국, 호주의 정부는 원격의료와 관련된 검사에 대해 신속한 심사를 진행하고 있으며, 디지털 지갑의 보급률 상승은 소비자에 대한 직접 판매를 용이하게 하고 있습니다. 공급망 현지화 노력은 수입 의존도를 더욱 낮추고, 국내 제조에 대한 투자를 촉진하고 있습니다.

유럽은 시장 규모가 크지만, 상환 제도의 분절화라는 과제에 직면해 있습니다. 체외진단용 의료기기 규정(IVDR)에 따라 안전 기준은 통일되어 있지만, 비용 대비 효과에 대한 각 보험사 간의 논의로 인해 국가별 시장 출시가 지연되고 있습니다. 그러나 친환경 조달 규정에 따라, 해당 지역은 지속가능성을 중시하는 제품 재설계의 선도자로서의 입지를 확고히 하고 있습니다.

라틴아메리카와 중동 및 아프리카는 모두 낮은 수준에서 일제히 성장하고 있습니다. 브라질과 사우디아라비아에서 진행된 시범 프로그램에서는 약국 내에 설치된 원격 진료 부스에서 신속 항원 검사를 실시하고 있으며, 이는 지역 사회에 뿌리를 둔 혁신의 한 사례로 꼽히고 있습니다. 그러나 보험 적용 범위의 제한과 수입 관세로 인해 성장 속도가 둔화되고 있어, 다국적 기업들은 경제 현대화 노력에 발맞추어 단계적으로 사업을 전개할 수밖에 없는 실정입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the self-testing market size is expected to grow from USD 12.90 billion in 2025 to USD 14.24 billion in 2026 and is forecast to reach USD 23.35 billion by 2031 at 10.40% CAGR over 2026-2031.

This report is Segmented by Test Type (Blood Glucose Tests, Pregnancy & Fertility Tests, and More), Sample Type (Blood, Urine, Saliva, and More), Distribution Channel (Retail Pharmacies & Drug Stores, Online Pharmacies & DTC Websites, Supermarkets/Hypermarkets, and More), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Self-testing Market Trends and Insights

Explosion of Post-COVID Consumer Acceptance of Home Diagnostics

Sustained behavioral change following pandemic lockdowns keeps home testing the preferred first step for everyday health queries. Over-the-counter antigen kits familiarized households with sample collection, and satisfaction scores from hospital-at-home programs remain high, prompting health systems to expand remote-first care pathways. Connected lateral-flow readers now transmit time-stamped results to clinicians, supporting prescription workflows without in-person visits. Medicare billing codes for remote monitoring reinforce physician adoption, and major pharmacy chains curate dedicated aisles for multi-condition self-tests. These shifts anchor recurring demand across metabolic, infectious, and hormonal panels.

Rising Diabetes & Chronic-Disease Burden Prompting Frequent Self-Monitoring

Global escalation of type 2 diabetes creates continuous need for finger-stick glucose strips and emerging continuous glucose monitors (CGMs). Abbott's Lingo sensor targets an expanding pre-diabetic population that seeks lifestyle guidance rather than insulin titration. Beyond glycemia, at-home lipid, renal and coagulation kits support proactive management of cardiovascular and renal conditions. Population aging amplifies multi-morbidities, and clinical guidelines increasingly endorse patient-initiated testing between clinic visits, sustaining long-term volume growth.

Accuracy & False-Negative Concerns Limiting Clinical Adoption

Sensitivity gaps between home antigen kits and centralized PCR assays prompt clinician requests for confirmatory testing, prolonging diagnostic pathways and dampening full substitution. Pre-analytic errors-such as insufficient sample volume-represent the majority of discrepancies, yet user education materials remain inconsistent. While regulatory post-market surveillance captures serious adverse events, real-world nuisance errors continue to erode physician confidence, particularly for complex multi-analyte panels.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Relaxation for OTC/At-Home Test Approvals in Key Markets

- Smartphone-Linked LFA Readers Enabling Tele-Consult Billing

- Fragmented Reimbursement & Regulatory Complexity Across Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blood-glucose kits captured 41.8% of 2025 revenue, making them the largest contributor to the self-testing market size. Strong insurance coverage, embedded care guidelines and continuous innovation-ranging from micro-sampling strips to factory-calibrated CGMs-consolidate this lead. Digital platforms now overlay behavior-change nudges, shifting value from consumables to data services.

Growing consumer appetite for ancestry and health-trait insights propels genetic self-tests at an 11.8% CAGR, the fastest pace among all panels. Lower sequencing costs allow multi-gene reporting, and saliva collection simplifies logistics. Industry partnerships with oncology networks position hereditary cancer screens for mainstream pharmacy shelves, signaling further share expansion within the self-testing market. Steady pregnancy-test turnover, a relaunch of respiratory panels targeting RSV and flu, and cholesterol kits leveraging smartphone colorimetry round out the menu. Each category benefits from retail brand diversification, yet none rival the scale of glucose in present-day sales.

Geography Analysis

North America's 49.7% revenue share derives from reimbursement alignment for chronic-disease supplies, early adoption of telehealth billing, and high smartphone ownership that facilitates connected diagnostics. FDA clearances of OTC syphilis and combo flu/COVID-19 kits underscore regulatory agility, while payer policy endorsements for remote physiologic monitoring codes underpin usage continuity.

The Asia Pacific self-testing market is projected to expand at 12.8% CAGR through 2031, outpacing all regions. Urban middle-class growth intersects with national e-health blueprints that incentivize remote diagnostics to combat physician shortages. Governments in Japan, South Korea, and Australia grant accelerated review to telehealth-linked tests, and rising digital-wallet penetration eases direct-to-consumer sales. Supply-chain localization initiatives further reduce import dependency, spurring domestic manufacturing investments.

Europe holds meaningful volume but confronts fragmented reimbursement. While the In Vitro Diagnostics Regulation harmonizes safety standards, individual payer debates over cost-effectiveness prolong country-by-country launches. Green-procurement rules, however, position the region as a leader in sustainability-driven product redesign.

Latin America, the Middle East and Africa collectively advance from low bases. Pilot programs in Brazil and Saudi Arabia couple rapid antigen tests with tele-consult stalls inside pharmacies, illustrating localized innovation. Yet limited insurance coverage and import tariffs temper acceleration, leaving multinational corporations to pursue phased rollouts aligned with economic modernization efforts.

- Abbott Laboratories

- Roche

- Siemens Healthineers

- QuidelOrtho

- Beckton Dickinson

- Thermo Fisher Scientific

- Danaher Corp. (Cepheid)

- Bio-Rad Laboratories

- Orasure Technologies

- Everlywell Inc.

- LetsGetChecked

- Cue Health

- Acon Laboratories

- Access Bio

- Mylab Discovery Solutions

- Arkray

- Bionime

- Genomex (23andMe)

- Chembio Diagnostics

- Binx Health

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion Of Post-COVID Consumer Acceptance Of Home Diagnostics

- 4.2.2 Rising Diabetes & Chronic-Disease Burden Prompting Frequent Self-Monitoring

- 4.2.3 Regulatory Relaxation For OTC/At-Home Test Approvals In Key Markets

- 4.2.4 Smartphone-Linked LFA Readers Enabling Tele-Consult Billing

- 4.2.5 Employer-Sponsored Wellness Testing Programs Expanding Access

- 4.2.6 Self-Collected Specimens Driving Faster Antiviral Prescriptions Via Telehealth

- 4.3 Market Restraints

- 4.3.1 Accuracy & False-Negative Concerns Limiting Clinical Adoption

- 4.3.2 Fragmented Reimbursement & Regulatory Complexity Across Regions

- 4.3.3 Data-Privacy Risks From Cloud-Connected Home Tests

- 4.3.4 Environmental Waste From Single-Use Plastic Test Kits

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Test Type

- 5.1.1 Blood Glucose Tests

- 5.1.2 Pregnancy & Fertility Tests

- 5.1.3 Infectious Disease Tests (HIV, COVID-19, Flu, etc.)

- 5.1.4 Cholesterol & Lipid Tests

- 5.1.5 Genetic & Ancestry Tests

- 5.2 By Sample Type

- 5.2.1 Blood

- 5.2.2 Urine

- 5.2.3 Saliva

- 5.2.4 Nasal / Throat Swab

- 5.2.5 Other Specimens (Stool, Hair, etc.)

- 5.3 By Distribution Channel

- 5.3.1 Retail Pharmacies & Drug Stores

- 5.3.2 Online Pharmacies & DTC Websites

- 5.3.3 Supermarkets / Hypermarkets

- 5.3.4 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abbott Laboratories

- 6.3.2 F. Hoffmann-La Roche AG

- 6.3.3 Siemens Healthineers

- 6.3.4 QuidelOrtho Corporation

- 6.3.5 Becton, Dickinson and Company

- 6.3.6 Thermo Fisher Scientific Inc.

- 6.3.7 Danaher Corp. (Cepheid)

- 6.3.8 Bio-Rad Laboratories

- 6.3.9 OraSure Technologies

- 6.3.10 Everlywell Inc.

- 6.3.11 LetsGetChecked

- 6.3.12 Cue Health Inc.

- 6.3.13 ACON Laboratories

- 6.3.14 Access Bio Inc.

- 6.3.15 Mylab Discovery Solutions

- 6.3.16 ARKRAY Inc.

- 6.3.17 Bionime Corporation

- 6.3.18 Genomex (23andMe)

- 6.3.19 Chembio Diagnostics

- 6.3.20 Binx Health

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment