|

시장보고서

상품코드

2062277

부직포 여과 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Nonwoven Filtration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

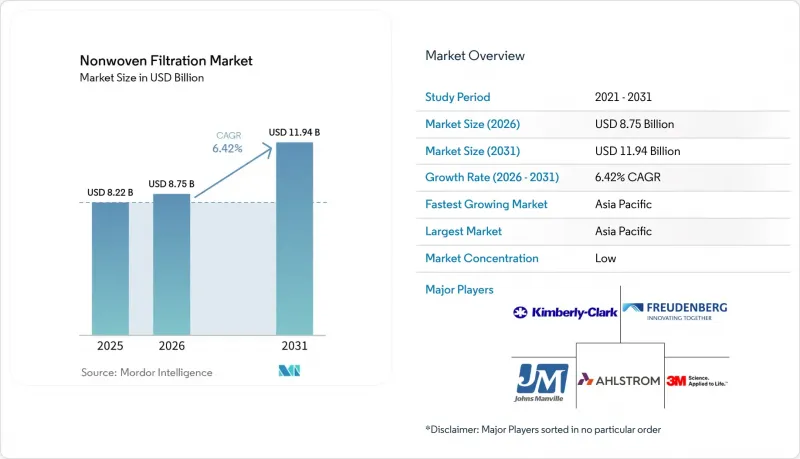

Mordor Intelligence에 의하면, 부직포 여과 시장 규모는 2025년 82억 2,000만 달러에서 2026년에는 87억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 6.42%로 성장을 지속하여, 2031년에는 119억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 부직포의 유형(스펀본드, 멜트블로운 등), 여과 유형(공기 여과, 액체 여과, HVAC 시스템, 자동차, 기타), 용도(수처리·폐수처리, 산업용 등), 최종 사용자(산업용, 상업용 등), 지역(아시아태평양, 북미, 유럽 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 부직포 여과 시장 동향과 인사이트

급속한 도시화가 HVAC 및 실내 공기질(IAQ) 수요를 촉진하고 있습니다.

2025년에 아시아 및 중동의 여러 관할 구역에서 채택된 개정판 ASHRAE 62.1 환기율에 따라, 상업시설의 기준으로 MERV 13이 의무화됨에 따라 건물 소유주는 기존의 거친 필터를 더 자주 교체해야만 하게 되었습니다. 2025년 시점에서 이미 전 세계 전력 소비량의 약 2%를 차지하는 데이터센터 사업자들은 팬의 전력 소비를 줄이기 위해 저압력 손실의 주름형 부직포를 표준화하고 있으며, 스펀본드 기판에 일렉트로스핀 가공을 적용한 오버레이를 선호하여 채택하고 있습니다. 북미 전역에서 유틸리티자가 자금을 지원하는 주택 개보수 환급 제도 덕분에 필터 교체 주기가 기존 5년에서 약 3년으로 단축되었습니다. 새로운 하우징에 내장된 IoT 압력 센서를 통해 예측 유지보수가 가능해졌으며, 분진 부하 조건에서도 선형적인 압력 상승 곡선을 보장하는 공급업체가 높은 평가를 받고 있습니다.

팬데믹 이후 의료 및 제약 클린룸 시장의 성장

mRNA 백신 생산 라인과 바이오시밀러 생산 시설이 가동을 시작함에 따라, 2024년부터 2025년까지 전 세계 무균 충전 능력은 35% 확대되었습니다. 이와 동시에 병원 내 HEPA 및 ULPA 필터의 설치도 증가했으며, 수술실과 중환자실에는 H14 터미널 필터가 도입되었습니다. 2026년 3월, MANN+HUMMEL사는 노스캐롤라이나주 윌슨에 레벨 7 클린룸을 개설하고, OEM 계약을 위한 의약품 등급 미디어의 검증을 시작했습니다. 미국 FDA 및 EMA의 엄격한 입자 수 제한으로 인해 충전 및 마무리 모듈의 업스트림에 0.2미크론 절대 여과 카트리지를 설치해야 하는 반면, 바이오의약품의 연속 생산으로 인해 장기간의 제조 공정에서도 중단 없이 가동할 수 있는 일회용 심층 필터에 대한 수요가 증가하고 있습니다.

복합 미디어의 폐기 및 재활용에 따른 과제

활성탄 라미네이트 부직포는 기존의 재활용 공정으로는 경제적으로 분리할 수 없습니다. 또한, 사용 후 필터를 수거하는 유럽의 시멘트 소성로에서는 전처리 비용으로 톤당 40-60달러가 청구됩니다. 새로운 용융 여과 회수 시스템에서는 다성분 웹의 경우 회수율이 65-70%에 그쳐, 단일 소재 스트림보다 훨씬 낮은 수준입니다. 프랑스와 독일의 확대 생산자 책임(EPR) 규정에 따라 제조업체는 사용 후 필터를 회수해야 할 의무가 있지만, 지방 지역의 물류 체계는 아직 미비한 상태이며, 그 결과 매립 처리에 대한 의존도가 높아지고 있습니다. ISO나 ASTM에 의한 통일된 재활용 가능성 기준의 부재는 설계상의 불확실성과 규정 준수 비용을 증가시키고 있습니다.

부문별 분석

스펀본드 부직포는 2025년 매출의 35.57%를 차지하며, 부직포 여과 시장에서 가장 큰 매출 비중을 차지하고 있습니다. 한편, 일렉트로스펀 부직포 시장은 2031년까지 연평균 성장률(CAGR) 6.79%로 성장할 것으로 전망됩니다.

팬데믹 기간 중 건설된 멜트블로운 생산 라인의 이익률 압박으로 인해, 아시아 기업들은 생산 능력을 유휴 상태로 두거나 배터리 분리막 생산으로 전환하는 움직임을 보이고 있습니다. 스펀본드 기재와 일렉트로스펀 층을 적층한 복합 구조는 주름의 강성을 유지하면서도 HEPA 등급과 ULPA 등급 간의 성능 격차를 좁혀줍니다. HIFYBER사와 Espin Nanotech사가 입증한, 나노섬유의 직경을 50-500 nm까지 축소하는 기술 혁신을 통해, 공급업체는 기존 HEPA에 비해 30-40% 낮은 압력 손실로 PM0.3에 대한 99.97%의 포집 효율을 달성할 수 있게 되어, 프리미엄 시장이 강화되고 있습니다. 역삼투막의 지지층에 0.04 dtex까지 미세화된 마이크로파이버를 사용한 습식 성형 합성섬유가 채택된 것은 특수한 제조 공정이 고생산성의 스펀본드 플랫폼과 공존해 나갈 것임을 보여주는 또 다른 징후입니다.

부직포 여과 시장 점유율 구성에서 2025년 매출액에서 공기 여과가 차지하는 비중은 50.22%로 압도적인 위치를 유지했으나, 액체 여과는 2031년까지 연평균 성장률(CAGR) 6.90%로 가장 빠르게 성장하고 있습니다. 2025년 3월 도레이의 한외여과 제품 출시와 2026년 3월 듀폰의 나노여과 기술 업그레이드는 지자체 재이용 프로젝트에서 공급업체들이 저에너지화와 오염(막힘) 저감에 주력하고 있음을 보여줍니다.

냉각탑 루프를 업그레이드하는 산업용 가공업체나 PFAS를 단계적으로 폐지하고 있는 식품 및 음료 공장은 현재, 스펀본드 프리필터와 나노파이버 폴리셔 단계를 결합한 다층 카트리지 트레인을 주문하고 있습니다. 반도체 제조 공장을 위한 하이브리드형(입자+분자) 필터는 부직포 주름에 가스 흡착층을 결합함으로써, 기존의 ‘공기’와 ‘액체’의 경계를 모호하게 만듭니다. 그 결과, 크로스 플랫폼 제품 포트폴리오를 보유한 공급업체는 번들 솔루션을 업셀링하여 부직포 여과 시장에서 설치당 평균 매출을 높일 수 있습니다.

지역별 분석

아시아태평양은 2025년 매출의 39.97%를 차지해, 2031년까지 연평균 성장률(CAGR) 7.12%로 성장할 것으로 전망됩니다. 중국의 반도체 자급화 추진에 따라 새로운 일렉트로스피닝 및 멜트블로우 생산 라인에 대한 투자가 진행되고 있는 반면, 인도에서는 생산 능력이 연간 1만 8,740톤으로 확대되어 급증하는 HVAC 및 캐빈 필터 수요를 충족시키고 있습니다.

북미와 유럽은 성숙한 교체용 필터 시장을 형성하고 있지만, PM2.5 규제 및 건축물 에너지 효율 관련 지침의 강화로 인해 한 자릿수 중반대의 성장이 예상됩니다. Avgol사의 1억 달러 규모 노스캐롤라이나주 스펀본드 공장과 MANN+HUMMEL사의 레벨 7 클린룸은 국내 생산 능력의 현지화에 대한 자신감을 보여주고 있습니다.

남미, 중동 및 아프리카는 매출 비중은 작지만, 브라질의 수처리 설비 교체, 아르헨티나 리튬 광산의 분진 대책, 사우디아라비아의 클린룸 구역, 그리고 관광용 Off-grid 해수 담수화용 마이크로필터와 같은 분야에서 높은 성장이 기대되고 있습니다. 중국, 유럽, 북미에 집중된 배터리 재활용 역량으로 인해 미디어 공급업체들은 지역별 기술 지원 연구소를 설치할 수밖에 없게 되었으며, 이로 인해 부직포 여과 시장 전반에 걸친 서비스 연계가 강화되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

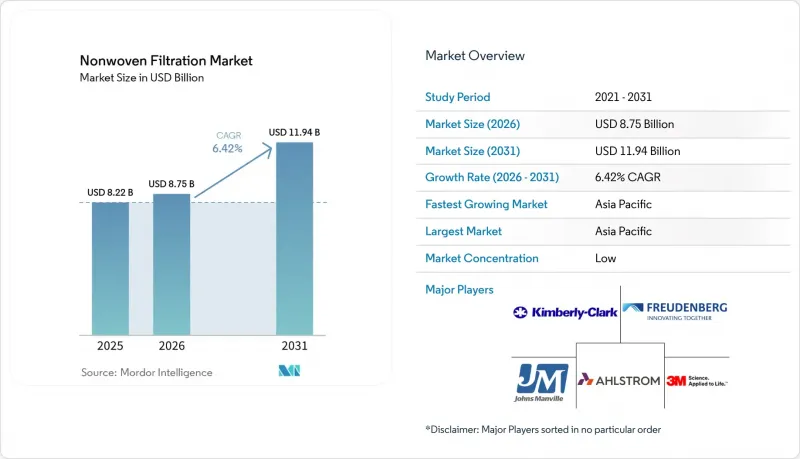

JHS 26.06.19According to Mordor Intelligence, the non-Woven filtration market size is expected to grow from USD 8.22 billion in 2025 to USD 8.75 billion in 2026 and is forecast to reach USD 11.94 billion by 2031 at 6.42% CAGR over 2026-2031.

This report is Segmented by Type of Nonwoven (Spunbond, Meltblown, and More), Filtration Type (Air Filtration, Liquid Filtration, HVAC Systems, Automotive, and Other Types), Application (Water and Waste-Water Treatment, Industrial, and More), End-User (Industrial, Commercial, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Nonwoven Filtration Market Trends and Insights

Rapid Urbanization Boosting HVAC and IAQ Demand

Revised ASHRAE 62.1 ventilation rates, adopted by several Asian and Middle-Eastern jurisdictions during 2025, now lock MERV 13 as the baseline for commercial sites, compelling building owners to replace legacy coarse filters more frequently. Data-center operators, already consuming roughly 2% of global electricity in 2025, are standardizing on low-pressure-drop pleated nonwovens to temper fan-energy draw, favoring electrospun overlays on spunbond carriers. Utility-funded residential retrofit rebates across North America are accelerating replacement cycles to roughly three years, down from five. Embedded IoT pressure sensors in new housings allow predictive maintenance, rewarding vendors that guarantee linear pressure-rise curves under dust loading.

Post-Pandemic Growth of Healthcare and Pharma Cleanrooms

Global aseptic-fill capacity expanded 35% between 2024 and 2025 as mRNA vaccine lines and biosimilar suites came online. HEPA and ULPA filter installations in hospitals rose in parallel, embedding H14 terminal filters in operating theaters and intensive-care wards. In March 2026, MANN+HUMMEL opened a Level 7 cleanroom in Wilson, North Carolina, to validate pharma-grade media for OEM contracts. Strict particle-count limits from both U.S. FDA and EMA now mandate 0.2-micron absolute cartridges upstream of fill-finish modules, while continuous biologics manufacturing pushes single-use depth-filter demand that can run uninterrupted for longer campaigns.

Disposal and Recycling Hurdles of Composite Media

Activated-carbon laminated nonwovens cannot be economically separated in traditional recycling lines, and European cement kilns that accept spent filters charge USD 40-60 per metric ton in pretreatment fees. New melt-filtration reclaim systems achieve only 65-70% yield with multi-component webs, well below mono-material streams. Extended producer responsibility rules in France and Germany now force manufacturers to collect end-of-life filters, but rural logistics remain undeveloped, increasing landfill reliance. Lack of harmonized ISO or ASTM recyclability standards adds design uncertainty and compliance cost.

Other drivers and restraints analyzed in the detailed report include:

- Data-Center Energy Mandates for Low-Pressure-Drop Filters

- Battery-Recycling Plants Needing Fine-Particle Filtration

- Regulatory Focus on Microfiber Shedding

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spunbond nonwoven delivered 35.57% of 2025 revenue and underpins the largest revenue tier of the nonwoven filtration market. Electro-spun nonwoven, however, is projected to advance at a 6.79% CAGR through 2031.

Margin pressure on melt-blown lines built during the pandemic is prompting Asian firms to idle or repurpose capacity toward battery separators. Composite constructions that laminate spunbond backers with electrospun layers are narrowing the performance gap between HEPA and ULPA classes while preserving pleat stiffness. Breakthroughs that cut nanofiber diameters to 50-500 nm, demonstrated by HIFYBER and Espin Nanotech, let suppliers hit 99.97% PM0.3 efficiency at 30-40% lower pressure drop than conventional HEPA, strengthening the premium tier. Adoption of wet-laid synthetics with microfibers down to 0.04 dtex in reverse-osmosis support layers is another sign that specialty processes will coexist with high-output spunbond platforms.

Air filtration maintained a commanding 50.22% share of 2025 revenue in the nonwoven filtration market share landscape, yet liquid filtration is accelerating fastest at a 6.90% CAGR through 2031. Toray's ultrafiltration launch in March 2025 and DuPont's March 2026 nanofiltration upgrade illustrate vendor focus on lower energy and fouling profiles for municipal reuse projects.

Industrial processors upgrading cooling-tower loops and food and beverage plants phasing out PFAS now order multi-layer cartridge trains that pair spunbond prefilters with nanofiber polisher stages. Hybrid particulate-plus-molecular filters for semiconductor fabs blur classical air versus liquid boundaries by embedding gas-adsorption layers into nonwoven pleats. Consequently, vendors with cross-platform portfolios can upsell bundled solutions, raising average sales per installation in the nonwoven filtration market.

Geography Analysis

Asia-Pacific held 39.97% of 2025 sales and is forecast to expand at a 7.12% CAGR through 2031. China's semiconductor self-sufficiency drive funds new electrospinning and melt-blown lines, while India's capacity surge to 18,740 tpa satisfies surging HVAC and cabin-filter demand.

North America and Europe form mature replacement markets, yet gain mid-single-digit lift from stricter PM2.5 and building-energy directives. Avgol's USD 100 million North Carolina spunbond plant and MANN+HUMMEL's Level 7 cleanroom demonstrate confidence in domestic capacity localization.

South America, and Middle-East and Africa contribute smaller revenues but see high-growth pockets in Brazilian water-treatment upgrades, Argentine lithium-mine dust control, Saudi cleanroom zones, and off-grid desalination micro-filters for tourism. Battery-recycling capacity, clustered in China, Europe, and North America, compels media suppliers to install regional tech-support labs, tightening service links across the nonwoven filtration market.

- 3M

- Ahlstrom

- DuPont

- Fibertex Nonwovens A/S

- Fitesa SA and Affiliates

- Freudenberg SE

- Hollingsworth and Vose

- Huvis Corp.

- Johns Manville

- KCWW

- Lydall, Inc.

- Mann+Hummel

- Parker Hannifin Corp

- Sandler AG

- TORAY INDUSTRIES, INC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid urbanisation boosting HVAC and IAQ demand

- 4.2.2 Post-pandemic growth of healthcare and pharma cleanrooms

- 4.2.3 Data-centre energy mandates for low-pressure drop filters

- 4.2.4 Battery-recycling plants needing fine-particle filtration

- 4.2.5 Off-grid tourist desalination micro-filters

- 4.3 Market Restraints

- 4.3.1 Disposal and recycling hurdles of composite media

- 4.3.2 Regulatory focus on microfiber shedding

- 4.3.3 Capital scarcity for AI retrofits at SME converters

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type of Nonwoven

- 5.1.1 Spunbond

- 5.1.2 Meltblown

- 5.1.3 Needle-punched

- 5.1.4 Composite

- 5.1.5 Electro-spun

- 5.1.6 Other Nonwoven Types (Wet-laid, Air-laid)

- 5.2 By Filtration Type

- 5.2.1 Air Filtration

- 5.2.2 Liquid Filtration

- 5.2.3 Other Types (Gas, Oil, Blood)

- 5.3 By Application

- 5.3.1 Water and Waste-water Treatment

- 5.3.2 Industrial (Manufacturing, Chemical, Power)

- 5.3.3 HVAC Systems

- 5.3.4 Automotive

- 5.3.5 Healthcare and Pharmaceuticals

- 5.3.6 Food and Beverage Processing

- 5.3.7 Electronics

- 5.3.8 Other Applications (Mining, Pulp and Paper)

- 5.4 By End-user

- 5.4.1 Industrial

- 5.4.2 Commercial

- 5.4.3 Residential

- 5.4.4 Municipal/Government

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Ahlstrom

- 6.4.3 DuPont

- 6.4.4 Fibertex Nonwovens A/S

- 6.4.5 Fitesa SA and Affiliates

- 6.4.6 Freudenberg SE

- 6.4.7 Hollingsworth and Vose

- 6.4.8 Huvis Corp.

- 6.4.9 Johns Manville

- 6.4.10 KCWW

- 6.4.11 Lydall, Inc.

- 6.4.12 Mann+Hummel

- 6.4.13 Parker Hannifin Corp

- 6.4.14 Sandler AG

- 6.4.15 TORAY INDUSTRIES, INC.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment